- Agrochemicals

- Potassium Dihydrogen Phosphate Market

Potassium Dihydrogen Phosphate Market Size, Share, and Growth Forecast, 2025 - 2032

Potassium Dihydrogen Phosphate Market by Grade Type (Technical Grade, Food Grade), Application (Fungicide, Food additive, Photo-optic, Nutrition, Others), End-user (Agrochemical, Food & beverages, Chemicals, Opto-Electronics, Others), and Regional Analysis for 2025 - 2032

Potassium Dihydrogen Phosphate Market Size and Trends Analysis

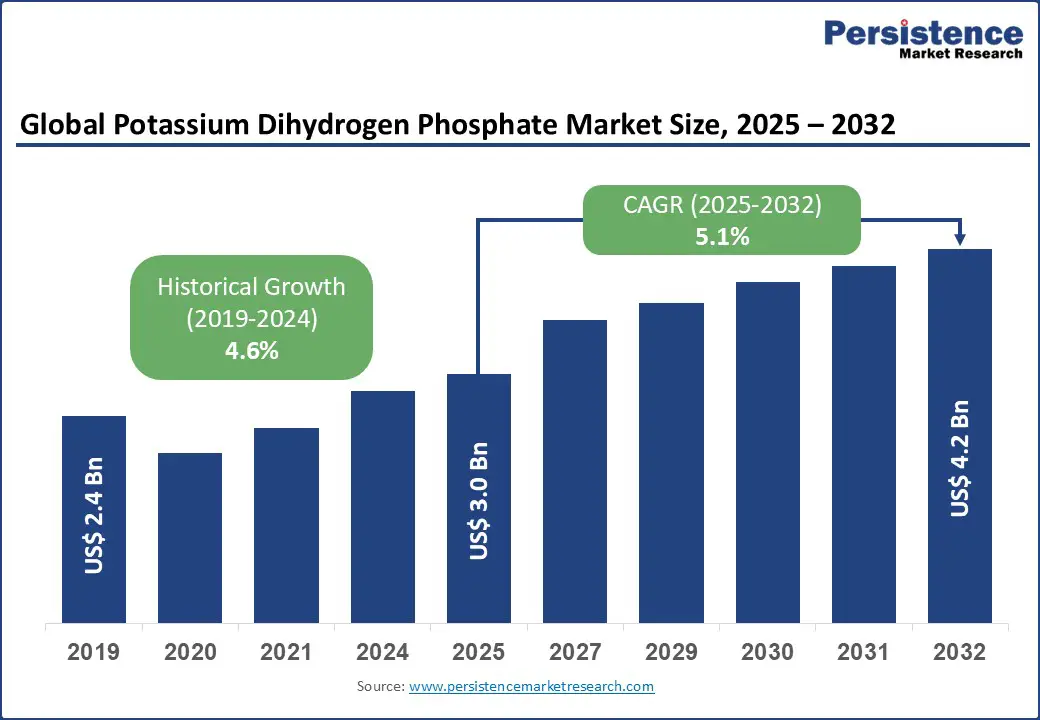

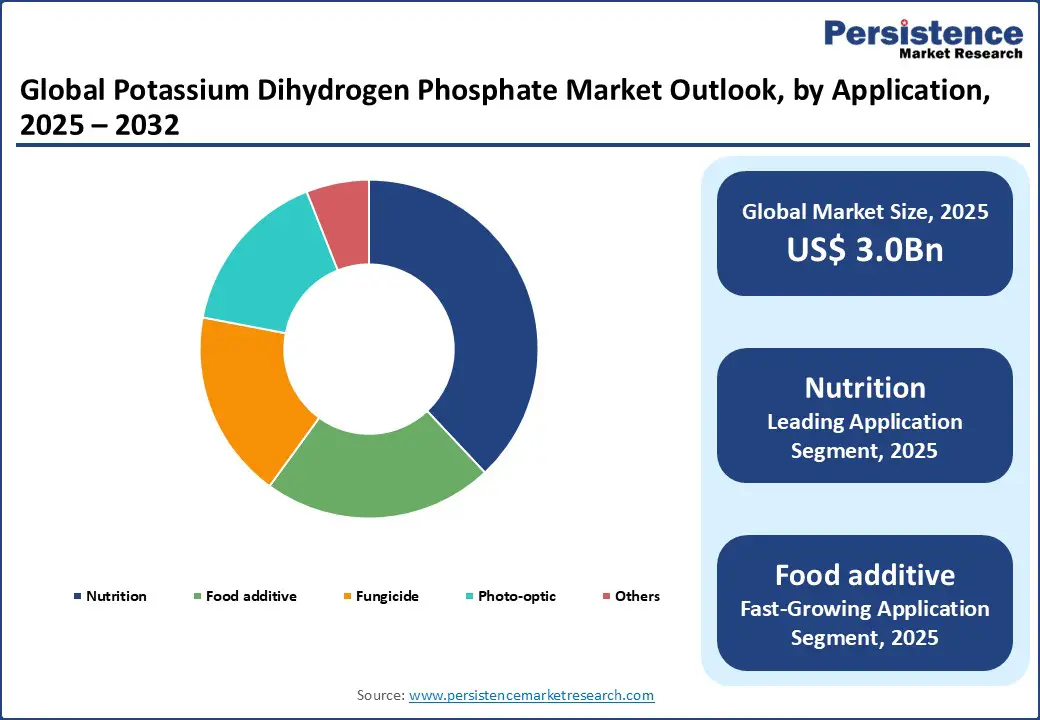

The global potassium dihydrogen phosphate market size is likely to be valued at US$3.0 Bn in 2025 and is expected to reach US$4.2 Bn by 2032, registering a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by the rising demand for agricultural fertilizers, advancements in chemical processing technologies, and the increasing need for sustainable food production solutions.

Key Industry Highlights:

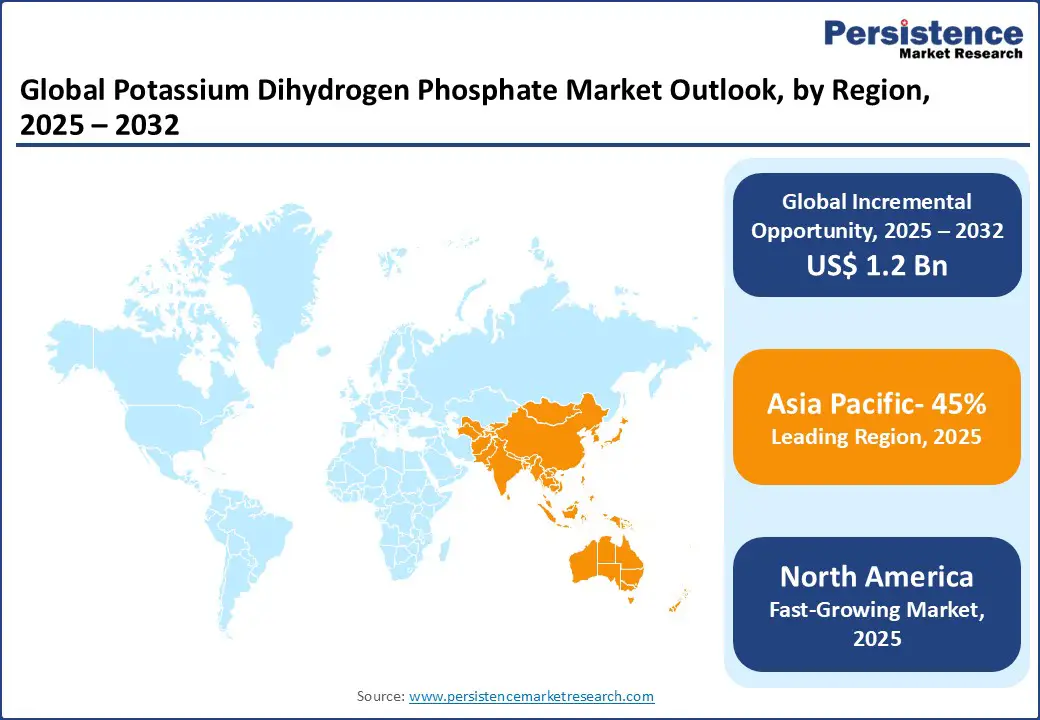

- Leading Region: Asia Pacific is likely to hold a 45% share in 2025, driven by expansive agricultural infrastructure, high crop production volumes, and widespread adoption of innovative fertilizer technologies.

- Fastest-growing Region: North America is expected to witness a rise in agricultural investments, a growing burden of food security, and expansions in chemical manufacturing facilities in the U.S. and Canada.

- Dominant Grade Type: Technical Grade accounts for approximately 35.5% of the potassium dihydrogen phosphate market share in 2025, driven by its cost-effective production.

- Leading Application: Nutrition leads with a 38% share, reflecting its widespread use in fertilizers and agricultural settings.

| Key Insights | Details |

|---|---|

| Potassium Dihydrogen Phosphate Market Size (2025E) | US$3.0 Bn |

| Market Value Forecast (2032F) | US$4.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.6% |

Market Dynamics

Driver - Rising Agricultural Demands and Technological Advancements Driving Market Growth

The global surge in agricultural demands is a primary driver of the potassium dihydrogen phosphate market. According to the Food and Agriculture Organization (FAO), global food production must increase by 60% by 2050 to feed a population of 9.7 billion, with fertilizers playing a critical role in boosting crop yields.

The rising demand, particularly in regions with intensive farming and soil nutrient depletion, underscores the need for effective phosphates such as potassium dihydrogen phosphate, which provides essential potassium and phosphorus for plant growth.

The FAO highlighted the vast global cropland requiring nutrient enhancement, emphasizing the growing demand for efficient fertilizers to support agricultural productivity. In the Asia Pacific, which holds the largest share of the world’s agricultural land, industry has emerged as a key solution to improve yields, particularly for staple crops such as rice and wheat, where productivity gains are critical for food security.

Technological advancements in phosphate production are further propelling market growth. Modern platforms, including ICL Group’s advanced manufacturing systems, utilize high-purity synthesis and controlled-release technologies designed to minimize environmental impact while improving nutrient absorption in crops. Optimized formulations enhance plant uptake efficiency, ensuring stronger crop performance compared to traditional fertilizers.

Innovations such as eco-friendly production methods and integration with precision agriculture tools are fostering adoption, especially in the Asia Pacific’s resource-constrained and price-sensitive markets. Companies such as Hubei Xingfa Chemicals have introduced water-soluble phosphate solutions that help reduce application costs, making fertilizers more accessible to small and medium-scale farmers.

Restraint - High Costs and Skilled Personnel Requirements Restrict Adoption

The high cost of production remains a significant barrier, particularly in low- and middle-income countries. Advanced manufacturing platforms, equipped with high-purity synthesis and environmental compliance systems, require substantial upfront investments for industrial-grade setups.

Ongoing costs for raw materials, energy-intensive processes, and quality control measures, such as testing for impurities, add to the total cost of ownership. In regions such as Sub-Saharan Africa and rural Latin America, where agricultural budgets are limited, these financial burdens restrict access to potassium dihydrogen phosphate, despite growing crop demands.

The FAO has noted that “the cost of advanced fertilizers may be a disincentive,” highlighting high input costs as a barrier to adoption in many developing economies.

The requirement for skilled personnel to manage and apply systems also hinders market growth. Proper formulation and application demand specialized training in agronomy, soil science, and precision agriculture techniques. For instance, achieving optimal nutrient delivery requires expertise in soil pH balancing, which is scarce in developing regions.

In Africa, only a small share of agricultural facilities have access to trained fertilizer specialists, exacerbating the skills gap. High training costs for technicians further restrict adoption in emerging markets, slowing market expansion despite strong demand in the Asia Pacific.

Opportunity - Innovation in Sustainable Systems and Multi-Application Use Boosts Consumption

The development of sustainable and eco-friendly potassium dihydrogen phosphate formulations presents significant growth opportunities, enabling deployment in regulated agriculture, food processing, and industrial applications. These formulations address environmental concerns such as nutrient runoff, making them ideal for eco-conscious markets.

For example, Yara International’s controlled-release phosphates reduce environmental impact, supporting their use in sustainable farming systems. As industries prioritize green chemistry, demand for such solutions is rising, particularly in North America, where regulatory pressures drive adoption.

The growing popularity of multi-functional applications, such as food additives and opto-electronics, provides another avenue for market expansion. The use of potassium dihydrogen phosphate as a buffering agent in food and as a crystal component in optical devices enhances its versatility.

Its role in food preservation supports longer shelf life in the Asia Pacific’s food sector, while its applications in opto-electronics, such as laser technology, are expanding in North America, contributing to growth in high-tech industries.

The integration of digital platforms for supply chain monitoring and precision agriculture further enhances market potential. Companies such as CF Industries are incorporating IoT-enabled systems for real-time fertilizer tracking, improving application efficiency.

In North America, digital platforms have supported rising sales, while in the Asia Pacific, they have strengthened adoption. These trends improve operational sustainability and farmer trust, supporting market growth in both dominant and emerging regions.

Category-wise Analysis

Grade Type Insights

The global potassium dihydrogen phosphate market is segmented into technical grade and food grade. Technical grade dominates, holding approximately 35.5% of the market share in 2025, due to its cost-effective production and scalability for agricultural and industrial applications. Companies such as Hubei Xingfa Chemicals leverage the technical grade’s lower production costs compared to food grade to supply bulk markets, particularly in Asia Pacific’s agrochemical sector.

Food grade is the fastest-growing segment, driven by increasing demand for safe additives in food and beverage settings. Innovations in high-purity food-grade technologies, such as those from Prayon, ensure compliance with stringent regulations such as FDA and EU standards, boosting adoption in premium markets.

Application Insights

The global potassium dihydrogen phosphate market is divided into fungicide, food additive, photo-optic, nutrition, and others. Nutrition leads with a 38% share in 2025, driven by its widespread use in fertilizers and agricultural settings. Its role in enhancing crop yields is critical, with significant volumes used annually worldwide for nutrition applications, particularly in the Asia Pacific, where rice and wheat production rely heavily on phosphates.

Food additive is the fastest-growing segment, fueled by advancements in food preservation and rising demand for processed foods. Its ability to act as a pH stabilizer and buffering agent drives adoption in North America, where processed food sales have continued to grow steadily. This segment’s expansion is further supported by post-pandemic demand for shelf-stable products.

End-user Insights

The potassium dihydrogen phosphate market is segmented into agrochemical, food & beverages, chemicals, opto-electronics, and others. Agrochemical dominates with a 55% share in 2025, driven by their essential role in fertilizer production. This end-user relies on efficient formulations for crop nutrition, with substantial volumes used annually in the Asia Pacific for staple crops such as rice and maize.

Food & beverages are the fastest-growing segment, propelled by increasing demand for additives in processed foods and beverages. In North America, this segment has experienced strong sales growth, driven by consumer demand for high-quality, shelf-stable products and regulatory support for safe additives.

Regional Insights

Asia Pacific Potassium Dihydrogen Phosphate Market Trends

Asia Pacific dominates the global potassium dihydrogen phosphate market, expected to account for 45% of the share in 2025, driven by expansive agricultural infrastructure, increasing food demands, and rising investments in chemical technologies. Asia Pacific remains the key growth engine for the industry.

In China, intensive farming practices and government programs such as the Green Agriculture Plan are boosting demand for affordable, technical-grade solutions. Domestic manufacturers such as Hubei Xingfa Chemicals and Sinochem Holdings play a vital role in meeting local needs, with widespread adoption across agricultural units.

India’s market growth is supported by large-scale upgrades and rising fertilizer demand, strengthened by subsidy programs that make advanced solutions more accessible to farmers. Japan’s market is shaped by its focus on high-precision chemicals for opto-electronics, where companies such as EuroChem Group are expanding their presence.

Across the region, increased spending on agricultural inputs, adoption of digital platforms for smart farming, and a heightened emphasis on food security continue to solidify Asia Pacific’s dominance in the industry.

North America Potassium Dihydrogen Phosphate Market Trends

North America is emerging as the fastest-growing region, driven by strong demand for fertilizers, advanced agricultural infrastructure, and rising crop production needs. The U.S. Department of Agriculture highlights the extensive reliance on fertilized acreage, underscoring the importance of efficient nutrient solutions. Leading brands such as CF Industries and Yara International are at the forefront, developing innovative platforms to optimize production.

Consumer preferences are shifting toward sustainable systems, with companies such as ICL Group introducing eco-friendly formulations designed to reduce nutrient runoff and environmental impact. Stringent regulations from the Environmental Protection Agency further encourage the use of reliable, low-impact components, aligning with regional sustainability goals.

Supportive policies across the U.S. and Canada also play a pivotal role, covering a significant share of production costs and encouraging adoption of advanced technologies. Together, these factors are fueling consistent market growth and reinforcing North America’s position as a critical driver of the industry.

Europe Potassium Dihydrogen Phosphate Market Trends

Europe’s market is led by Germany, the U.K., and France, supported by strong regulatory frameworks and high production volumes. Germany holds a prominent share, driven by established players such as EuroChem Group and Tessenderlo Group. The European Union’s Common Agricultural Policy continues to promote advanced technical- and food-grade systems, encouraging adoption across a wide base of agricultural and industrial facilities.

In the U.K., growing demand for sustainable fertilizers is driving expansion, with Prayon’s specialized kits gaining traction among environmentally conscious users. France is witnessing rising demand for chemical applications, supported by solutions from Sinochem Holdings that cater to diverse industrial and agricultural needs.

Regulatory emphasis on sustainable and green practices across the region further strengthens growth prospects. These combined factors are reinforcing Europe’s market trajectory, ensuring steady expansion and highlighting its role as a key hub for market innovation and adoption.

Competitive Landscape

The global potassium dihydrogen phosphate market is highly competitive, with global and regional players vying for share through innovation, competitive pricing, and reliability. The rise of sustainable and multi-grade products intensifies competition, as companies meet stringent regulatory and industrial demands. Strategic partnerships, mergers, and regulatory approvals are key differentiators.

Key Developments

- November 2024: PhosAgro announced an investment plan of RUB 75 billion for 2024, which was directed toward executing key projects at its production facilities. The initiative expanded phosphate processing capacity, boosted fertilizer output, and strengthened acid production units, reinforcing its position as a leading global fertilizer producer.

- September 2025: Cronus Chemicals announced a $2 billion investment to establish a major ammonia production facility in Tuscola, Illinois. The project featured an annual capacity of 950,000 short tons and incorporated advanced carbon capture technology, strengthening domestic fertilizer supply while supporting sustainable industrial growth and environmental responsibility.

Companies Covered in Potassium Dihydrogen Phosphate Market

- Hubei Xingfa Chemicals

- Sinochem Holdings

- Prayon

- CF Industries

- ICL Group

- Yara International

- Tessenderlo Group

- Coromandel International

- EuroChem Group

Frequently Asked Questions

The potassium dihydrogen phosphate market is projected to reach US$3.0 Bn in 2025.

Rising agricultural demands, technological advancements in fertilizers, and government initiatives for food security are key drivers.

The market is poised to witness a CAGR of 5.1% from 2025 to 2032.

Innovations in sustainable systems and multi-application solutions present significant growth opportunities.

ICL Group, Yara International, and CF Industries are among the leading players.