- Industrial Machinery

- Hydraulic Cylinder Market

Hydraulic Cylinder Market Size, Share, and Growth Forecast 2025 - 2032

Hydraulic Cylinder Market By Product Type (Tie-Rod Cylinder, Others), Application (Industrial Equipment, Mobile Equipment), Bore Size (<50 mm, 51-100 mm, 101-150 mm, Others), Operating Principle (Single Acting, Others), and Regional Analysis for 2025 - 2032

Hydraulic Cylinder Market Size and Trend Analysis

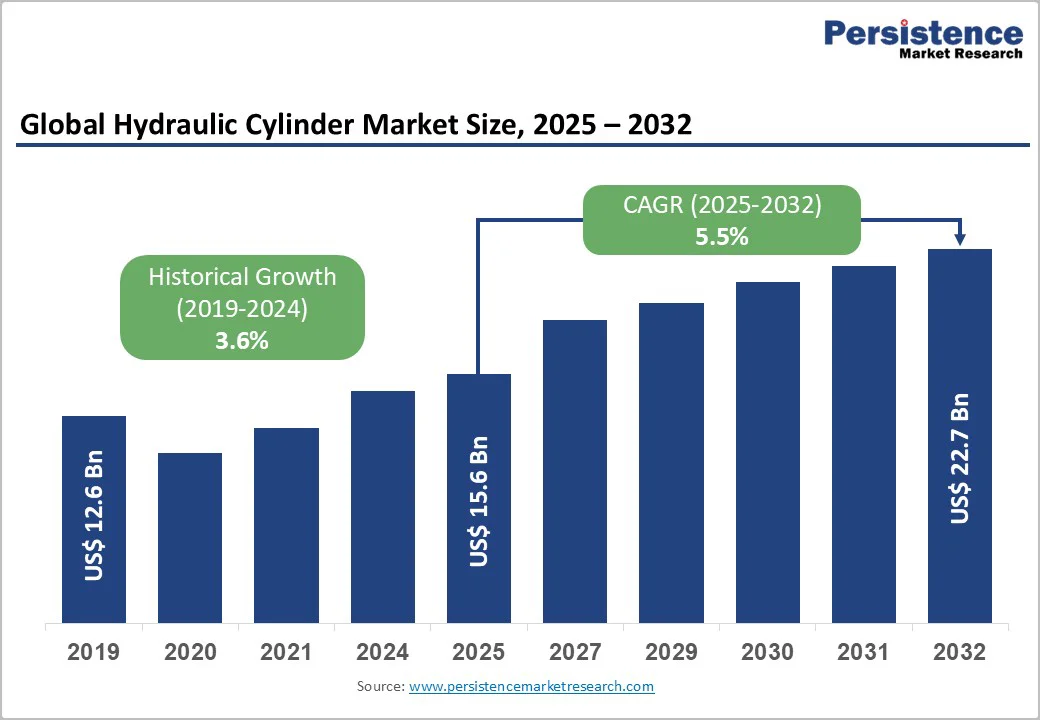

The global hydraulic cylinder market size was valued at US$15.6 Billion in 2025 and is projected to reach US$22.7 Billion by 2032, growing at a CAGR of 5.5% during the forecast period from 2025 to 2032, driven by increasing automation across industrial sectors and surging infrastructure development globally.

The market expansion is further propelled by the rising adoption of construction and agricultural machinery, particularly in emerging economies, where urbanization and mechanization are accelerating rapidly.

Key Market Highlights

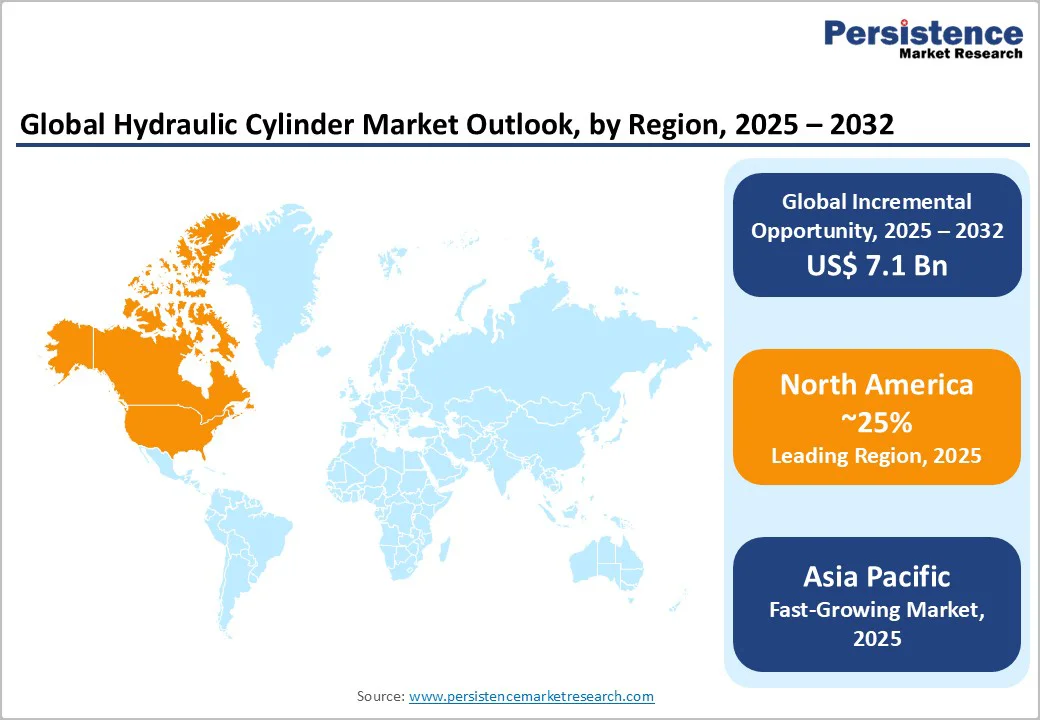

- Leading Region: North America maintains a leadership position with approximately 25% of the global market share, supported by advanced manufacturing capabilities, infrastructure investments, and technological innovation in smart hydraulic systems.

- Emerging Region: Asia Pacific leads as the fastest-growing regional market with sustained infrastructure development, manufacturing expansion, and government-supported industrialization driving hydraulic cylinder demand across diverse applications.

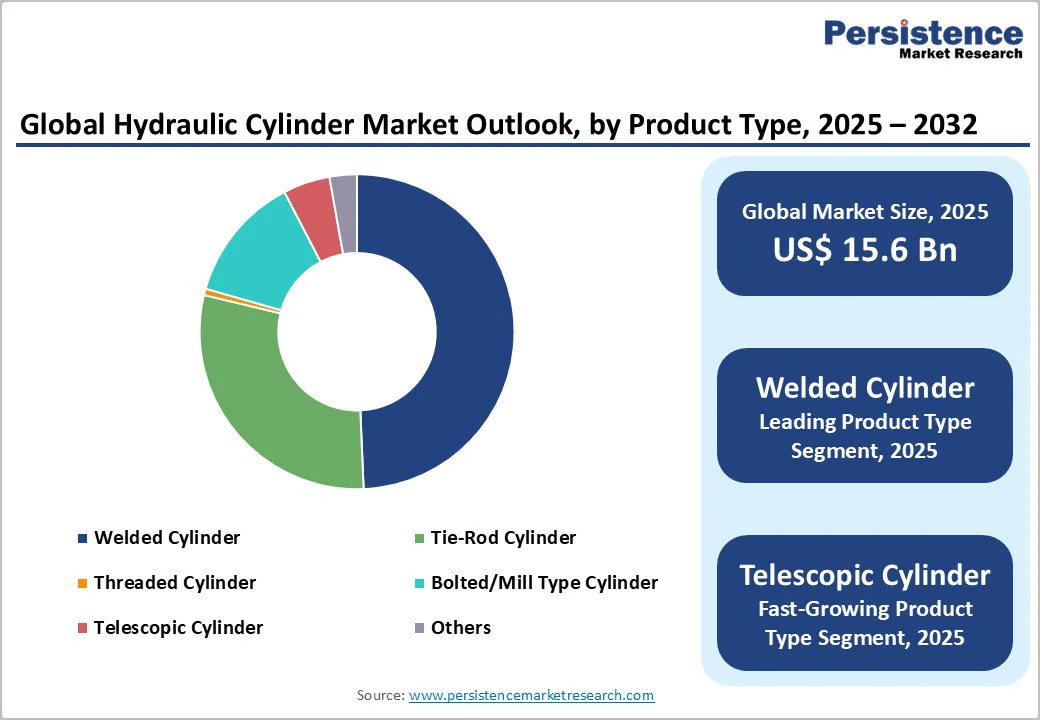

- Dominant Segment: Welded cylinders dominate the product type segment with 50% of the market share in 2025, preferred for their durability, compact design, and cost-effectiveness across mobile and industrial applications.

- Fastest-Growing Segment: Single acting cylinders represent the fastest-growing operating principle segment with 6% CAGR through 2025 - 2032, driven by cost optimization and applications requiring simplified hydraulic circuit designs.

- Key Opportunity: Smart hydraulic systems and Industry 4.0 integration create significant market opportunities through predictive maintenance capabilities, real-time monitoring, and enhanced operational efficiency across industrial applications.

| Key Insights | Details |

|---|---|

| Hydraulic Cylinder Market Size (2025E) | US$15.6 Bn |

| Market Value Forecast (2032F) | US$22.7 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.5% |

| Historical Market Growth (2019 - 2024) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Construction and Infrastructure Development Fueling Global Demand

The global construction industry boom continues to be the primary catalyst driving hydraulic cylinder demand, with unprecedented infrastructure investments across developed and emerging markets. According to industry data, construction equipment utilization has increased significantly, with hydraulic cylinders essential for operating excavators, loaders, cranes, and other heavy machinery.

Asia Pacific infrastructure spending reached approximately US$2.8-3.1 Trillion annually, while governments worldwide have launched massive infrastructure programs, including India’s National Infrastructure Pipeline worth INR 111 lakh crore (US$1.28 Trillion) through FY2025. This construction surge directly translates to higher hydraulic cylinder consumption, as these components are indispensable for powering lifting, digging, and material handling operations in construction machinery.

Accelerating Agricultural Mechanization and Automation Trends

Agricultural mechanization is experiencing unprecedented growth globally, particularly in emerging markets where traditional farming practices are rapidly being replaced by hydraulic-powered equipment. The mechanization trend spans tractors, harvesters, sprayers, and specialized agricultural implements, all requiring reliable hydraulic cylinder systems for optimal performance.

India’s agricultural machinery market demonstrates this trend with hydraulic cylinder demand growing at over 6% CAGR, driven by government initiatives promoting farm mechanization. Precision agriculture and automation technologies are increasing the sophistication of hydraulic systems, with farmers investing in advanced equipment featuring integrated hydraulic controls for improved efficiency, reduced labor costs, and enhanced crop productivity across global agricultural regions.

Barrier Analysis - High Manufacturing and Maintenance Costs Limiting Market Penetration

Hydraulic cylinder manufacturing involves complex engineering processes, precision machining, and high-quality materials, resulting in substantial initial investment costs. The production requires specialized steel forging, precise component assembly, including pistons, cylinder barrels, piston rods, and advanced sealing systems, creating significant barriers for small and medium enterprises.

Ongoing maintenance costs, including regular fluid monitoring, seal replacement, and component inspection, add to the total cost of ownership, particularly impacting cost-sensitive segments and limiting adoption in price-competitive markets.

Raw Material Price Volatility and Supply Chain Disruptions

The hydraulic cylinder industry faces persistent challenges from fluctuating raw material prices, particularly steel and aluminum, which constitute major cost components in manufacturing. Recent global supply chain disruptions have exacerbated these challenges, with manufacturers experiencing delivery delays and inventory management complexities.

Steel tubing imports and material availability variations significantly impact production costs and planning, forcing manufacturers to implement risk management strategies and potentially pass costs to end-users, thereby affecting market growth in price-sensitive applications and regions.

Opportunity Analysis - Smart Hydraulic Systems and Industry 4.0 Integration Creating New Revenue Streams

The integration of IoT sensors, artificial intelligence, and predictive maintenance technologies into hydraulic cylinders represents a transformative opportunity for market participants. Smart hydraulic systems featuring embedded sensors for real-time monitoring of pressure, temperature, position, and performance parameters are gaining traction across industries. These advanced systems enable predictive maintenance, reducing unplanned downtime by up to 70% according to industry studies.

The Industry 4.0 revolution is driving demand for connected hydraulic solutions that can integrate with SCADA systems, PLCs, and cloud-based monitoring platforms, offering manufacturers opportunities to develop higher-value products with recurring service revenue models and enhanced customer relationships.

Green Hydrogen and Renewable Energy Applications Driving Innovation

The global transition toward green hydrogen production and renewable energy infrastructure is creating substantial opportunities for hydraulic cylinder manufacturers to develop specialized products for emerging applications. Green hydrogen production facilities require precise hydraulic systems for electrolysis equipment operation, while offshore wind installations demand robust marine-grade hydraulic cylinders for turbine positioning and maintenance.

The renewable energy sector expansion, supported by government policies worldwide, is driving demand for hydraulic solutions in solar tracking systems, wind turbine control, and energy storage applications. China’s renewable energy investments exceeding US$890 Billion and similar commitments from other nations indicate sustained long-term opportunities in this rapidly expanding sector.

Category-wise Analysis

Product Type Insights

Welded cylinders dominate the hydraulic cylinder market with approximately 50% market share in 2025, attributed to their superior durability, compact design, and cost-effectiveness for high-volume applications. These cylinders feature welded end caps and barrel construction, providing exceptional strength for high-pressure applications up to 350 bar.

The welded design offers significant advantages, including space-efficient installation, reduced maintenance requirements, and enhanced reliability in harsh operating conditions. Their popularity spans across mobile equipment applications, including construction machinery, agricultural implements, and material handling equipment.

Manufacturing efficiencies and standardization have made welded cylinders particularly attractive for OEMs seeking reliable, cost-effective solutions, while their robust construction ensures performance in demanding applications from mining operations to marine environments.

Application Insights

Mobile equipment applications command the largest market segment with 72% market share in 2025, driven by extensive adoption across construction, agricultural, and mining machinery sectors. This dominance reflects the critical role of hydraulic cylinders in powering excavators, loaders, tractors, and specialized mobile equipment requiring high force-to-weight ratios and precise control.

The mobile segment benefits from ongoing mechanization trends, particularly in emerging markets where infrastructure development and agricultural modernization drive equipment demand. Construction equipment manufacturers such as Caterpillar, Komatsu, and regional players increasingly specify hydraulic cylinders for their reliability, power density, and operational efficiency.

The waste management equipment market integration and shipping containers handling applications further expand mobile equipment opportunities, with specialized hydraulic solutions enabling automated material handling and logistics optimization across global supply chains.

Bore Size Insights

The 51-100 mm bore size segment leads with 42% market share in 2025, representing the optimal balance between power output and application versatility across diverse industrial and mobile applications. This size range offers ideal power-to-size ratios for medium-duty applications, including agricultural tractors, construction equipment, and industrial machinery requiring moderate force capabilities.

The segment’s dominance stems from its suitability for standardized equipment designs, enabling manufacturers to achieve economies of scale while meeting diverse customer requirements. Manufacturing optimization and supply chain efficiencies favor this size range, as component standardization reduces inventory complexity and production costs.

The 51-100 mm segment serves applications from precision manufacturing equipment to mobile machinery, providing sufficient force for most operational requirements while maintaining compact installation profiles essential for modern equipment design.

Operating Principle Insights

Double acting cylinders maintain a dominant market position in 2025 with a substantial market share, preferred for applications requiring bidirectional force and precise control capabilities. These cylinders utilize hydraulic pressure for both extension and retraction strokes, enabling superior operational control and efficiency compared to single-acting alternatives.

Single acting cylinders represent the fastest-growing segment with 6% CAGR through 2025 - 2032, driven by cost optimization strategies and applications where gravity or springs provide adequate return force.

Single-acting designs offer simplified hydraulic circuits, reduced component costs, and lower maintenance requirements, making them attractive for price-sensitive applications, including dump trucks, lifting equipment, and specialized industrial machinery. The growth trajectory reflects increasing adoption in emerging markets and applications prioritizing cost-effectiveness over operational complexity.

Regional Insights

North America Hydraulic Cylinder Market Trends

North America maintains approximately 25% global market share, with the United States leading regional demand through robust construction activity and advanced manufacturing capabilities. The region benefits from substantial infrastructure investments, including highway reconstruction, airport expansions, and urban development projects, driving construction equipment demand. Government infrastructure spending programs and private sector investments in manufacturing automation continue to support hydraulic cylinder consumption across industrial and mobile applications.

The U.S. construction machinery market demonstrates resilience, with manufacturers such as Caterpillar and John Deere maintaining strong domestic production capabilities. Advanced manufacturing technologies and Industry 4.0 adoption enhance regional competitiveness, with companies integrating smart sensors and predictive maintenance capabilities into hydraulic systems. The region’s regulatory framework, emphasizing safety standards and environmental compliance, drives demand for advanced hydraulic solutions with enhanced efficiency and reduced environmental impact.

Europe Hydraulic Cylinder Market Trends

Europe represents a mature market characterized by technological innovation and stringent regulatory standards, driving premium product demand across Germany, the U.K., France, and Spain. The region leads in hydraulic technology development, with companies such as Bosch Rexroth pioneering smart hydraulic solutions and Industry 4.0 integration. European manufacturers focus on high-performance applications, including aerospace, renewable energy, and precision industrial machinery, requiring advanced hydraulic capabilities.

Germany’s engineering excellence and manufacturing expertise position the country as a global hydraulic technology leader, with numerous specialized manufacturers serving diverse industrial segments. The region’s emphasis on environmental sustainability drives the development of energy-efficient hydraulic systems and biodegradable fluids.

The EU regulatory harmonization and emission standards influence product development, with manufacturers investing in cleaner technologies and improved efficiency. The offshore wind energy sector expansion provides growth opportunities for marine-grade hydraulic cylinders and specialized renewable energy applications.

Asia Pacific Hydraulic Cylinder Market Trends

Asia Pacific emerges as the fastest-growing market with significant expansion driven by rapid industrialization, infrastructure development, and manufacturing growth across China, India, Japan, and ASEAN nations. The region benefits from massive construction projects, urbanization trends, and government-led infrastructure initiatives, creating sustained hydraulic cylinder demand. China’s Belt and Road Initiative contributes US$30.5 Billion in construction engagement, while India’s infrastructure investments approach US$1.4 Trillion through 2030.

Manufacturing advantages, including cost-effective production, skilled workforce availability, and supply chain proximity, enable regional manufacturers such as Jiangsu Hengli Hydraulic to capture global market share. The region’s agricultural mechanization accelerates hydraulic cylinder adoption, with governments promoting farm modernization and productivity enhancement.

ASEAN economic growth and industrial development create opportunities for hydraulic system suppliers, while Japan’s technological expertise drives innovation in precision hydraulic applications and automation solutions. Regional manufacturers increasingly focus on quality improvements and international expansion, supported by favorable government policies and infrastructure investments.

Competitive Landscape

The global hydraulic cylinder market exhibits moderate consolidation with established international manufacturers coexisting alongside numerous regional players serving specialized market niches.

Market leaders, including Parker Hannifin Corporation, Bosch Rexroth, Caterpillar Inc., and Eaton Corporation, maintain significant market shares through comprehensive product portfolios, global distribution networks, and technological innovation capabilities. Companies pursue growth strategies emphasizing geographic expansion, product diversification, and strategic acquisitions to enhance market position.

Research and development investments focus on smart hydraulic technologies, energy efficiency improvements, and application-specific solutions. Key differentiators include engineering expertise, manufacturing scale, service network coverage, and the ability to provide integrated hydraulic systems rather than standalone components.

Key Market Developments

- August 2024: Parker Hannifin launched the T7G Series hydraulic pump for heavy-duty truck applications, offering high efficiency, low noise performance, and compatibility with bio-based hydraulic fluids (HEES).

- June 2024: Eaton Corporation introduced the PFS 02 Particle Flow Sensor for real-time particle counting and sizing in hydraulic systems, supporting predictive maintenance and minimizing equipment downtime.

- August 2024: Wipro Infrastructure Engineering completed the acquisition of Columbus Hydraulics, expanding its North American manufacturing footprint and enhancing customized hydraulic solution capabilities across multiple industries.

Companies Covered in Hydraulic Cylinder Market

- Parker Hannifin Corporation

- Eaton Corporation

- Bosch Rexroth

- Caterpillar Inc.

- Jiangsu Hengli Hydraulic Co., Ltd.

- Wipro Infrastructure Engineering

- SMC Corporation

- Danfoss A/S

- KYB Corporation

- HYDAC

- Liebherr Group

- Weber Hydraulik

- Enerpac Tool Group

- Bailey International LLC

- Aggressive Hydraulics Inc.

Frequently Asked Questions

The hydraulic cylinder market was valued at US$15.6 Billion in 2025 and is projected to reach US$22.7 Billion by 2032, growing at a CAGR of 5.5% during the forecast period.

Key demand drivers include rising construction and infrastructure development, accelerating agricultural mechanization, industrial automation trends, and increasing adoption of smart hydraulic systems with IoT integration across global markets.

Welded cylinders dominate the market with approximately 50% market share in 2025, preferred for their durability, compact design, cost-effectiveness, and reliability in high-pressure applications across mobile and industrial segments.

Asia Pacific represents the fastest-growing regional market, driven by rapid infrastructure development, manufacturing expansion, government-led industrialization initiatives, and increasing mechanization across China, India, and ASEAN nations.

Major opportunities in the hydraulic cylinder market include smart hydraulic systems development, Industry 4.0 integration, green hydrogen applications, renewable energy infrastructure, predictive maintenance solutions, and expansion in emerging markets with growing industrial automation needs.

Key market players include Parker Hannifin Corporation, Bosch Rexroth, Caterpillar Inc., Eaton Corporation, Jiangsu Hengli Hydraulic Co. Ltd., Wipro Infrastructure Engineering, SMC Corporation, Danfoss A/S, KYB Corporation, and HYDAC.