- Energy Storage Solutions

- Hydrogen Tube Trailer Market

Hydrogen Tube Trailer Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Hydrogen Tube Trailer Market by Trailer Type (Modular Tube Trailer, Intermediate Trailer, Jumbo Tube Trailer), Pressure Rating (Below 250 Bar, 250 to 500 Bar, Above 500 Bar), Application (Industrial Use, Hydrogen Fuel Stations), and Regional Analysis for 2026 - 2033

Hydrogen Tube Trailer Market Share and Trends Analysis

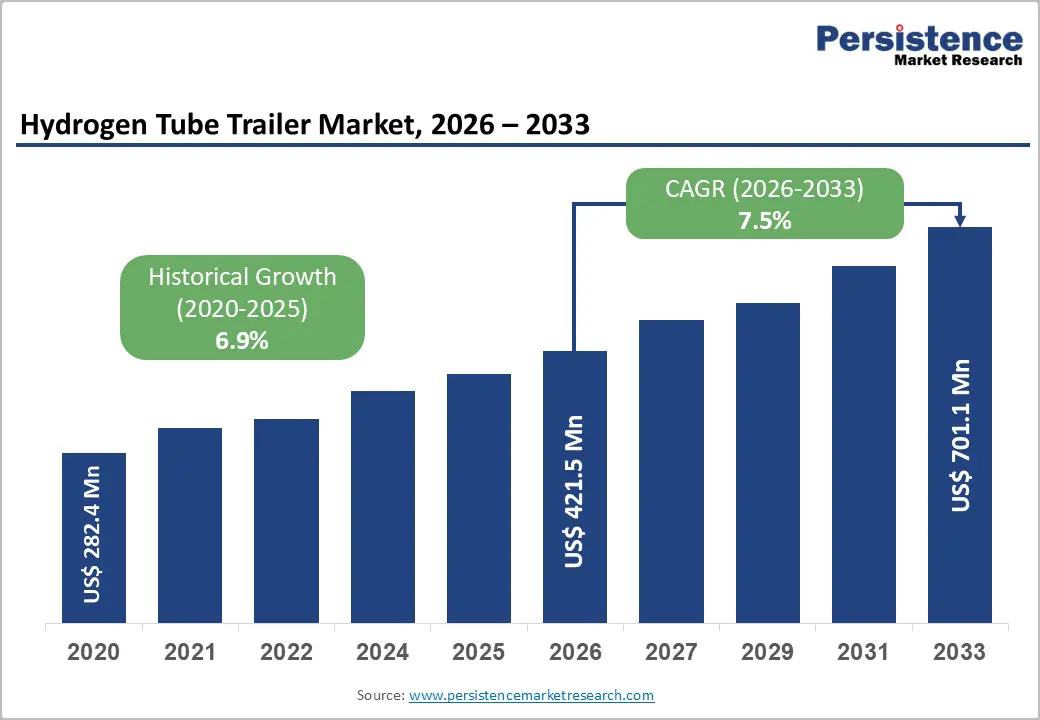

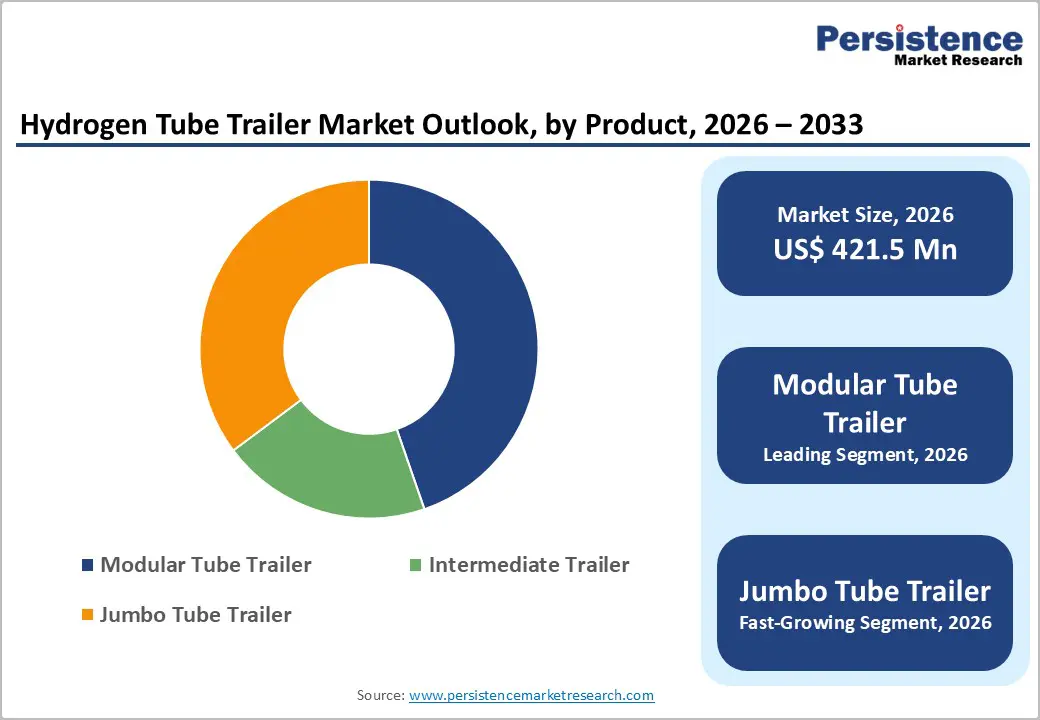

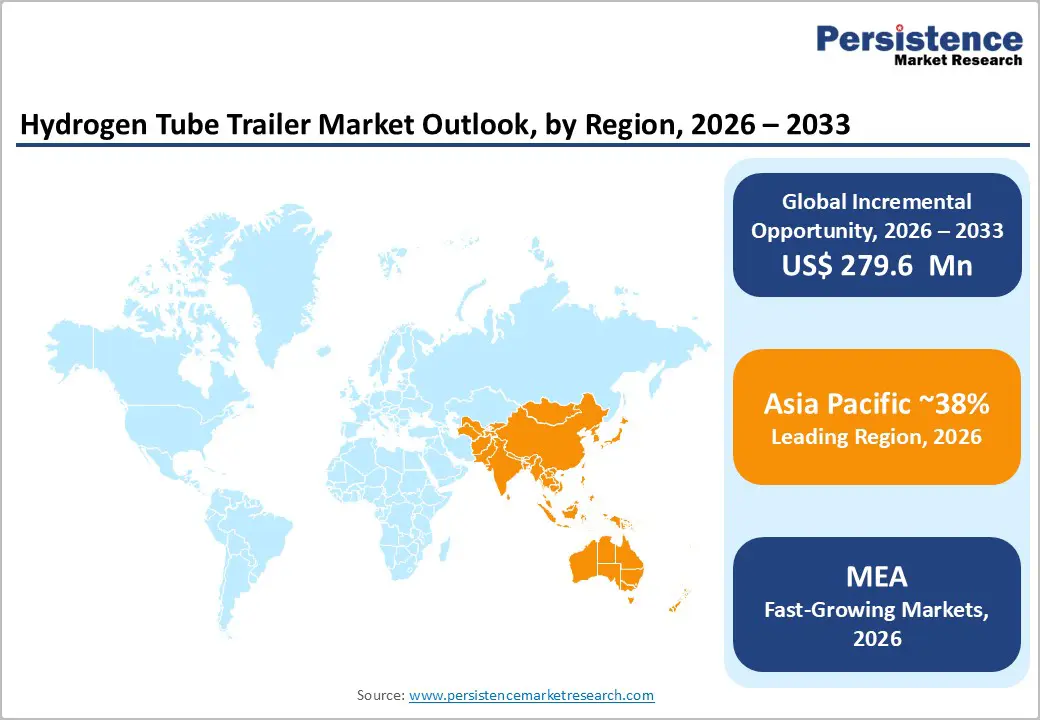

The global hydrogen tube trailer market size is projected at US$ 421.5 million in 2026 and is projected to reach US$ 701.1 million by 2033, growing at a CAGR of 7.5% between 2026 and 2033. Expansion aligns with hydrogen demand reaching 179.9 MT by 2030, driven by industrial applications, fuel cell mobility and refueling infrastructure buildout. Investments in production and transport networks, coupled with policy support for decarbonization, underpin fleet requirements for safe, high-capacity gaseous hydrogen delivery where pipelines remain underdeveloped.

Key Industry Highlights:

- Modular tube trailers dominate the market with nearly 45% share, while jumbo trailers are witnessing the fastest growth at 8.3% CAGR due to rising demand for higher hydrogen payload transportation.

- 250-500 bar pressure trailers account for around 40% of market demand, whereas above-500 bar systems are expanding at 8.2% CAGR, supported by advancements in composite cylinder technologies.

- Industrial applications contribute about 54% of total demand, but hydrogen fuel stations are emerging as the fastest-growing application, projected to expand at 8.8% CAGR with accelerating station deployments.

- Asia Pacific leads the global market with roughly 38% share, while Europe is projected to grow steadily at 7.3% CAGR, driven by strong hydrogen policies and infrastructure investments.

| Key Insights | Details |

|---|---|

| Hydrogen Tube Trailer Market Size (2026E) | US$ 421.5 million |

| Market Value Forecast (2033F) | US$ 701.1 million |

| Projected Growth CAGR (2026 - 2033) | 7.5% |

| Historical Market Growth (2020 - 2025) | 6.9% |

Market Dynamics Analysis

Drivers - Accelerating Hydrogen Infrastructure Development

Government-backed hydrogen roadmaps across major economies are catalyzing significant investments in hydrogen transport and distribution infrastructure. The European Union's Hydrogen Strategy targets 40 GW of electrolyzer capacity by 2030, necessitating extensive tube trailer fleets for last-mile hydrogen delivery. The U.S. Department of Energy's Hydrogen Shot initiative aims to reduce clean hydrogen costs to US$ 1/kg within a decade, prompting expanded logistics networks. Japan's hydrogen supply chain development program has allocated over US$ 3.4 Bn through 2030. These public investments are directly stimulating tube trailer procurement across industrial gas distributors, energy companies, and logistics providers globally, with demand expected to intensify as electrolyzer output scales considerably.

Decarbonization Mandates and Emission Regulations

Stringent carbon reduction targets are compelling industries to transition from fossil-based fuels toward clean hydrogen, amplifying tube trailer demand. The EU's Fit for 55 package mandates a 55% reduction in greenhouse gas emissions by 2030, with hydrogen positioned as a cornerstone decarbonization vector for hard-to-abate sectors including steelmaking, ammonia production, and heavy transport. China's 14th Five-Year Plan explicitly targets 1 million hydrogen fuel cell vehicles by 2030, creating substantial demand for high-pressure tube trailers. South Korea's Hydrogen Economy Roadmap commits to deploying 15,000 hydrogen buses and 200 hydrogen refueling stations, further amplifying logistical infrastructure requirements and underpinning robust medium-to-long-term procurement cycles for tube trailer manufacturers.

Restraints - High Capital Investment and Certification Costs

The production of high-pressure tube trailers involves substantial capital expenditures in specialized materials, including CFRP composites and precision-engineered valves, alongside rigorous certification processes mandated by bodies such as the UN ECE R134, ISO 11515, and DOT regulations. Certification compliance can add 15 to 25% to per-unit manufacturing costs, creating significant barriers for new market entrants and constraining capacity expansion among smaller regional players. These cost pressures limit market accessibility, particularly in price-sensitive emerging economies where infrastructure budgets remain constrained.

Pipeline Hydrogen Infrastructure as Competing Alternative

The expanding development of dedicated hydrogen pipeline networks in Europe and Asia poses a medium-term displacement risk for tube trailer logistics. Germany's planned 9,700 km hydrogen pipeline network, targeted for completion by 2032, alongside similar pipeline initiatives in the Netherlands and Belgium, may reduce dependence on mobile tube trailer distribution in densely industrial regions. For large-volume, fixed-route hydrogen delivery, pipeline economics become favorable beyond a threshold volume, potentially limiting tube trailer market expansion in high-pipeline-density geographies over the forecast horizon.

Opportunities - Green Hydrogen Export Corridors and Cross-Border Logistics

Emerging green hydrogen export corridors between hydrogen-surplus nations and industrial import hubs present a significant untapped opportunity. Australia-Japan, Chile-Germany, and MENA-EU green hydrogen trade lanes are actively developing distribution logistics frameworks where tube trailers serve as critical short-to-medium haul connectors. The International Energy Agency (IEA) projects global hydrogen trade flows to reach 150 Mt/year by 2050. Tube trailers operating in port logistics, connecting hydrogen import terminals to downstream consumers, represent a growing incremental market estimated to contribute meaningfully to overall trailer demand across the 2026-2033 forecast period.

Industrial Decarbonization in Emerging Economies

Rapidly industrializing economies across Southeast Asia, India, and Latin America are formulating national hydrogen strategies that will necessitate cost-effective distribution solutions. India's National Green Hydrogen Mission targets 5 MMT of green hydrogen annual production by 2030, creating significant distribution infrastructure requirements. In these markets, tube trailers offer a practical alternative to capital-intensive pipeline networks during early infrastructure development stages. The combination of growing industrial hydrogen consumption in refining, fertilizers, and chemicals, alongside nascent FCEV ecosystems, positions emerging economies as the next high-growth frontier for hydrogen tube trailer manufacturers and distributors through 2033.

Category-wise Analysis

Trailer Type Insights

Modular tube trailers lead with approximately ~45% market share, favored for their flexibility in configuration, ease of maintenance and compatibility with standard chassis across diverse applications. Typically featuring 4-6 tubes at 250-500 bar, they dominate short- to medium-haul routes serving industrial sites and fuel stations where payload optimization balances with regulatory weight limits. Their standardized design facilitates rapid deployment and scalability for fleet operators transitioning from legacy gas transport.

Jumbo tube trailers emerge as the fastest-growing type at ~8.3% CAGR to 2033, driven by demand for higher capacities exceeding 1 ton H2 per load in extended-range fuel station and industrial supply chains. Advances in 45-foot carbon fiber composites at >500 bar enable 20-30% payload gains over modular units, aligning with infrastructure scaling and cost-per-kg reductions essential for commercial viability.

Pressure Rating Insights

The 250 to 500 bar segment commands ~40% market share, striking a balance between payload efficiency and manufacturing costs for prevalent industrial and station applications. Operating pressures around 300-450 bar support payloads of 400-800 kg H2, suiting most current refilling infrastructure and tube materials while complying with major transport codes like ADR. This rating prevails in modular and intermediate trailers where volumetric density meets typical route economics without excessive complexity.

Above 500 bar ratings will grow fastest at ~8.2% CAGR, propelled by composite tube innovations enabling >1 ton capacities and longer ranges critical for hub-to-hub logistics. As stations upgrade compressors and steel decarbonizes via blue/green hydrogen, high-pressure trailers reduce delivery frequency by 25%, optimizing fleet productivity amid tightening emissions rules.

Application Insights

Industrial use dominates with ~54% market share, reflecting hydrogen's entrenched role in refining, chemicals, glass and electronics where tube trailers bridge production to consumption sites absent pipelines. Reliable delivery of compressed H2 at scale underpins processes like ammonia synthesis and methanol production, with fleets ensuring >95% uptime critical for continuous operations.

Hydrogen fuel stations grow fastest at ~8.8% CAGR, fueled by FCEV deployments targeting >40,000 vehicles by 2030 and station networks expanding in Europe, California and Asia. High-frequency, just-in-time deliveries demand agile modular/jumbo trailers, creating opportunities for specialized fleets integrated with station digital management.

Regional Market Insights

North America Hydrogen Tube Trailer Market Share and Trends

North America holds approximately 27% of the global hydrogen tube trailer market in 2026, underpinned by the United States' dominant position as the region's primary hydrogen consumer and distribution infrastructure developer. The U.S. market benefits from substantial federal support through the Inflation Reduction Act's US$ 3/kg hydrogen production tax credit (45V provision), directly incentivizing green hydrogen production scale-up and associated distribution logistics demand. Industrial hydrogen consumption in Gulf Coast refining, ammonia production, and emerging hydrogen mobility corridors in California and the Northeast drives consistent tube trailer procurement. Canada's growing clean hydrogen export ambitions, particularly from Alberta and British Columbia, further expand regional market scope through 2033.

The regulatory framework governed by DOT, PHMSA, and CGA standards provides a structured certification environment supporting market confidence. Strong industrial gas sector players and active venture investment in hydrogen mobility infrastructure present clear expansion opportunities for tube trailer manufacturers in the region through 2033.

Europe Hydrogen Tube Trailer Market Share and Trends

Europe is a strategically important hydrogen tube trailer market, growing at a prominent CAGR of 7.3% through 2033, driven by the EU's comprehensive hydrogen policy ecosystem. Germany leads regional demand, with its National Hydrogen Strategy allocating EUR9 Bn in public investment and a strong industrial hydrogen base in chemical and steel sectors. France's hydrogen plan committing EUR7.2 Bn and the U.K.'s Hydrogen Strategy targeting 10 GW of production capacity by 2030 are expanding distribution requirements. Spain's emerging role as a green hydrogen export hub targeting North African-sourced hydrogen inflows further amplifies trailer logistics demand across Iberian distribution networks.

Regulatory harmonization under EU pressure vessel directives and ADR transport regulations streamlines cross-border tube trailer operations. Competitive dynamics are shaped by established industrial gas multinationals and a growing cohort of specialized European tube trailer manufacturers leveraging advanced composites manufacturing capabilities.

Asia Pacific Hydrogen Tube Trailer Market Share and Trends

Asia Pacific is the leading region globally, commanding approximately 38% of global market share in 2026, propelled by China, Japan, South Korea, and India's ambitious hydrogen economy programs. China's hydrogen strategy targeting 1 million FCEVs and 1,000 refueling stations by 2025 has accelerated tube trailer fleet expansion across eastern industrial corridors. Japan's hydrogen society roadmap and well-established FCEV deployment, with over 160 operational HRS, sustains consistent demand. South Korea's Hydrogen Economy Roadmap commits to 15,000 hydrogen buses by 2030. India's National Green Hydrogen Mission is emerging as a significant growth catalyst, with distribution infrastructure at early-stage development but accelerating rapidly.

Asia Pacific's manufacturing cost advantages, high-density industrial hydrogen consumption clusters, and proactive government co-investment in hydrogen logistics infrastructure solidify the region's market leadership position. Competitive intensity is high, with domestic Chinese manufacturers gaining share through cost-competitive offerings.

Competitive Landscape

Market leaders are pursuing innovation-led differentiation through advanced composite cylinder integration, IoT-enabled fleet management, and strategic geographic expansion into high-growth Asia Pacific and European corridors. Cost leadership through manufacturing scale and supply chain localization complements premium positioning in safety-critical, high-pressure segments. Emerging business models increasingly emphasize trailer-as-a-service and long-term hydrogen logistics contracts aligned with offtake agreements.

Strategic Developments

- In May 2024, Calvera Hydrogen developed a 45-foot tube trailer with >1 ton H2 capacity at 517 bar for Shell Hydrogen, enabling global station servicing with highest-pressure certification.

- In October 2023, Calvera reported surging orders for 30 MPa trailers amid European bus/truck adoption, scaling production for urban hydrogen logistics demands.

- In August 2023, FIBA Technologies invested in next-gen valves, targeting 20% maintenance reductions for high-utilization industrial trailer operations worldwide.

Companies Covered in Hydrogen Tube Trailer Market

- Chart Industries

- Hexagon Purus

- Linde Group

- CIMC Enric Holdings

- Weldship Group

- BayoTech

- Nishal Group

- Nanliang Pressure Vessel (Shanghai)

- Shanghai Pujiang Special Gas

- Sinoma Science & Technology

- Luxfer Gas Cylinders

- Calvera Hydrogen

- FIBA Technologies

- Xinxiang Chengde Energy

- Qingdao Eleph Industry & Trade

Frequently Asked Questions

The global Hydrogen Tube Trailer Market stands at US$ 421.5 million in 2026, expanding to US$ 701.1 million by 2033 amid infrastructure scaling.

Key drivers include surging hydrogen demand to 179.9 MT by 2030, policy investments like U.S. $9.5B hubs and composite tech enabling >1-ton payloads.

The market anticipates 7.5% CAGR from 2026-2033, building on 6.9% historical growth fueled by fuel stations and industrial corridors.

Opportunities center on fuel station networks (>1,000 by 2025), industrial corridors and jumbo trailers at 8.3% CAGR for Asia Pacific dominance.

Leading players encompass Chart Industries, Hexagon Purus, Linde Group, CIMC Enric, Weldship, BayoTech and Chinese manufacturers like Nanliang and Sinoma.