- Industrial Machinery

- Material Handling Equipment Market

Material Handling Equipment Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Material Handling Equipment Market Equipment Type (Conveyor Systems & Palletizers, Forklifts, Cranes & Hoists, AMRs & AGVs, Industrial Trucks, Automated Storage and Retrieval Systems, Others), Industry (Automotive, Food & Beverages, Construction, Consumer Goods & Electronics, E-commerce, Aerospace, Others), and Region Analysis 2026 - 2033

Material Handling Equipment Market Share and Trends Analysis

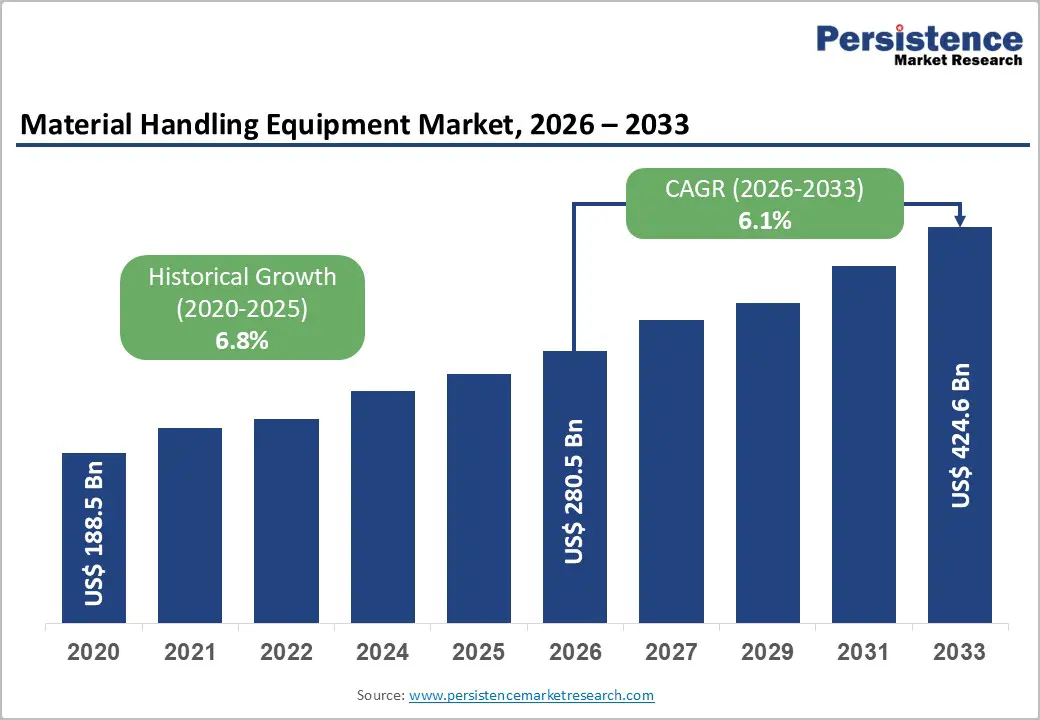

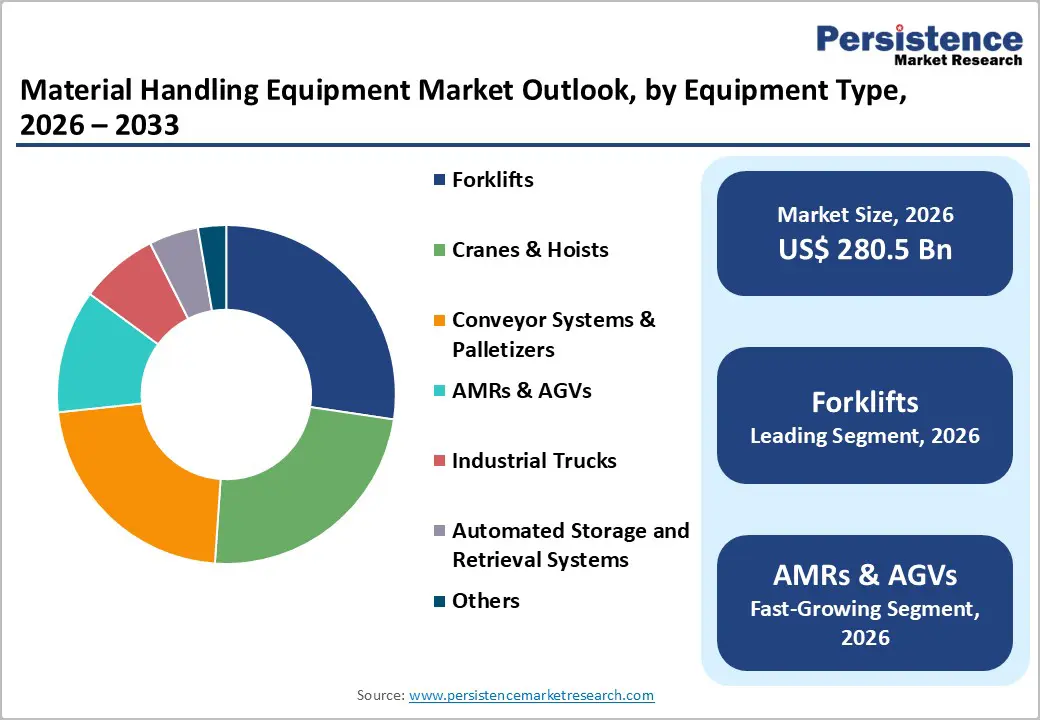

The global material handling equipment market size is projected to be at US$ 280.5 billion in 2026 and is anticipated to reach US$ 424.6 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

The market expansion is driven by accelerating e-commerce logistics infrastructure investments, Industry 4.0 adoption mandating automated warehouse solutions, and supply chain resilience initiatives following global disruptions. Technological convergence of robotics, artificial intelligence, and Internet of Things in material handling systems is enhancing operational efficiency and driving replacement cycles across manufacturing and distribution facilities.

Key Industry Highlights:

- Forklifts dominate with 27% market share, while AMRs & AGVs represent the fastest-growing segment at 9.6% CAGR, driven by warehouse automation adoption and flexible deployment capabilities.

- Automotive leads Industry industries with 19% market share, with E-commerce growing fastest at 10.8% CAGR due to fulfillment infrastructure expansion and same-day delivery requirements.

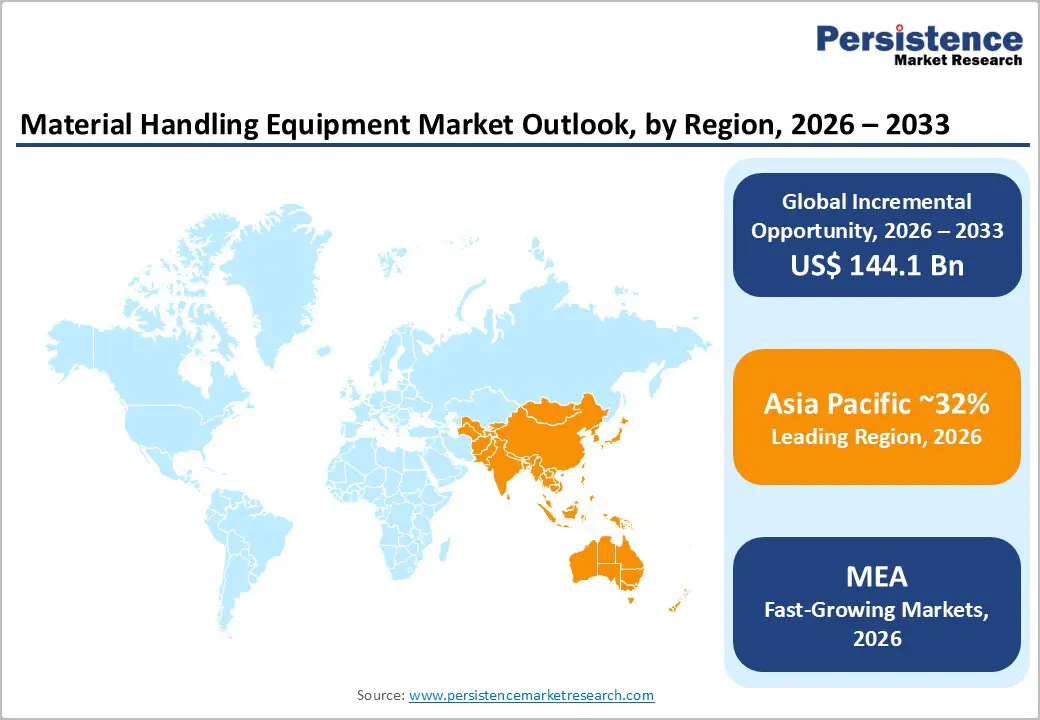

- Asia Pacific holds approximately 32% global market share as the largest regional market, while Europe maintains 30% share driven by advanced manufacturing and Industry 4.0 adoption.

- North America grows at 5.3% CAGR supported by e-commerce investments, nearshoring manufacturing expansion, and warehouse automation addressing labor shortages.

- Strategic developments emphasize electrification initiatives, autonomous mobile robot deployments, and integrated automation solutions combining equipment, software, and service offerings.

- Market growth driven by e-commerce proliferation requiring automated fulfillment capabilities, Industry 4.0 integration across manufacturing sectors, and supply chain resilience initiatives promoting nearshoring and warehouse network optimization.

| Key Insights | Details |

|---|---|

|

Material Handling Equipment Market Size (2026E) |

US$ 280.5 Billion |

|

Market Value Forecast (2033F) |

US$ 424.6 Billion |

|

Projected Growth CAGR (2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

6.8% |

Market Dynamics Analysis

Drivers - E-commerce Proliferation and Warehouse Automation Imperatives

Global e-commerce sales surpassed $6.3 trillion in 2024 according to the United Nations Conference on Trade and Development, representing 22% of total retail transactions and necessitating sophisticated fulfillment infrastructure. The U.S. Census Bureau reports online retail grew 42% between 2020-2024, compelling logistics operators to deploy automated material handling systems achieving processing speeds exceeding 1,000 units per hour. Amazon alone operates over 175 million square feet of warehouse space globally, with 75% incorporating advanced automation including autonomous mobile robots, automated storage and retrieval systems, and AI-powered sorting equipment. The International Warehouse Logistics Association projects the automated warehouse market value reaching ~$51 billion by 2028, with material handling equipment representing 60% of capital expenditures. This structural shift toward omnichannel fulfillment, same-day delivery expectations, and labor cost optimization creates sustained demand for advanced conveyor systems, AMRs, and automated storage solutions across retail, third-party logistics, and consumer goods sectors.

Industry 4.0 Integration and Smart Manufacturing Adoption

Manufacturing sector digitalization initiatives are fundamentally transforming production environments, with the World Economic Forum identifying 132 lighthouse factories implementing advanced Industry 4.0 technologies, including connected material handling systems. Germany's Federal Ministry for Economic Affairs reports that 68% of industrial manufacturers have adopted smart factory components, with material handling automation representing priority investment areas. The International Federation of Robotics documents that global industrial robot installations exceeded 553,000 units in 2023, with collaborative mobile robots and automated guided vehicles increasingly integrated into flexible manufacturing cells. China's Ministry of Industry and Information Technology targets 70% automation rates across key manufacturing sectors by 2030, driving material handling equipment modernization across automotive, electronics, and consumer goods production facilities. Smart material handling systems incorporating real-time tracking, predictive maintenance analytics, and adaptive routing algorithms improve throughput efficiency by 25-35% while reducing operational costs, accelerating replacement of legacy equipment and expanding market opportunities across established industrial economies.

Restraints - High Capital Investment Requirements and Extended Payback Periods

Advanced material handling systems require substantial upfront capital investments ranging from $2-15 million for automated warehouse installations, creating adoption barriers particularly among small and medium-sized enterprises. Automated storage and retrieval systems, autonomous mobile robot fleets, and integrated conveyor networks involve complex implementation timelines averaging 18-24 months from design through commissioning. The typical payback period for warehouse automation investments extends 4-7 years, with ROI heavily dependent on throughput volumes, labor cost structures, and operational reliability. Economic uncertainty and rising interest rates in 2024-2025 have constrained capital availability, with industrial equipment financing costs increasing 200-300 basis points. Small warehouse operators and regional manufacturers often cannot justify automation investments given throughput limitations, maintaining reliance on manual material handling approaches, and limiting market penetration.

Skilled Workforce Shortage and Integration Complexity Challenges

The material handling equipment industry faces critical skilled labor shortages, with the Manufacturing Institute reporting 2.1 million unfilled U.S. manufacturing positions through 2033, including technicians capable of maintaining automated systems. Complex integration requirements involving warehouse management systems, enterprise resource planning platforms, and legacy equipment create implementation risks and extended deployment timelines. Autonomous mobile robot deployments require specialized programming, safety certification, and operational training that many Industryrs struggle to provide internally. The Association for Supply Chain Management reports 47% of warehouse automation projects experience delays or cost overruns due to integration challenges and inadequate technical expertise. These workforce constraints and technical complexity barriers slow adoption rates, particularly in sectors with limited automation experience, while increasing total cost of ownership through extended implementation services and ongoing maintenance dependencies.

Opportunities - Autonomous Mobile Robot Adoption Across Diverse Industry Applications

Autonomous mobile robots represent transformative technology with applications extending beyond traditional warehouse environments into manufacturing, healthcare, hospitality, and retail sectors. The Global Autonomous Mobile Robotics Market is projected to reach $13.6 billion by 2032, with collaborative robots enabling flexible material transport, inventory management, and production line feeding without fixed infrastructure requirements. Healthcare facilities are increasingly deploying AMRs for medication delivery, linen transport, and meal distribution, with hospital automation markets growing 15% annually. Retail stores utilize shelf-scanning robots and inventory management systems reducing stockout rates by 25-30% while improving labor productivity. Manufacturing environments benefit from AMR flexibility in dynamic production layouts, with automotive suppliers reporting 40% reduction in internal transport costs. Advanced navigation technologies including LiDAR, computer vision, and collaborative operation capabilities expand addressable applications, with opportunities to capture market share from traditional industrial trucks and manual material handling processes.

Retrofitting and Modernization of Existing Warehouse Infrastructure

The global warehouse installed base exceeds ~8 billion square feet, with 65% of facilities constructed prior to 2010 lacking modern automation capabilities, creating substantial retrofitting opportunities. Warehouse operators face pressure to improve operational efficiency without greenfield construction costs averaging $80-120 per square foot, making modular automation solutions increasingly attractive. Scalable technologies including AMRs, collaborative robots, and bolt-on conveyor extensions enable phased automation deployments with investment flexibility matching throughput growth. The average warehouse modernization project involves $3-8 million in material handling equipment upgrades, with modular approaches reducing implementation risk and capital requirements. Third-party logistics providers managing multi-client facilities particularly favor flexible automation supporting diverse product characteristics and seasonal volume fluctuations. The retrofitting market opportunity could represent 35-40% of total material handling equipment demand through 2033, with established warehouse networks in North America and Europe offering substantial addressable revenue potential for equipment manufacturers providing adaptable, integration-friendly solutions.

Category-wise Analysis

Equipment Type Insights

Forklifts command the leading market position with approximately 27% market share in the global material handling equipment sector, reflecting versatility across manufacturing, warehousing, construction, and logistics applications worldwide. The installed base exceeds 15 million units, with annual shipments reaching 1.8 million across internal combustion and electric models. Forklifts support diverse load handling needs, from pallets to containers, with established service networks and operator familiarity driving consistent replacement demand. Electric forklift adoption accelerates as lithium-ion technology improves energy density, charging speed, and lifecycle efficiency across regulated warehouse environments.

Autonomous mobile robots and automated guided vehicles are the fastest-growing segment with a projected 9.6% CAGR through 2033. Flexible deployment, collaborative operation, advanced navigation, and fleet management optimize material flow. E-commerce, logistics, and automotive facilities increasingly adopt AMRs for transport, order picking, and line feeding.

Industry Analysis

Automotive represents the leading Industry segment with approximately 19% market share, reflecting substantial material handling needs across vehicle assembly, component manufacturing, and aftermarket distribution operations worldwide. Global automotive production exceeded 93 million vehicles in 2023, requiring advanced infrastructure for just-in-time delivery, heavy assembly, and finished vehicle logistics. Automotive plants deploy conveyors, overhead cranes, AGVs, and robotic handling cells, achieving production efficiencies exceeding 85%. Electric vehicle manufacturing adds complexity through battery pack transport, cleanroom electronics handling, and specialized lifting systems, driving modernization demand.

E-commerce is the fastest-growing Industry segment with a projected 10.8% CAGR through 2033. Explosive online retail growth drives automated warehouses using sortation systems, AMRs, ASRS, and conveyors. Fulfillment center expansion and rapid delivery expectations accelerate equipment investment by retailers, logistics providers, and regional platforms globally.

Regional Insights and Trends

North America Material Handling Equipment Market Insights

North America is experiencing robust growth at approximately 5.3% CAGR, supported by e-commerce infrastructure investments, nearshoring manufacturing expansion, and rising warehouse automation adoption across logistics sectors. The United States dominates regional performance, with market value exceeding $52 billion, driven by major retailers and third-party logistics operators deploying automation across vast warehouse networks. Canada contributes through automotive clusters and food processing, requiring specialized material handling systems. Key drivers include automated fulfillment expansion, cross-border manufacturing demand, and labor shortages pushing automation amid low warehouse vacancy rates.

Regulation emphasizes workplace safety through OSHA standards governing forklifts, cranes, and automated equipment, creating compliance-driven replacement cycles. Established manufacturers and emerging AMR specialists compete strongly. Investment focuses on retrofit automation, scalable solutions, modernization, throughput optimization, and flexible capital deployment strategies.

Europe Material Handling Equipment Market Insights

Europe holds a prominent market share of approximately 30% in the global material handling equipment sector, driven by advanced manufacturing infrastructure, widespread automation adoption, and stringent environmental regulations. Germany leads with a market exceeding $22 billion, supported by automotive, chemical, and logistics strengths. The United Kingdom, France, and Spain contribute through diversified industries and e-commerce–driven warehouse automation. Growth is fueled by Industry 4.0 integration, Green Deal electrification mandates, and supply chain localization following Brexit and pandemic disruptions.

The regulatory framework emphasizes CE safety standards, emission controls, and Extended Producer Responsibility. Investment focuses on modernizing aging warehouses, with over half built before 2000, requiring automation upgrades to improve efficiency and competitiveness across Europe.

Asia Pacific Material Handling Equipment Market Insights

The Asia Pacific region maintains a significant market share of approximately 32%, positioning it as the largest geographic market for material handling equipment driven by massive manufacturing capacity, rapid infrastructure development, and accelerating automation adoption. China dominates regional performance with a market value exceeding $85, billion, supported by manufacturing, e-commerce logistics networks serving consumers, and government initiatives promoting intelligent manufacturing. Japan sustains advanced automation through robotics integration, while India offers growth potential via manufacturing expansion and logistics modernization. ASEAN nations emerge.

Manufacturing advantages, including extensive industrial ecosystems, competitive labor costs, and technology incentives, drive leadership. Growth factors include automotive and electronics concentration, e-commerce automation expansion, and infrastructure modernization. Investments prioritize AMRs, electric forklifts, smart warehouses, and IoT systems. Companies build local manufacturing, partnerships, distribution, and after-sales networks meeting diverse requirements globally.

Competitive Landscape

Market leaders prioritize automation using autonomous navigation, AI fleet management, and IoT predictive maintenance to enhance efficiency and ownership value. Expansion targets emerging markets through localization and partnerships. Electrification drives zero-emission portfolios. Integrated equipment, software, and services differentiate competitors, while after-sales excellence and flexible equipment-as-a-service financing strengthen long-term customer relationships.

Strategic Developments

- In December 2024, Hapman introduced the CablePro Tubular Drag Conveyor, an FDA-approved, self-lubricating conveyor designed for efficient food and delicate item conveyance.

- In September 2024, Crown Equipment introduced Crown C-B Series 80V electric, pneumatic tire counterbalance forklifts, offering robust, efficient performance, ergonomic design, and clean power for operators.

- In August 2024, Godrej & Boyce introduced India's first lithium-ion battery-operated forklift, offering 15% more run time and scalability, and plans to extend the technology to other material handling equipment.

Companies Covered in Material Handling Equipment Market

- BEUMER Group

- Daifuku Co., Ltd.

- Honeywell International, Inc.

- KION Group AG

- Mecalux, S.A.

- Murata Manufacturing Co., Ltd.

- SSI SCHAEFER

- Swisslog Holding AG

- TOYOTA Industries Corporation

- Vanderlande Industries B.V.

Frequently Asked Questions

The global material handling equipment market is projected at US$280.5 billion in 2026, expected to reach US$424.6 billion by 2033.

E-commerce logistics infrastructure expansion, Industry 4.0 adoption requiring automated manufacturing systems, and supply chain resilience initiatives promoting nearshoring and warehouse modernization drive market growth.

The market is projected to grow at a 6.1% CAGR between 2026 and 2033.

Emerging market infrastructure development, autonomous mobile robot adoption across diverse industries, and retrofitting existing warehouse facilities represent primary growth opportunities.

Industries Corporation, KION Group AG, Jungheinrich AG, Crown Equipment Corporation, Hyster-Yale Materials Handling, Daifuku Co., Ltd., and Körber AG lead the global market.