- Energy Storage Solutions

- Hydrogen Storage Market

Hydrogen Storage Market Size, Share, and Growth Forecast, 2026 - 2033

Hydrogen Storage Market By Product Type (Cylinder, Merchant/Bulk, On-Site, On-Board), Storage (Material, Physical) End-user (Chemical, Oil refineries, Automotive and transportation, Metalworking), and Regional Analysis for 2026 - 2033

Hydrogen Storage Market Size and Trends Analysis

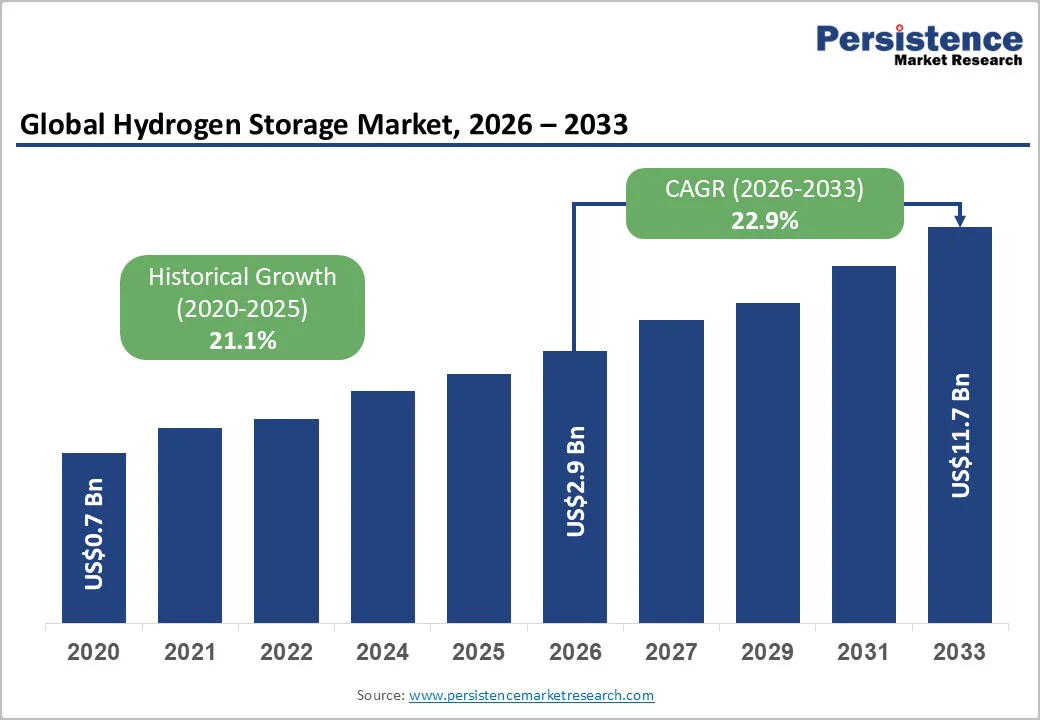

The global hydrogen storage market size is likely to be valued at US$2.9 billion in 2026. It is expected to reach US$11.7 billion by 2033, growing at a CAGR of 22.9% from 2026 to 2033, driven by rising demand for low-emission fuels as governments and industries accelerate decarbonization efforts across refining, chemicals, transportation, and power generation.

Refineries are increasingly transitioning from fossil-derived hydrogen to low-carbon and renewable hydrogen in response to stringent sulfur-reduction and clean-fuel regulations.

Key Industry Highlights

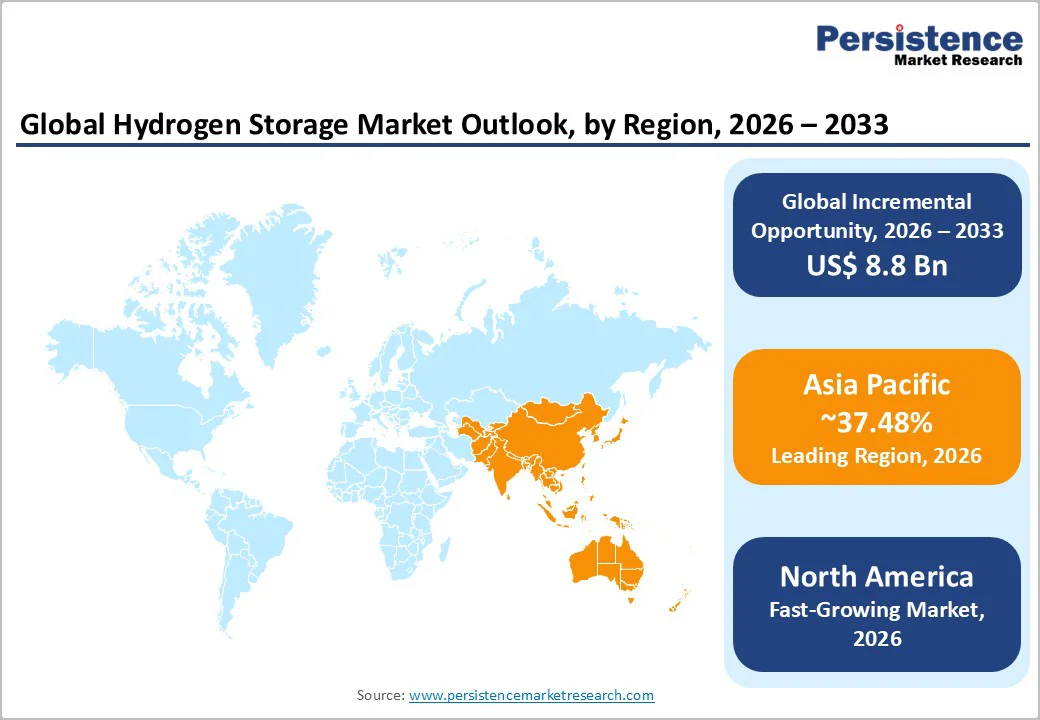

- Leading Region: Asia Pacific is anticipated to lead the market with around 37.48% share in 2026, driven by strong manufacturing hubs in China and Japan, India’s hydrogen mission, growing momentum in ASEAN, renewable integration, automotive leadership, and rapid infrastructure scaling with rising FDI.

- Fastest-growing Region: North America is likely to be the fastest-growing region, driven by U.S. hydrogen hubs, strong federal incentives, renewable-energy integration, supportive regulations, major industry innovators, large-scale investments, and emerging opportunities in underground storage.

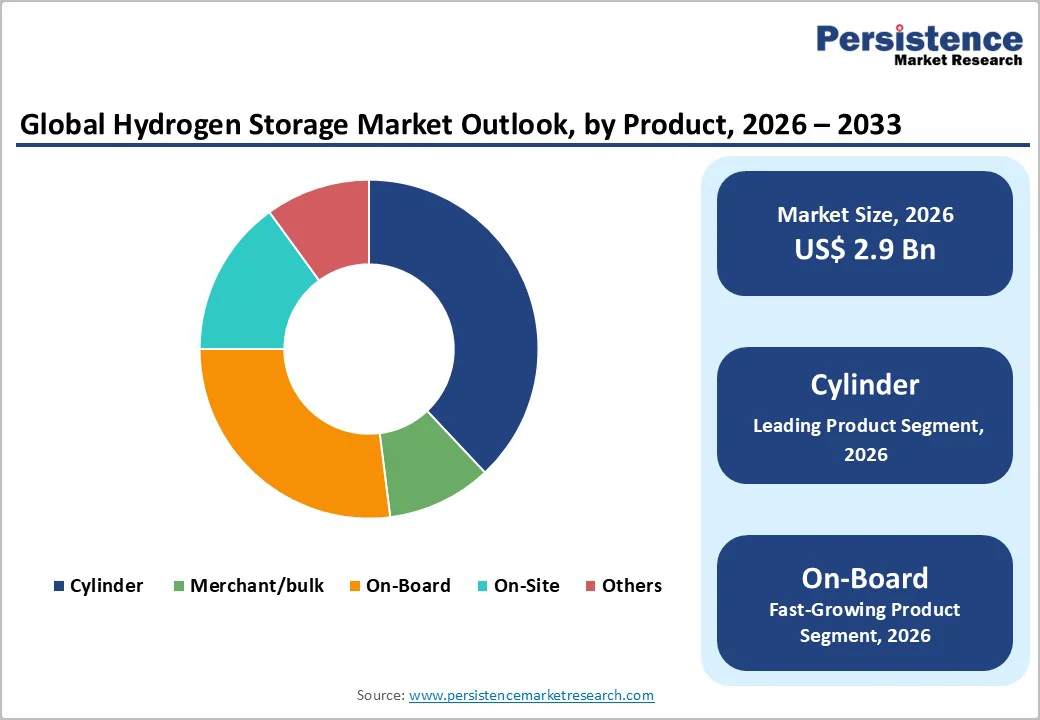

- Leading Product Type: The cylinder segment is projected to lead the market, capturing around 42.2% of the market share in 2026, supported by high-pressure reliability and broad compatibility across industrial and refinery operations.

- Leading Storage Type: Physical storage is likely to be the leading segment in the market with about 80% share in 2026, enabled by the maturity of compressed and liquefied hydrogen systems suited to existing refinery infrastructure.

- Leading End-user: Oil refineries are expected to be the leading segment in the market, with about 33% share in 2026, driven by rising desulfurization demand, which favors large-scale physical storage tanks.

| Key Insights | Details |

|---|---|

| Hydrogen Storage Market Size (2026E) | US$2.9 Bn |

| Market Value Forecast (2033F) | US$11.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 22.9% |

| Historical Market Growth (2020 - 2025) | 21.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Low-Emission Fuels

The growing demand for low-emission fuels is a key driver of the market, as governments and industries accelerate decarbonization efforts across refining, chemicals, transportation, and power generation. Stricter sulfur-reduction and clean-fuel regulations are transforming refineries, prompting a shift from fossil-derived hydrogen to low-carbon and renewable hydrogen.

This transition is also reshaping national energy strategies, with many countries incorporating hydrogen into renewable-energy systems to balance the variability of solar and wind power. As green hydrogen production scales, flexible and reliable storage solutions become critical for grid stability, energy buffering, and transportation logistics.

Industrial clusters, hydrogen hubs, and large-scale pilot projects are increasingly relying on advanced storage materials, compressed-gas systems, and cryogenic technologies to manage fluctuating renewable energy supply and meet sustainability targets efficiently.

Limited Refueling Infrastructure

Limited refueling infrastructure remains a major restraint for the hydrogen storage market, slowing adoption across transportation, industrial, and commercial sectors. Hydrogen refueling stations (HRS) require high capital investment, stringent safety compliance, and advanced compression or liquefaction systems, factors that restrict rapid deployment, especially in emerging economies.

The uneven distribution of stations creates a range anxiety effect for fuel-cell electric vehicles (FCEVs) and limits the scalability of on-board storage technologies.

The limited availability of refueling points disrupts the entire hydrogen value chain, reducing investment confidence and delaying the commercialization of high-capacity storage systems. Without widespread stations, fleet operators, logistics companies, and public transport agencies are reluctant to transition to hydrogen-powered platforms.

Industrial clusters also struggle to optimize on-site storage because inconsistent refueling access leads to higher operational costs and redundancy requirements.

Integration with Renewables for Grid Storage

The intermittency of renewable energy creates supply-demand gaps that conventional batteries cannot fully address, particularly for long-duration or seasonal storage. Hydrogen provides a scalable solution by converting surplus renewable electricity into storable energy via electrolysis, which can then be compressed, liquefied, or stored using advanced material-based systems for later use.

This capability enhances grid flexibility, supporting frequency stabilization, peak management, and renewable load balancing, and thereby strengthening global energy security.

Rising investments in green hydrogen hubs, renewable-to-hydrogen microgrids, and power-to-gas (P2G) infrastructure are further driving market growth. Across Europe, Asia-Pacific, and North America, multi-gigawatt electrolyzer projects integrated with large-scale solar and offshore wind farms are driving sustained demand for robust hydrogen storage solutions.

Technologies such as underground caverns, large-scale tanks, and solid-state materials are enabling reliable long-duration and seasonal renewable energy storage.

Category-wise Analysis

Product Type Insights

The cylinder segment is expected to lead the market, capturing around 42.2% of the total revenue share in 2026. These cylinders remain the preferred choice for both stationary and mobile applications due to their compatibility with diverse hydrogen purity requirements and their seamless integration into existing industrial processes.

For example, the continued reliance of refineries and industrial gas suppliers on high-pressure steel and composite cylinders for hydrogen distribution, with companies such as Air Liquide, Linde, and Air Products supplying bulk and packaged hydrogen via standardized cylinder networks that meet global ISO 11119 and DOT regulations.

The dominance of cylinders is further anchored by their long-standing certification standards, wide commercial availability, and robust safety profiles, making them indispensable for hydrogen handling in refineries, hydrotreating, and desulfurization processes.

On-board storage is anticipated to represent the fastest-growing product type in 2026, expanding rapidly as automotive fuel cell deployment accelerates in passenger vehicles, buses, and heavy-duty fleets. Lightweight composite cylinders significantly reduce vehicle mass, improving range and efficiency while complying with increasingly strict emission and zero-emission vehicle mandates.

The rise of hydrogen corridors, FCEV subsidies, and advancements in Type-IV tank technology are enabling faster commercialization. For example, the adoption of Type-IV hydrogen tanks by leading FCEV automakers such as Toyota (Mirai), Hyundai (NEXO), and various fuel-cell bus manufacturers globally, where composite on-board tanks certified to 700 bar are now standard for long-range mobility.

Storage Type Analysis

Physical storage is estimated to dominate the hydrogen storage market, accounting for approximately 80% of total revenue in 2026, driven by the maturity of compressed gas and liquefied hydrogen systems widely used in refineries, chemical plants, and hydrogen distribution networks.

Within physical storage, gas compression holds a leading position due to its established infrastructure, particularly for industrial hydrogen storage in hydrotreating units. Advances in liquefaction technology, including improved insulation and cryogenics, are enabling higher-density storage for transportation and mobility applications.

Material-based storage is the fastest-growing segment, driven by innovations in metal hydrides, chemical carriers, and adsorption materials to improve volumetric density, safety, and stability. As green hydrogen production scales, industries are increasingly adopting solid-state storage solutions for distributed and on-site applications.

For example, researchers at Hereon (Helmholtz-Zentrum Hereon) are developing metal-hydride-based modular hydrogen tanks under the HyCARE project that can store dozens of kilograms of hydrogen in a compact, low-pressure, safer form. Advances in nanomaterials and low-temperature hydrides are enabling compact, safe systems suitable for backup power, small-scale refueling, and renewable microgrid operations.

End-user Insights

Oil refineries are anticipated to lead the hydrogen storage market, capturing around 33% of the total revenue share in 2026, driven by continuous demand for hydrogen in desulfurization, hydrotreating, and hydrocracking processes. As global fuel standards tighten and ultra-low sulfur fuel regulations expand, refineries require larger and more reliable hydrogen storage capacities.

Physical storage tanks and high-pressure vessels dominate this segment as refineries operate on a large scale and need an uninterrupted hydrogen supply for daily operations.

Automotive and transportation represent the fastest-growing end-user, driven by the rapid expansion of fuel-cell electric vehicles (FCEVs), hydrogen buses, heavy-duty trucks, and emerging rail and maritime applications. The sector’s strong momentum comes from government incentives, zero-emission mandates, and major automakers investing in hydrogen mobility platforms.

On-board storage systems, especially Type-III and Type-IV cylinders, play a central role in enabling long-range performance and high energy density.

Regional Insights

North America Hydrogen Storage Market Trends

North America is likely to be the fastest-growing region in the hydrogen storage market in 2026, driven by strong federal and state-level support, growing clean-hydrogen production, and increasing industrial adoption. The U.S. is leading in hydrogen generation and storage infrastructure, supporting applications across industrial, chemical, and transportation sectors.

Government incentives, including production tax credits and clean-energy programs, are accelerating investment in storage solutions such as compressed gas, liquefied hydrogen, and advanced material-based systems.

Infrastructure development is driving growth in the mobility and heavy-duty transport sectors. Hydrogen fueling networks are expanding rapidly to support freight, logistics, and commercial vehicle fleets. At the same time, advanced storage technologies such as metal hydrides and nanostructured materials are being adopted for safer, more compact, and more efficient storage.

The region is also seeing a surge in hydrogen hubs integrating production, storage, and distribution, enhancing reliability for industrial and mobility applications.

Europe Hydrogen Storage Market Trends

Europe remains a significant market for hydrogen storage, due to major investments in green hydrogen production, supportive policy frameworks, and growing industrial and energy System decarbonization.

Governments and regulators are backing large-scale hydrogen hubs and infrastructure build-out, aligning with climate-neutrality ambitions under initiatives such as the new national hydrogen strategies in Germany and France, as well as broader EU decarbonization goals.

Europe is making strong strides in hydrogen mobility and transport infrastructure, which is creating fresh demand for storage solutions tailored for fuel-cell vehicles and heavy-duty transport.

Europe added dozens of new hydrogen-refueling stations, many capable of serving heavy-duty vehicles like buses and trucks, signaling that transport-oriented hydrogen demand is gaining traction. Cross-border hydrogen pipelines and a planned hydrogen backbone are enhancing Europe’s storage and distribution network.

Asia Pacific Hydrogen Storage Market Trends

Asia Pacific is expected to be the leading region in the market, accounting for 37.48% of the market share in 2026, driven by extensive investments in green and blue hydrogen production, large-scale industrial demand, and strong government support across China, Japan, South Korea, India, and Australia. T

The region’s dominance is underpinned by the strategic deployment of storage infrastructure, including high-pressure cylinders, cryogenic tanks, and underground caverns, which ensure a reliable supply for refineries, chemical plants, and industrial clusters.

Asia Pacific is also witnessing rapid growth in hydrogen mobility and renewable-energy integration, driving demand for innovative storage solutions. On-board storage for fuel-cell vehicles, material-based storage like metal hydrides, and large-scale cryogenic systems are being implemented to support transport, seasonal energy storage, and power-to-gas applications.

Cross-sector initiatives and industrial hydrogen hubs are expanding, enabling long-duration storage for variable renewable generation.

Competitive Landscape

The global hydrogen storage market exhibits a moderately fragmented structure, driven by a mix of established industrial?gas giants, specialized cryogenic storage providers, and innovative composite?tank makers.

Key leaders, including Linde plc, Air Liquide, Chart Industries, Hexagon Composites ASA, Air Products and Chemicals, Inc., and Praxair Technology, Inc., dominate much of the global capacity via cryogenic, high?pressure, and integrated hydrogen?distribution networks.

These players compete through technological innovation, broad infrastructure deployment, and strategic partnerships aimed at integrating hydrogen production, storage, and distribution. Many are investing in composite?tank and cryogenic storage technologies, expanding refueling infrastructure, and pursuing collaborations with automakers, renewables, and industrial hydrogen users to secure long-term hydrogen supply chains.

Key Industry Developments:

- In December 2025, Enagás introduced a public participation plan for its proposed 2,600 km hydrogen backbone network, aiming to gather stakeholder input ahead of construction. The Navarre section includes a key aggregation node in Tudela to support future green hydrogen production and consumption projects, helping advance the region’s 2030 Green Hydrogen Agenda.

- In June 2025, Vallourec announced DNV’s official qualification of Delphy, its vertical gaseous hydrogen storage solution. Marking a world first, Delphy enables safe storage of 1 to 100 tons of hydrogen under high safety standards.

Companies Covered in Hydrogen Storage Market

- Air Products Inc.

- Nedstack Fuel Cell Technology BV

- Iwatani Corp.

- Engie

- ITM Power

- Steelhead Composites Inc.

- Nel ASA

- Air Liquide

- Linde PLC

- Cummins Inc.

Frequently Asked Questions

The hydrogen storage market is valued at US$2.9 billion in 2026 and expected to reach US$11.7 billion by 2033, reflecting robust growth.

Key drivers include growing industrial hydrogen use, expansion of fuel-cell mobility, and integration with renewable energy systems.

Physical storage is the leading segment in the market with about 80% share, enabled by the maturity of compressed and liquefied hydrogen systems suited to existing refinery infrastructure.

Asia Pacific leads the market with around 37.48% share, driven by strong manufacturing hubs in China and Japan, India’s hydrogen mission, growing ASEAN momentum, renewable integration, automotive leadership, and rapid infrastructure scaling with rising FDI.

A key opportunity lies in integration with renewable energy for long-duration and seasonal grid storage.