- Automation & Robotics

- Industrial Metal Detector Market

Industrial Metal Detector Market Size, Share, and Growth Forecast 2025 - 2032

Industrial Metal Detection Market by End-use (Food & Beverages, Pharmaceuticals, Chemicals, Mining, Plastic & Rubber, Others), Product Type (Conveyorized Metal Detector, Gravity Feed Metal Detector, Pipeline Metal Detector, Pharma Metal Detector, Others), Capability Type (Ferrous, Non-Ferrous, Non-Magnetic), and Regional Analysis for 2025 - 2032

Industrial Metal Detector Market Share and Trends Analysis

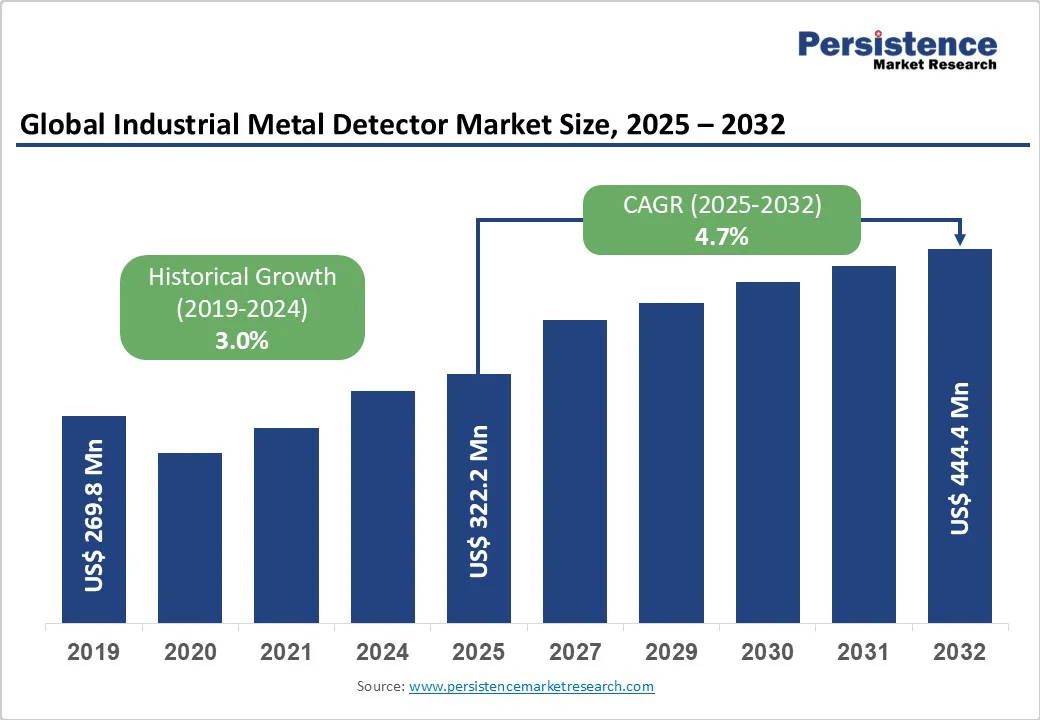

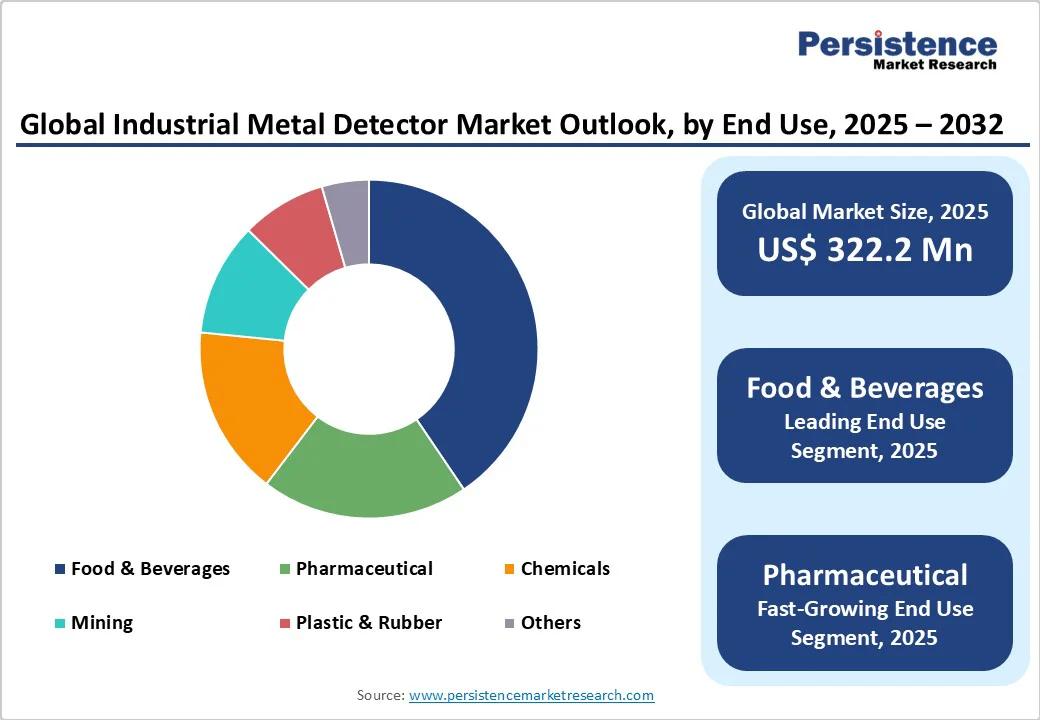

The global industrial metal detector market size is expected to be valued at US$322.2 million in 2025 and is projected to reach US$444.4 million by 2032, growing at a CAGR of 4.7% during the forecast period of 2025 -2032.

Market expansion is driven by stringent regulatory requirements from agencies such as the FDA and USDA, which mandate rigorous contamination control measures, particularly within food processing operations, where metal detection has become a critical control point under HACCP systems.

Key Market Highlights

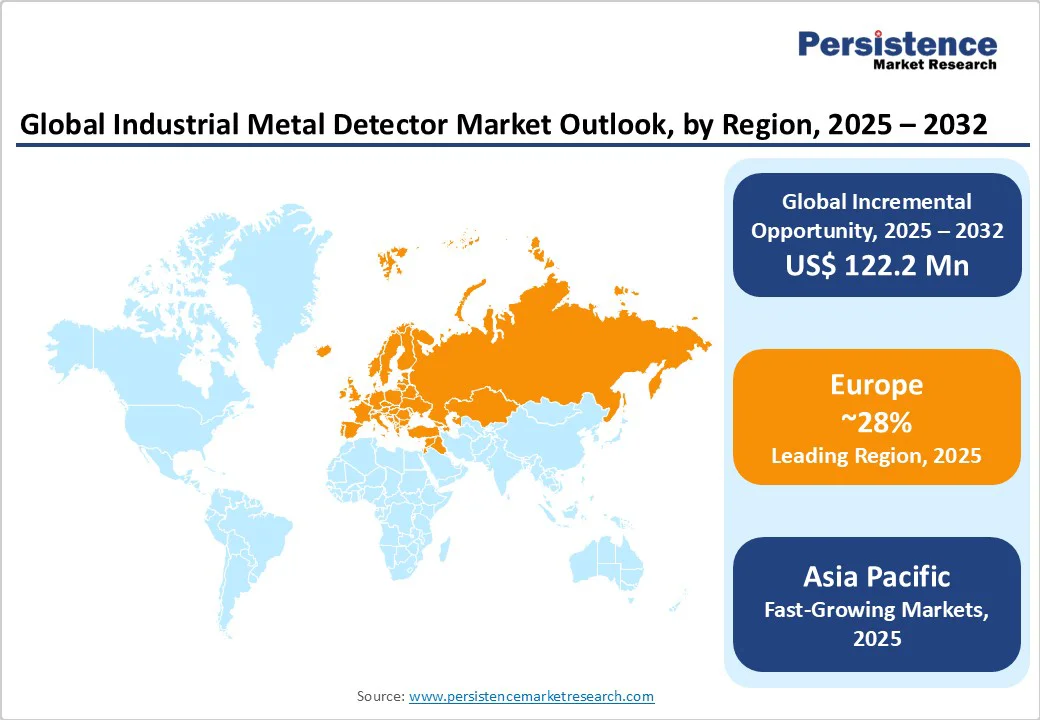

- Leading Region: Europe is slated to hold around 28% share in 2025, driven by strong regulatory harmonization under the European Union (EU) framework, a mature manufacturing infrastructure, and stringent contamination control standards.

- Fastest-Growing Regional Market: Asia Pacific is likely to expand at an estimated CAGR of 5.3% through 2032, propelled by rapid industrialization, developing infrastructure, increasing regulatory scrutiny, and rising quality expectations in food, pharmaceutical, and mining sectors across China, Japan, India, and ASEAN countries.

- Investment Plans: Manufacturers are integrating AI and smart sensor technologies, establishing R&D hubs, and launching digitally adjustable systems with Ethernet and Wi-Fi connectivity, as well as automated product effect learning.

- Dominant End-Use Segment: The food & beverages segment is expected to capture approximately 66% market revenue share in 2025, driven by contamination prevention needs in vegetables, fruits, dairy, meat, seafood, and processed foods.

- Leading Product Type: Conveyorized metal detectors, with an approximately 47% share in 2025, are widely preferred for their seamless integration with production lines, automated rejection systems, and multi-spectrum detection capabilities for ferrous, non-ferrous, and stainless steel contaminants.

| Key Insights | Details |

|---|---|

| Industrial Metal Detector Market Size (2025E) | US$322.2 Mn |

| Market Value Forecast (2032F) | US$ 444.4 Mn |

| Projected Growth CAGR (2025 - 2032) | 4.7% |

| Historical Market Growth (2019-2024) | 3.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Stringent Food Safety Regulations and Compliance Mandates

Government regulatory bodies worldwide have intensified enforcement of contamination control standards, creating substantial demand for industrial metal detection systems. The FDA has outlined specific metal detection critical limits to be implemented across the food industry by 2024, emphasizing the importance of critical control points in manufacturing processes.

In Europe, Regulation EC 2023/915 establishes maximum levels for certain contaminants in foodstuffs, while the EU Directive on Food Hygiene 93/43/EEC obligates food producers to establish self-control systems based on HACCP principles.

These regulatory frameworks mandate that metal detectors be positioned at critical control points, particularly before packaging stages, with standards such as BRC requiring equipment capable of identifying metal particles smaller than 1.5 mm in certain food types.

The regulatory pressure extends beyond food to pharmaceuticals, where contamination-led recalls have driven widespread adoption of sensitive detection systems to maintain compliance with quality assurance standards established by the FDA and EMA.

Rising Product Contamination Incidents to Drive Preventive Investments

Rising contamination incidents are driving the adoption of metal detectors across various industries. In 2024, food recalls sickened 1,392 people, with hospitalizations doubling from 230 in 2023 to 487 and deaths rising from 8 to 19. Foreign material, including metal and plastic, caused 12 recalls, highlighting persistent production and packaging risks.

Metal detectors are developed to meet safety standards in food and pharmaceutical manufacturing, as contamination is a leading concern. For example, devices such as Mettler-Toledo's M30 R-Series metal detectors focus on novel contamination detection with digital integration.

On the other hand, Loma Systems' IQ4 series offers highly accurate sensitivity and real-time monitoring. High-profile cases, such as the Boar’s Head deli meat recall (resulting in 61 illnesses and 10 deaths) and the McDonald’s Quarter Pounders incident (leading to 104 illnesses), have further heightened industry vigilance.

High Initial Capital Investment and Maintenance Expenses

Industrial metal detectors come with substantial upfront costs that create adoption barriers, particularly for small and medium-sized enterprises. Basic metal detection units start at approximately US$3,000, while advanced systems from leading manufacturers such as Mettler-Toledo and Thermo Fisher Scientific can exceed US$45,000.

Beyond initial purchase prices, these systems incur annual maintenance expenses ranging from 10% to 15% of the equipment cost, alongside additional expenditures for calibration, validation protocols, and potential production downtime during equipment servicing. Integration with existing production lines adds further financial burden, as manufacturers must modify conveyor systems, install reject mechanisms, and implement supporting infrastructure.

Even larger corporations face budgetary constraints and prolonged capital approval cycles that delay equipment upgrades, while price-sensitive emerging markets experience particularly acute financial barriers that hinder the widespread adoption of technology.

Integration of Artificial Intelligence and Smart Sensor Technologies

The pharmaceutical sector offers significant growth potential, with the metal detector segment projected to achieve the fastest CAGR during the forecast period. AI and smart sensor integration are enhancing detection accuracy and operational efficiency through advanced signal processing, automatic product effect learning, and reduced manual calibration.

For instance, Illinois Tool Works’ IQ4M Metal Detector, launched in April 2025, delivers high-precision contamination detection with minimized false rejects. Another notable development occurred in September 2024, when Eriez partnered with Cardiff University to establish an R&D hub that advances detection technologies.

The adoption of digitally adjustable systems with Ethernet/Wi-Fi connectivity, barcode support, and integrated I/O communication is driving new opportunities as manufacturers seek comprehensive, high-performance contamination control solutions in pharmaceutical production.

Manufacturers’ Focus on Consumer Safety to Foster Growth Avenues

Over the next ten years, the global demand for industrial metal detectors is expected to increase due to heightened consumer awareness of safety. Surging scrutiny of industries such as food processing, pharmaceuticals, and packaging necessitates the development of effective detection systems. To identify pollutants and preserve product integrity, businesses are investing heavily in sophisticated metal detection technologies.

They prioritize their usage to protect customers, improve brand reputation, and ensure regulatory compliance. Modern advances in technology are driving the market for industrial metal detectors by providing high standards of safety and operational efficiency. It is anticipated to, in turn, improve public health and customer confidence.

Category-wise Analysis

End-use Insights

The food & beverages segment is expected to lead the industrial metal detector market in revenue, with a share of around 66% in 2025, driven by the need for contamination prevention in processing operations. Regulatory agencies such as the FDA, USDA, CFIA, and EFSA mandate metal detection at critical control points.

The U.K. food and beverage industry contributed £30 billion in 2021, with 93% consumer trust in food safety, reflecting the effectiveness of detection protocols. High-risk products include vegetables, fruits, dairy, meat, seafood, and processed foods due to mechanical processing with blades, conveyors, and sealing equipment.

The pharmaceutical sub-segment is adopting detection systems for tablets, capsules, liquids, and ampules. At the same time, the chemical industry uses metal detectors in agrochemicals, paints, dyes, and petrochemicals to ensure product purity and protect equipment.

Product Type Insights

Conveyorized metal detectors are poised to lead the market, with an estimated 47% share in 2025, driven by their versatility and seamless integration with production lines. Designed to detect metal contaminants on conveyor belts, these systems employ automated rejection mechanisms, including pushers, air blasts, or belt stops.

CEIA systems combine conveyor integration with multi-spectrum technology, detecting magnetic, non-magnetic, and stainless steel metals while minimizing product effects, achieving precision comparable to hundreds of conventional transits.

Bunting detectors handle ferrous, non-ferrous, stainless, and manganese steel in food processing, plastics, recycling, and bulk handling industries. Flexible installation around or beneath belts, coupled with automatic rejection, ensures effective metal control, preventing equipment damage, recalls, and production downtime.

Capability Type Insights

Ferrous metal detection is likely to hold approximately 45% market share in 2025, driven by the prevalence of iron-based contaminants in industrial production. Ferrous materials’ strong magnetic properties enable reliable detection of iron fragments from worn machinery, processing equipment, and conveyors.

Advanced algorithms target iron and manganese steel, protecting crushers, screens, and conveyor belts in the mining and aggregates industries. For example, Eriez’s MetAlarm system automates detection, improving productivity and safety by reducing manual inspection risks.

Non-ferrous detection covers aluminum, brass, copper, and other non-magnetic metals in food packaging and pharmaceuticals. Detecting non-magnetic stainless steel is technically challenging, requiring multi-spectrum technology to differentiate metals from conductive products while maintaining high detection performance across all contaminant types.

Regional Insights

North America Industrial Metal Detector Market Trends

North America is forecasted to capture around 20% share of the metal detection market in 2025, on account of the strict food safety and pharmaceutical regulations enforced by the FDA and CFIA. Widespread adoption spans food processing, pharmaceuticals, and chemical manufacturing to ensure product quality.

The presence of leading pharmaceutical companies, including Pfizer, Johnson & Johnson, Merck, AbbVie, Bristol Myers Squibb, Eli Lilly, Amgen, Gilead, and Regeneron, accelerates adoption and innovation in contamination detection.

U.S. growth is fueled by supply chain strengthening and regulatory compliance, with systems featuring digital signal processing for high-speed accuracy under HACCP, FSMA, FDA, USDA, and GFSI standards.

Canada’s pharmaceutical sector further supports market expansion through rigorous control of contamination. Innovation in the region, exemplified by Advanced Detection Systems’ ProScan Conveyor, enhances detection accuracy, user interfaces, and reliability in packaged and dry food inspection.

Europe Industrial Metal Detector Market Trends

Europe is expected to account for a dominant 28% of the industrial metal detector market share in 2025, driven by strong regulatory harmonization under the EU framework, which ensures consistent contamination control across member states.

Key regulations include EC 2023/915 on maximum contaminant levels, EC 333/2007 on sampling and analysis methods, and Directive 93/43/EG mandating HACCP-based self-control systems, with metal detectors as critical hazard control points.

Germany, the U.K., and France lead adoption due to mature manufacturing infrastructures and quality assurance systems. The U.K.’s 1,685 food processing plants contributed £ 30?billion in 2021, relying on metal detectors to meet a 93% consumer trust threshold.

Compliance with standards such as DIN ISO 9000, IFS, BRC, and ISO 22000 drives demand for high-precision, hygienic metal detection systems featuring traceability, validation, and washdown-compatible designs.

Asia Pacific Industrial Metal Detector Market Trends

The Asia Pacific is set to emerge as the fastest-growing regional market, driven by rapid industrial expansion, developing infrastructure, and an increased focus on security measures across the manufacturing sector.

The regional metal detector market is expanding at a CAGR of about 5.3% through 2032, driven by growing regulatory scrutiny, strong industrial expansion, and mounting security concerns. China, Japan, India, and ASEAN countries demonstrate particularly dynamic growth trajectories as manufacturers across food, pharmaceutical, and mining industries invest heavily in quality control procedures to guarantee product integrity and safety.

China's senior citizen population, growing by 10 million annually, creates expanding demand for pharmaceutical products requiring stringent contamination control, while rising disposable incomes among the middle class drive increased medical care spending and heightened quality expectations.

India's growing manufacturing sector benefits from government policies established by the Food Safety and Standards Authority of India (FSSAI) that regulate metal detector implementation across food processing operations. Japan contributes through advanced technological capabilities and mature manufacturing standards that emphasize precision detection systems.

Competitive Landscape

The global industrial metal detector market structure exhibits moderate consolidation with established global players maintaining significant market presence through extensive product portfolios, technological innovation, and comprehensive distribution networks.

Leading manufacturers deploy strategic initiatives including product innovations, partnerships with research institutions, and geographic expansion to strengthen competitive positions. Companies prioritize R&D investments to introduce cutting-edge detection systems incorporating artificial intelligence, multi-spectrum technology, and automated learning capabilities that differentiate their offerings in increasingly competitive markets.

Key differentiators employed by market leaders include superior washdown construction, exclusive auto-learn systems, comprehensive connectivity options, and industry-specific customization capabilities that address unique contamination challenges across food, pharmaceutical, chemical, and mining applications.

Emerging business model trends emphasize integration of metal detectors with complementary inspection technologies, remote monitoring capabilities, and predictive maintenance features that enhance overall equipment effectiveness and reduce total cost of ownership.

Key Market Developments

- In October 2025, Eriez showcased its latest inspection and magnetic separation technologies at Pack Expo 2025 in Las Vegas, including the PrecisionGuard X8 Metal Detector and SenseGuard X-ray Inspection Systems. The X8 detector offers high sensitivity across ferrous, nonferrous, and stainless-steel contaminants, featuring an intuitive touchscreen and auto-learn capabilities for ease of use. The X-ray systems provide high-resolution imaging and adaptable software to detect a wide range of foreign objects and product flaws, enhancing product safety and brand protection.

- In July 2025, Mettler-Toledo displayed its latest pharmaceutical manufacturing solutions at the PPMA Total Show 2025. The company presented advanced weighing, inspection, and analytical technologies aimed at enhancing production efficiency and ensuring regulatory compliance. Highlights included equipment designed to improve quality control, streamline processes, and support digital transformation in pharmaceutical manufacturing.

- In April 2025, Loma Systems introduced the IQ4M Metal Detector in North America, designed to enhance food safety by detecting contaminants while reducing false rejects. The system utilizes patented Variable Frequency and advanced Multi-Spectrum technologies for effective detection across various products including meat, bakery, and snacks. It features Dynamic Data Screen+ (DDS+) for improved signal analysis and Quick Recovery for faster product changeover, minimizing downtime.

Companies Covered in Industrial Metal Detector Market

- Mettler-Toledo International Inc.

- Eriez Manufacturing Co. Inc.

- Illinois Tool Works Inc.

- Anritsu Corporation

- Sesotec GmbH

- Mesutronic Gerätebau GmbH

- Thermo Fisher Scientific Inc.

- Fortress Technology Inc.

- Nikka Densok Limited

- Cassel Messtechnik GmbH

- Foremost Machine Builders Inc.

- Technofour Electronics Pvt. Ltd.

- Das Electronics

- CEIA S.p.A.

- Bunting Magnetics Co.

- Loma Systems Ltd.

- Minebea Intec GmbH

Frequently Asked Questions

The global industrial metal detector market size is projected to reach US$ US$ 322.2 million in 2025.

Market growth is primarily driven by stringent regulatory requirements from agencies such as the FDA, USDA, CFIA, and EFSA mandating contamination control, along with rising product recall incidents that increased by 114% in 2022, compelling manufacturers to invest in advanced detection systems to prevent financial losses and reputational damage.

The industrial metal detector market is poised to witness a CAGR of 4.7% from 2025 to 2032.

Key opportunities include integration of AI and smart sensor technologies in pharmaceutical applications and an increasing demand from mining and aggregates industries requiring protection for crushers and conveyor systems.

Leading market players include Mettler-Toledo International Inc., Thermo Fisher Scientific Inc., Eriez Manufacturing Co. Inc., and Illinois Tool Works Inc.