- Sporting Goods & Equipment

- Football Equipment Market

Football Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Football Equipment Market by Product Type (Shoes and Cleats, Jersey, Shorts, Shins, Socks, Soccer Balls), End-user (Men, Women, Kids), Distribution Channel (Online, Specialty Stores, Sports Shops, Hypermarkets/Supermarkets), and Regional Analysis for 2026 - 2033

Football Equipment Market Size and Trend Analysis

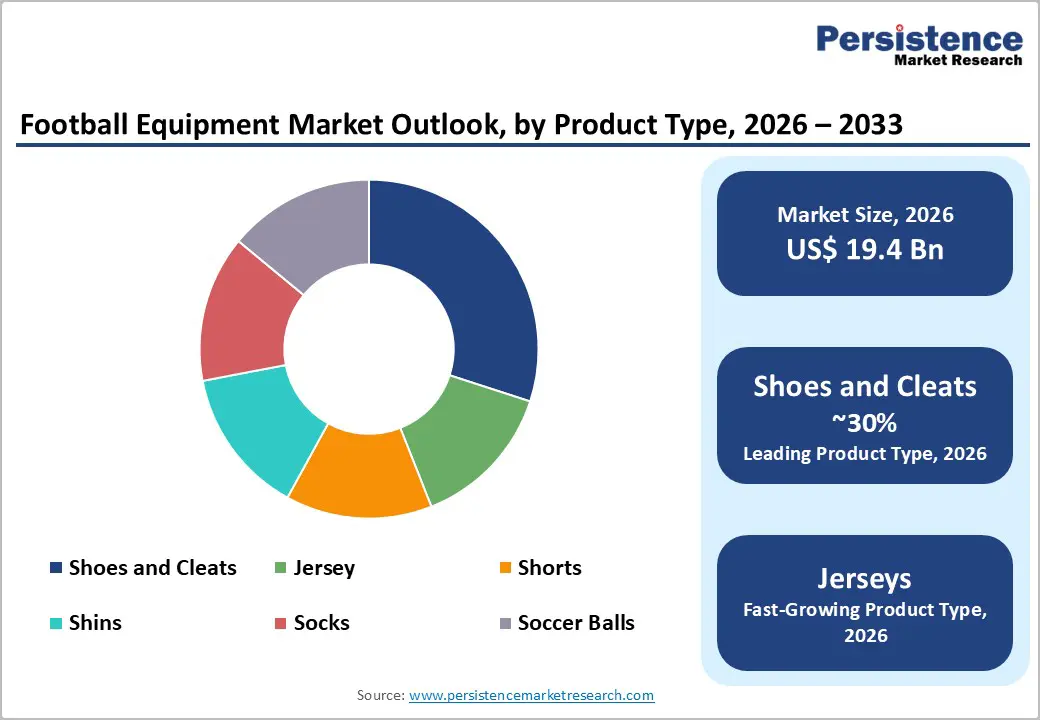

The global football equipment market size is valued at US$ 19.4 billion in 2026 and is projected to reach US$ 25.0 billion by 2033, growing at a CAGR of 3.7% between 2026 and 2033.

The market’s sustained growth is underpinned by the global expansion of organized football participation, complemented by the significant commercial uplift anticipated from the FIFA World Cup 2026 across the United States, Canada, and Mexico. Additionally, the rising involvement of women and youth is broadening the addressable consumer base for football apparel, footwear, and accessories across all major regions.

Key Industry Highlights:

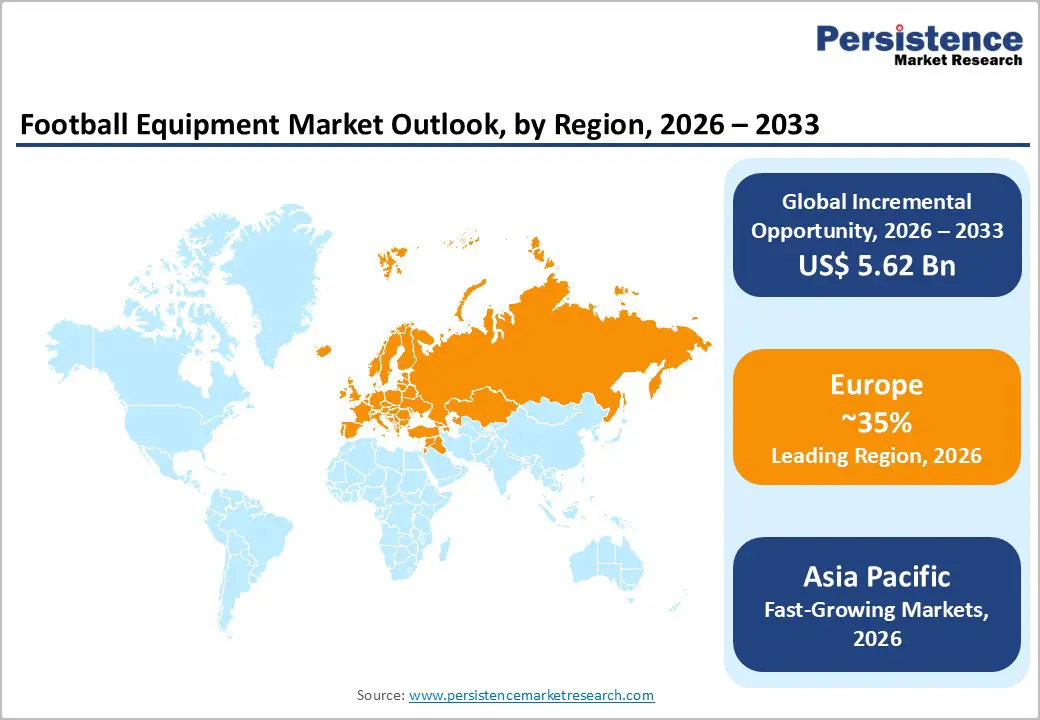

- Regional Leader: Europe leads the global football equipment market, with 35% market share, accounting for the largest share of global football equipment sales in 2024, driven by the English Premier League, La Liga, and Bundesliga, which generate year-round club merchandise and kit demand at the world's highest per-capita spending rates.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market for football equipment and remains the world’s leading manufacturing hub for football footwear, apparel, and accessories.

- Leading Segment: The Men segment dominates the global football equipment market, representing nearly 65% of total end-user revenue by 2026. This is due to higher male participation, greater spending on men’s apparel, and the strong commercial impact of men’s professional club competitions.

- Fastest Growing Segment: The Women end-user segment is the fastest-growing consumer category within the football equipment market, supported by the FA's confirmation of a 56% participation increase in England over four years and Australia's record 158,000+ women and girls actively playing football in 2024, driving OEM investment in women 's specific boot and kit product lines.

- Key Opportunity: The most significant near-term market opportunity is the FIFA World Cup 2026 demand cycle and technology-integrated premium equipment, where smart insoles, carbon fiber boot plates, and connected performance analytics are enabling brands to capture higher average selling prices across an engaged and participation-expanding global football consumer base.

| Key Insights | Details |

|---|---|

|

Football Equipment Market Size (2026E) |

US$ 19.4 Bn |

|

Market Value Forecast (2033F) |

US$ 25.0 Bn |

|

Projected Growth CAGR (2026–2033) |

3.7% |

|

Historical Market Growth (2020–2025) |

3.2% |

Market Dynamics

Drivers - Major Tournament Cycles Generating Structural Consumption Surges

Major international football tournaments serve as the most influential and recurring demand catalysts for the global football equipment market, generating multi-year cycles of elevated jersey sales, increased licensed merchandise purchases, enhanced grassroots equipment investment, and renewed participation that collectively support sustained above-trend revenue growth for manufacturers and retailers.

The FIFA World Cup 2026, co-hosted by the United States, Mexico, and Canada, represents the largest edition in history, featuring 48 participating nations and an anticipated global audience of nearly 6 billion viewers, reflecting an unprecedented commercial reach for tournament-related equipment and merchandise. This follows FIFA’s confirmation that approximately 5 billion people engaged with the FIFA World Cup Qatar 2022. Similarly, the FIFA Club World Cup 2025 in the United States drew 2.7 billion viewers and 2.5 million in-person attendees, underscoring persistent global football engagement and reinforcing the market's demand resilience throughout the forecast period.

Women's Participation Broadening the Consumer Base for Football Equipment

The rapid and well-documented rise in women’s and youth participation in football is structurally expanding the addressable consumer base for the football equipment market beyond its traditionally male-dominated foundation. This shift is driving demand for new product categories, including women-specific footwear, apparel, and protective gear. The Football Association (FA) of England reported in September 2024 that participation among women and girls increased by 56% over the preceding four years under its Inspiring Positive Change strategy, with 77% of schools offering equal access to football for girls, surpassing the 75% target.

In Australia, the 2024 National Participation Report confirmed a 10% rise in outdoor football participation and an 11% overall increase, with more than 158,000 women and girls now active in the sport. Football also remains the country’s most widely played team sport, with over 1.9 million participants. Complementing these developments, UEFA’s Time for Action strategy, supported by record-breaking attendance and viewership for the UEFA Women’s EURO 2022, reinforces the institutional commitment driving long-term growth in women’s football across Europe.

Restraints - Widespread Counterfeit Football Equipment Undermining Brand Revenue

The global football equipment market is experiencing notable revenue loss due to the widespread circulation of counterfeit and unauthorized replica products, particularly jerseys, boots, and soccer balls, sold through informal retail networks and unregulated online platforms across South Asia, Southeast Asia, Latin America, and Sub-Saharan Africa.

Counterfeit jerseys, often priced at only 5% to 10% of the genuine retail value, directly erode licensed product sales and dilute the brand equity that leading companies such as Adidas AG, Nike Inc., and PUMA SE invest substantial resources to build. Beyond financial impact, counterfeit protective equipment, such as shin guards and football boots lacking certified material standards, poses documented safety risks to players, creating reputational challenges for the entire football equipment category.

Rising Raw Material and Labor Cost Pressures Compressing Manufacturer Margins

The football equipment market continues to face sustained upward pressure on key raw material inputs, such as synthetic leathers, thermoplastic polyurethane (TPU) used in football bladders, and advanced performance fabrics, alongside rising labor costs across major manufacturing hubs in Vietnam, China, Indonesia, and Bangladesh. These escalating input costs, as reflected in Nike’s production-related challenges and resulting revenue pressures during fiscal years 2024–2025, highlight the broader commercial impact of sourcing inflation across the global athletic footwear and equipment supply chain.

Consequently, these margin constraints are accelerating manufacturing consolidation among larger companies with stronger supply chain leverage, while disproportionately disadvantaging smaller regional brands. These dynamic risks are diminishing competitive diversity, particularly within the market’s mid-tier price segment.

Opportunities - Technology-Integrated Football Equipment as a Premium Growth Segment

The integration of sensor technologies, advanced materials innovation, and data analytics is establishing a distinct, premium-priced segment within the football equipment market. These advancements enable manufacturers to command higher average selling prices, strengthen brand differentiation, and stimulate trade-up behavior among both amateur and professional players. Smart footballs equipped with motion sensors, impact-tracking modules, AI-enabled smart insoles, carbon-fiber energy-return plates, and GPS-compatible performance wearables illustrate the technological frontier now being commercialized.

Adidas’ release of 26 Predator boot colorways in 2024 highlights the scale of product diversification used to drive repeat purchases, while the company’s e-The commerce channel, which accounted for 22% of total turnover in 2023, underscores the importance of digital platforms for high-margin, technology-driven products. Declining IoT and machine-learning costs are making smart insole technologies feasible in mid-range and, eventually, entry-level price tiers. For manufacturers developing proprietary analytics ecosystems, opportunities extend beyond hardware to recurring, subscription-based sports data services.

FIFA World Cup 2026 Merchandise and Equipment Demand Surge in North America

The FIFA World Cup 2026, hosted across the United States, Canada, and Mexico, represents the most significant near-term commercial opportunity for the football equipment market in North America. The region’s expanding participation base and mature sporting goods retail ecosystem further enhanced this potential. Brands and retailers have already begun scaling inventory and licensing activities ahead of the tournament, which is expected to attract nearly 6 billion viewers.

In the United States, rising participation across youth and adult leagues continues to drive demand for equipment and licensed merchandise. As the World Cup returns to North America for the first time since 1994, it is expected to generate unprecedented commercial momentum. Historically, major retailers and e-commerce platforms have recorded peak sales during World Cup years, and the 2026 edition is projected to set new regional benchmarks.

Category-wise Analysis

Product Type Insights

The Shoes and Cleats segment remains the leading product type within the global Football Equipment Market, representing nearly 30% of total product-type revenue in 2026. Football footwear holds the highest unit value across all equipment categories, with premium boots from Adidas AG, Nike Inc., and PUMA SE priced between US$150 and more than US$300 per pair.

Performance-enhancing features such as carbon-fiber outsoles, TPU lockdown systems, and smart-insole integrations continue to drive consistent consumer trade-up behavior. Adidas’ introduction of 26 Predator colorways in 2024 demonstrates an accelerated product innovation cycle that supports repeat purchases. Apparel, including jerseys, shorts, and socks, accounts for a similarly significant revenue share, representing 55.54% of total football equipment sales in 2025, positioning footwear and apparel as the market’s two primary commercial pillars.

End User Analysis

The Men segment retains a dominant position in the global football equipment market, accounting for nearly 65% of total end-user revenue in 2026. This leadership reflects the historically larger male participation base, higher average spending on licensed men’s apparel, and the substantial commercial influence of men’s professional club competitions worldwide. The FIFA World Cup Qatar 2022 alone engaged roughly 5 billion viewers and generated record merchandise revenue, with men’s national team jerseys representing the highest-volume licensed product category.

Conversely, the Women and Kids segments are expanding rapidly. The FA reported a 56% increase in women and girls’ participation in England over four years, while Australia recorded an 11% rise in 2024, reinforcing football’s position as the nation’s leading team sport. These structural shifts are prompting OEMs to accelerate investment in women ’s-specific footwear and apparel, gradually reshaping end-user revenue distribution.

Distribution Channel Insights

The Specialty Stores channel remains the leading distribution avenue in the global Football Equipment Market, accounting for approximately 35% of total market share in 2026. This leadership is supported by the specialized role these retailers play in offering product expertise, fitting services, and hands-on performance assessments, factors that are essential for high-Involvement purchases such as football footwear and protective gear. Established chains like Fútbol Emotion in Spain, JD Sports in the UK, and dedicated football boutiques across Germany, France, and Italy continue to earn consumer trust through knowledgeable staff, exclusive brand partnerships, and extensive product assortments across all price segments.

Is the online channel the fastest-growing distribution format, with Adidas reporting that e-commerce contributed 22% of its total turnover in 2023. Growth is being accelerated by social-commerce-driven product discovery, exclusive digital-only colorway launches, and expanding direct-to-consumer investments by Nike, Adidas, and PUMA, which are increasingly drawing share away from general mass-market retail formats.

Regional Insights

North America Football Equipment Trends

North America is projected to remain the most commercially dynamic region for the Football Equipment Market through the forecast period, driven primarily by the significant demand surge associated with the FIFA World Cup 2026, co-hosted by the United States, Canada, and Mexico, and expected to reach a global audience of nearly 6 billion viewers. The United States continues to witness steady growth in organized soccer participation across youth, amateur, and professional levels, with Major League Soccer’s expansion to 30 clubs further stimulating demand for equipment and licensed merchandise.

North America also serves as a key hub for innovation in smart sports wearables and performance analytics, while structured development programs led by the U.S. Soccer Federation continue to generate new demand for entry-level boots, shin guards, and performance kits.

Europe Football Equipment Market Trends

Europe remains the global revenue leader in the Football Equipment Market, supported by the deep cultural integration of football across Germany, the United Kingdom, France, Spain, and Italy. These countries exhibit the world’s highest per-capita spending on football merchandise, with major leagues generating continuous demand through annual kit launches, player transfers, and year-round competition cycles. Europe accounted for the largest share of global football equipment sales in 2024.

Regulatory harmonization under the EU’s sustainable product and textile framework is increasingly shaping competitive differentiation, prompting brands such as Adidas and PUMA to invest in sustainable materials, including biodegradable boot concepts. Meanwhile, UEFA’s expanding investment in women’s and youth football, highlighted by the UEFA Women’s Europa Cup and the updated Women’s Champions League, continues to strengthen long-term participation and demand for equipment.

Asia Pacific Football Equipment Market Trends

Asia Pacific is the fastest-growing regional market for football equipment and remains the world’s leading manufacturing hub for football footwear, apparel, and accessories. China, Vietnam, Indonesia, and Bangladesh collectively produce most global football boots, jerseys, and soccer balls, supported by strong textile infrastructure, skilled labor, and competitive cost structures that benefit both major international brands and emerging regional labels.

India offers a significant near-term consumption opportunity, driven by the All India Football Federation’s grassroots initiatives under the Khelo India mission, which is expanding infrastructure and long-term football development. Japan continues to exhibit high demand for premium, high-specification products, with ASICS and MIZUNO competing alongside global leaders. Meanwhile, China’s investments in domestic league development and its ambition to participate in and potentially host a future FIFA World Cup are driving sustained institutional and consumer demand for equipment.

Competitive Landscape

The global football equipment market is moderately consolidated, with Nike, Adidas, and PUMA dominating the premium segment through extensive distribution networks, elite athlete endorsements, and continuous product innovation. Nike reported US$51.4 billion in revenue for 2024, while Adidas recorded EUR 21.4 billion in 2023, supported by strong e-commerce performance. Below these leaders, brands such as New Balance, Under Armour, ASICS, and MIZUNO compete through specialized footwear innovation and regional strength. Key competitive differentiators include exclusive athlete partnerships, sustainability initiatives, direct-to-consumer digital investments, and proprietary material technologies. Emerging trends include digital-physical licensed merchandise, fashion collaborations, and subscription-based performance analytics.

Key Developments:

- December 2025: Adidas has launched its latest Predator football boot, enhancing game-changing control with innovations like POWERSPINE and NANOSTRIKE+ for stability and precision. The updated design, celebrating the Predator legacy, is available worldwide and will be worn by elite players, including Jude Bellingham.

- April 2025: Nike and the NFL announced the Rivalries program, a four-season initiative featuring specially designed uniforms and fan gear that celebrate league rivalries and local communities. The first teams from the AFC East and NFC West will debut these unique uniforms ahead of select home games, with apparel available globally.

- June 2025: Boston College Athletics and New Balance have expanded their long-standing partnership to include the Eagles’ football program. Beginning in the 2025 season, New Balance will supply all BC football apparel and footwear, marking its first major NCAA football sponsorship.

Top Companies in the Football Equipment Market

Adidas AG (Herzogenaurach, Germany) is the world's most deeply embedded football equipment brand, holding the exclusive FIFA World Cup official ball supply partnership through 2030 and maintaining commercial relationships with the majority of the world's leading national teams and club franchises. Its football-specific product portfolio, spanning the Predator, X, and Copa boot families alongside 26 distinct Predator colorways launched in 2024, reflects unmatched category depth. E-commerce accounts for 22% of the company's turnover, indicating a strong transition to direct-to-consumer.

Nike Inc. (Beaverton, U.S.) is the global revenue leader in athletic footwear and apparel, with football representing one of its largest sporting category investments anchored by the Mercurial, Phantom, and Tiempo boot platforms. Nike's 2024 strategy of merging lifestyle and football performance aesthetics, exemplified by the Air Max Mercurial collaborative boot design, targets younger urban demographics and reinforces the brand's dual positioning across performance sport and street culture.

PUMA SE (Herzogenaurach, Germany) is the third global pillar of the Football Equipment Market, differentiating through high-profile athlete endorsements, sustainability innovation, including biodegradable boot concepts, and design collaborations that bridge football performance and fashion culture. It's 2025 ULTRA 6 launch and multi-sport aesthetic positioning strategy across Formula 1, and football demonstrates PUMA's ambition to build a distinctive brand identity. PUMA benefits from partnerships with national federations across Africa, Latin America, and Asia, providing a broad geographic market reach.

Companies Covered in Football Equipment Market

- Adidas AG

- Nike Inc.

- Under Armour, Inc.

- New Balance, Inc

- ASICS Corporation

- MIZUNO Corporation

- Lotto SpA

- Hummel

- BasicNet

- PUMA SE

- Baden Sports Inc.

- Diadora Spa

- Adams

- JOMA SPORT SA

- Lotto sport Italia Spa

- Schutt Sports

Frequently Asked Questions

The global Football Equipment Market is valued at US$ 19.4 Bn in 2026 and is projected to reach US$ 25.0 Bn by 2033, growing at a CAGR of 3.7%. Historically, the market grew at a CAGR of 3.2% between 2020 and 2025, supported by rising global football participation, major tournament commercial cycles, and the ongoing premiumization of football footwear and apparel driven by leaders Nike, Adidas, and PUMA.

The foremost demand drivers are the FIFA World Cup 2026 co-hosted in the U.S., Mexico, and Canada with a projected 6 billion viewers, the largest tournament in history, and the structural advance of women's and youth football participation globally, including a 56% surge in women and girls playing football in England per the FA and an 11% overall participation advance in Australia in 2024 per the Australian Government's National Participation Report.

Shoes and Cleats collectively represent the leading product type segment, accounting for approximately 30% of total product-type market share in 2026. Football footwear commands the highest individual unit value in the market, with premium boots from Adidas, Nike, and PUMA retailing above US$ 300, while apparel categories including jerseys, shorts, and socks collectively represent a 55.54% combined share of broader football equipment revenue per available industry data, making footwear and apparel the market's dual commercial pillars.

Europe is the leading region in the global Football Equipment Market, confirmed as accounting for the largest share of global sales in 2024, driven by the English Premier League, Bundesliga, La Liga, and Serie A generating sustained demand for licensed kits and performance equipment. UEFA's institutional development of women's football infrastructure and the region's dense specialist football retail network further consolidate Europe's leadership position, with Germany, the United Kingdom, France, and Spain as the dominant national markets.