- Pharmaceuticals

- Medicated Skincare Market

Medicated Skincare Market Size, Share, and Growth Forecast, 2025 - 2032

Medicated Skincare Market By Product Type (Creams & Ointments, Lotions, Others), Indication (Acne, Psoriasis, Others), Technology, Distribution Channel, and Regional Analysis for 2025 - 2032

Medicated Skincare Market Size and Trends Analysis

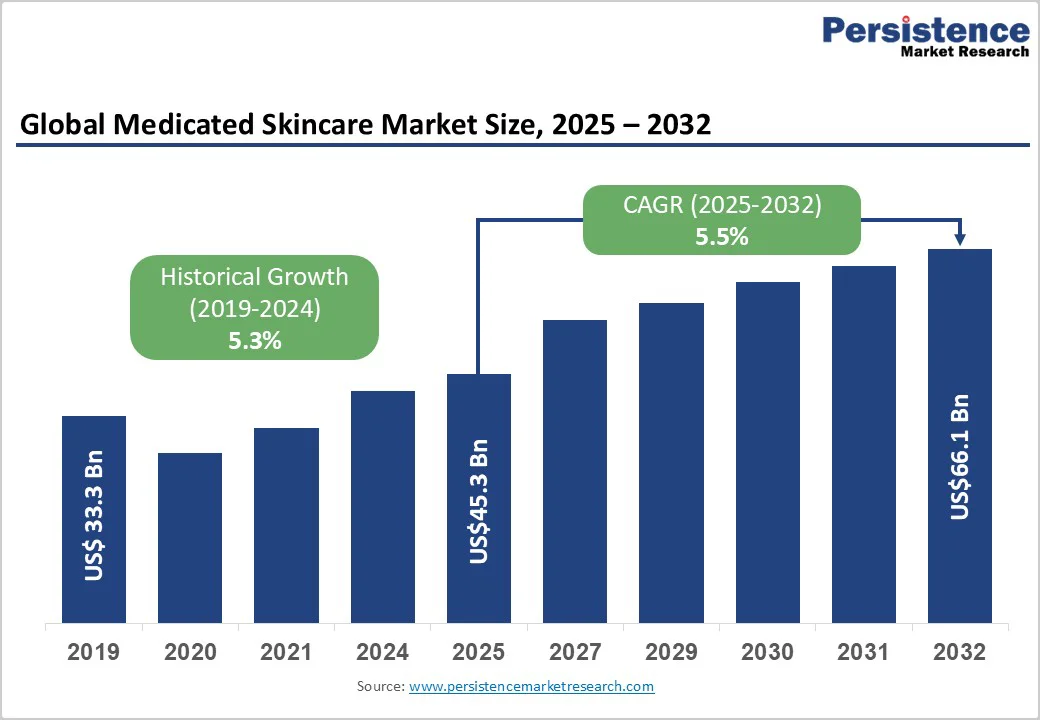

The global medicated skincare market is estimated at around US$45.3 billion in 2025. It is expected to grow to approximately US$66.1 billion by 2032, implying a CAGR of 5.5% during the forecast period from 2025 to 2032, driven by the rising prevalence of dermatological conditions such as acne, eczema, and rosacea, alongside increasing availability of clinically validated active ingredients.

Strong dermatology-led product pipelines and broader OTC access continue to support growth. Dermatologist-recommended brands and clinical channels remain influential, while digital dermatology and e-commerce accelerate penetration, particularly in emerging markets.

Key Industry Highlights

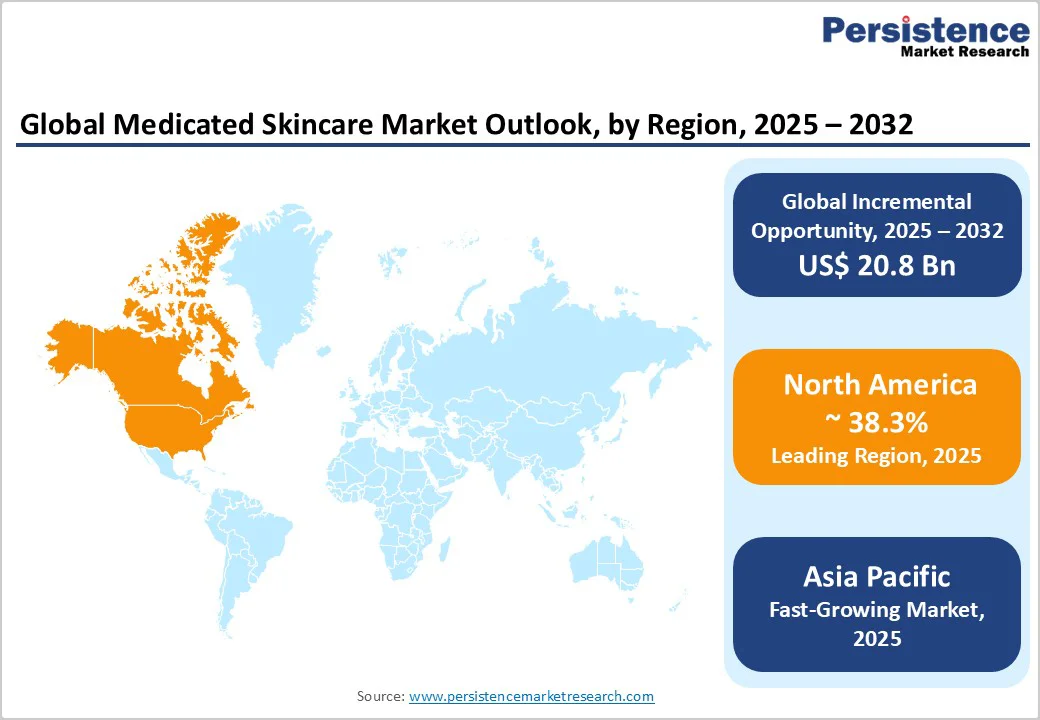

- Leading Region: North America maintained the largest share of the global market at around 38.3% in 2025, supported by high dermatology visit rates, strong retail pharmacy penetration, and rapid uptake of prescription-support OTC formats.

- Fastest-growing Region: Asia Pacific, driven by rising acne and eczema incidence, urban pollution exposure, and expanding cosmeceutical retail channels across China, India, and Southeast Asia.

- Investment Plans: Global manufacturers increased capital allocation toward microbiome-focused formulations, advanced delivery systems, and clinical-grade anti-inflammatory actives, with R&D spending rising by nearly 12% in 2024–2025 across leading brands.

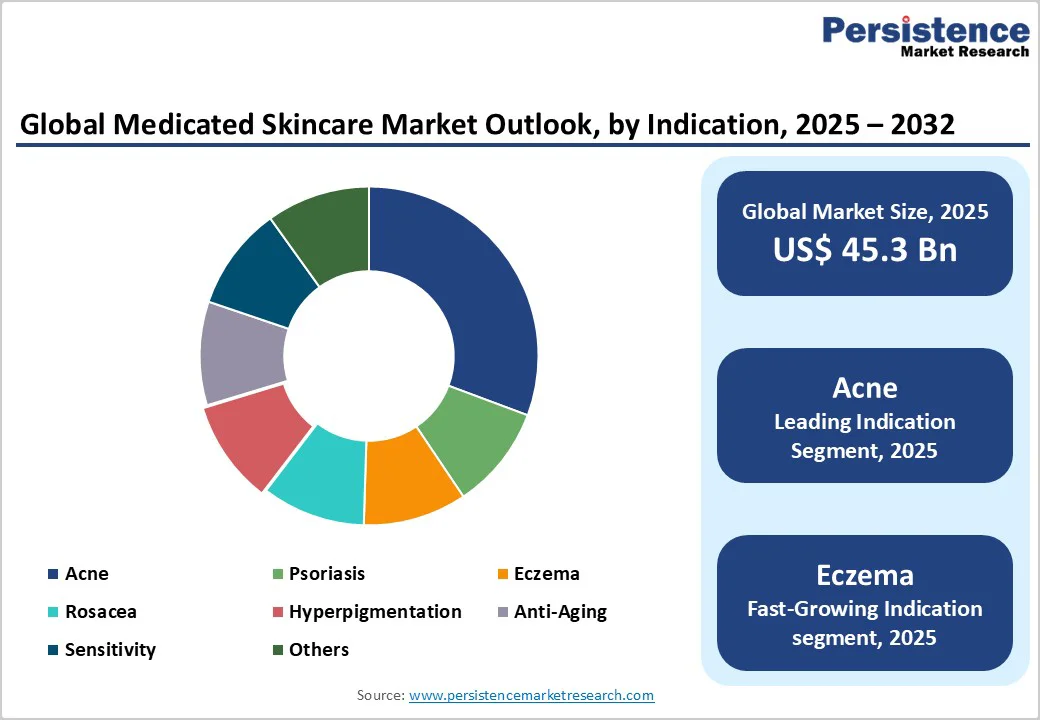

- Dominant Indication: Acne-focused medicated skincare products account for the largest share, with about 31.5% of total revenue in 2025, reflecting strong consumer demand for benzoyl peroxide, retinoid, and salicylic acid solutions with clinically validated claims.

- Leading Distribution Channel: Dermatology clinics remain the highest-value channel, with a market share of around 30.7%, driven by strong consumer trust and the clinical endorsement associated with physician-dispensed products.

| Key Insights | Details |

|---|---|

|

Medicated Skincare Market Size (2025E) |

US$45.3 Bn |

|

Market Value Forecast (2032F) |

US$66.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Prevalence and Improved Diagnosis of Skin Disorders

Higher incidence of acne, eczema, rosacea, and photo-aging has expanded the addressable patient base for medicated skincare. Greater diagnostic access, including teledermatology platforms and increased dermatology visits, contributes to early identification and longer-term treatment. Medicated formulations used in clinics often command higher prices due to greater efficacy and clinical validation. As diagnoses become more accessible and awareness increases, more patients are transitioning toward prescription-grade or physician-endorsed OTC solutions. This combination of growing patient volume and premium product adoption directly lifts revenue and strengthens recurring demand through extended treatment durations.

Advances in Clinical R&D and Cross-Sector Collaboration

Product innovation in medicated skincare has accelerated due to investments in dermatology-focused research. New formulations incorporate stabilized retinoids, microbiome-friendly actives, targeted anti-inflammatory agents, and next-generation delivery systems. Clinical studies supporting efficacy claims improve trust among physicians and consumers, thereby strengthening brand positioning and driving premium pricing. Strategic collaborations between skincare manufacturers, clinical researchers, and pharmaceutical partners accelerate differentiated product development, streamline regulatory submissions, and strengthen reimbursement pathways. As a result, clinically validated formulations achieve faster adoption across both clinic and retail channels.

Digital Dermatology, Teleconsultation, and E-Commerce Expansion

Teledermatology and online pharmacies significantly reduce the gap between diagnosis and product purchase. Digital platforms allow rapid prescription fulfillment for acne, eczema, and pigmentation concerns, while e-commerce improves availability across regions with limited dermatology infrastructure. Younger consumers increasingly rely on digital consultations, and chronic-condition subscription models simplify refills and adherence. These trends broaden market access and enable smaller brands to reach national and international customers quickly. Competitive intensity rises as digital-native medicated brands invest in data-driven marketing and tailored treatment pathways. The combined effects increase the accessibility of the total addressable market and accelerate product adoption.

Barrier Analysis - Regulatory Complexity and Compliance Burden

Medicated skincare often falls between cosmetic and pharmaceutical classifications, creating complex regulatory pathways across regions. Requirements for clinical evidence, safety testing, manufacturing audits, and post-market surveillance extend development timelines and raise operating costs. Compliance, particularly for products containing active pharmaceutical ingredients, adds substantial cost, which disproportionately affects smaller companies. These regulatory hurdles increase barriers to market entry and slow product launches, especially for innovative or high-potency formulations.

Ingredient Scrutiny, Recalls, and Rising Safety Concerns

Active ingredients such as retinoids, exfoliating acids, and antimicrobials are subject to heightened regulatory and consumer scrutiny. Manufacturing inconsistencies or contamination risks can trigger recalls, creating financial and reputational damage. The growing demand for transparency in ingredient safety increases the pressure on companies to elevate quality assurance measures. Smaller manufacturers often struggle to meet these cost-intensive safety standards, raising the risk of non-compliance. As surveillance becomes stricter, brands must prioritize rigorous testing and documentation to reduce liability exposure.

Opportunity Analysis - High-Growth Potential in Asia Pacific Markets

Asia Pacific offers the strongest growth outlook, supported by rising disposable incomes, increased diagnosis of dermatological conditions, and rapid expansion of digital healthcare. Urban pollution-induced skin concerns heighten demand for medicated solutions, while e-commerce adoption simplifies access to global and local brands. Tailoring formulations to regional skin types and sensitivities can unlock significant incremental market potential. Companies entering these markets through localized manufacturing, regulatory alignment, and dermatology partnerships can capture substantial share in a rapidly expanding consumer base.

Microbiome-Friendly Formulations and Personalized Medicated Regimens

Advances in microbiome science are reshaping product development, allowing companies to create medicated topicals that minimize irritation and support skin-barrier health. Personalized skincare powered by AI-based analysis and adaptive formulations is emerging as a premium opportunity. Subscription models for customized medicated regimens improve retention and lifetime value while meeting increasing consumer expectations for tailored solutions. If personalization captures even a modest portion of medicated skincare spend by 2032, the category could generate several billion dollars in incremental revenue. Brands that combine clinical insight with personalization platforms gain a competitive advantage.

Category-wise Analysis

Product Type Insights

Creams and ointments comprise the largest product segment with a market share of around 33% due to their versatility and compatibility with a wide range of therapeutic actives. They remain the preferred format for managing eczema, psoriasis, acne, and post-procedural care. Their ability to deliver both high-potency and barrier-repair ingredients makes them suitable for physician dispensing and recurring prescriptions. Higher-viscosity formulas offer improved stability for retinoids and corticosteroids, while ointments remain essential for managing chronic dryness and inflammation. These formulations command higher price points due to clinical validation, broad applicability, and integration into dermatology treatment plans.

Serums and medicated gels are expanding quickly as consumers seek fast-absorbing, high-potency actives for pigmentation, acne scarring, and inflammation. Dermatologists prefer these formats for targeted, high-bioavailability therapies. Growth is strengthened by online education and telederm guidance, with stabilized retinoids, azelaic acid, and peptide gel serums leading the way in performance, as efficacy drives purchasing decisions.

Indication Insights

Acne remains the largest indication within medicated skincare, holding a market share of 31.5% due to high global prevalence across adolescent and adult populations. Treatment spans multiple product types, including retinoid creams, antibacterial formulations, acid-based exfoliants, and adjunctive anti-inflammatory therapies. Longer treatment cycles, frequent recurrence, and physician-directed regimens create sustained demand. Digital consultations have increased diagnosis rates, enabling rapid prescription fulfillment and broader access to therapeutic solutions. Acne’s large patient base and wide product range give it outsized influence on overall market revenue.

Eczema-related products are experiencing accelerated demand as awareness of atopic conditions rises among both adults and children. Developments in non-steroidal anti-inflammatory formulations, advanced barrier-repair creams, and pH-balanced medicated moisturizers support growth. Many patients prefer alternatives to long-term steroid use, driving adoption of gentler but clinically effective options. Urban pollution, climatic stressors, and rising allergies contribute to the increasing prevalence. As diagnoses expand and treatment guidelines evolve, the eczema category is poised for sustained double-digit growth across several countries.

Distribution Channel Insights

Dermatology clinics remain the highest-value channel, with a market share of around 30.7%, driven by strong consumer trust and the clinical endorsement associated with physician-dispensed products. These products often support post-procedural care, acne management, and the management of chronic skin conditions that require ongoing supervision. Clinics benefit from higher margins and repeat sales, while patients value guidance and assurance of efficacy. The integration of clinic-based product lines with digital scheduling and follow-up systems further strengthens adherence and retention. As aesthetic procedures expand, so does the demand for clinic-adjacent medicated formulations.

Online pharmacies and telederm platforms are experiencing the fastest growth, driven by convenience, rapid prescription fulfillment, and broad access to specialized products. Subscription models for acne and eczema care drive predictable revenue while improving treatment adherence. Younger consumers increasingly prefer digital pathways that streamline consultation, diagnosis, and product delivery. The combination of remote care and e-commerce logistics shortens time-to-treatment, making this channel highly competitive.

Regional Insights

North America Medicated Skincare Market Trends - Clinically Driven Demand and Teledermatology-Enabled Growth

North America represents the largest regional market, holding a market share of 38.3%, supported by high healthcare expenditure, widespread dermatology access, and strong adoption of clinically validated products. The U.S. accounts for the majority of regional demand due to its extensive network of dermatology practices and robust presence of prescription-adjacent and physician-dispensed brands. High consumer awareness of skin health, preference for scientifically supported ingredients, and strong aesthetic treatment volumes make the region a lucrative environment for clinical skincare.

Digital healthcare adoption is advanced, with teledermatology platforms enabling convenient consultations for acne, eczema, and pigmentation disorders. These platforms often integrate prescription services, improving continuity of care and adherence to treatment plans. Subscription-based medicated regimens are increasingly common, offering predictable revenue streams for brands and simplified care pathways for patients.

U.S. regulations clearly distinguish cosmetics, OTC drugs, and prescription topicals, requiring strong evidence for active ingredients and manufacturing standards. While compliance raises development costs, it boosts consumer trust and supports successful OTC switches. Growth is reinforced by expanding aesthetic procedures and clinic-led distribution, which drive demand for medicated post-treatment skincare.

Europe Medicated Skincare Market Trends - Pharmacy-Led Dermocosmetic Strength and Strict Regulatory Assurance

Europe is a mature market marked by longstanding pharmacy-led distribution, strong dermocosmetic traditions, and high consumer trust in clinically supported brands. Germany, France, the U.K., and Spain represent the largest markets within the region. Pharmacy recommendation plays a significant role in product selection, influencing both OTC medical skincare and prescription-adjacent solutions.

The region benefits from well-defined regulatory standards that require stringent ingredient safety assessments and robust substantiation of claims. Harmonized regulations across EU member states allow companies to scale launches efficiently, although prescription pathways and reimbursement criteria vary by country. These differences influence product availability and pricing strategies across markets. Demographic trends, such as population aging, support demand for topical solutions that address chronic dryness, photo-aging, and inflammatory skin diseases.

The rise in pollution-related skin concerns has increased demand for medicated barrier-repair and anti-inflammatory formulations. Digital adoption has increased, with online pharmacies gaining momentum in several countries. Private teledermatology services are expanding, particularly in markets including the U.K. and Germany, where digital health infrastructure is advanced. Traditional pharmacy channels remain dominant for high-credibility medicated products. Investment activity in the region includes acquisitions of clinical skincare lines, expansion of microbiome-friendly innovations, and partnerships between dermatology clinics and product developers.

Asia Pacific Medicated Skincare Market Trends - Digital-First Expansion and High Growth in Therapeutic Skincare

Asia Pacific is the fastest-growing region in the medicated skincare market, driven by rising disposable incomes, heightened awareness of skin conditions, and the rapid expansion of e-commerce and teleconsultation services. Urban pollution, humidity fluctuations, and lifestyle shifts are contributing to the rising incidence of acne, eczema, and pigmentation issues, fueling demand for therapeutic skincare. China leads the region with substantial scale and a rapidly evolving digital ecosystem that integrates dermatology, e-commerce, and influencer-driven education. Widespread adoption of online consultations and cross-border product imports significantly accelerates market penetration. Japan’s market is shaped by demanding consumers who prioritize efficacy, safety, and cosmetic elegance in medicated formulations.

High interest in anti-aging clinical skincare also drives growth. India is another high-potential market, supported by a young population and strong uptake of teledermatology. Online pharmacies and localized brands backed by dermatologists are expanding quickly. Price-sensitive consumers drive hybrid demand for both physician-dispensed products and clinically inspired OTC formulations.

The region benefits from manufacturing advantages, with countries such as India, South Korea, and China offering cost-efficient production capabilities and advanced formulation technologies. This supports competitive pricing and rapid product development. Many global brands partner with local manufacturers or enter joint ventures to accelerate market entry. Regulatory standards vary widely across the region, with distinct classification systems for cosmetics and therapeutic products. Local clinical data requirements, ingredient approvals, and import regulations influence time-to-market and product strategy.

Competitive Landscape

The global medicated skincare market is moderately concentrated, led by companies with strong clinical credibility, R&D capabilities, and robust distribution networks. Regional and specialist brands compete in niches such as acne, hyperpigmentation, and barrier repair. Firms with validated science, dermatologist endorsements, and clinic-based channels maintain an advantage. Competitive intensity is rising as players invest in microbiome-based formulations, stabilized actives, digital prescription models, personalization technologies, and regional expansion, particularly across Asia Pacific.

Key Industry Developments

- In June 2025, Novology launched a new, dermatologist-built acne solution, based on a “clinical science” TT2 technology tailored for the skin microbiome and Indian skin types.

- In December 2024, L’Oréal acquired Dr.G, a Korean dermatologist-founded skincare brand known for its clinically formulated products such as the R.E.D Blemish Clear Soothing Cream.

Companies Covered in Medicated Skincare Market

- Galderma

- L’Oréal Group (Dermo-Cosmetics Division)

- Beiersdorf AG

- Johnson & Johnson

- Procter & Gamble

- Pierre Fabre

- Unilever

- AbbVie (Allergan Aesthetics)

- Kao Corporation

- Perrigo

- Obagi Medical

- SkinCeuticals

- Murad

- PCA Skin

Frequently Asked Questions

The medicated skincare market size in 2025 is estimated at US$45.3 Billion.

By 2032, the medicated skincare market is expected to reach US$66.1 Billion.

Key trends include rising demand for clinically validated formulations, growing adoption of microbiome-focused products, increased preference for dermatologist-backed OTC solutions, wider use of advanced delivery systems, and higher consumer spending on specialty acne-, eczema-, and pigmentation-care treatments.

Acne-focused medicated skincare is the leading segment, contributing about 31% of the total revenue in 2025.

The medicated skincare market is projected to expand at a 5.5% CAGR from 2025 to 2032.

Major players include Johnson & Johnson, Beiersdorf, L’Oréal, Galderma, and Unilever.