- Aerospace & Defense

- Aerospace and Defense Springs Market

Aerospace and Defense Springs Market Size, Share, and Growth Forecast 2026 - 2033

Aerospace and Defense Springs Market by Spring Type (Compression Springs, Tension Springs, Torsion Springs, Flat Springs, Belleville Washers), Material (Metal Springs and Non-metal Springs), End-user (Commercial Aviation, Military Aviation, Space Exploration, Defense Contractors, Government Agencies), and Regional Analysis for 2026 - 2033

Aerospace and Defense Springs Market Size and Trend Analysis

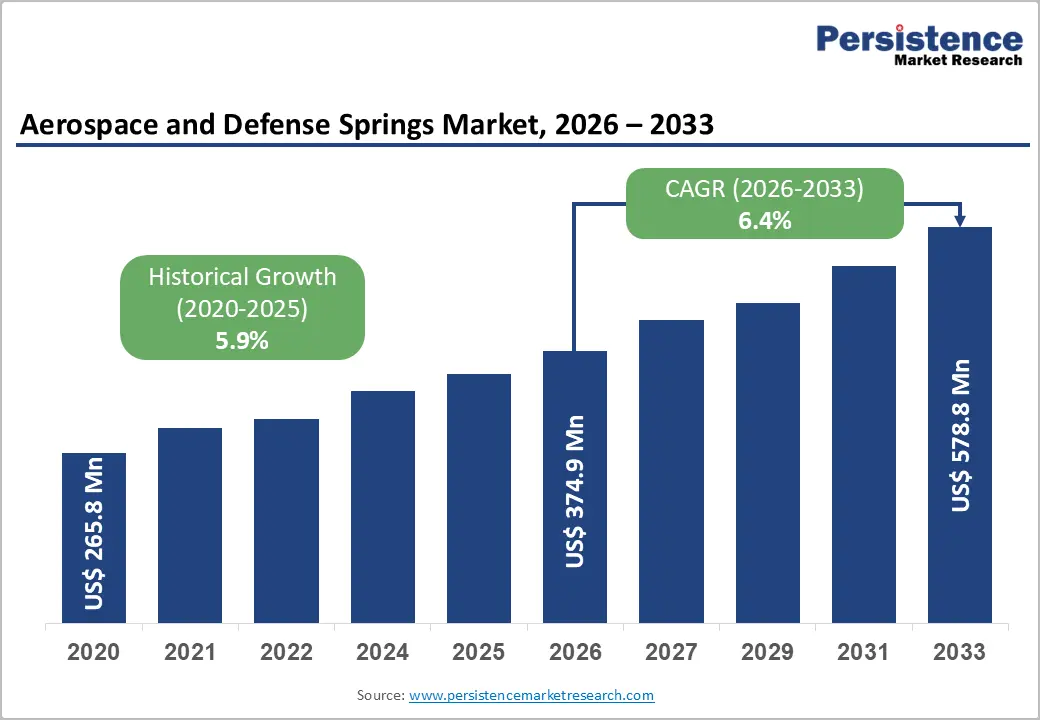

The global aerospace and defense springs market size is valued at US$ 375.0 Mn in 2026 and is projected to reach US$ 578.8 Mn by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

This sustained growth is primarily driven by accelerating global defense procurement budgets, fleet modernization programs across commercial and military aviation, and expanding space exploration initiatives. According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure surpassed US$ 2.2 trillion in 2023, marking a consecutive year of increase, which directly underpins demand for precision mechanical components such as aerospace springs.

Key Industry Highlights:

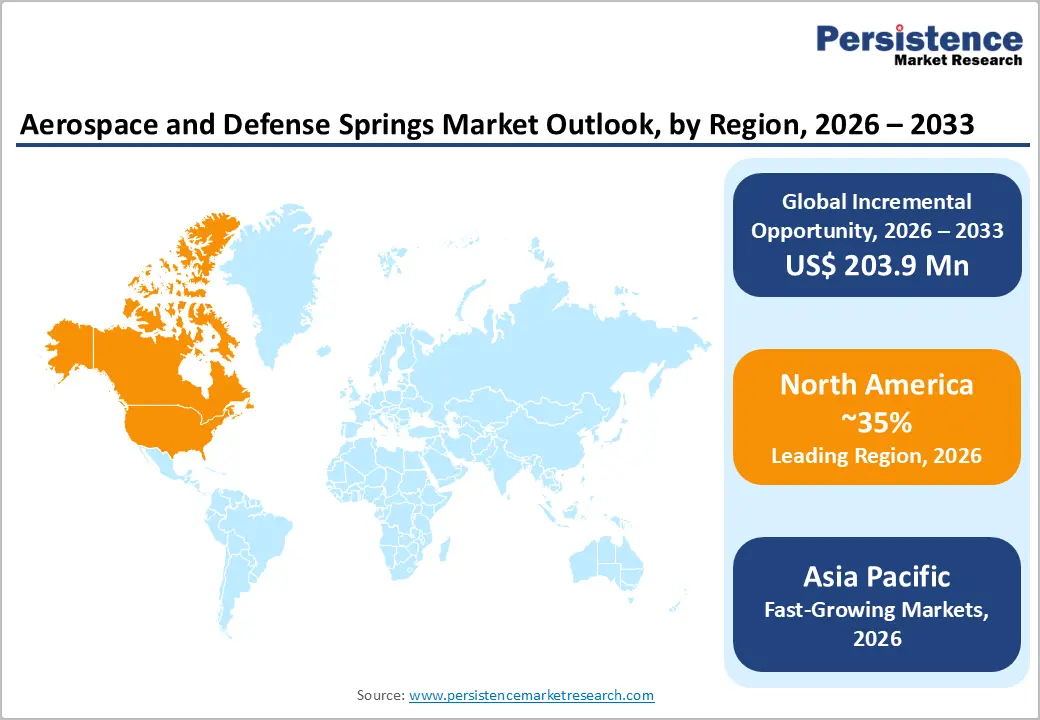

- Leading Region: North America leads the global Aerospace and Defense Springs Market, driven by the world's largest defense budget, major OEM presence (Boeing, Lockheed Martin), and a robust FAA-governed MRO replacement demand cycle sustaining high-volume component procurement.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, with India, China, and Japan increasing defense modernization spending, expanding domestic aviation manufacturing under indigenization mandates, and developing MRO hubs across ASEAN nations.

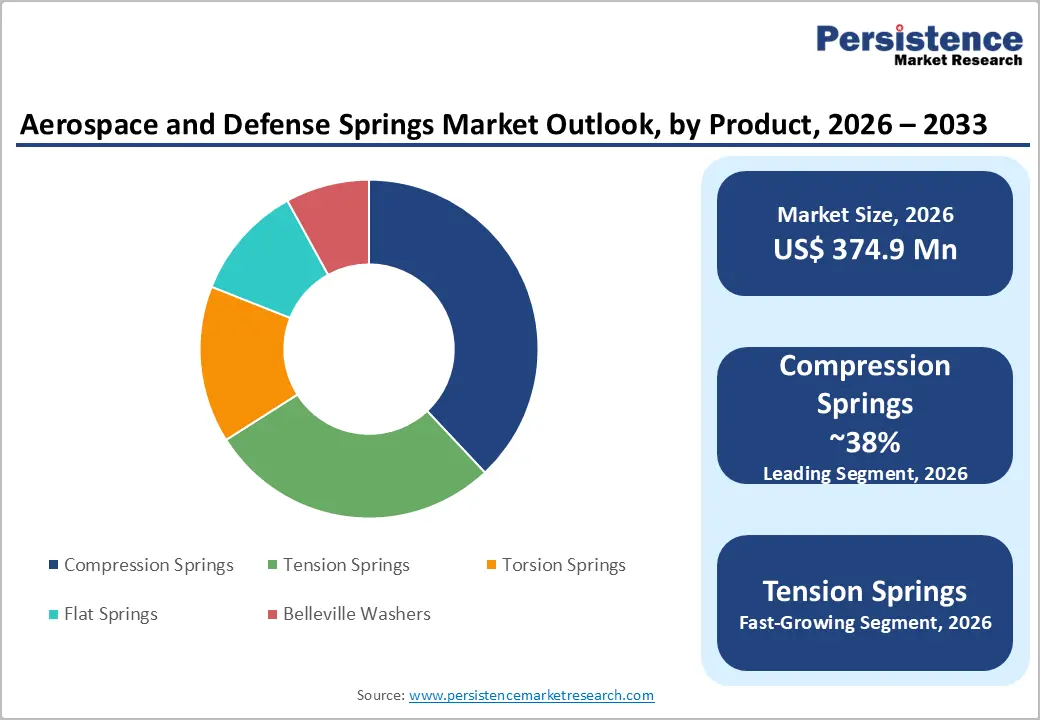

- Dominant Material Segment: Compression Springs dominate the Spring Type segment with approximately 38% market share, driven by extensive adoption in landing gear systems, engine components, missile platforms, and actuation assemblies across commercial and military aircraft programs.

- Fastest Growing End-user Segment: The Military Aviation end-user segment is the fastest-growing category, fueled by UAV proliferation, next-generation fighter aircraft procurement programs, and rising global defense budgets exceeding US$ 2.2 trillion annually per SIPRI.

- Opportunities: Space exploration presents the highest-potential emerging opportunity, with the global space economy valued at US$ 546 billion (2023, Space Foundation), creating demand for ultra-precision, high-reliability springs in satellite deployment, rocket separation, and deep-space systems.

| Key Insights | Details |

|---|---|

| Aerospace and Defense Springs Market Size (2026E) | US$ 375.0 Mn |

| Market Value Forecast (2033F) | US$ 578.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Dynamics

Drivers - Rising Global Defense Expenditure Fueling Demand for Precision Spring Components

Escalating geopolitical tensions across Eastern Europe, the Indo-Pacific, and the Middle East are compelling governments worldwide to significantly increase defense budgets. NATO member nations have collectively pledged to meet the 2% of GDP defense spending benchmark, with several nations including Poland, Germany, and Greece already exceeding this threshold in 2024. The U.S. Department of Defense (DoD) requested a defense budget of US$ 849.8 billion for FY2024, sustaining high procurement of fighter aircraft, armored vehicles, and missile systems, all of which depend heavily on precision-engineered springs for actuation, shock absorption, and load-bearing mechanisms. This sustained investment in military hardware directly drives demand for specialized springs manufactured to aerospace-grade tolerances, stimulating market expansion throughout the forecast period.

Commercial Aviation Fleet Expansion and MRO Activities Accelerating Component Demand

Global commercial aviation is experiencing a structural resurgence, with airlines rapidly expanding fleets to meet recovering passenger demand. Airbus reported a net order book exceeding 8,500 aircraft as of early 2024, while Boeing maintained a backlog of over 5,600 aircraft, collectively representing a multi-decade production pipeline. Each new generation aircraft including the Airbus A320neo and Boeing 737 MA incorporates hundreds of spring components in landing gear systems, flight control surfaces, engine nacelles, and cabin interiors. Simultaneously, the global Maintenance, Repair, and Overhaul (MRO) market, valued at approximately US$ 82 billion in 2023 according to Oliver Wyman, ensures continuous replacement demand. The convergence of new aircraft deliveries and active fleet service provides a dual demand engine, sustaining long-term market growth for aerospace and defense springs.

Restraints - Stringent Aerospace Certification Standards Increasing Time-to-Market and Costs

The aerospace and defense spring manufacturing sector is subject to rigorous quality and certification requirements imposed by authorities such as the Federal Aviation Administration (FAA), European Union Aviation Safety Agency (EASA), and military specification standards like MIL-SPEC and AS9100D. Achieving and maintaining these certifications demands significant capital investment in testing infrastructure, process documentation, and supplier qualification. For smaller manufacturers, certification cycles can extend beyond 18-24 months, delaying market entry and increasing production costs. These compliance burdens create barriers that slow market responsiveness and disproportionately impact mid-tier suppliers, constraining the pace at which new players can scale capacity to meet growing aerospace demand.

Volatility in Specialty Raw Material Supply Chains Disrupting Production Continuity

Aerospace-grade Spring manufacturing relies heavily on specialty materials including titanium alloys, high-carbon stainless steel, and Inconel superalloys, which are subject to global supply chain disruptions and price volatility. The U.S. Geological Survey (USGS) has consistently identified titanium and certain nickel-based alloys as critical minerals vulnerable to supply concentration risks. Geopolitical factors, export controls, and limited smelting capacity for titanium sponge approximately 70% of which is concentrated in Russia, Japan, and Kazakhstan create procurement challenges. These supply-side constraints can elevate input costs and delay production schedules, placing downward pressure on manufacturer margins and creating uncertainty in long-term project planning.

Opportunity - Surging Space Exploration Programs Creating New Application Avenues for Advanced Springs

The global space economy is entering an unprecedented expansion phase, driven by both government and commercial actors. NASA's Artemis program, the European Space Agency (ESA) lunar gateway initiatives, and commercial ventures by SpaceX, Blue Origin, and Rocket Lab are collectively escalating demand for ultra-reliable, lightweight spring components designed for extreme temperature and vacuum environments. The Space Foundation estimated the global space economy at US$ 546 billion in 2023, with launch activity and satellite constellation deployments accelerating. Springs used in rocket stage separation mechanisms, payload deployment systems, and deep-space instrumentation must meet extraordinarily stringent durability standards. For manufacturers capable of serving the Aerospace High Performance Alloys Market and related precision components ecosystem, space exploration represents a high-margin, long-term growth opportunity with limited competitive saturation.

Next-Generation Military Aircraft and Unmanned Aerial Vehicle (UAV) Proliferation Driving Specialized Demand

The proliferation of Unmanned Aerial Vehicles (UAVs) and next-generation fighter platforms including the F-35 Lightning II, Eurofighter Typhoon upgrades, and emerging sixth-generation programs by the U.S., U.K., and Japan demands increasingly miniaturized, high-performance spring solutions. The Association for Unmanned Vehicle Systems International (AUVSI) projects global UAV market expansion through the early 2030s, with defense applications accounting for a significant share. UAV systems require compact, corrosion-resistant springs capable of withstanding vibration, rapid actuation cycles, and thermal cycling under operational conditions. Defense contractors seeking to differentiate through advanced materials and precision manufacturing can capitalize on this structural shift, offering proprietary spring solutions tailored to platform-specific performance envelopes, especially as UAV procurement programs scale globally across NATO and allied defense forces.

Category-wise Analysis

Spring Type Insights

Compression springs represent the dominant segment within the Spring Type category of the Aerospace and Defense Springs Market, accounting for approximately 38% of total market share. Their dominance is rooted in their extensive application across critical aerospace sub-systems, including landing gear shock absorbers, aircraft seat mechanisms, engine valve assemblies, and missile launch systems. Compression springs offer reliable load-bearing performance across a wide range of stroke lengths and force requirements, making them indispensable in both commercial and military platforms. According to SAE International technical standards, compression springs are among the most specified mechanical components in aircraft structural and actuation system designs. The high production volumes associated with commercial aircraft OEM program sled by Airbus and Boeing further reinforce this segment's dominant revenue position.

Material Insights

Metal springs, particularly those fabricated from stainless steel and titanium alloys, dominate the Material category, commanding an estimated 82% share of the Aerospace and Defense Springs Market. Stainless steel remains the most widely deployed material due to its excellent strength-to-weight ratio, corrosion resistance, and machinability, all of which are critical for aviation and defense environments. Titanium alloys are gaining prominence in high-performance applications requiring weight reduction without sacrificing mechanical integrity particularly relevant given that modern aircraft designs target 15-20% weight reduction per generation to improve fuel efficiency. The aerospace industry's ongoing alignment with Aerospace High Performance Alloys Market trends further reinforces metal springs' material dominance. Non-metal springs comprising plastic and composite materials, while growing, remain a niche solution in low-load, non-critical applications.

End-user Insights

The military aviation segment holds the leading position in the End User category, representing approximately 35% of total market revenue. Military aviation platforms including fighter jets, bombers, rotary-wing aircraft, and surveillance UAVsdemand components designed to withstand extreme operational stress, sustained G-forces, and harsh environmental conditions. DoD budget allocations for aircraft procurement and modernization consistently prioritize mission-critical component reliability, sustaining steady demand for high-specification springs. Programs such as the F-35 Joint Strike Fighter with over 3,300 units planned across international partner nations represent multi-decade procurement pipelines for aerospace spring manufacturers. Defense Contractors supplying these programs are required to maintain AS9100D-certified supply chains, ensuring only qualified spring manufacturers benefit from these high-value contracts.

Regional Insights

North America Aerospace and Defense Springs Market Trends

North America represents the largest regional market for aerospace and defense springs, underpinned by the world's most significant defense industrial base. The United States alone accounts for approximately 40% of global military expenditure, with the DoD sustaining multi-year procurement programs across air, land, sea, and space domains. Major OEMs including Boeing, Lockheed Martin, and Northrop Grumman maintain extensive domestic supply chains that create sustained, high-volume demand for aerospace-grade springs.

The innovation ecosystem in North America is further strengthened by the integration of advanced manufacturing technologies, including Computer Numerical Control (CNC) precision machining and additive manufacturing, into spring production workflows. NASA's escalating space exploration budgets under the Artemis program and growing commercial launch activity from companies such as SpaceX are expanding the addressable market into space-grade spring applications. U.S.-based spring manufacturers are well-positioned to serve these emerging high-value segments.

Europe Aerospace and Defense Springs Market Trends

Europe represents the second-largest regional market, supported by a mature aerospace manufacturing ecosystem centered on Germany, France, and the United Kingdom. Airbus, headquartered in Toulouse, France, is the world's largest commercial aircraft manufacturer by order backlog and relies extensively on European-based tier-1 and tier-2 suppliers for precision mechanical components. Germany's ThyssenKrupp AGa key market participant leverages deep materials science expertise to supply high-performance spring solutions to both commercial and defense customers.

Regulatory harmonization under EASA's Part-21 production approval framework and the European Commission's European Defense Fund (EDF)which allocated approximately €8 billion for the 2021-2027 period to defense research and capability development are catalyzing regional market growth. U.K. defense spending commitments post-Brexit, including a pledge to raise defense expenditure to 2.5% of GDP by 2030, further reinforce demand for defense-grade spring components from British and continental European suppliers.

Asia Pacific Aerospace and Defense Springs Market Trends

Asia Pacific is the fastest-growing regional market for aerospace and defense springs, driven by escalating defense modernization programs and expanding domestic aviation industries across China, India, Japan, and South Korea. China's People's Liberation Army Air Force (PLAAF) modernization, including deployment of J-20 stealth fighters and expanding naval aviation capacity, is generating substantial demand for domestically manufactured aerospace components. Simultaneously, India's Ministry of Defence has mandated indigenization under its Defence Acquisition Procedure (DAP) 2020, pushing domestic manufacturing of aerospace sub-components including precision springs.

Japan's Mitsubishi Heavy Industries and Kawasaki Heavy Industries are central to regional aerospace manufacturing, while ASEAN nations particularly Singapore and Malaysia are emerging as MRO hubs for Asia-Pacific aviation. India's aviation market, projected by IATA to become the world's third largest by 2030 is creating sustained commercial aviation-driven demand. The combination of cost-competitive manufacturing capabilities and government-backed industrial policies creates a compelling growth environment for both regional and global spring manufacturers expanding their Asia Pacific footprint.

Competitive Landscape

The Aerospace and Defense Springs Market exhibit a moderately consolidated structure, with a mix of global tier-1 aerospace component suppliers and specialized spring manufacturers competing for program-specific contracts. Market leaders differentiate through AS9100D certification, material engineering expertise, and long-term OEM supply agreements. Leading players are investing in lean manufacturing, automated coiling technologies, and advanced testing capabilities to improve precision and reduce lead times. Consolidation through acquisitions is an observable trend, as larger aerospace conglomerates seek to internalize critical component supply chains.

Key Developments

- In January 2024, U.S.-based Honeywell Aerospace launched an initiative to integrate smart materials into its spring designs. It aims to enhance functionality through adaptability to varying environmental conditions, increasing the lifespan and efficiency of aerospace components.

- In March 2024, Eaton Corporation announced a strategic agreement with Lockheed Martin to supply precision actuation spring assemblies for the F-35 Lightning II program's sustainment and retrofit operations, reinforcing its long-term defense aftermarket position.

Companies Covered in Aerospace and Defense Springs Market

- Keller Technology Corporation

- Graham-White Manufacturing

- Associated Spring

- Helical Products Company

- Landefeld

- Bishop Wisecarver

- Spring Engineering

- Jergens, Inc.

- Smalley Steel Ring Company

- Mubea

- Eaton Corporation

- Rolls-Royce plc

- Goodrich Corporation (Collins Aerospace)

- Hawker Beechcraft

- ThyssenKrupp AG

- Other Key Players

Frequently Asked Questions

The global Aerospace and Defense Springs Market is valued at US$ 375.0 Mn in 2026 and is projected to reach US$ 578.8 Mn by 2033, expanding at a forecast CAGR of 6.4% during the 2026-2033 period.

The market is primarily driven by escalating global defense expenditures surpassing US$ 2.2 trillion in 2023 per SIPRIand the commercial aviation fleet expansion, with Airbus and Boeing collectively maintaining backlogs of over 14,000 aircraft. These factors sustain high-volume demand for aerospace-grade precision spring components across OEM and MRO channels.

Compression Springs are the leading segment in the Spring Type category, accounting for approximately 38% of total market share. Their dominance is attributed to wide application in landing gear systems, engine valve assemblies, missile actuation systems, and cabin structural components across commercial and military aircraft.

North America is the dominant regional market, supported by the world's highest defense budget with the U.S. DoD FY2024 request of US$ 849.8 billion alongside a mature aerospace manufacturing base, major OEM programs, and stringent FAA airworthiness maintenance requirements driving consistent component demand.

Key companies operating in the market include Associated Spring, Mubea, Eaton Corporation, Smalley Steel Ring Company, ThyssenKrupp AG, Rolls-Royce plc, Goodrich Corporation (Collins Aerospace), Keller Technology Corporation, Graham-White Manufacturing, Helical Products Company, TransDigm Group Incorporated, and MW Industries, Inc., among others.