- Renewable Energy

- Hydrogen Market

Hydrogen Market Size, Share, Trends, and Growth Forecast, 2025 - 2032

Hydrogen Market By Product Type (Gray Hydrogen, Blue Hydrogen, Others), Technology (Steam Methane Reforming (SMR), Electrolysis, Others), Application (Energy, Mobility, Chemical & Refinery, Steel Manufacturing, Others), and Regional Analysis for 2025 - 2032

Hydrogen Market Size and Trends Analysis

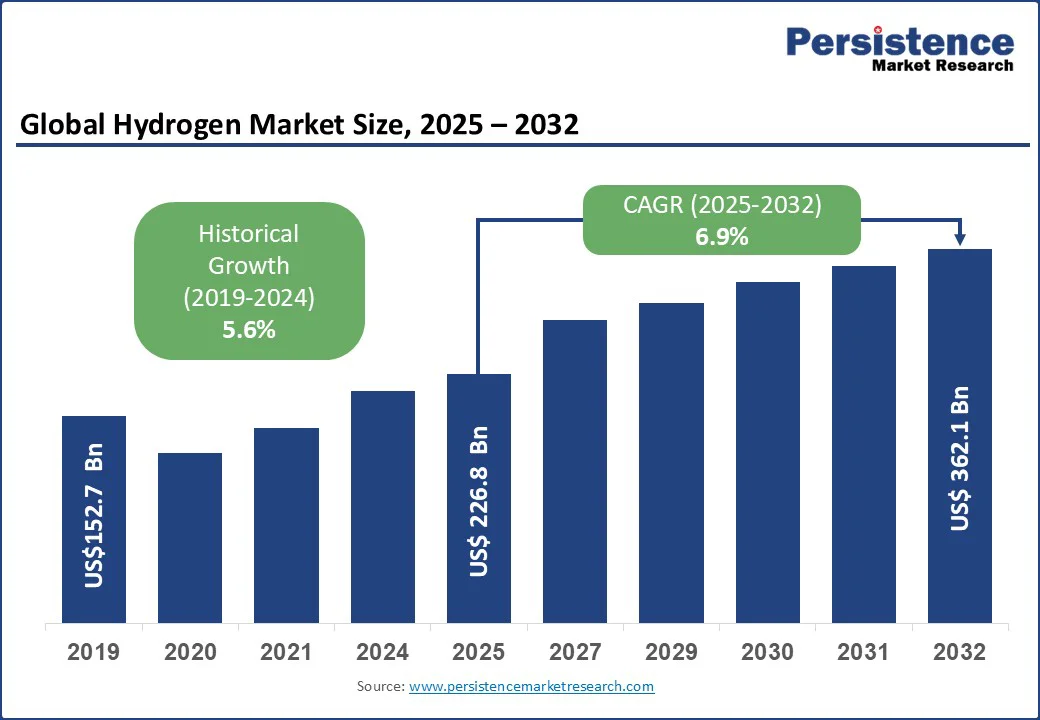

The global hydrogen market size is likely to value at US$226.8 Bn in 2025 and reach US$362.1 Bn by 2032 growing at a CAGR of 6.9% during the forecast period from 2025 to 2032.

Supportive government policies, decarbonization targets, and growing hydrogen infrastructure are accelerating large-scale adoption, and the market growth is driven by the rising adoption of low-emission and sustainable energy solutions across transportation, power generation, and industrial sectors.

Key Industry Highlights:

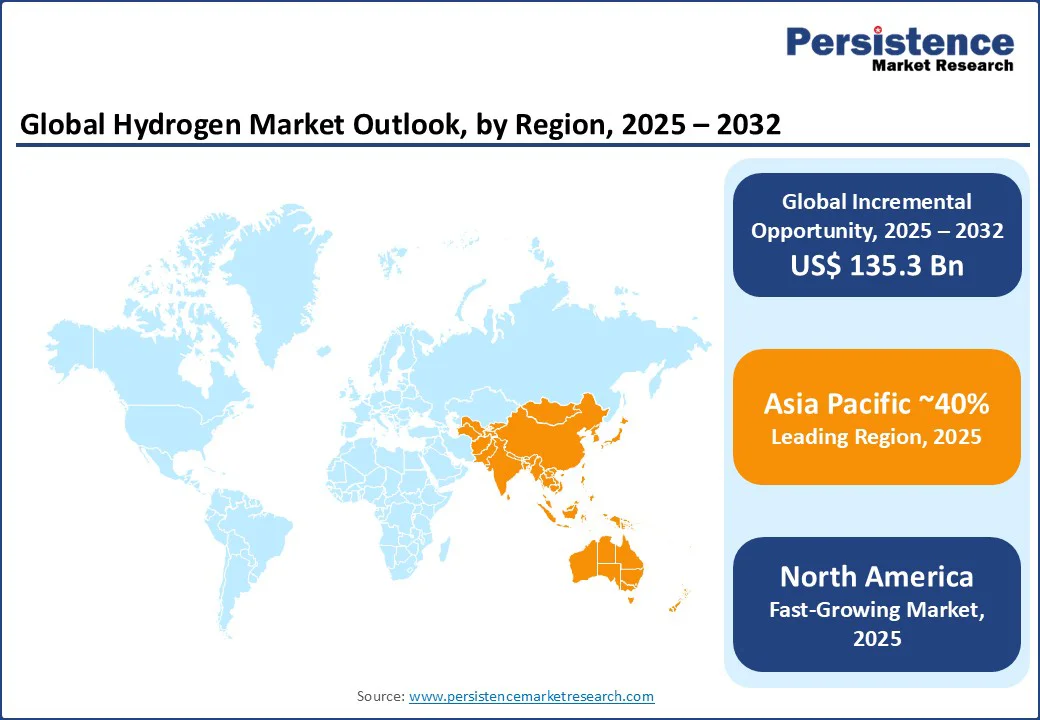

- Leading Region: Asia Pacific is anticipated to dominate with over 40% market share in 2025, driven by strong government policies, large-scale electrolyzer capacity, and leadership in hydrogen infrastructure and fuel cell deployment.

- Fastest-growing Region: North America is projected to be the fastest-growing region, fueled by DOE’s Hydrogen Energy Earthshot, IRA clean hydrogen tax credits, and US$750 Mn funding for R&D projects.

- Investment Plans: Major investments include Air Liquide and TotalEnergies’ US$1+ Bn partnership in the Netherlands for large-scale green hydrogen, and India’s National Green Hydrogen Mission targeting 5 Mt of renewable hydrogen by 2030.

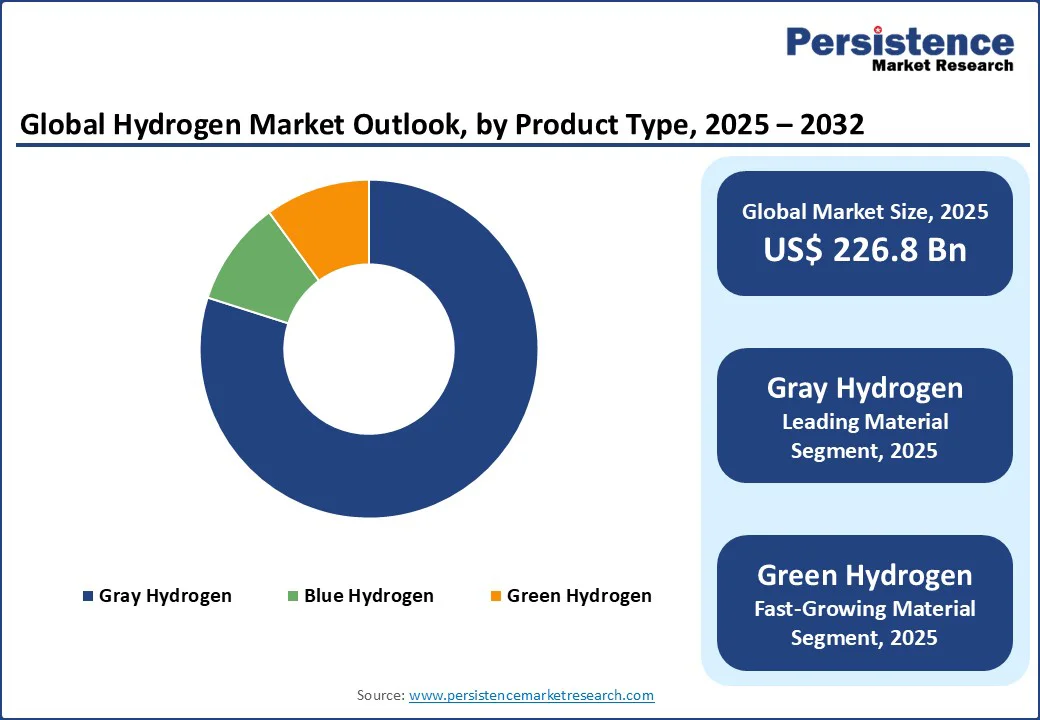

- Dominant Product Type Segment: Gray hydrogen is anticipated to account for over 95% of global production in 2025, due to low costs (US$1–2/kg) and reliance on steam methane reforming (SMR).

- Leading Application Segment: Mobility is expected to hold more than 30% revenue share in 2025, driven by hydrogen fuel cell vehicles (FCEVs), buses, trucks, and trains.

- Landmark Projects in Green Hydrogen: In 2025, ANDRITZ received an order for a 100 MW green hydrogen plant in Germany, while Air Liquide launched the 200 MW “ELYgator” electrolyzer in Rotterdam.

|

Global Market Attribute |

Key Insights |

|

Hydrogen Market Size (2025E) |

US$226.8 Bn |

|

Market Value Forecast (2032F) |

US$362.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Dynamics

Driver - Expanding Hydrogen Applications Across Industries and Supportive Government Initiatives

The hydrogen market is rapidly expanding as hydrogen emerges as a versatile clean energy carrier, driving the energy transition. Traditionally used in oil refining and ammonia production, hydrogen is now reshaping industries such as steel manufacturing, transportation, power generation, and residential heating.

In the steel industry, hydrogen is replacing coal in Direct Reduced Iron (DRI), with projects by Thyssenkrupp and ArcelorMittal targeting up to 95% CO2 reduction. In the fertilizer industry, companies such as Yara are producing green ammonia using renewable hydrogen, while hydrogen also plays a key role in methanol production. The refining sector continues to rely on hydrogen for desulfurization, transforming crude oil into cleaner fuels.

The hydrogen mobility sector is gaining momentum, led by fuel cell electric vehicles (FCEVs), particularly heavy-duty trucks, buses, and trains. According to the IEA, global FCEVs could exceed 15 million by 2040. Leading OEMs such as Toyota (Mirai) and Hyundai (NEXO, XCIENT trucks) are advancing hydrogen fuel cell vehicles, while StellarJet is pioneering solid-state hydrogen storage for aviation.

Government initiatives play a critical role, with policy frameworks, public funding, and regulatory initiatives accelerating production and infrastructure. National strategies across North America, Europe, and Asia Pacific, backed by public investment, play a major role in fostering large projects and R&D in key technologies. Tax breaks and carbon pricing also help make hydrogen more cost-competitive with fossil fuels.

Restraint - Energy Loss During Hydrogen Production

Hydrogen is a synthetic energy carrier, i.e., it stores energy generated from other sources rather than occurring naturally as a fuel. One common method of producing hydrogen is through alkaline electrolysis, where electrical energy is converted into hydrogen. This is not just the only stage where energy is consumed. Additional energy is required to compress, liquefy, transport, transfer, or store hydrogen after its production. In an ideal scenario, the energy used to produce hydrogen would equal the energy it contains, but this is rarely the case. Whether hydrogen is generated from electricity or through chemical reforming of hydrocarbons, energy transformations are involved.

During these processes, electrical or chemical energy is converted into chemical energy stored in hydrogen. Unfortunately, no energy conversion process is 100% efficient, resulting in inevitable energy losses. These losses reduce the overall energy efficiency of hydrogen production, posing a key challenge for the widespread adoption of hydrogen as a clean energy source.

Opportunity - Growing Emphasis on Advancing the Hydrogen-Based Economy

Governments around the world are increasingly expected to support hydrogen programs in the coming years as part of their strategies to achieve net-zero carbon emissions. Crafting the most effective green hydrogen strategy remains complex due to the wide range of decarbonization options available across different applications and industries. As innovation and technology evolve, the cost-effectiveness and benefits of these alternatives are likely to change. Consequently, countries are exploring technologies that align best with their national needs while being cautious not to adopt less efficient or outdated decarbonization routes.

The number of low-emission hydrogen project announcements continues to grow, but only 7% have taken firm investment decisions due to uncertainties around the future evolution of demand, the lack of clarity about certification and regulation, and the lack of infrastructure available to deliver hydrogen to end-users. On the demand side, hydrogen demand keeps growing, but remains concentrated in traditional applications. Novel applications in heavy industry and long-distance transport account for less than 0.1% of hydrogen demand, yet are projected to contribute nearly 40% by 2030 under the Net Zero Emissions by 2050 (NZE) Scenario.

Category-wise Analysis

Application Insights

The mobility segment is anticipated to dominate with a market revenue of more than 30% in 2025, fueled by government subsidies, grants, and global initiatives to cut carbon emissions. Hydrogen fuel cell vehicles (FCEVs) deliver long driving ranges, quick refueling, and zero tailpipe emissions, making them ideal for passenger cars, buses, and commercial trucks. The rising demand for clean public transport and sustainable logistics is further boosting hydrogen adoption, positioning it as the foundation of the global hydrogen economy and net-zero transition.

The market is gaining momentum, with major OEMs spearheading innovation. In April 2025, Hyundai launched the new NEXO, built on 27 years of fuel cell expertise, while the 2025 Toyota Mirai combines hydrogen and oxygen to produce clean power. Hyundai’s hydrogen brand HTWO is advancing large-scale projects to strengthen the hydrogen ecosystem. Similarly, BMW’s iX5 Hydrogen pilot fleet, launched in 2024, highlights automakers’ strong commitment to hydrogen fuel cells and the broader clean energy transition.

Product Type Insights

The gray segment is expected to dominate global hydrogen production, accounting for over 95% of supply through steam methane reforming (SMR). Its primary advantage lies in low production costs, averaging US$1-2/kg, compared to green hydrogen at US$4-8/kg (2024 estimates). Abundant natural gas supply, mature SMR technology, and established infrastructure drive this cost advantage.

Key cost factors for grey hydrogen include natural gas prices, carbon taxes on CO2 emissions, and relatively low operational and maintenance costs. Regions with cheap gas resources, such as North America, the Middle East, and the Asia Pacific, remain leaders in grey hydrogen supply.

Grey hydrogen is widely used in petroleum refining (desulfurization), ammonia and methanol production, steelmaking, and electronics manufacturing due to its cost-effectiveness and reliability. However, rising carbon costs and stricter emission regulations may accelerate the shift toward green hydrogen, reshaping long-term market dynamics.

Regional Insights

Asia Pacific Hydrogen Market Trends

Asia Pacific is projected to dominate, accounting for over 40% of global market share in 2025, making it the largest regional hub for hydrogen development. Strong government policies, ambitious decarbonization goals, and rapid industrial growth fuel this leadership.

China, Japan, South Korea, India, and Australia are at the forefront, deploying both green hydrogen and blue hydrogen technologies to accelerate the clean energy transition. China leads globally in electrolyzer capacity, with 780 MW installed in 2023 and over 9 GW under development, while also pioneering large-scale infrastructure and fuel cell vehicle rollouts. In 2025, China began building the world’s largest pure-hydrogen power project in Inner Mongolia, featuring a 30MW hydrogen-fired turbine integrated with renewable energy storage.

India is rapidly emerging as a key player in the market under the National Green Hydrogen Mission, targeting 5 Mt of renewable hydrogen by 2030. By 2025, India awarded 19 projects totaling 862,000 tonnes/year, launched its first hydrogen-powered train (1,200 HP Jind-Sonipat route), and expanded domestic electrolyser manufacturing via the SIGHT programme.

Meanwhile, Japan and South Korea are advancing hydrogen mobility and integrated value chain initiatives, while Australia focuses on large-scale green hydrogen exports. With strong investments, innovation, and public-private partnerships, Asia Pacific leads the global market, driving sustainable growth, energy security, and decarbonization.

North America Hydrogen Market Trends

North America is set to become the second-largest region, capturing over 30% of the market share, and is also projected to be the fastest-growing region primarily due to strong government support, technological innovation, and rapid deployment across key industries. The increasing use of hydrogen fuel cells in transportation, industrial processes, and power generation, supported by strict carbon reduction regulations and clean energy adoption initiatives.

The U.S. and Canada are leading the regional hydrogen ecosystem through comprehensive national hydrogen strategies and large-scale funding programs. In March 2023, the Biden-Harris Administration announced US$750 Mn through the U.S. Department of Energy (DOE) to accelerate research, development, and demonstration projects, aiming to make clean hydrogen cost-competitive. The DOE’s Hydrogen Energy Earthshot (“1-1-1”) targets production costs of $2/kg by 2025 and $1/kg by 2030, positioning the U.S. at the forefront of the global hydrogen economy.

Further momentum comes from the US$1.7 Bn Industrial Demonstration Programme, funding six projects to decarbonize hard-to-abate sectors. In early 2025, the release of final rules for the Inflation Reduction Act (IRA) clean hydrogen tax credit provided powerful incentives for large-scale private investment.

Competitive Landscape

The global hydrogen market is highly competitive, driven by the rapid push for clean energy solutions and the transition toward a hydrogen-based economy. Several key players are actively expanding their share through technological innovation, strategic collaborations, and international partnerships.

Leading companies such as Air Liquide, Linde plc, and Plug Power dominate the global hydrogen space with robust infrastructure, vast production capabilities, and diversified portfolios. These firms are heavily focused on green and blue hydrogen production, electrolyzer technology, and fueling infrastructure to support decarbonization in transport, industry, and power generation.

Meanwhile, regional and emerging players such as Nel ASA, ITM Power, and Sunfire GmbH are driving competition by offering cutting-edge electrolyzer technologies, modular systems, and cost-effective hydrogen solutions. Innovation in storage, transport, and fuel cell integration is further intensifying the competitive landscape. Stringent global emission regulations and carbon neutrality goals are also driving companies to adopt low-carbon hydrogen production technologies.

Key Industry Developments

- In March 2025, International technology group ANDRITZ received an order for the authority engineering of a 100 MW green hydrogen plant in Rostock, Germany.

- In February 2025, Air Liquide and TotalEnergies partnered to develop two large-scale green hydrogen projects in the Netherlands, with a combined investment exceeding US$1 Bn. Air Liquide will build and operate the 200 MW "ELYgator" electrolyzer in Rotterdam, supplying 23,000 tons of green hydrogen annually by 2027. A 50/50 joint venture will also develop a 250 MW electrolyzer near the Zeeland refinery, set to produce 30,000 tons per year by 2029 and cut CO2 emissions at Zeeland and Antwerp by up to 450,000 tons annually.

Companies Covered in Hydrogen Market

- Linde plc

- Air Products and Chemicals, Inc.

- Air Liquide

- Chevron Corporation

- Saudi Arabian Oil Co.

- Uniper SE

- Worthington Industries

- INOX India Limited

- Cryolor

- Pragma Industries

- BNH Gas Tanks

- Hexagon Purus

- NPROXX

- Oxygen Service Company, Inc. (OSC)

- BayoTech

- Other Market Players

Frequently Asked Questions

The hydrogen market is estimated to be valued at US$226.8 Bn in 2025.

Expanding hydrogen applications across industries is the key demand driver for the hydrogen market.

In 2025, the Asia Pacific region is projected to dominate the market with an exceeding 40% revenue share in the hydrogen market.

Gray hydrogen is anticipated to dominate, capturing approximately 95% of the market revenue share in 2025.

The key players in the hydrogen market include Linde plc, Air Products and Chemicals, Inc., Air Liquide, Chevron Corporation, and Saudi Arabian Oil Co.