- Food Ingredients & Additives

- Sugar Substitute Market

Sugar Substitute Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Sugar Substitute Market is segmented by Product Type (HFCS, Sugar Alcohols, Saccharin, Sucralose, Allulose, Stevia, Others), by Intensity (High intensity, Low intensity), by Application (Food, Beverage, Healthcare & Personal Care, Others), by Distribution Channel (B2B, B2C), and by Regional Analysis, 2026 - 2033

Sugar Substitute Market Share and Trends Analysis

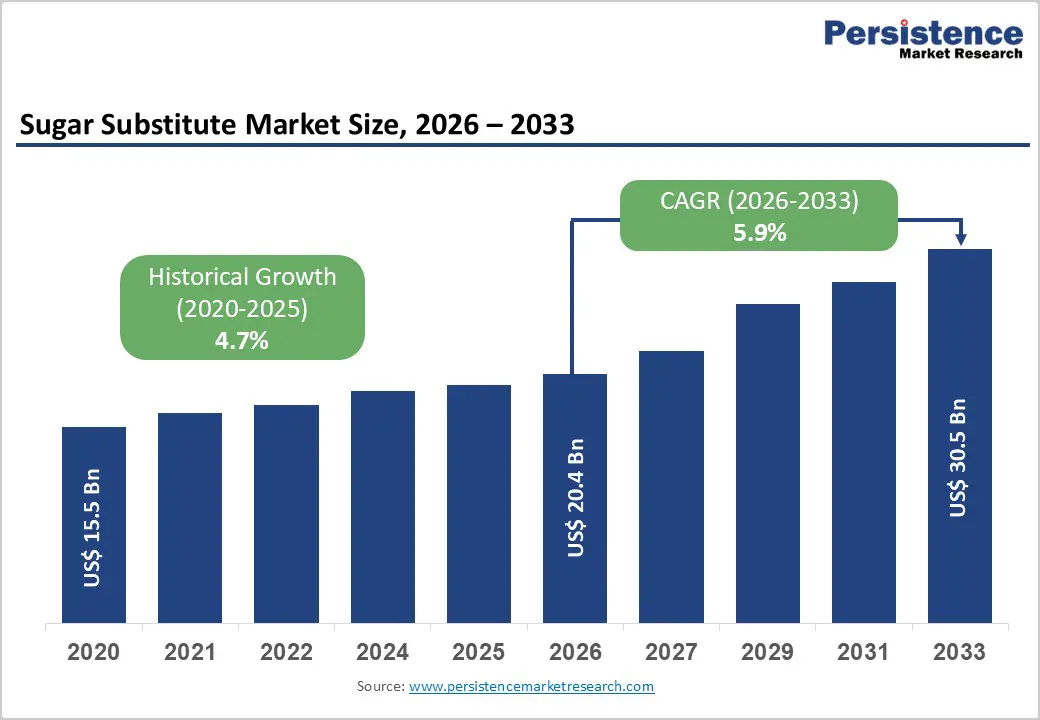

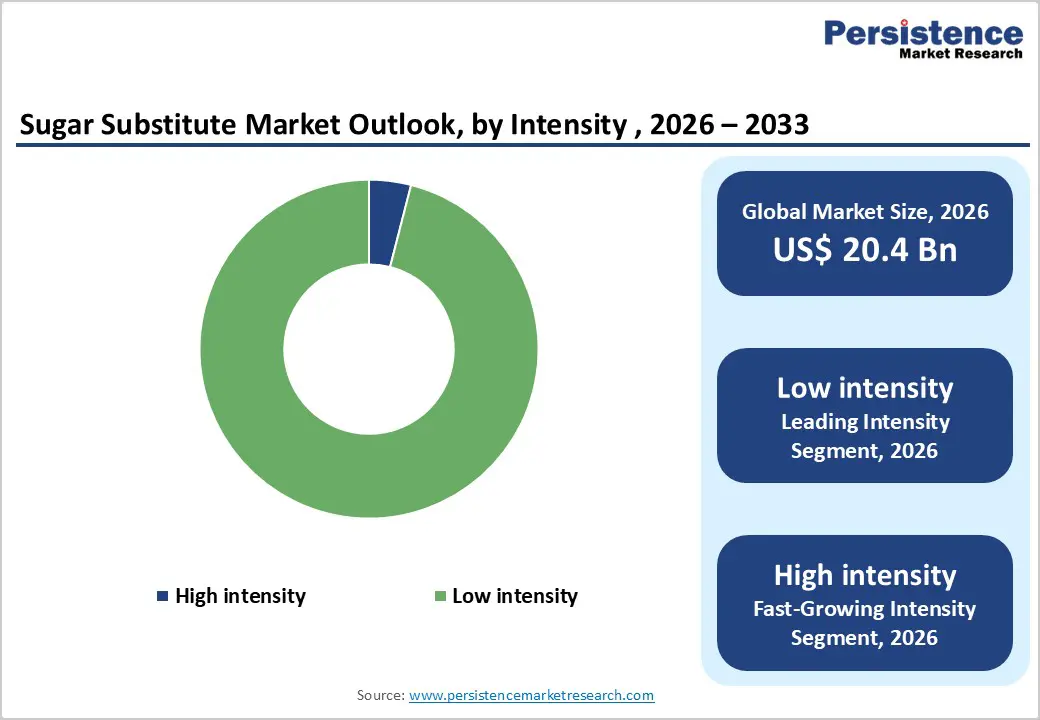

The global sugar substitute market size is expected to be valued at US$ 20.4 billion in 2026 and projected to reach US$ 30.5 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

According to the World Health Organization (WHO), one in eight people worldwide suffered from obesity in 2022. Since 1975, the prevalence of obesity has more than tripled. Sugar substitutes are gaining popularity worldwide due to their high sweetness and low-calorie content. They are preferred by individuals looking to manage their blood sugar levels, decrease weight, and reduce their calorie intake.

Several food brands are using sugar substitutes to promote their products as healthy. Consumers are showing a rising interest in sugar-free products, thereby providing these substitutes with an impetus for market growth. Food and beverage manufacturers are adopting substitutes in their products as these enable them to meet the rising demand for sweetened products with zero sugar content.

Key Industry Highlights

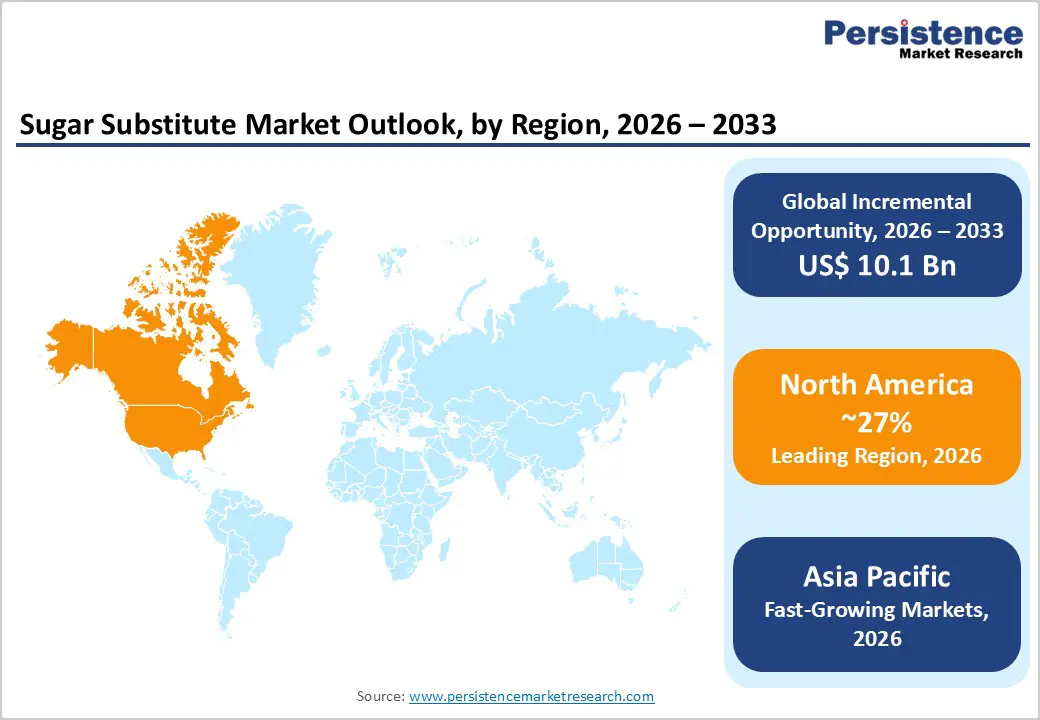

- Leading Region: North America, holding 27% market share, driven by high diabetes prevalence, regulatory push on sugar labeling, and strong adoption of low- and no-calorie sweeteners across food and beverage applications.

- Fastest-Growing Region: Asia Pacific, fueled by an expanding middle-class population, rising diabetes awareness, rapid urbanization, and a strong manufacturing base for stevia and sucralose in countries like China and India.

- Fastest-Growing Product Type Segment: Stevia, driven by surging demand for plant-based, zero-calorie sweeteners, clean-label positioning, and strong regulatory acceptance supporting large-scale food and beverage reformulations.

- Growth Indicator: Rising global demand for low-calorie and functional food products is accelerating the shift toward sugar alternatives that support weight management, blood sugar control, and overall metabolic health.

- Opportunities: Strategic alliances with food and beverage brands, retailers, and research institutions are enabling faster innovation, expanded distribution, and improved scalability of next-generation sweetening solutions.

- Key Developments: In March 2026, Skyway launched Cloud Shake in India using monk fruit and ashwagandha. In January 2026, Manus scaled monk fruit production via fermentation in the U.S. In June 2025, Layn Natural Ingredients introduced SteviUp M2 Reb M for improved formulation performance.

| Key Insight | Details |

|---|---|

| Global Sugar Substitute Market Size (2026E) | US$ 20.4 Bn |

| Market Value Forecast (2033F) | US$ 30.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Driver - Rising Global Demand for Low-Calorie and Functional Food Products

The primary driver for the industry is the fundamental pivot toward health-conscious consumption. According to the World Health Organization (WHO), global obesity rates have nearly tripled in the last two decades, creating an urgent requirement for reduced-sugar alternatives. Consumers are increasingly seeking better-for-you options that provide the sweetness they crave without the metabolic risks associated with high sucrose intake. This has led to a surge in demand for sweeteners like Stevia and Allulose in the Beverage sector. Manufacturers are responding to this trend by launching clean-label products that utilize natural substitutes, which are perceived as safer and more sustainable by the modern shopper, thereby driving consistent volume growth across retail and industrial channels.

Restraints - Stringent regulations to make compliance difficult

Manufacturers in the keto-friendly sweeteners industry are facing challenges in dealing with complex and constantly changing regulations. Meeting the several international and regional regulations related to food additives, labelling, and health claims is becoming a key obstacle. Health authorities require thorough safety assessments, and different standards in various markets make compliance difficult.

Sugar substitute manufacturers need to invest a substantial amount in research and testing to meet these regulatory requirements, which often result in high costs and product delays. It is hence essential for brands to effectively address these regulatory hurdles to gain market access. They are set to focus on building consumer trust and maintaining growth in this dynamic and heavily regulated industry.

Opportunity - Forming strategic alliances with food and beverage companies, retailers, or health-focused brands

Strategic partnerships are emerging as a critical growth lever in the sugar substitutes market, enabling manufacturers to expand distribution reach and strengthen market presence. Collaborations with food and beverage companies, retailers, and health-focused brands allow producers to integrate sugar alternatives into a wide range of end-use products, enhancing visibility and accelerating consumer adoption. These alliances also support co-branding initiatives and product innovation, helping companies tap into established customer bases while reinforcing credibility in health-conscious segments.

In addition, partnerships with research institutions and ingredient technology providers are accelerating innovation cycles and improving access to advanced sweetening solutions. As demand for low-calorie and natural sweeteners rises due to increasing health awareness and lifestyle diseases, collaborative ecosystems enable faster development of novel formulations. This approach not only enhances product differentiation but also supports scalability, allowing manufacturers to respond effectively to evolving consumer preferences and strengthen their competitive positioning.

Category-wise Analysis

Intensity Insights

Low-intensity sugar substitutes hold a staggering market share of 96% as of 2025, driven largely by the widespread use of High-Fructose Corn Syrup (HFCS) across the food and beverage industry. HFCS, being cost-effective and highly functional, is extensively used in carbonated drinks, baked goods, sauces, and ready-to-eat products due to its similar sweetness profile and caloric content compared to regular sugar. These substitutes provide bulk, texture, and taste while fitting seamlessly into existing manufacturing processes. Their compatibility with large-scale production and wide consumer acceptance contributes significantly to their dominance. In contrast, high-intensity sugar substitutes such as stevia and sucralose, although growing in popularity, are primarily used in niche formulations where calorie reduction is prioritized.

Product Type Insights

By product type, stevia is expected to grow at a leading CAGR in the forecast period 2026 to 2033, driven by rising consumer preference for natural, zero-calorie sweeteners. Extracted from the Stevia rebaudiana plant, it offers high sweetness intensity without raising blood sugar levels, making it ideal for diabetics and weight-conscious consumers.

According to the U.S. Department of Agriculture, the demand for natural sugar alternatives has increased steadily since 2020, aligning with dietary shifts toward clean-label products. The FDA’s GRAS (Generally Recognized As Safe) status for steviol glycosides has further strengthened its acceptance in food and beverage applications. While artificial sweeteners like aspartame are widely used, growing scrutiny over synthetic additives is causing a pivot toward plant-derived solutions. Monk fruit and Advantame are also gaining attention, though their niche appeal and cost barriers may limit broader adoption compared to stevia’s scalable versatility.

Regional Insights

North America Sugar Substitute Market Trends and Insights

North America dominates with a 27% market share as of 2025, driven by growing health consciousness and policy-driven dietary changes. According to the Centers for Disease Control and Prevention (CDC), over 38 million Americans have diabetes, while an additional 97.6 million adults are living with prediabetes, signaling an urgent shift toward sugar alternatives. In response, U.S. regulatory bodies such as FDA have mandated transparent labeling of added sugars, prompting manufacturers to reformulate products.

The dietary guidelines for American population recommends keeping added sugars under 10% of daily calories. Consumers are embracing low- or no-calorie sweeteners to support weight control and manage glucose levels. Demand for sugar-free molasses and natural alternatives in packaged goods continues to surge. In Canada, similar trends are evident, with increasing public awareness around sugar-related health risks and a parallel rise in demand for clean-label sugar substitutes.

Europe Sugar Substitute Market Trends and Insights

Europe sugar substitutes market is expected to show lucrative growth of 5.3% during the forecast period 2026 to 2033, driven by escalating health concerns, evolving consumer preferences, and stringent food regulations. Rising obesity and diabetes projections are prompting food and beverage manufacturers in countries like Germany, the U.K., France, Italy, and Spain to reformulate products with reduced or no added sugar.

Positive safety assessments from the European Food Safety Authority (EFSA) and the U.K. Food Standards Agency (FSA) are facilitating market entry for newer, plant-derived sweeteners. Clean-label demand is rising sharply, as European consumers increasingly reject artificial additives and opt for recognizable, naturally sourced ingredients. In Germany, more than half the population favors sugar-free alternatives, signaling a strong shift in dietary attitudes. Regulatory enforcement on transparency and fair trade practices further fosters trust and drives innovation, positioning Europe as a key region for the advancement of sugar substitute solutions.

Asia Pacific Sugar Substitute Market Trends and Insights

Asia Pacific is identified as the fastest growing segment for the sugar substitute market through 2033. This rapid expansion is primarily driven by the burgeoning middle class in China, India, and ASEAN countries, combined with a rising awareness of diabetes management. The region's growth dynamics are further supported by a massive expansion in the modern retail and food service sectors. China is a major global player, not only as a massive consumer but also as a leading producer of Stevia and Sucralose.

The region also benefits from significant manufacturing advantages and a lower cost of raw materials. In India, the government's focus on nutrition and health has encouraged local food processors to introduce reduced-sugar snacks. The rapid growth of the tea and coffee culture in urban centers is also driving the demand for tabletop sweeteners. As international players like Ajinomoto Co., Inc. and Daesang Corporation increase their regional investments, Asia Pacific is poised to become the global hub for both the production and consumption of innovative sugar substitutes.

Competitive Landscape

The Sugar Substitute Market exhibits a moderately consolidated structure, where a group of established global ingredient giants hold significant influence over the industrial supply chain. Leaders like ADM, Cargill, and Ingredion dominate the market through extensive distribution networks and advanced R&D capabilities. These companies employ strategies focused on vertical integration and strategic partnerships with biotech firms to secure access to novel sweetener technologies. However, the retail landscape remains dynamic with a vibrant array of boutique brands like Pyure Brands LLC and Whole Earth catering to specific lifestyle niches. Key differentiators include the ability to provide high-purity, standardized extracts and the attainment of prestigious safety and sustainability certifications. Emerging business model trends show a move toward co-creation, where sweetener producers work directly with food brands to develop customized, category-specific flavor solutions.

Key Developments:

- In March 2026, Skyway entered India’s ready-to-drink nutrition segment with the launch of Cloud Shake, a protein milkshake sweetened with monk fruit and formulated with KSM-66 Ashwagandha, targeting health-conscious consumers.

- In January 2026, Manus announced plans to scale monk fruit production in the U.S. through fermentation technology at its Augusta, Georgia facility, aiming to improve accessibility and supply.

- In June 2025, Layn Natural Ingredients launched SteviUp M2 Reb M, a next-generation stevia ingredient designed to offer enhanced solubility and improved application performance in food and beverage formulations.

- In April 2025, Ingredion Incorporated achieved a major milestone by becoming the first and only company to reach Farm Sustainability Assessment (FSA) Silver level for 100% of its stevia supply chain, as verified through an external audit. This recognition by the Sustainable Agriculture Initiative (SAI) marks the only third-party verified stevia supply chain globally.

Companies Covered in Sugar Substitute Market

- IFF

- ADM

- Cargill, Inc

- Ingredion

- Tate & Lyle

- Ajinomoto Co., Inc.

- Daesang Corporation

- Roquette

- Sweegen

- Pyure Brands LLC

- The Truvía Company, LLC

- B&G Foods, Inc.

- Cumberland Packing Corp.

- Whole Earth

- Others

Frequently Asked Questions

The global Sugar Substitute market is projected to be valued at US$ 20.4 Bn in 2026.

Rising Global Demand for Low-Calorie and Functional Food Products is a major factor driving the global Sugar Substitute market.

The Global Sugar Substitute market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Forming strategic alliances with food and beverage companies, retailers, or health-focused brands is the key market opportunity.

Major players in the Global Sugar Substitute market include Cargill, Inc., ADM, IFF, Ingredion, Tate & Lyle, Ajinomoto Co., Inc., Roquette, and others.