- Plastics, Polymers & Resins

- Nonwoven Fabric Market

Nonwoven Fabric Market Size, Share, and Growth Forecast 2026 - 2033

Nonwoven Fabric Market by Technology (Spun Bond, Wet Laid, Dry Laid, Other), Material Type (Polyester, Polypropylene, Polyethylene, Rayon, Other), Application (Personal Care & Hygiene, Filtration, Healthcare, Automotive, Building & Construction, Others), and Regional Analysis for 2026 - 2033

Nonwoven Fabric Market Size and Trend Analysis

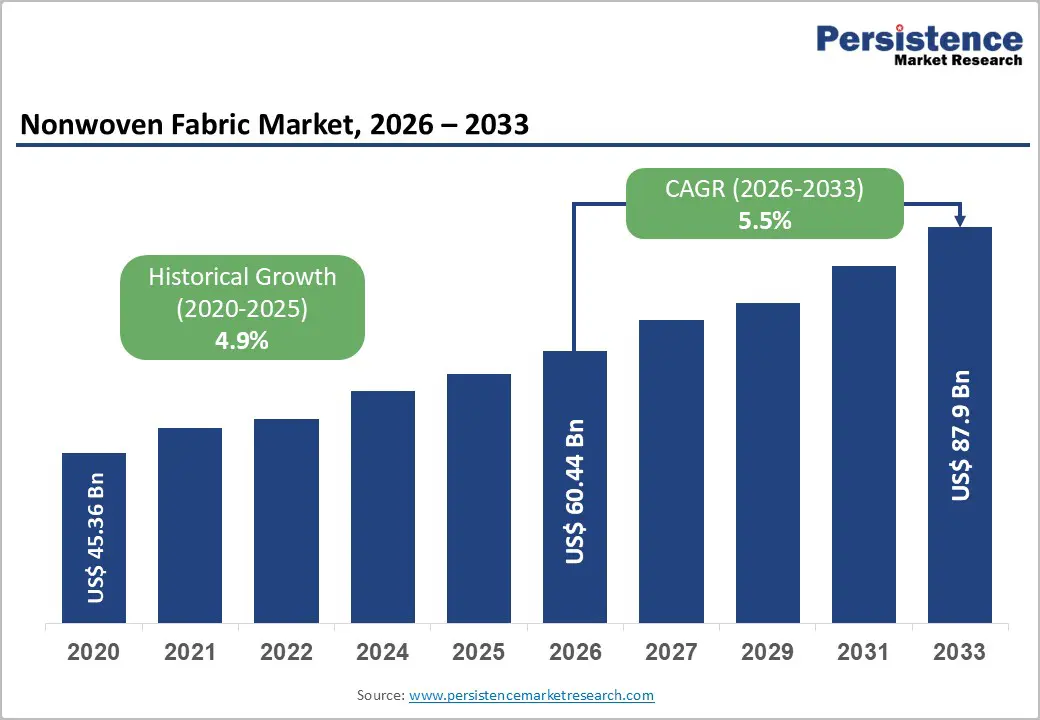

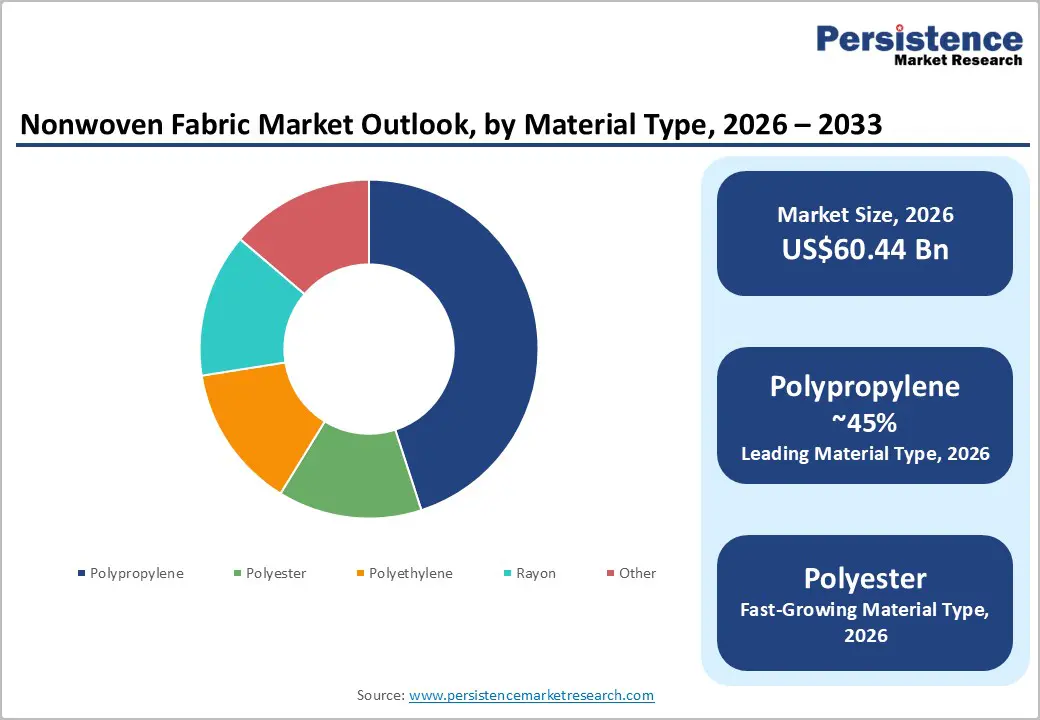

The global Nonwoven Fabric Market size is supposed to be valued at US$60.4 Bn in 2026 and is projected to reach US$87.9 Bn by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Market expansion is primarily driven by accelerating demand for disposable hygiene products in emerging economies, stringent infection-control protocols in healthcare facilities that necessitate single-use medical disposables, and automotive lightweighting initiatives that require advanced acoustic and thermal-insulation materials. Growing environmental consciousness is simultaneously propelling innovations in biodegradable and recycled nonwoven materials, while expanding filtration requirements in industrial and residential air purification systems create substantial growth opportunities for technical nonwoven applications.

Key Market Highlights

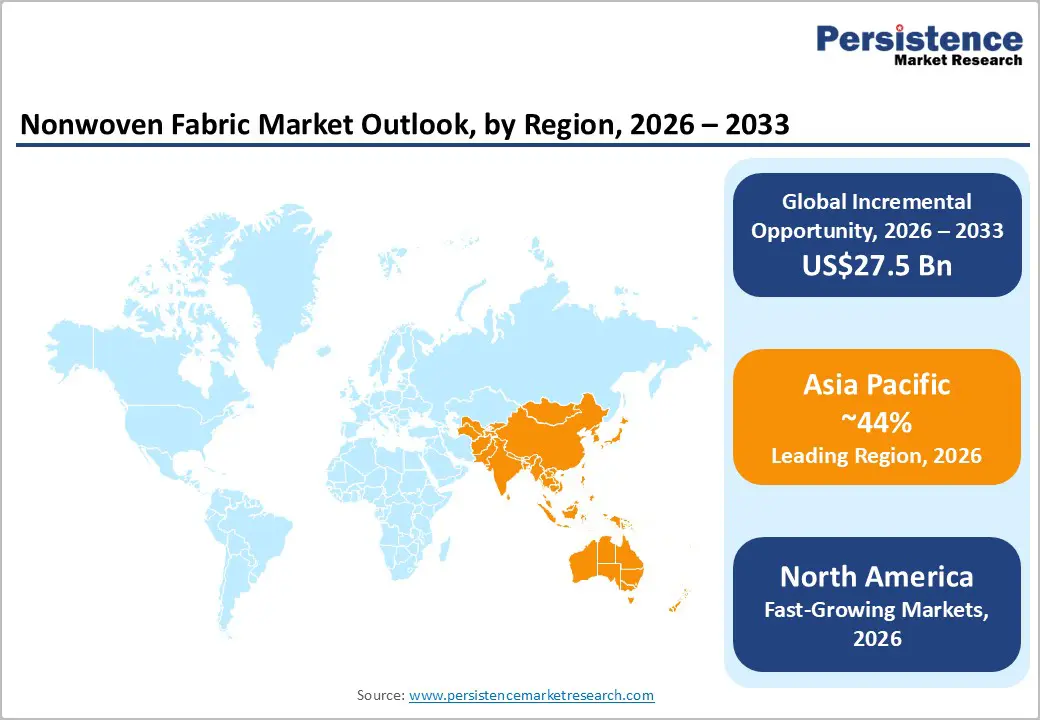

- Regional Leader: Asia Pacific leads the market with 44% market share, propelled by China's consumption reaching 5 million tons with 4.5% growth and expanding middle-class populations across India and Southeast Asia.

- Fastest-Growing Region: North America emerges as the fastest-growing region, supported by significant expansions in nonwoven production capacity, advanced manufacturing capabilities, and solid demand across hygiene, medical, and industrial applications.

- Leading Segment: Spunbond technology dominates the market with approximately 42% market share, driven by versatility across hygiene, medical, geotextile, and agricultural applications; cost-effectiveness that enables high-volume production; and continuous innovation in multilayer SMS and SMMS structures.

- Fastest-Growing Segment: Personal Care and Hygiene represents the fastest-growing application segment, with approximately 38% market share, driven by increased baby diaper consumption, expanding adult incontinence product demand, and improved penetration of feminine hygiene products.

- Key Market Opportunity: Sustainable nonwoven development presents the most significant market opportunity, as environmental regulations, with innovations in PLA fibers, agricultural waste-based substrates, and mechanical recycling systems, enabling manufacturers to address premium market segments while fulfilling regulatory compliance requirements.

| Key Insights | Details |

|---|---|

|

Nonwoven Fabric Market Size (2026E) |

US$ 60.4 Bn |

|

Market Value Forecast (2033F) |

US$ 87.9 Bn |

|

Projected Growth CAGR (2026-2033) |

5.5% |

|

Historical Market Growth (2020-2025) |

4.9% |

Market Dynamics

Market Growth Drivers

Escalating Demand for Absorbent Hygiene Products

The global nonwoven fabric market is experiencing strong growth, driven by rising consumption of absorbent hygiene products, including baby diapers, feminine hygiene products, and adult incontinence products, across both developed and emerging regions. Aging populations in North America, Europe, and East Asia are significantly expanding the population aged 65 and above, thereby sustaining demand for adult incontinence products that rely on nonwoven materials for their superior absorbency, breathability, and skin compatibility. compatible properties.

Concurrently, higher birth rates in South Asia, Southeast Asia, and Africa, combined with increasing disposable incomes, are accelerating the transition from cloth to disposable diapers. Industry bodies such as INDA and EDANA report that wipes, medical, and hygiene applications recorded the fastest growth between 2013 and 2023, with global nonwoven production rising by 5.4 % annually. Pandemic-driven hygiene awareness has further reinforced the preference for convenient, disposable solutions.

Automotive Industry Lightweighting and Acoustic Performance Enhancement

The automotive industry has become a major and rapidly expanding market for nonwoven fabrics, driven by stringent fuel-efficiency and emissions-reduction requirements across leading manufacturing regions. Due to their high strength-to-weight ratios, nonwoven materials allow automakers to replace heavier components such as carpets, headliners, door panels, trunk liners, and acoustic insulation systems, resulting in reduced vehicle weight and improved fuel economy.

The transition toward electric vehicles further broadens the potential for applications, as EVs require specialized nonwovens for battery thermal management, fire-retardant interior insulation, and noise, vibration, and harshness (NVH) mitigation. Additionally, stringent noise-pollution regulations, particularly in the European Union, are accelerating the adoption of advanced acoustic nonwovens. Growing industry commitments to sustainability are also driving demand for nonwoven fabrics produced from recycled polypropylene and polyester, supporting circular-economy objectives while maintaining rigorous performance requirements.

Market Restraints

Raw Material Price Volatility and Supply Chain Dependencies

The nonwoven fabric industry faces persistent challenges due to fluctuations in raw material costs, particularly for synthetic polymers such as polypropylene, polyester, and polyethylene, which serve as the primary feedstock for most nonwoven production. Because these materials are derived from petrochemical sources, manufacturers are directly exposed to crude oil price volatility and geopolitical supply disruptions that periodically unsettle global energy markets.

The material and supply costs reached USD 240.8 million in 2023, underscoring the high capital intensity of raw material procurement. Producers operating on narrow margins often struggle to immediately transfer rising input costs to customers, especially in price-sensitive hygiene product segments. Additionally, the concentration of raw material production in specific regions, most notably China’s dominance in polypropylene manufacturing, heightens supply chain vulnerabilities and increases exposure to potential trade policy risks.

Environmental Regulations and Growing Pressure for Sustainable Alternatives

Increasing environmental scrutiny of single-use plastics and synthetic materials is creating significant challenges for the nonwoven fabric industry. Regulatory frameworks in regions such as the European Union are introducing stringent measures, including Extended Producer Responsibility requirements, single-use plastics directives, and waste-management obligations, all of which require substantial investments in recycling infrastructure, biodegradable material development, and closed-loop manufacturing systems. These mandates impose considerable capital burdens, particularly on small and medium-sized manufacturers.

At the same time, shifting consumer preferences toward sustainable products are encouraging brands to adopt nonwovens made from renewable or recycled materials, although these alternatives often involve higher costs and technical limitations compared with conventional synthetics. Additional sustainability reporting and carbon footprint disclosure requirements further increase compliance complexity, while limited recycling infrastructure in many markets continues to hinder practical progress toward circular-economy solutions despite rising environmental expectations.

Market Opportunities

Expansion of High-Efficiency Filtration Applications

The filtration segment offers significant growth potential for technical nonwoven fabrics, driven by rising awareness of air quality, stricter industrial emission standards, and expanding liquid filtration applications. Melt-blown nonwoven technology, characterized by ultrafine fibers and microscale pore structures, is essential for producing HEPA filters capable of capturing 99.97% of 0.3-µm particles. Increasing adoption of residential air purifiers in pollution-affected urban regions, particularly in China, India, and Southeast Asia, is further accelerating demand.

Industrial applications such as HVAC systems, cleanrooms, pharmaceutical manufacturing, and automotive cabin air filtration require advanced nonwovens with high dust resistance. holding capacity, low pressure drop, and long service life. Post-pandemic focus on airborne pathogen control has strengthened demand for high-performance respiratory protection. Additional applications include EV battery thermal management, oil and fuel filtration, and water treatment systems, supported by ongoing melt-blown capacity expansion in North America and Europe.

Infrastructure Development and Geotextile Applications

The building and construction sector presents strong growth potential for nonwoven fabrics, particularly in geotextile applications used for road construction, erosion control, drainage, waterproofing, and soil stabilization. Nonwoven geotextiles made from polypropylene or polyester provide essential separation, filtration, and drainage functions that enhance road durability by preventing the mixing of subgrade and aggregate. INDA reports that such applications can increase the load-carrying capacity of roads and railway tracks by more than 50% through improved stress distribution and reduced lateral spreading.

Infrastructure programs across India, Southeast Asia, Latin America, and Africa are increasingly adopting these materials to reduce maintenance costs and extend service life. Beyond geotextiles, nonwovens serve as roofing underlayments, offering waterproofing, vapor-barrier performance, and thermal insulation. Rising sustainability priorities are also driving the use of biodegradable nonwoven geotextiles made from jute, coir, and agricultural waste for temporary erosion-control applications.

Category-wise Insights

Technology Analysis

Spun Bond technology remains the dominant segment of the nonwoven fabric market, accounting for 42% of global share due to its versatility, cost efficiency, and suitability for high-volume production of durable materials. The process involves extruding continuous thermoplastic filaments that are bonded mechanically or thermally to produce fabrics with high strength, uniformity, and dimensional stability. According to EDANA and INDA, spun-laid technologies, including spunbond, significantly contributed to the 5.4% annual growth in production from 2013 to 2023.

In 2024, China alone added more than 450 thousand tons of new spunbond and meltblown capacity, including around 32 combined production lines, reflecting sustained investment. Polypropylene spunbond materials serve hygiene, medical, geotextile, and agricultural markets, while polyester variants support furniture, automotive, and filtration applications. Advances such as SMS and SMMS multilayer structures enhance performance for protective medical apparel and filtration solutions. Modern production lines now exceed 10,000 tons per year, with widths up to 3,200 mm and speeds near 600 m/min, reinforcing the technology’s leadership.

Material Type Analysis

Polypropylene is the leading material segment in the nonwoven fabric market, accounting for about 45% of global share due to its strong balance of performance, processing versatility, and cost efficiency. Its lightweight nature, chemical and moisture resistance, hydrophobic properties, and thermal stability make it well-suited for hygiene products, medical disposables, geotextiles, and filtration media. The material’s low density enables greater surface-area coverage per unit weight, reducing raw material consumption. Where-weight requirements allow.

Polypropylene nonwovens also exhibit excellent resistance to acids, alkalis, and chemicals, ensuring durability in industrial and agricultural environments. Capable of withstanding temperatures up to 90°C, it maintains structural integrity in demanding applications. China’s dominant production capacity ensures stable availability and competitive pricing, while medical-grade polypropylene meets stringent global regulatory standards. Sustainability initiatives are further driving investment in recycled polypropylene and mechanical recycling technologies.

Application Analysis

The Personal Care and Hygiene segment is the largest application area, accounting for approximately 38% of the market, driven by strong demand for sanitary protection products and the global shift from reusable to disposable hygiene solutions. This segment includes baby diapers, feminine hygiene products, adult incontinence products, and wet and dry wipes, collectively consuming millions of tons of nonwoven materials annually. Baby diapers alone use multiple nonwoven layers, including topsheets, acquisition-distribution layers, and backsheet laminates.

Kimberly-Clark’s 150,000 square-foot expansion in Corinth, Mississippi, represents its largest investment in nonwovens, enabling innovations in comfort, sustainability, and product fit. The company’s 2024 Huggies Skin Essentials diaper features textured nonwoven liners for improved skin protection. Feminine hygiene products increasingly incorporate softer, breathable topsheets, while adult incontinence is the fastest-growing subsegment, supported by aging OECD populations and reduced social stigma.

Regional Insights

North America Nonwoven Fabric Market Trends

North America demonstrates strong market performance supported by significant expansions in nonwoven production capacity, advanced manufacturing capabilities, and solid demand across hygiene, medical, and industrial applications. INDA’s 12th annual North American Nonwovens Supply Report notes that regional capacity surpassed 5.73 million tonnes in 2024, marking a second consecutive year of additions exceeding 100,000 tonnes.

Investments across processing technologies and end-use sectors, along with larger machine installations, are expected to improve efficiency and strengthen competitiveness. Capacity expansion efforts also aim to mitigate supply-chain vulnerabilities exposed during COVID-19. Regulatory oversight and growing partnerships with sustainable-material innovators further support the commercialization of bio-based and recycled nonwovens, enhancing the region’s market position.

Europe Nonwoven Fabric Market Trends

Europe represents a technologically advanced nonwoven fabric market shaped by stringent sustainability regulations, circular-economy frameworks, and strong industry leadership in developing environmentally responsible solutions. EDANA reported a 2.6 % increase in European nonwovens production in 2024, marking a return to pre-pandemic levels. Its comprehensive statistics across multiple production processes and market segments support strategic planning and benchmarking for industry participants.

Sustainability remains central to the region’s long-term direction, reinforced by EDANA’s 2025 Sustainability and Policy Forum, which brought together industry leaders and EU policymakers to address evolving regulations related to chemicals management, product design, waste directives, and climate due diligence requirements. Regulatory initiatives such as the Single. The use of the Plastics Directive, Waste Framework Directive, and Extended Producer Responsibility schemes is driving innovation in biodegradable materials and recycling systems. Adoption varies across key markets, while medical nonwovens continue to grow due to strict infection-control standards and aging demographics.

Asia Pacific Nonwoven Fabric Market Trends

Is Asia-Pacific the largest and fastest-growing regional market, supported by China’s manufacturing leadership, expanding middle-class populations in India and Southeast Asia, and extensive infrastructure projects that use nonwoven geotextiles. China produced 8.56 million tons of nonwovens in 2024, reflecting 5.1 % year-over-year growth and reaching a nameplate capacity of about 2,003.7 thousand tons. It also led global production growth from 2013 to 2023 with a 9.4 % annual rate, adding 4.5 million tonnes.

In 2024, investment activity included new spunlace, needlepunch, spunbond/meltblown, and air-through lines totaling over 450 thousand tons, with a shift toward improved quality and digitalization. India offers strong growth potential due to low per-capita consumption and supportive government policies, while Japan, South Korea, and Southeast Asia attract investment through advanced applications, competitive costs, and favorable trade agreements.

Competitive Landscape

The nonwoven fabric market is moderately consolidated, with major multinational companies operating alongside regional and specialized manufacturers. Leading players, including Berry Global, Glatfelter, Kimberly-Clark, DuPont, and Freudenberg, maintain advantages through vertical integration, global production networks, and proprietary technologies. Ongoing consolidation, driven by mergers and acquisitions, enables firms to expand capabilities and strengthen customer relationships. Key differentiators include advanced manufacturing technologies, integrated raw-material operations, and strong R&D investments supporting continual innovation. Emerging trends include closer collaboration with end-product brands, increased investment in sustainable materials such as bio-based and recycled polymers, and adoption of digital manufacturing, automation, and AI to enhance efficiency and product quality.

Key Market Developments

- December 2025: Asahi Kasei has announced the merger of Asahi Kasei Advance Corp. with Teijin Limited, whereby Teijin Frontier will serve as the surviving company and become a joint venture between Asahi Kasei (20%) and Teijin (80%), effective October 1, 2026.

- September 2025: Glatfelter showcased several new nonwoven innovations at the INDEX23 industry event, including its sustainable GlatPure portfolio, enhanced soft fabric options like Sontara Silk and Sontara EC Green, and a home-compostable airlaid material aimed at eco-friendly applications.

- October 2025: Kimberly-Clark provided details on its strategic partnership with Suzano S.A., confirming that Suzano will pay about $1.7 Bn in cash for a 51 % majority stake in the new international tissue and professional products joint venture, while Kimberly-Clark retains a 49 % equity interest and will treat its International Family Care & Professional business as discontinued operations.

Top Companies in the Nonwoven Fabric Market

Kimberly-Clark Corporation (Dallas, U.S.) ranks among the global leaders in nonwoven fabrics through its dual role as both a major producer of nonwoven materials and the world's largest consumer of nonwovens for its hygiene products portfolio, including Huggies, Kotex, and Depend brands. The company's vertical integration strategy encompasses proprietary nonwoven manufacturing technologies developed through decades of materials science research, enabling continuous innovation in softer, stretchier, and more sustainable materials that deliver garment-like fit and feel.

Berry Global Inc. (Evansville, U.S.) operates as one of the world's largest nonwoven fabric manufacturers through its Health, Hygiene, and Specialties Nonwovens segment, supplying materials to major hygiene product brands, healthcare providers, and industrial customers globally. The company's comprehensive technology portfolio spans spunbond, meltblown, spunlace, and composite nonwoven platforms, enabling customized material solutions across diverse application requirements.

DuPont de Nemours, Inc. (Wilmington, U.S.) maintains a leadership position in high-performance nonwoven materials through its Tyvek brand, a unique spunbonded olefin material offering exceptional properties, including breathability combined with water and bacterial penetration resistance, making it indispensable for medical protective apparel, sterile medical packaging, building envelope systems, and protective covers. The company's materials science expertise and innovation heritage enable the development of specialized nonwoven solutions addressing demanding performance requirements in healthcare, construction, and industrial protection applications where conventional nonwovens prove inadequate.

Companies Covered in Nonwoven Fabric Market

- Glatfelter Company

- DuPont de Nemours, Inc.

- Kimberly-Clark Corporation

- Asahi Kasei Corporation

- Toray Industries, Inc.

- Lydall Inc.

- Ahlstrom-Munksjö Oyj

- Berry Global Inc.

- Suominen Corporation

- TWE Group

- The Freudenberg Group

- PFNonwovens Group

- Johns Manville Corporation

- Fitesa S.A.

Frequently Asked Questions

The global Nonwoven Fabric Market is valued at US$60.4 Bn in 2026 and is projected to reach US$87.9 Bn by 2033, expanding at a CAGR of 5.5% during the forecast period.

Primary growth drivers include escalating demand for absorbent hygiene products propelled by demographic shifts and urbanization, and automotive industry lightweighting imperatives requiring advanced acoustic and thermal insulation materials.

Spun Bond technology commands the leading position with approximately 42% market share, attributed to its versatility across diverse applications, cost-effectiveness enabling high-volume production, suitability for manufacturing durable nonwoven materials, and continuous innovation in multilayer structures.

Asia Pacific exhibits the domination in the market, driven by China's consumption reaching 5 million tons with 4.5 % annual growth, and expanding middle-class populations across India and Southeast Asia.