- Electric Mobility

- Hydrogen Buses Market

Hydrogen Buses Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Hydrogen Buses market by Technology (proton exchange membrane fuel cell, solid oxide fuel cell, phosphoric acid fuel cell, and others (alkaline fuel cell), Power Output (less than 150 kW, 150 to 250 kW, and more than 250 kW), Bus Type (single deck, double deck, and articulated deck), and Regional Analysis for 2026 - 2033

Hydrogen Buses Market Size and Trends Analysis

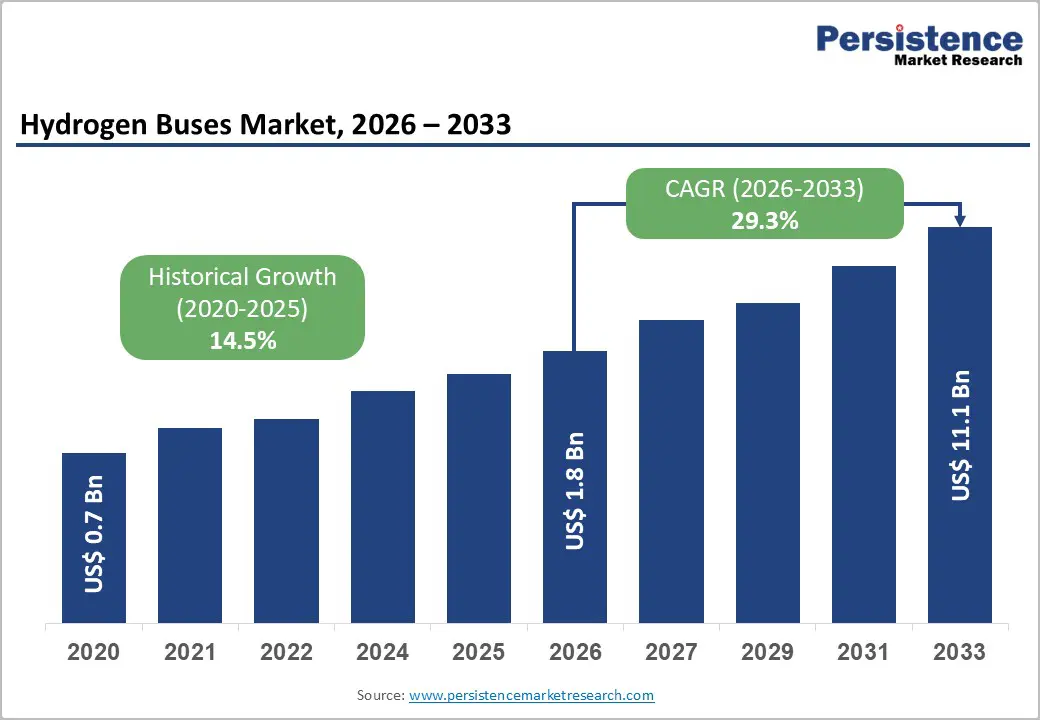

The global hydrogen buses market size is likely to be valued at US$ 1.8 billion in 2026 and is projected to reach US$ 11.1 billion by 2033, growing at a CAGR of 29.3% between 2026 and 2033. The market builds on a historical CAGR of 15.5% from 2020, supported by the rapid deployment of zero-emission heavy-duty vehicles (ZE-HDVs), policy-backed pilots, and large OEM product pipelines.

According to the International Council on Clean Transportation (ICCT), ZE?HDV sales in China reached 110,400 units in 2023, with an 8% share, while buses showed 17% zero-emission penetration, confirming strong structural momentum in bus decarbonization. At the same time, OEMs such as Wrightbus, Solaris, Hyundai, New Flyer, Yutong, and CaetanoBus are launching advanced hydrogen bus platforms with ranges above 300-550 km and refuelling times of 6-10 minutes, backed by long-term fuel cell supply agreements and regional industrial investments.

Key Industry Highlights:

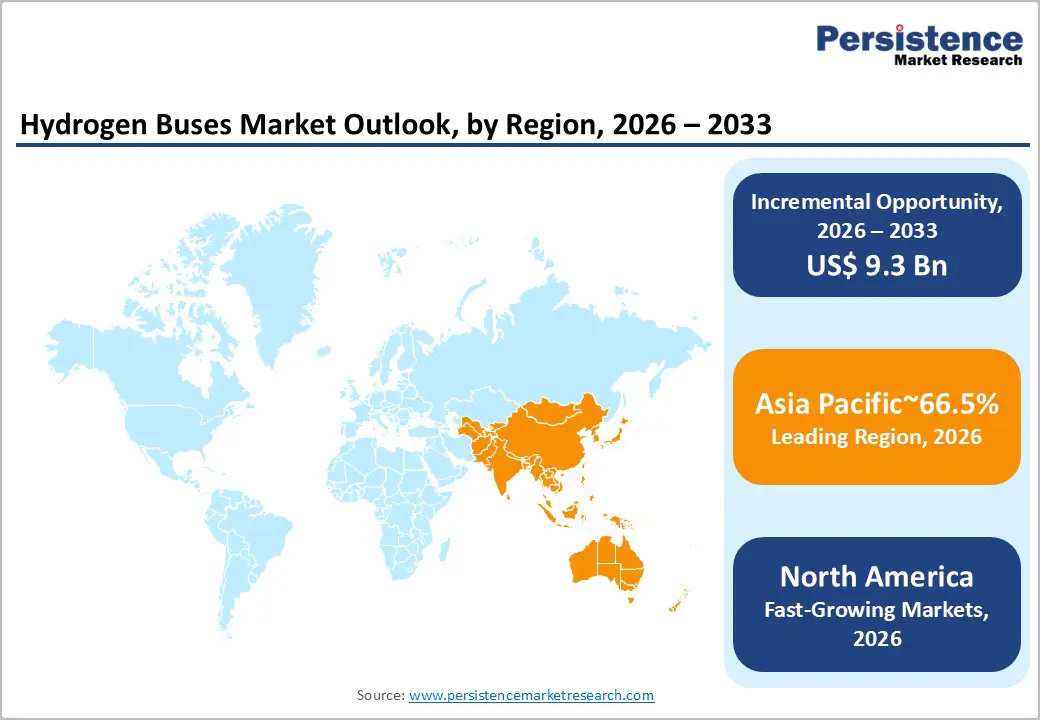

- Regional Leadership: Asia Pacific leads the global Hydrogen Buses Market with ~65.5% share in 2026, supported by large-scale deployments in China, Korea, and Japan and strong government hydrogen strategies.

- Fastest-Growing Market: Europe captures ~27.7% share in 2026 and is rapidly advancing due to EU climate policies, city-level clean air initiatives, and zero-emission bus programs

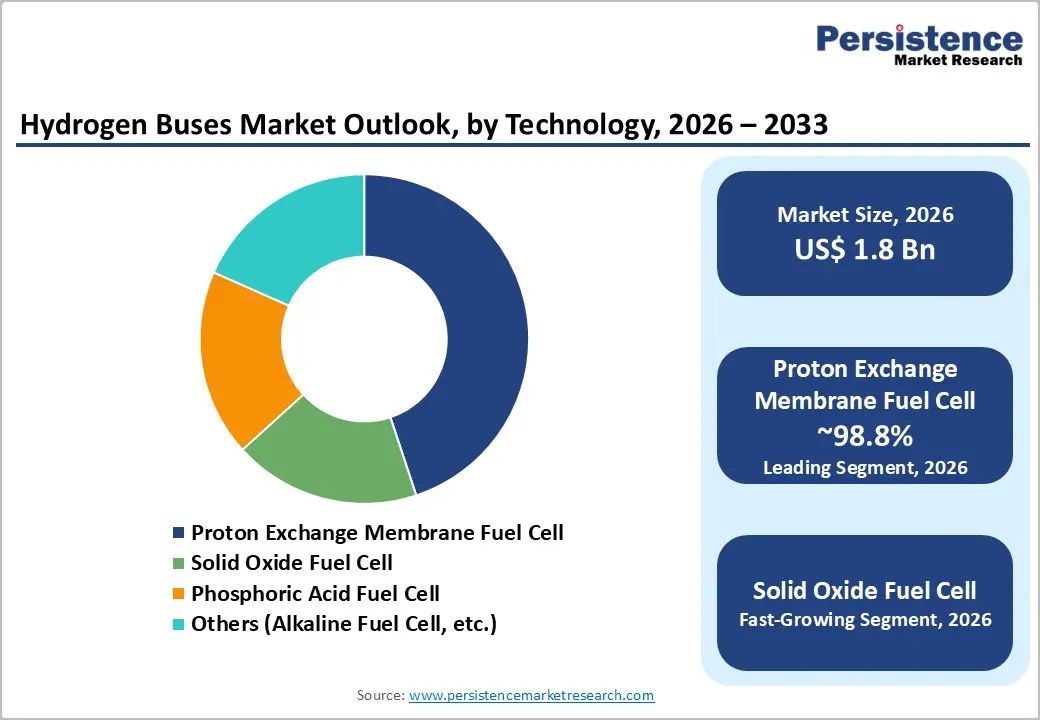

- Technology Dominance: Proton Exchange Membrane Fuel Cells (PEMFC) lead with ~98.8% market share in 2026, driven by suitability for bus duty cycles and widespread OEM adoption.

- Rapidly Rising Technology: Solid Oxide Fuel Cells (SOFCs) are the fastest-growing segment, offering higher efficiency and niche applications in high-temperature and auxiliary power applications.

- Leading Bus Type: Single-deck buses hold ~78.8% market share in 2026, dominating urban public transport networks worldwide.

- Fastest-Growing Bus Type: Double-deck and articulated hydrogen buses are expanding quickly to meet high-capacity urban and long-distance route demands.

| Key Insights | Details |

|---|---|

| Hydrogen Buses Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 11.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 29.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 14.5% |

Market Dynamics

Drivers - Government Regulations and Policy Support Driving the Adoption of Zero-Emission Transport Solutions

Government regulations and policy frameworks play a decisive role in shaping the adoption pathway for hydrogen buses by setting long-term decarbonization targets, defining compliance requirements, and enabling large-scale infrastructure planning. Across major economies, hydrogen fuel cell buses are increasingly positioned as a strategic solution for high-capacity, long-range public transport where battery-only systems face operational constraints. Clear policy direction reduces investment uncertainty for transit agencies, OEMs, and infrastructure developers, strengthening confidence in hydrogen-based mobility ecosystems.

In Europe, the European Commission’s Hydrogen Strategy and REPowerEU plan establish a robust policy foundation for hydrogen use in transport. The EU’s objective to produce and import 10 million tonnes of renewable hydrogen by 2030, alongside binding renewable hydrogen targets under the Renewable Energy Directive, directly supports the deployment of hydrogen buses in urban and intercity networks. Funding mechanisms such as the Important Projects of Common European Interest (IPCEI) on hydrogen, covering Hy2Tech, Hy2Use, and Hy2Infra, accelerate development across the hydrogen value chain, including refuelling infrastructure essential for bus fleets.

At the national level, governments are translating regional strategies into targeted mobility programs. The UK’s commitment to near-complete adoption of zero-tailpipe-emission vehicles by 2040 includes dedicated support for hydrogen fuel cell buses through schemes administered by the Office for Low Emission Vehicles (OLEV). Programs such as the FCEV Fleet Support Scheme, which offers funding of up to 75% for eligible fleets, directly address the cost and infrastructure barriers associated with hydrogen bus adoption, while also supporting refuelling station development.

Increasing Infrastructure Development for Hydrogen Refueling Stations Globally

The availability and geographic spread of hydrogen refueling stations (HRS) are foundational drivers of hydrogen bus deployment, as fleet operations depend on reliable, high-capacity fueling access. Hydrogen buses, unlike passenger vehicles, require stations capable of serving frequent refueling cycles, higher daily hydrogen throughput, and centralised depot-based operations. As governments and transit authorities prioritise zero-emission public transport, coordinated investment in hydrogen infrastructure has become a prerequisite for large-scale adoption of hydrogen buses.

Globally, hydrogen refueling infrastructure has reached about 1,150 operational stations, representing a 65% increase compared with 2021. Infrastructure deployment remains uneven, with China, Japan, and South Korea accounting for more than 850 stations combined, reflecting their early policy alignment between hydrogen mobility and industrial strategy. Europe hosts roughly 250 stations, while North America experienced a notable contraction in station counts over the past year, underscoring regional disparities in policy continuity, permitting frameworks, and operating economics.

Regulatory mandates are shaping the next phase of infrastructure rollout. In Europe, the Alternative Fuels Infrastructure Regulation (AFIR) requires hydrogen refueling stations every 200 km along the Trans-European Transport Network (TEN-T), a measure expected to enable more than 400 stations by 2030 and directly support long-distance and intercity hydrogen bus routes. In Asia, Japan and South Korea have each committed to deploying more than 600 hydrogen refueling stations by 2030, aligning public transit decarbonization with national hydrogen roadmaps.

Infrastructure deployment shows a clear linkage with hydrogen vehicle penetration in public and commercial transport. China leads global hydrogen bus and truck deployment, supported by dense refueling networks tied to logistics corridors and municipal fleets. Beyond road transport, hydrogen stations are increasingly designed to accommodate buses, trucks, and emerging off-road applications such as rail and port operations. For the hydrogen buses market, sustained investment in refueling infrastructure reduces operational risk, improves fleet utilisation, and anchors hydrogen buses within broader national and regional clean mobility systems.

Restraint - High capital intensity and infrastructure complexity

Hydrogen bus projects require substantial upfront investment in vehicles, refuelling stations, and supporting systems, which can slow adoption relative to diesel or battery-electric alternatives. Many European and North American fleets still depend on multi-million-euro or multi-million-dollar grants, green bonds, or national programs to finance hydrogen production and depot stations, as seen in German and Italian projects and U.S. deployments supported by FTA funding and California vouchers.

Operators face uncertainty about hydrogen prices, station utilisation, and long-term maintenance costs, particularly in smaller or less dense cities. These factors raise the risk of stranded assets and complicated procurement decisions, especially for agencies without strong fiscal backing.

Opportunity - National hydrogen missions and structured pilot programs

National hydrogen missions and structured pilot programs are emerging as practical pathways for introducing hydrogen buses into public transport systems under controlled, low-risk conditions. Governments are using pilots to validate vehicle performance, safety, refuelling logistics, and operating economics before committing to large-scale procurement. These initiatives align transport decarbonization goals with broader hydrogen production, storage, and distribution strategies.

India’s National Green Hydrogen Mission has sanctioned five pilot projects involving 37 hydrogen-powered buses and trucks (15 fuel cell, 22 hydrogen ICE) on 10 routes, supported by nine hydrogen refuelling stations and approximately INR 208 crore in public funding. Complementary initiatives include 15 Tata Motors PEM fuel cell buses awarded by Indian Oil Corporation in 2021 and subsequent deliveries of hydrogen fuel cell buses for Delhi-NCR trials, accumulating 300,000 km under Indian Oil’s real-world operations.

These programs provide a template for other emerging markets to structure hydrogen bus pilots around rigorous technical, safety, and economic validation. For OEMs, integrators, and infrastructure providers, participation offers reference projects, localised data sets, and the ability to shape standards for hydrogen quality, safety, and operational procedures. Once pilots confirm technical feasibility and cost trajectories, governments can move to scaled tenders linking hydrogen bus adoption with domestic manufacturing, skills development, and green hydrogen production targets.

Diversification into double?deck, articulated, and long-distance formats

Rising demand for higher-capacity and long-range transport solutions is driving innovation in hydrogen bus platforms. Wrightbus has evolved from early hydrogen double-deck deployments to the StreetDeck Hydroliner Gen 2.0 and is committing £25 million to zero-emission R&D, including £5 million for a hydrogen-powered coach with a range of up to 1,000 km on a single refuel. Daimler Buses has launched the H? Coach (Setra S 517 HD) with an 800 km range for test drives, indicating a clear path toward series production of hydrogen coaches.

Solaris has introduced the Urbino 18 hydrogen articulated bus, awarded Bus of the Year 2025, while CaetanoBus offers hydrogen variants in 8.5 m, 12 m, and 18 m configurations, including BRT-style platforms. These developments allow hydrogen buses to address dense urban corridors, intercity routes, tourist networks, and high-altitude or steep-gradient environments, as demonstrated by Hyundai’s UNIVERSE Fuel Cell coach operating at elevations up to 2,080 meters with 24% gradients in NEOM. As operators look beyond depot-based city services to regional and long-distance applications, diversified hydrogen bus platforms offer a compelling solution set.

Category-wise Analysis

Technology Insights

Proton Exchange Membrane Fuel Cell (PEMFC) is the clear technology leader in the global hydrogen buses market, accounting for about 98.8% of demand in 2026. This dominance reflects PEM’s proven suitability for bus duty cycles, characterised by fast start-up, high power density, and compatibility with compressed hydrogen storage. Major OEMs, including Solaris, Wrightbus, Hyundai, Tata Motors, Yutong, King Long, Ankai, CaetanoBus, and New Flyer, deploy PEM stacks from established suppliers such as Ballard, Toyota, and Hyundai’s HTWO, backed by industrial-scale agreements, such as Solaris’s 1,000-engine LTSA with Ballard.

Solid Oxide Fuel Cells (SOFC) represent the fastest-advancing technology segment, even though actual bus deployments remain limited compared with PEM. SOFC systems offer higher electrical efficiency and can utilise different fuel streams when coupled with reformers, creating potential for specialised applications where high-temperature operation and integrated heat recovery add value. In the medium term, SOFCs are likely to complement PEM in niche roles such as auxiliary power or specific high-efficiency routes rather than replace it.

Power Output Insights

Hydrogen buses with power output below 150 kW hold the largest share of the global Hydrogen Buses Market, representing around 50.8% of demand in 2026. This power band is well aligned with standard 10-12 meter city buses that operate on urban and suburban routes with frequent stops and moderate gradients. Typical configurations combine 70-100 kW fuel cell stacks with high-power batteries and efficient electric drivetrains, as seen in many Solaris Urbino 12, Tata Motors FCEV buses, and Chinese city bus platforms. This segment benefits from high fleet volumes, well-understood duty cycles, and the ability to share core components across multiple OEMs.

The 150 to 250 kW segment is the fastest-advancing power band, reflecting the needs of articulated, double-deck, and long-distance coach applications. New Flyer’s Xcelsior CHARGE FC buses employ high-output fuel cell modules paired with robust drivetrains suited for 40-foot heavy-duty transit operations, while Hyundai’s Elec City and Universe buses leverage a 180-kW fuel cell system and large hydrogen storage capacity to deliver ranges of up to 550 km. As cities and regions deploy hydrogen buses on BRT corridors, airport links, and intercity services, demand in this power category will continue to accelerate, anchored by both European and Asian platforms.

By Type Insights

Single-deck buses constitute the leading bus type in the global Hydrogen Buses Market, accounting for about 78.8% of demand in 2026. This dominance reflects their position as the standard vehicle format for urban public transport networks worldwide. Large orders such as 137 Solaris Urbino 12 hydrogen buses for Bologna and Ferrara, fleets in German cities including Essen and Rostock, and numerous 12-meter deployments in Chinese and Indian cities illustrate the central role of single-deck buses in policy-driven decarbonization programs. OEMs have optimised single-deck hydrogen platforms in terms of passenger capacity, low-floor accessibility, range, and refuelling time, making them the preferred technology demonstrator for zero-emission bus initiatives.

Double-deck buses represent the fastest-advancing segment, responding to demand for higher capacity on constrained urban corridors. Wrightbus’s StreetDeck Hydroliner, now upgraded to Gen 2.0 with 300+ mile range, 8-minute refuelling, and improved cost metrics, has positioned the company as a leader in double-deck hydrogen bus supply across the UK and, increasingly, continental Europe. Similar capacity-enhancing formats, including articulated hydrogen buses seeking to manage peak demand efficiently while maintaining zero-emission operations.

Regional Insights and Trends

North America Hydrogen Buses Market Trends

North America accounts for approximately 19.3% of the global market, driven primarily by the United States and Canada. In recent years, agencies have moved from pilots to larger fleet commitments. The Orange County Transportation Authority (OCTA) placed an order for 40 New Flyer Xcelsior CHARGE FC hydrogen buses as part of a 50-bus zero-emission procurement, supported by U.S. Federal Transit Administration (FTA) funding and state-level programs. San Mateo County Transit (SamTrans) in California ordered 108 hydrogen fuel cell buses, the largest single fuel cell bus order in New Flyer’s history, backed by California HVIP vouchers and local funds. These deployments are anchored by one of the largest hydrogen fueling stations for transit buses in the U.S., located in Orange County.

Key performance metrics in North America focus on operational reliability, range under mixed urban and highway conditions, and emissions reductions compared with diesel fleets. Some fleets report greenhouse gas reductions of 85-175 tons of CO2 per bus per year for hydrogen fuel cell buses, supporting state and federal climate goals. The regulatory environment-especially in California-mandates the phase-out of fossil-fuel buses under the Innovative Clean Transit regulation, encouraging agencies to evaluate both battery-electric and hydrogen solutions.

The competitive landscape is led by New Flyer, with contributions from foreign OEMs and technology providers. Investment opportunities include regional green hydrogen production facilities, corridor-based refuelling hubs, and fleet-as-a-service models that bundle vehicles, fuel, and maintenance.

Asia Pacific Hydrogen Buses Market Trends

Asia Pacific accounts for around 65.5% of the global market, reflecting large-scale deployments and strong industrial policies. ICCT reports that in 2023, China recorded 110,400 ZE?HDV sales, with ZE-HDVs achieving an 8% market share, and buses recording 17% zero-emission penetration, making them the most electrified heavy?duty subgroup. ZE adoption is highest in leading cities such as Shenzhen, Shanghai, Chengdu, and Beijing, where local governments combine purchase subsidies, operational incentives, and environmental regulations to support large new-energy bus fleets. Hydrogen buses from Yutong, Zhongtong, King Long, Ankai, and other domestic OEMs have been deployed for major events.

In Korea, Hyundai has surpassed 1,000 cumulative sales of Elec City FCEV buses. The regulatory and industrial environment is characterised by national hydrogen strategies, fuel cell industrial bases, and large-scale demonstration zones. Investment trends include Hyundai’s KRW 930 billion fuel cell plant in Ulsan, municipal hydrogen industrial parks, and export-oriented bus programs targeting Asia, the Middle East, and Europe. Competitive dynamics favour domestic champions, but foreign suppliers of components and stacks (e.g., Ballard) participate through partnerships and technology licensing.

Europe Hydrogen Buses Market Trends

Europe represents around 27.7% of the global hydrogen buses market, driven by EU climate policies, national zero-emission bus programs, and city-level clean air strategies. Solaris has delivered over 200 Urbino hydrogen buses across 10+ countries, with 370 units operating in 31 cities and nearly 500 more on order, supported by a 1,000-engine LTSA with Ballard. Key contracts include 137 Urbino 12 buses for Bologna and Ferrara in Italy and 19 hydrogen buses for Ruhrbahn in Essen. Poland’s Konin will receive five Urbino 18 articulated hydrogen buses, marking its domestic debut.

Regulatory support comes from EU CO standards, the Clean Vehicles Directive, and low-emission zones, encouraging zero-emission bus adoption. The competitive landscape includes Solaris, Wrightbus, CaetanoBus, IVECO BUS, Daimler Buses, and Yutong. Investment opportunities focus on integrated solutions, such as CaetanoBus’s EMaaS model, cross-border partnerships, green hydrogen production, depot refueling infrastructure, and long-term fleet service agreements.

Competitive Landscape

The competitive landscape of the global hydrogen buses market is best described as consolidated with oligopolistic characteristics, where a handful of established manufacturers and specialised suppliers dominate commercial deployments and technological leadership. Major players such as Hyundai Motor Company, Wrightbus, Solaris, Beiqi Foton Motor Co., Ltd., Zhengzhou Yutong Bus Co., Ltd., NFI Group Inc., and King Long lead product development, secure large fleet contracts, and form strategic partnerships with fuel-cell suppliers and public transport agencies.

Competition centres on fuel-cell system integration, vehicle range and reliability, total cost of ownership, and after-sales support; manufacturers differentiate through local service networks, modular platforms, and bespoke integration with hydrogen refuelling partners. High capital intensity, certification requirements, and limited refuelling infrastructure create significant entry barriers, reinforcing the position of incumbent OEMs while encouraging alliances with technology suppliers and operators.

Regional specialisation is evident in European and North American transit tenders, favoring Wrightbus, Solaris, and NFI, while Chinese manufacturers like Yutong, King Long, and Beiqi Foton dominate large domestic procurement and export programs. For the Global Hydrogen Buses Market, strategic wins increasingly hinge on demonstrated fleet performance, supply-chain resilience for fuel-cell stacks, and the ability to offer turnkey solutions that reduce operator risk.

Key Industry Developments:

- Nov 11, 2025 - Solaris Bus & Coach: Solaris will deliver 5 Urbino 18 hydrogen-powered articulated buses to Konin, Poland, marking the model's debut in the country. The buses feature a 10-kW hydrogen fuel cell, 240-kW traction motor, eight composite hydrogen tanks, and High-Power batteries, offering fully zero-emission operation, over 600-km range, high passenger capacity, and short refueling times. This delivery reinforces Solaris’ leadership in hydrogen bus deployment across Europe, following previous deliveries of 370 hydrogen buses to 31 cities, with nearly 500 additional units on order.

- On April 15, 2025, Wrightbus committed £25 million to zero-emission R&D, including £5 million for a new hydrogen-powered coach designed to deliver up to 1,000 km range on a single refuel, positioning the company to advance long-distance hydrogen mobility with diesel-competitive performance.

Companies Covered in Hydrogen Buses Market

- Wrightbus

- Solaris

- Tata Motors Ltd.

- Hyundai Motor Company

- Beiqi Foton Motor Co. Ltd.

- NFI Group Inc.

- Zhengzhou Yutong Bus Co., Ltd.

- Daimler Buses

- Salvador Caetano Group

- Zhongtong Bus Holding

- IVECO Bus

- Zhejiang Geely New Energy Commercial Vehicle Group Co. Ltd.

- King Long

- Anhui Ankai Automobile Co.,Ltd

- CHERY & WANDA GUIZHOU BUS CO.,LTD

Frequently Asked Questions

The global hydrogen buses market is projected to be valued at US$ 1.8 Bn in 2026.

The Proton Exchange Membrane Fuel Cell segment is expected to account for approximately 98.8% of the global Hydrogen Buses market by Technology in 2026.

The hydrogen buses market is expected to witness a CAGR of 29.3% from 2026 to 2033.

The global hydrogen buses market is primarily driven by supportive government policies for zero-emission transport and the rapid expansion of hydrogen refueling infrastructure.

Key market opportunities in the global hydrogen buses market include national hydrogen missions and structured pilot programs, as well as diversification into double‑deck, articulated, and long‑distance bus formats.

The key players in the Hydrogen Buses market include Hyundai Motor Company, Wrightbus, Solaris, Beiqi Foton Motor Co. Ltd., Zhengzhou Yutong Bus Co., Ltd., NFI Group Inc., and King Long.