- Inks, Coatings, Adhesives & Sealants (ICAS)

- Adhesives and Sealants Market

Adhesives and Sealants Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Adhesives and Sealants Market by Product Type (Adhesives and Sealants), Technology (Water-based, Solvent-based, Hot Melt, Reactive, and Others), Application (Paper board & Packaging, Building & Construction, Furniture & Woodworking, Automotive & Transportation, Footwear & Leather, Medical, Consumer & DIY, and Others), and Regional Analysis for 2026 to 2033

Adhesives and Sealants Market Size and Share Analysis

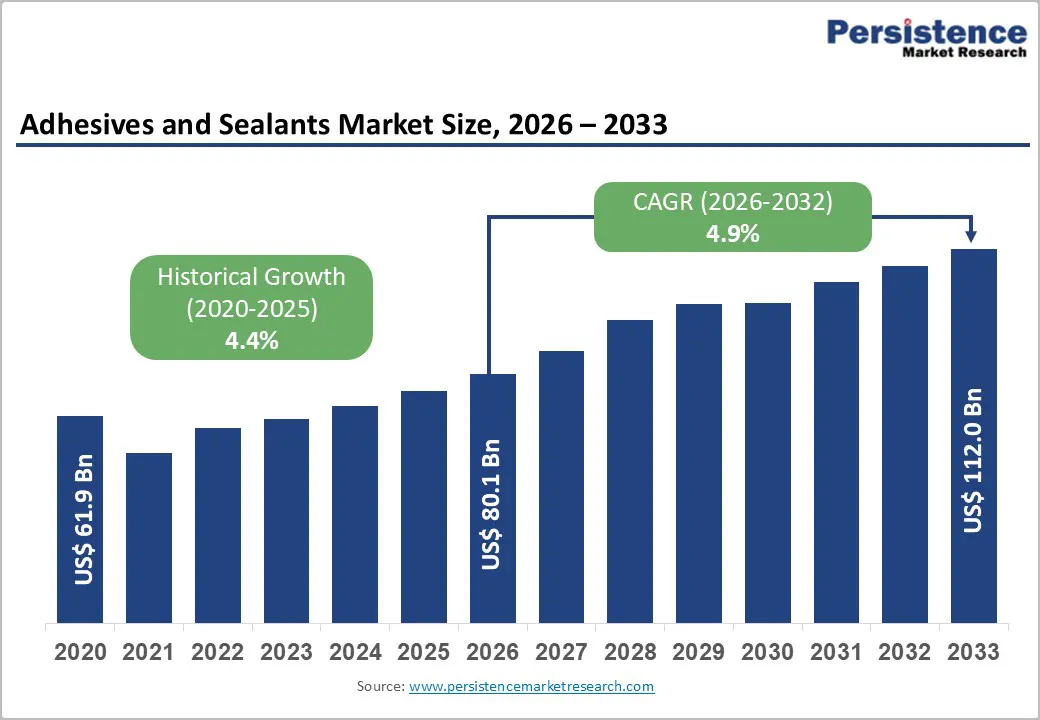

The global adhesives and sealants market size is likely to be valued at US$ 80.1 billion in 2026 and is projected to reach US$ 112.0 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The market growth is fundamentally driven by the robust expansion of the global construction industry, rising preference for energy-efficient, lightweight, and sustainable building materials, and increasing demand from the automotive sector. Rapid urbanization in emerging economies, particularly in the Asia Pacific, including China and India, coupled with substantial infrastructure investment initiatives, is further driving demand for construction-grade adhesives and sealants across residential, commercial, and industrial applications.

Key Market Highlights

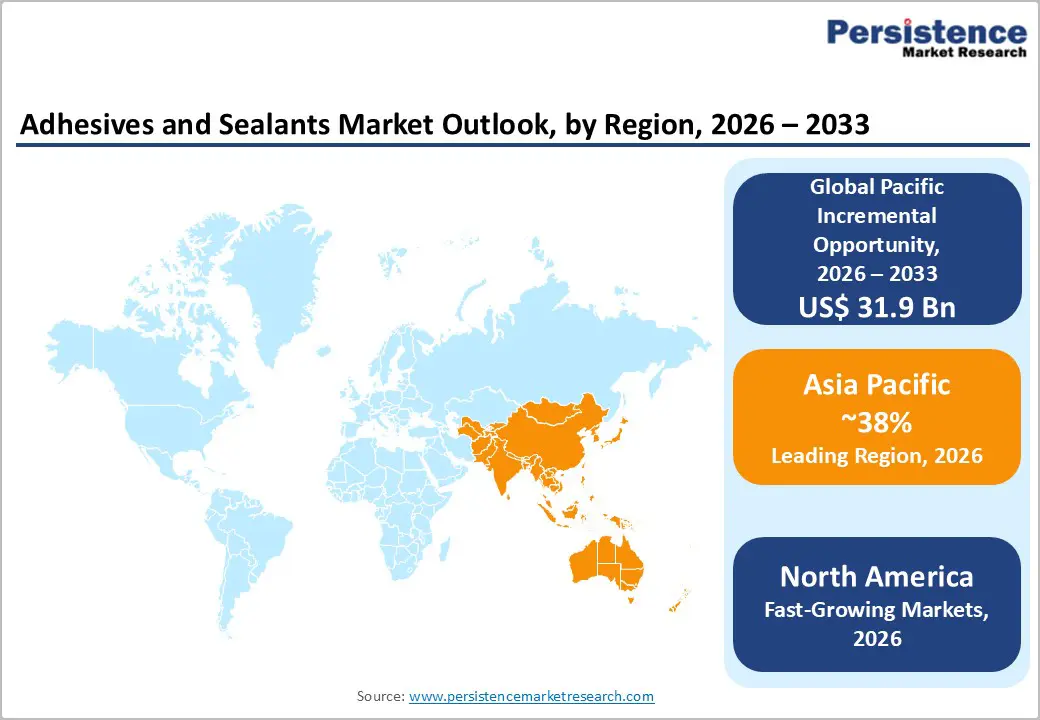

- Leading Region: Asia Pacific dominates global market leadership, commanding approximately 38% of the worldwide adhesives and sealants market share driven by rapid industrialization in China, infrastructure expansion in India, and manufacturing acceleration across Southeast Asian nations.

- Fastest Growing Region: North America maintains a significant market position, supported by established automotive and construction industries, stringent environmental regulatory frameworks promoting sustainable formulations, and substantial infrastructure investment programs.

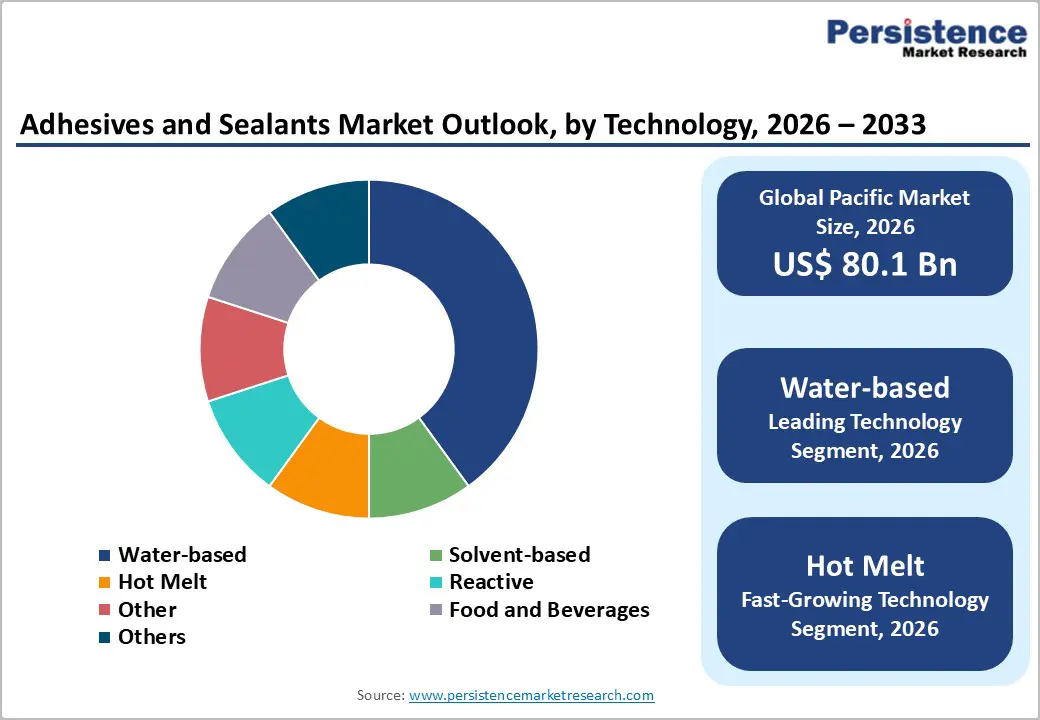

- Dominant Technology: Water-based adhesive technology dominates product segment, commanding 37.9% of total market share, driven by superior environmental characteristics, regulatory compliance advantages, and increasing adoption across construction, packaging, and automotive applications aligned with sustainability objectives.

- Key Application: Paper, board, and packaging segment generates significant demand, representing 31% of market consumption, accelerated by explosive e-commerce growth, FMCG industry expansion, and increasing demand for sustainable, recyclable packaging solutions.

- Key Opportunity: Sustainable and bio-based adhesives present paramount market opportunity, driven by regulatory pressures, corporate sustainability commitments, and consumer preferences for renewable feedstock-based formulations outpacing overall adhesives market growth trajectory.

| Key Insights | Details |

|---|---|

| Global Adhesives and Sealants Market Size (2026E) | US$ 80.1 Bn |

| Market Value Forecast (2033F) | US$ 112.0 Bn |

| Projected Growth CAGR(2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Accelerating Infrastructure and Building Construction Initiatives

Accelerating investment in residential, commercial, and infrastructure construction is one of the most influential demand drivers for the global adhesives and sealants market. According to projections by the United Nations, global construction spending is expected to reach approximately USD 15 trillion annually by 2030, supported by rapid urbanization, population growth, and sustained government-led infrastructure development. Adhesives and sealants are increasingly essential in modern construction for applications such as glazing systems, façade sealing, flooring installation, roofing, insulation, and waterproofing, where high durability, flexibility, and long-term performance are critical.

The global transition toward energy-efficient buildings and sustainable construction practices is further strengthening market growth. Green building frameworks and certifications such as LEED are encouraging the use of high-performance sealants that minimize air leakage, enhance thermal insulation, and improve overall building efficiency. As construction practices continue to evolve toward lightweight materials, modular structures, and sustainability-driven design, adhesives and sealants are becoming indispensable components, reinforcing infrastructure and building activity as a long-term growth engine for the global market.

Automotive Lightweighting and Electric Vehicle Assembly Revolution

The automotive industry is undergoing a paradigm shift toward lightweight vehicle architectures to improve fuel efficiency and meet carbon emission targets mandated by global regulatory frameworks. Adhesives have become preferred alternatives to traditional welding and mechanical fasteners, reducing vehicle weight by 15-25% while improving structural integrity and crash safety. Electric vehicles (EVs), representing the fastest-growing segment in automotive manufacturing with an estimated CAGR of 20% through 2030, require specialized adhesive solutions for battery pack integration, thermal management, and composite material bonding.

China leads global EV production with approximately 10.2 million units sold in 2023, and this trajectory is expected to accelerate substantially through 2030, generating robust demand for industrial adhesives and advanced sealants. Major automotive manufacturers including Volkswagen, Tesla, General Motors, and BMW are expanding adhesive usage in vehicle assembly, particularly in lightweight aluminum and composite applications where traditional fastening methods prove inadequate, driving market growth across both developed and emerging economies.

Restraint - Stringent Environmental Regulations and Complex Compliance Requirements

Regulatory frameworks including REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) in Europe, the EPA Volatile Organic Compound (VOC) regulations in North America, and country-specific emission standards in Asia Pacific regions impose stringent limits on chemical content and VOC emissions in adhesive and sealant formulations. EU regulations mandate VOC limits of 200 g/L for adhesives and 40-500 g/L for sealants, depending on application, creating significant reformulation and testing requirements for manufacturers.

The U.S. Environmental Protection Agency estimates that industrial adhesives contribute approximately 9% of global VOC emissions, positioning these products under increasing regulatory scrutiny. Compliance requires extensive documentation, safety assessments, and product testing, extending commercialization timelines and increasing operational costs. These regulatory pressures particularly impact smaller manufacturers and companies in developing regions lacking advanced research and development infrastructure, potentially limiting product innovation and market entry opportunities for new competitors.

Performance Limitations and Application-Specific Challenges Are Restricting Wider Adoption

Despite technological advancements, adhesives and sealants can face performance limitations and application challenges that restrict broader adoption in certain end-use sectors. Variations in temperature, humidity, surface compatibility, and curing conditions can affect bonding strength, durability, and long-term performance. In construction and industrial applications, improper application or inadequate surface preparation can lead to adhesion failure, increasing maintenance costs and reducing customer confidence.

Transitioning from traditional mechanical fasteners to adhesive-based solutions often requires changes in design, training, and installation practices, which can slow adoption rates. These technical and operational barriers, combined with the need for application-specific customization, act as restraints on rapid market penetration, particularly in cost-conscious and risk-averse industries.

Opportunity - Sustainable and Bio-Based Adhesive Solutions Growth Trajectory

Environmental regulations, corporate sustainability commitments, and consumer preferences for eco-friendly products are driving transition from petroleum-derived formulations to renewable feedstocks including plant oils, natural resins, and seaweed-derived materials. Manufacturers including Henkel, H.B. Fuller, and Arkema are investing substantially in bio-based polyurethane hot melt adhesives, with some formulations achieving up to 50% renewable content while maintaining performance parity with traditional products.

The Construction Chemicals Market, encompassing eco-friendly sealants for green building projects, is projected to expand at 5.7% annually through 2030, driven by LEED certification requirements and energy efficiency standards. Companies positioning themselves as innovation leaders in sustainable adhesive chemistry are capturing premium market segments and differentiating from commodity competitors, particularly in developed markets where environmental consciousness and sustainability certifications command price premiums.

Emerging Applications in Flexible Electronics, Renewable Energy, and Medical Devices

High-growth opportunities are emerging in specialized applications including flexible hybrid electronics, wearables, wind energy systems, and medical devices, where conventional adhesive chemistries prove inadequate. The global wearables market is projected to exceed USD 115 billion by 2030, requiring specialized adhesives with exceptional flexibility, biocompatibility, and moisture resistance for seamless integration with textile and polymeric substrates. Wind energy installations are expanding at a CAGR of 8.7% globally, creating demand for high-performance structural adhesives capable of bonding composite blade materials and withstanding extreme environmental conditions and mechanical stresses.

Medical device manufacturers increasingly utilize adhesives for biocompatible bonding in applications including wound care, surgical tapes, and implantable devices, with the global medical adhesives market projected to grow at 6.8% annually through 2032. Manufacturers developing application-specific adhesive solutions with advanced performance characteristics, rapid curing capabilities, and regulatory compliance certifications are well-positioned to capture these high-value market segments and achieve sustained competitive advantage.

Category-wise Analysis

Adhesives Type Insights

Acrylic adhesives represent the dominant adhesive segment, commanding approximately 23% of the global adhesives market share, supported by their exceptional weather resistance, UV stability, and compatibility with diverse substrates including metals, plastics, and composites. Acrylic systems deliver superior peel strength and elasticity, making them ideal for pressure-sensitive labeling applications, automotive trim bonding, and construction facade applications where long-term durability against environmental exposure is paramount. The segment is experiencing steady growth from increasing adoption in automotive lightweighting applications and construction modernization projects, particularly in developed regions pursuing energy efficiency upgrades and sustainable building standards.

Polyurethane adhesives maintain a strong market position, particularly in transportation and aerospace applications where exceptional bond strength, chemical resistance, and ability to accommodate thermal expansion and contraction are critical performance requirements. Epoxy adhesives, while representing a smaller market segment, serve specialized high-performance applications in electronics, composite bonding, and aerospace assembly where extreme temperature resistance and exceptional adhesion strength justify premium pricing.

Sealants Type Insights

Silicone sealants represent the dominant segment within the global sealants market, supported by their outstanding flexibility, weather resistance, UV stability, and long-term durability across a wide temperature range. Silicone systems exhibit excellent adhesion to substrates such as glass, metals, ceramics, and plastics, making them the preferred choice for glazing, curtain walls, façade joints, sanitary applications, and high-movement expansion joints. Their ability to retain elasticity and performance under extreme environmental exposure has driven widespread adoption in both residential and commercial construction, as well as in industrial and automotive sealing applications. The segment continues to benefit from growing investments in infrastructure development, high-rise construction, and energy-efficient building envelopes.

Technology Insights

Water-based adhesive technology dominates the market, accounting for approximately 37.9% to 40% of total market volume, driven by superior environmental characteristics, lower health risks, and increasing regulatory support for low-VOC formulations. Water-based adhesives, primarily comprising acrylic polymer emulsions and polyvinyl acetate dispersions, are experiencing projected growth of 12% over the forecast period, significantly outpacing traditional solvent-based alternatives. These formulations offer exceptional advantages including zero to minimal VOC emissions, enhanced worker safety, and full compliance with EPA, REACH, and regional environmental regulations across developed markets.

Hot melt adhesives represent the second-largest technology segment, valued for their rapid application, zero VOC emissions, and suitability for automated high-speed manufacturing processes in packaging and assembly operations. Reactive adhesives and other advanced systems, collectively comprising approximately 48.4% of the market, include polyurethane reactive adhesives, moisture-curing epoxies, and cyanoacrylates that deliver superior performance characteristics for demanding industrial applications. Solvent-based adhesives, traditionally dominant in industrial applications, are experiencing gradual market share erosion as manufacturers transition toward water-based and reactive alternatives to meet environmental regulations and customer sustainability requirements.

Application Insights

The building and construction segment represents the leading application area for adhesives and sealants, accounting for approximately 34% of total market demand. These products are extensively used across glazing systems, façade sealing, flooring installation, roofing, interior fit-out applications, and large-scale infrastructure projects. Sustained investments in residential housing, commercial buildings, and public infrastructure continue to support steady demand. Increasing adoption of energy-efficient building designs, green construction standards, and prefabricated structures further reinforces the importance of high-performance adhesives and sealants in this segment.

The paper, board, and packaging segment, while remaining one of the largest application domains and accounting for approximately 31% of total market demand, is exhibiting relatively stagnant growth compared to other end-use sectors. Market maturity in developed regions, pricing pressure, and ongoing optimization of packaging material usage are moderating expansion despite continued demand from e-commerce, FMCG, and food and beverage industries.

The automotive and transportation segment is emerging as the fastest-growing application area for adhesives and sealants. Vehicle manufacturers are rapidly shifting toward adhesive-based assembly solutions to replace traditional welding and mechanical fastening methods in order to achieve lightweighting targets, improve structural integrity, and enhance crash performance. The growing adoption of electric vehicles, advanced composites, and mixed-material designs is further accelerating demand.

Regional Insights

North America Adhesives and Sealants Trends

North America maintains a significant market position, with the United States dominating the region through established automotive, aerospace, construction, and packaging industries characterized by high technical sophistication and mature market dynamics. The U.S. Environmental Protection Agency (EPA) enforces rigorous Architectural Sealants Rule regulations limiting VOC emissions to 200 g/L for adhesives, compelling manufacturers to develop advanced water-based and reactive chemistries that maintain performance while reducing environmental impact.

The Infrastructure Investment and Jobs Act, representing a USD 1.2 trillion investment program, is generating substantial demand for high-performance construction adhesives and sealants across infrastructure modernization, bridge repair, and renewable energy projects. The automotive sector in North America is experiencing accelerated transition toward adhesive-based assembly, with major manufacturers including General Motors, Ford, and Stellantis expanding adhesive usage in lightweight aluminum and composite vehicle structures to meet federal fuel efficiency standards and carbon emission reduction targets. Regulatory initiatives, including the EPA's January 2024 grant program offering USD 200 million for sustainable adhesive technology adoption, are directly incentivizing manufacturing transitions toward eco-friendly formulations and supporting market growth toward green adhesive solutions.

Europe Adhesives and Sealants Market Trends

Europe adhesives and sealants market is evolving under the influence of sustainability, regulatory pressures, and innovation across key end-use industries. One of the most prominent trends is the shift toward environmentally friendly and low-VOC formulations, driven by stringent European Union environmental regulations and sustainability goals. Manufacturers are increasingly developing water-based, bio-based, and recyclable adhesive and sealant systems to comply with REACH restrictions and low emission standards, as well as to meet growing demand from eco-conscious construction, automotive, and packaging sectors. This focus on greener chemistries not only supports regulatory compliance but also aligns with broader circular economy initiatives throughout the region.

The rise of electric vehicles (EVs) and sustainability mandates in the automotive industry are accelerating the adoption of structural adhesives and sealants designed for lightweight materials and battery assembly, supporting both fuel efficiency and safety requirements. Meanwhile, building renovation initiatives and energy-efficiency mandates, such as the EU Renovation Wave, are bolstering demand for adhesives and sealants in façade systems, insulation bonding, and retrofit applications. Technological innovation remains at the forefront of regional trends, with Europe leading development in advanced adhesive chemistries such as UV-cured systems, smart adhesives, and high-performance polymers that offer enhanced thermal stability, rapid curing, and multifunctional bonding properties.

Asia Pacific Adhesives and Sealants Market Trends

Asia Pacific dominates the global adhesives and sealants market, commanding approximately 38% of worldwide market share, making it a critical growth engine for global manufacturers. This growth is primarily driven by rapid industrialization, infrastructure development, and expanding manufacturing sectors across major economies. China exercises dominant influence over regional markets, commanding approximately 43% of Asia Pacific adhesives and sealants demand, leveraging its position as the world's largest manufacturing hub for automotive, electronics, packaging, and construction materials.

India emerges as the fastest-growing market within the region, with water-based adhesives specifically representing a 9.8% CAGR. The "Make in India" initiative and foreign direct investment policies are catalyzing manufacturing expansion, particularly in automotive assembly, consumer goods, and electronics production, creating substantial demand for industrial adhesives and specialized sealants. Japan maintains technological leadership in eco-friendly and high-performance adhesive innovation, with manufacturers introducing bio-based additives addressing regional environmental concerns and stringent quality standards.

Competitive Landscape

The global adhesives and sealants market exhibits a moderately consolidated structure, with significant market power concentrated among multinational chemical corporations including Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema (Bostik), 3M Company, and Sika AG, collectively controlling approximately 35% to 40% of global market revenue. Market differentiation is achieved primarily through advanced product innovation, sustainability certifications, application engineering expertise, and integrated supply chain networks that enable rapid customer support and customized formulation development.

Competitive strategies emphasize research and development investments in sustainable chemistries, automation technology integration, and expansion into emerging market segments including electric vehicle assembly, renewable energy applications, and medical device manufacturing. Emerging market challengers and regional manufacturers are gaining competitive traction by emphasizing cost-effective solutions, geographic market penetration, and application-specific formulation development, with regional leaders including Pidilite Industries in India and Wacker Chemie AG in Europe capturing market share through localized customer relationships and manufacturing proximity.

Key Market Developments

- In May 2025, Henkel and Sasol entered a strategic partnership to lower the environmental footprint of hot melt adhesives. By incorporating Sasol’s newly developed SASOLWAX LC into Henkel’s TECHNOMELT portfolio across Europe, India, the Middle East, and Africa, Henkel is offering advanced adhesive solutions with reduced carbon emissions for consumer goods packaging manufacturers.

- In April 2025, Trinseo launched LIGOS A 9210, an all-acrylic latex binder designed for flexible flooring adhesives. This product launch strengthens Trinseo’s CASE portfolio and highlights its focus on delivering high-performance materials aligned with evolving industry requirements.

- In February 2025, LG Chem announced a collaboration with HL Mando to jointly develop adhesives for automotive electronic components, aiming to expand LG Chem’s footprint in the rapidly growing automotive adhesives market.

Companies Covered in Adhesives and Sealants Market

- Henkel AG & Co. KGaA

- H.B. Fuller

- Arkema (Bostik)

- 3M Company

- Sika AG

- Dow Inc.

- ITW

- PPG Industries, Inc

- Wacker Chemie AG

- Pidilite Industries

- Avery Denison Corporation

- Ashland Inc.

- Kuraray Co., Ltd.

- RPM International Inc.

- Huntsman Corporation

Frequently Asked Questions

The global Adhesives and Sealants Market was valued at US$ 80.1 billion in 2025 and is projected to reach US$ 112.0 billion by 2032, expanding at a CAGR of 4.9% during the forecast period, driven by construction industry growth, automotive lightweighting trends, and increasing demand for sustainable, low-VOC formulations across industrial and consumer applications worldwide.

Primary market drivers include accelerating global construction activity, automotive sector's transition toward lightweight vehicle design and electric vehicle manufacturing; environmental regulations promoting low-VOC formulations; surging e-commerce and packaging demand; infrastructure investment initiatives; and growing consumer preference for sustainable and bio-based adhesive solutions supporting circular economy objectives.

Water-based adhesive technology dominates product segment, commanding 37.9% of total market share with projected growth of 12% throughout forecast period, driven by superior environmental characteristics, regulatory compliance advantages, and increasing adoption across construction, packaging, and automotive applications aligned with sustainability objectives.

Asia Pacific is the largest regional market, commanding approximately 38% of global adhesives and sealants market share, driven by rapid industrialization in China, infrastructure expansion and manufacturing growth in India, urbanization trends across Southeast Asia, and expansion of automotive, construction, packaging, and electronics sectors.

Manufacturers developing high-performance renewable feedstock-based formulations with sustainability certifications and regulatory compliance advantages are positioned to capture premium market segments and achieve differentiation.

Major market leaders include Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema (through its Bostik division), 3M Company, Sika AG, Dow Inc., Illinois Tool Works, PPG Industries Inc., Wacker Chemie AG, Pidilite Industries, Avery Dennison Corporation, Ashland Inc., Kuraray Co., Ltd., RPM International Inc., and Huntsman Corporation.