- Food Ingredients & Additives

- Corn Starch Derivatives Market

Corn Starch Derivatives Market Size, Share, and Growth Forecast, 2025 - 2032

Corn Starch Derivatives Market by Product Type (Corn Starch, Corn Starch Derivatives, Corn Oil, Corn Flour, Corn Meal/Flakes/Grits, Corn Protein), Application (Food & Beverage, Animal Feed, Paper and Board, Pharmaceutical, Biodiesel, Textiles, Others), and Regional Analysis for 2025 - 2032

Corn Starch Derivatives Market Size and Trends Analysis

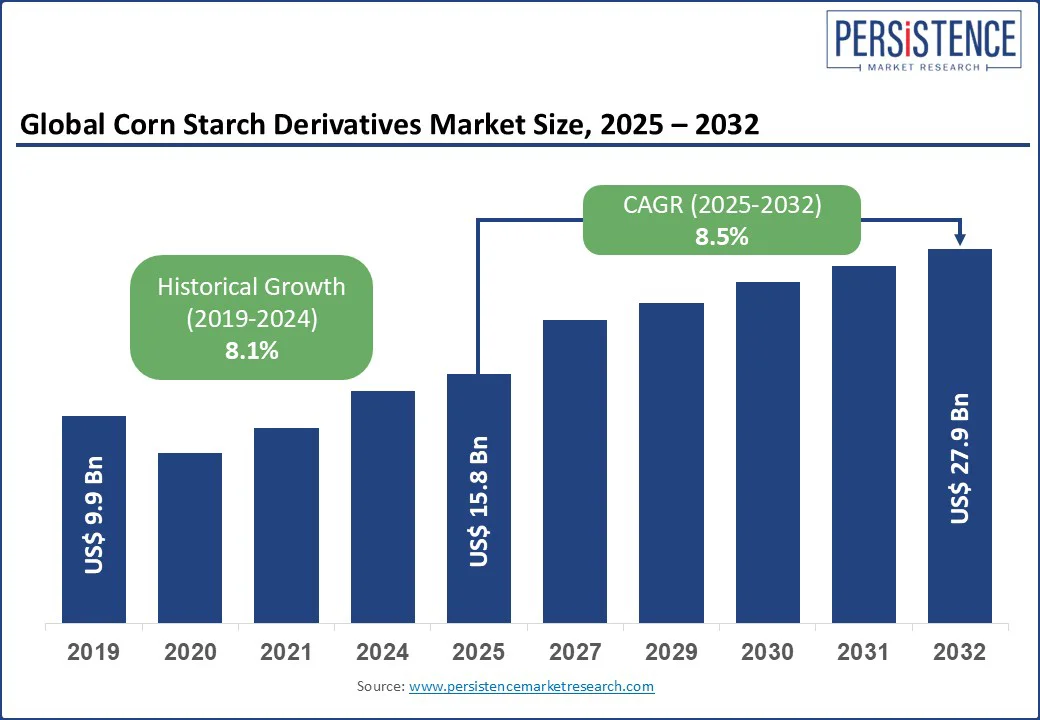

The global corn starch derivatives market size is projected to rise from US$15.8 Bn in 2025 to US$27.9 Bn by 2032, registering a CAGR of 8.5% during the forecast period from 2025 to 2032.

The sector has experienced steady growth, driven by the increasing demand for processed and convenience foods, advancements in starch modification technologies, and the expanding use of corn starch derivatives in non-food applications such as pharmaceuticals and biodiesel.

The sector is propelled by the versatility of corn starch derivatives, which offer functional properties such as thickening, stabilizing, and texturizing, catering to a wide range of industrial needs with cost-effective and sustainable solutions.

Key Industry Highlights:

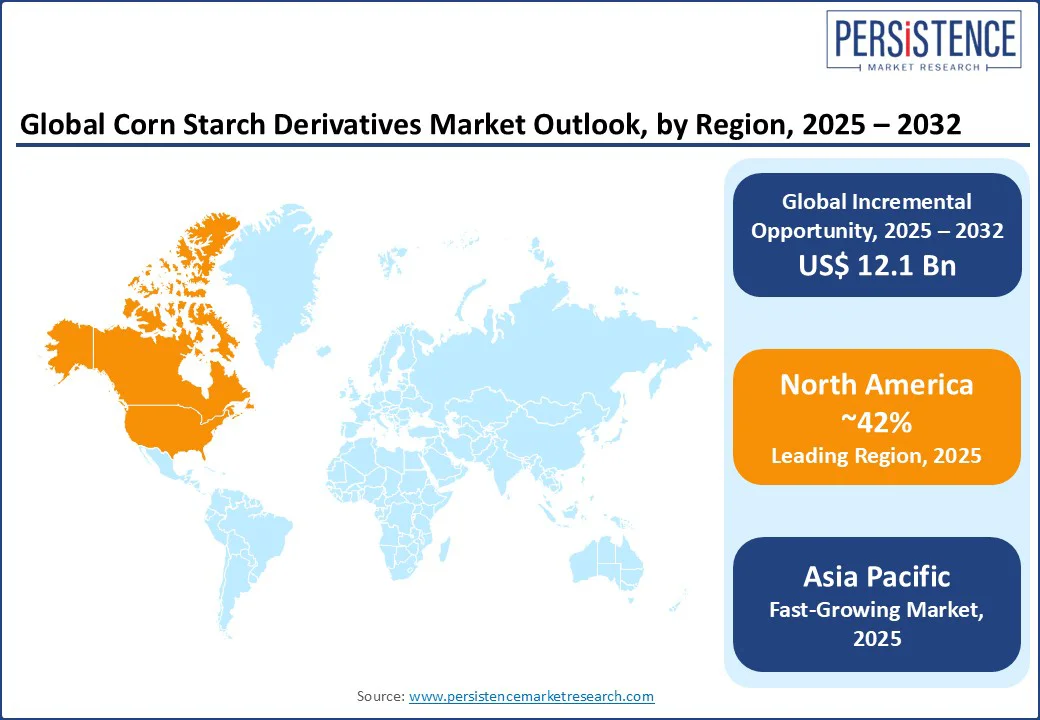

- Leading Region: North America, holding a 42% market share in 2025, driven by a robust food processing industry, advanced technological infrastructure, and high consumer demand for convenience foods.

- Fastest-growing Region: Asia Pacific, fueled by rapid industrialization, growing population, and increasing adoption of corn starch derivatives in food, pharmaceutical, and textile industries in countries such as China and India. Europe is advancing through sustainable production initiatives and increasing demand for clean-label and plant-based products.

- Dominant Product Type: Corn starch derivatives, commanding nearly 60% market share, reflecting the recurring demand for modified starches in food and non-food applications.

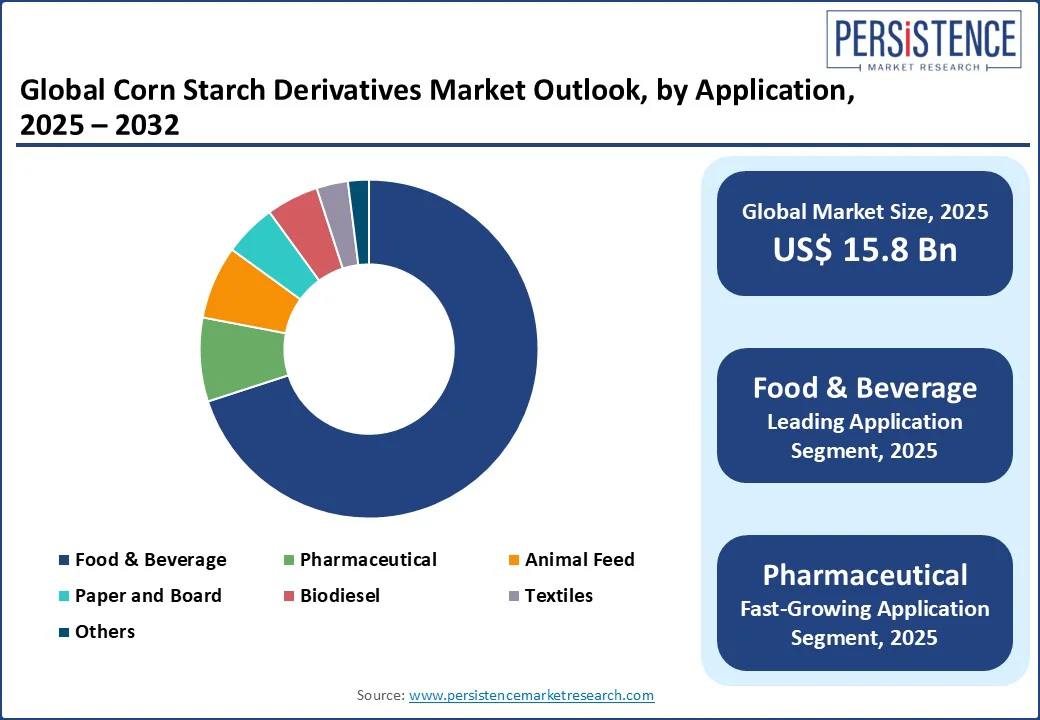

- Leading Application: Food & Beverage, accounting for 70% of global market revenue, driven by the widespread use of corn starch derivatives in processed foods, beverages, and bakery products.

|

Global Market Attribute |

Key Insights |

|

Corn Starch Derivatives Market Size (2025E) |

US$15.8 Bn |

|

Market Value Forecast (2032F) |

US$27.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.1% |

Market Dynamics

Driver - Rising Demand for Convenience Foods and Clean-Label Products

The rising demand for convenience foods and clean-label products is a significant driver of the corn starch derivatives market. Busy lifestyles, urbanization, and increasing disposable incomes are fueling the consumption of ready-to-eat meals, snacks, bakery products, and processed beverages, all of which rely on corn starch derivatives for texture, stability, and shelf-life enhancement. At the same time, health-conscious consumers are pushing brands toward clean-label formulations that avoid artificial additives while maintaining quality and functionality.

Corn starch derivatives, particularly modified starches and maltodextrin, align well with these trends as they are derived from natural sources and can be processed to meet clean-label requirements. Food manufacturers are increasingly reformulating products to include simple, recognizable ingredients while still delivering convenience and taste.

Additionally, the versatility of corn starch derivatives allows their use in gluten-free and low-fat products, further expanding their appeal. For instance, companies such as Cargill have launched clean-label starch solutions to cater to the growing demand for minimally processed, plant-based ingredients in bakery and dairy products. This convergence of convenience and clean-label demand is driving robust growth in the domain.

Restraint - Raw Material Price Volatility and Supply Chain Challenges

Raw material price volatility and supply chain challenges pose significant restraints to the corn starch derivatives market. The production of these derivatives depends heavily on corn, whose prices are influenced by factors such as weather conditions, crop yields, global demand, and trade policies. Fluctuations in corn prices can directly impact production costs, making pricing strategies difficult for manufacturers. Additionally, supply chain disruptions, such as transportation bottlenecks, labor shortages, and geopolitical tensions, can delay raw material procurement and product distribution.

The COVID-19 pandemic highlighted these vulnerabilities, with lockdowns and logistics constraints affecting corn availability and delivery schedules. In some regions, competition between food, feed, and biofuel industries for corn further strains supply and drives up prices.

For instance, in 2022, drought conditions in the U.S. Midwest reduced corn yields, leading to price surges that significantly impacted starch derivative manufacturers. Similarly, the Russia-Ukraine conflict disrupted global grain trade, tightening supply and pushing raw material costs higher. These uncertainties hinder long-term planning, profit margins, and the ability to maintain a stable supply for end-use industries.

Opportunity - Expansion in Bio-Based Applications and Sustainability Initiatives

The expansion in bio-based applications and sustainability initiatives presents a significant opportunity for the corn starch derivatives market. With increasing global emphasis on reducing carbon footprints and dependence on fossil fuels, industries are turning to renewable, plant-based materials.

Corn starch derivatives serve as a sustainable feedstock for producing biodegradable plastics, bio-based packaging, adhesives, and biochemicals. This aligns with circular economy goals and growing consumer demand for eco-friendly products.

Governments worldwide are introducing incentives, subsidies, and regulations favoring biodegradable and compostable materials, further boosting market potential. For instance, the European Union’s Single-Use Plastics Directive is encouraging packaging manufacturers to adopt bio-based alternatives. Similarly, Cargill’s investment in its U.S.-based bioplastics plant in 2023 aims to increase the production of PLA (polylactic acid) derived from corn starch to meet rising demand for sustainable materials.

In addition, innovations in processing technologies are enhancing the performance and cost-effectiveness of corn-based materials, making them competitive with petroleum-derived counterparts. The convergence of regulatory support, technological advancement, and corporate sustainability commitments positions corn starch derivatives as a key player in the transition toward greener industrial solutions across multiple sectors.

Category-wise Analysis

Product Type Insights

Corn starch derivatives dominate and are expected to account for approximately 60% share in 2025. The leadership stems from the recurring demand for modified starches such as maltodextrin, cyclodextrin, and glucose syrup, which are essential for applications in food, pharmaceuticals, and industrial processes.

The versatility of corn starch derivatives, which can be tailored for specific functionalities such as thickening, stabilizing, or binding, ensures steady demand across multiple industries. The increasing adoption of clean-label and gluten-free products further drives the dominance of this segment, as corn starch derivatives meet consumer preferences for natural ingredients.

Corn Oil is the fastest-growing product type from 2025 to 2032. This growth is driven by rising demand in the food industry for healthier cooking oils and in the industrial sector for bio-based lubricants and biodiesel. Innovations in extraction technologies have improved the yield and quality of corn oil, making it a cost-effective alternative to other vegetable oils.

Application Insights

Food & Beverage applications accounted for 70% of the global corn starch derivatives market revenue. This segment’s dominance is driven by the widespread use of corn starch derivatives in processed foods, beverages, and bakery products, where they serve as thickeners, stabilizers, and texturizers.

The global rise in demand for convenience foods, coupled with the increasing popularity of plant-based and gluten-free products, has solidified the food and beverage sector’s leadership. Large-scale food processing initiatives, such as those supported by companies such as ADM and Cargill, further drive demand for corn starch derivatives in this segment.

Pharmaceutical applications are the fastest-growing, driven by the increasing use of corn starch derivatives as excipients in drug formulations and as carriers in drug delivery systems. The pharmaceutical industry’s focus on precision medicine and the development of novel drug delivery mechanisms, such as starch-based encapsulation, is accelerating adoption. For example, modified starches such as cyclodextrin are used to enhance the solubility and stability of active pharmaceutical ingredients, supporting growth in this segment.

Regional Insights

North America Corn Starch Derivatives Market Trends

North America, projected to hold a 42% share in 2025, is a dominant player in the corn starch derivatives market, supported by its robust food processing industry, advanced technological infrastructure, and strong consumer demand for convenience foods.

The U.S. and Canada lead the region with large-scale corn production, ensuring a reliable supply of raw materials at competitive costs. The well-developed food and beverage sector utilizes corn starch derivatives extensively in bakery, confectionery, beverages, dairy, and ready-to-eat meals for texture, stability, and shelf-life enhancement.

Growing health awareness and demand for clean-label products are further driving reformulation efforts, with starch derivatives serving as natural, functional ingredients. For instance, Cargill and Ingredion have invested in clean-label starch innovations to meet evolving consumer preferences.

Beyond food, industrial applications in paper, pharmaceuticals, textiles, and bio-based plastics add to market expansion. Strong R&D capabilities, supportive trade policies, and sustainability initiatives position the region for continued growth.

Europe Corn Starch Derivatives Market Trends

Europe’s corn starch derivatives market is characterized by strong demand from the food and beverage, paper, and pharmaceutical industries, driven by the region’s emphasis on product quality, sustainability, and regulatory compliance.

The sector benefits from well-established processing facilities and advanced manufacturing technologies, particularly in countries such as Germany, France, and the Netherlands. Strict EU food safety regulations and consumer preference for clean-label, non-GMO, and natural ingredients are encouraging the adoption of corn starch derivatives in bakery, confectionery, dairy, and beverage products for texture, viscosity, and stability enhancement.

For instance, European food manufacturers are increasingly replacing synthetic additives with modified starches to meet clean-label standards. Additionally, the region’s push toward a circular economy and reduced plastic use is fostering bio-based applications such as biodegradable packaging. Growth is also supported by innovations in specialty starches tailored for niche applications. Overall, Europe’s strong regulatory framework and sustainability goals position it as a key market for corn starch derivatives.

Asia Pacific Corn Starch Derivatives Market Trends

The Asia Pacific corn starch derivatives market is witnessing strong growth, fueled by rapid industrialization, a growing population, and expanding applications across food, pharmaceutical, and textile industries. Countries such as China and India are at the forefront, driven by rising disposable incomes, urbanization, and increasing demand for processed and convenience foods.

In the food sector, corn starch derivatives are widely used in bakery, confectionery, beverages, and ready-to-eat meals for their thickening, stabilizing, and texturizing properties. For instance, the booming bakery and snack markets in India are significantly increasing the demand for modified starches.

The pharmaceutical industry also leverages these derivatives for tablet binding and coating, while the textile sector uses them for fabric finishing and sizing. Supportive government policies promoting domestic manufacturing and the availability of abundant raw materials further enhance regional production capacity. Continuous advancements in processing technology and growing export opportunities position the Asia Pacific as a high-potential and competitive market.

Competitive Landscape

Intense competition, regional expansion strategies, and a focus on innovation in product development characterize the Global corn starch derivatives market. Key companies compete on cost-efficiency, product functionality, and sustainability. ADM and Cargill lead with significant R&D investments, with ADM allocating over $150 million annually to develop innovative starch solutions.

Ingredion advances its clean-label portfolio, while Roquette Frères focuses on sustainable and bio-based applications. Emerging technologies, such as enzyme-based starch modification, add to the competitive rivalry. Partnerships with food and pharmaceutical companies, along with investments in sustainable production, enhance market positioning.

Key Developments

- In February 2024, Ingredion introduced Novation® Indulge 2940, the first non-GMO functional native corn starch designed for dairy and dairy-alternative products. This clean-label starch offers improved texture, mouthfeel, and natural labeling benefits, with cost-efficiency gains in formulations.

- In March 2025, Cargill inaugurated a new corn milling plant in Gwalior, Madhya Pradesh, in collaboration with Saatvik Agro Processors. This facility currently produces 500 tons per day of starch derivatives, serving sectors such as confectionery, dairy, and infant formula, thereby strengthening supply chain efficiency and market reach in Northern and Western India.

Companies Covered in Corn Starch Derivatives Market

- ADM

- Cargill

- Ingredion

- Tate & Lyle

- Agrana Group

- Roquette Frères

- Wacker Chemie AG

- National Starch and Chemical Company

- Ashland

- Fibersol

Frequently Asked Questions

The global Corn Starch derivatives market is projected to reach US$ 15.8 Bn in 2025.

Rising demand for convenience foods and clean-label products, along with government-backed sustainability initiatives, are key drivers.

The Corn Starch Derivatives market is poised to witness a CAGR of 8.5% from 2025 to 2032.

Expansion of corn starch derivatives in bio-based applications, such as biodegradable plastics and biofuels, is a key opportunity.

ADM, Cargill, Ingredion, Tate & Lyle, and Roquette Frères are key players.