- Home Appliances

- Smart Kitchen Appliances Market

Smart Kitchen Appliances Market Size, Share, and Growth Forecast 2026 - 2033

Smart Kitchen Appliances by Product Type (Large Smart Kitchen Appliances, Small Smart Kitchen Appliances), Connectivity (Bluetooth, Wi-Fi, NFC, Others), Application (Residential, Commercial), Distribution Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Smart Kitchen Appliances Market Size and Trend Analysis

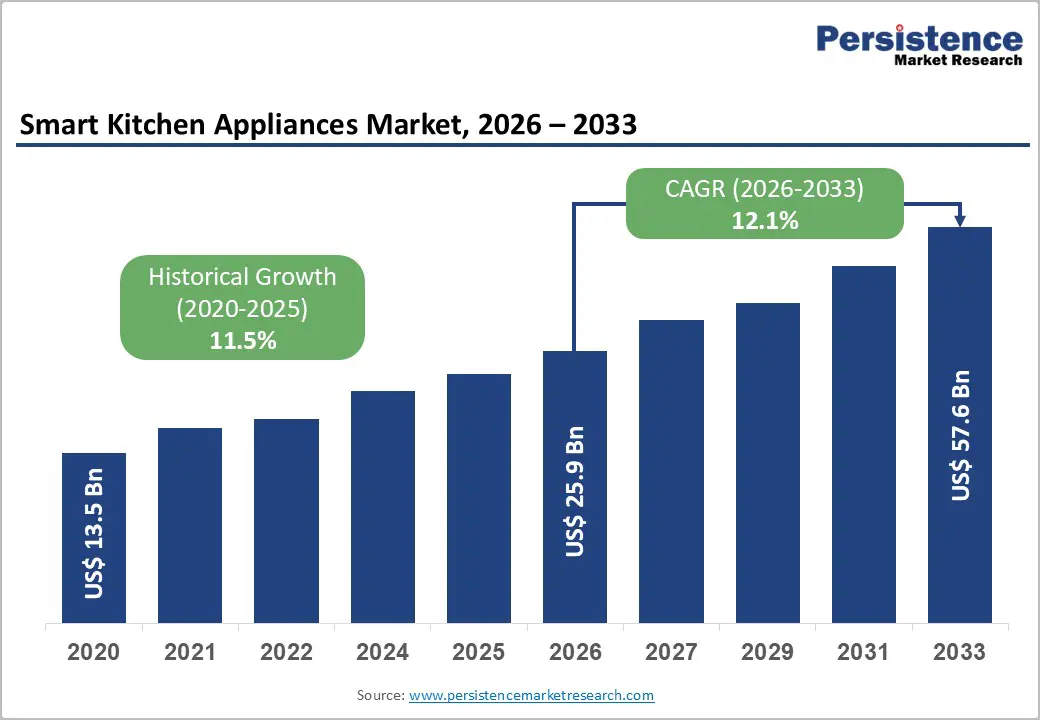

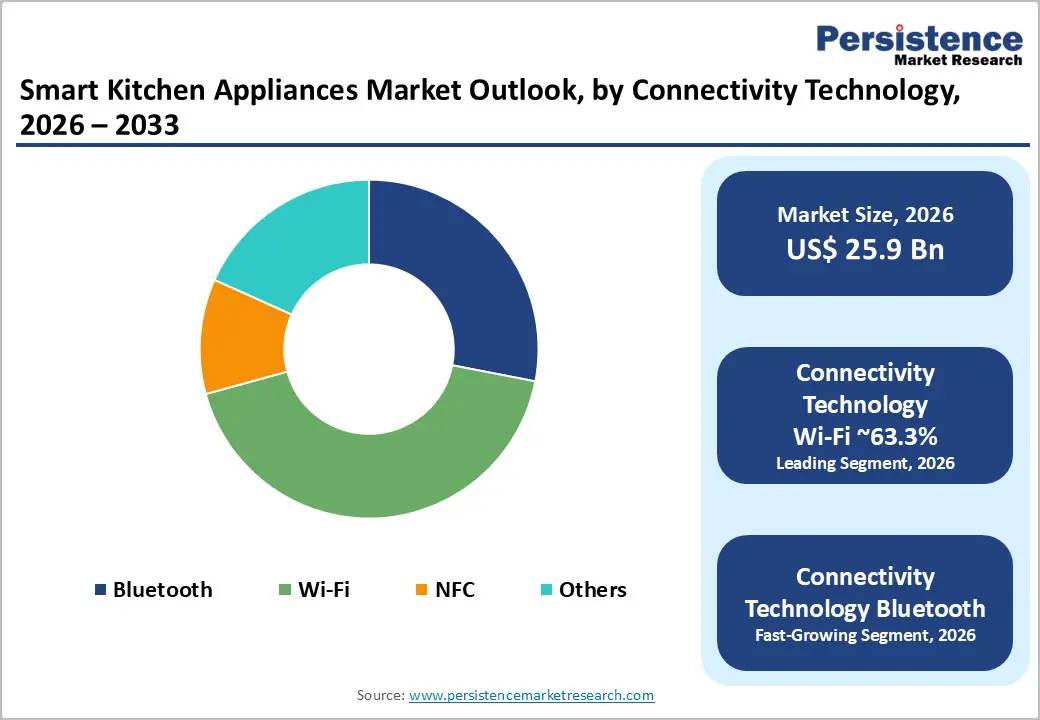

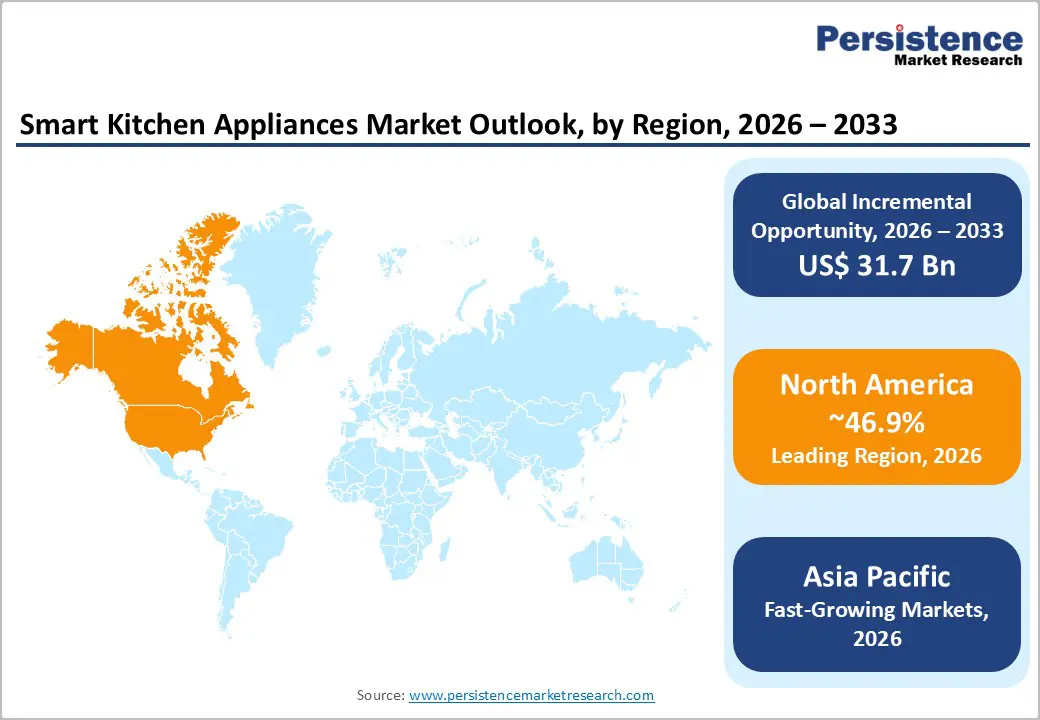

The global smart kitchen appliances market is likely to value US$ 25.9 billion in 2026 and is expected to expand to US$ 57.6 billion by 2033, registering a CAGR of 12.1% during the forecast period from 2026 to 2033.

The growth is driven by the accelerated integration of Internet of Things (IoT) technologies with residential and commercial kitchens, enabling enhanced automation, energy efficiency, and user convenience. Rising compatibility with voice assistants such as Amazon Alexa and Google Assistant is strengthening product differentiation, while the growing adoption of modular kitchens and improving living standards across both developed and emerging economies are further supporting demand for connected, intelligent cooking solutions.

Key Industry Highlights:

- Leading Region: North America leads with 46.9% share in 2024, driven by advanced technology, high disposable incomes, and smart home infrastructure enabling connected refrigerators, ovens, and dishwashers.

- Fastest-Growing Region: Asia Pacific holds 36.8% share, propelled by urbanization, rising middle-class incomes, and strong technology adoption.

- Leading Product: Smart refrigerators dominate with 39% share, featuring AI Vision Inside, remote monitoring, expiration tracking, and recipe recommendations.

- Fastest-Growing Product: Smart cooktops and intelligent appliances grow at a 19.3% CAGR through 2030, supported by precision control, energy efficiency, and meal-planning integration.

- Growth Opportunity: Commercial kitchens report 20%+ cost reductions, 25% energy savings, and 15% reductions in downtime, highlighting expansion potential.

| Key Insights | Details |

|---|---|

| Smart Kitchen Appliances Market Size (2026E) | US$ 25.9 Billion |

| Market Value Forecast (2033F) | US$ 57.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 12.1% |

| Historical Market Growth (2020 - 2025) | 11.5% |

Market Dynamics

Drivers - Rising Consumer Adoption of Smart Home Ecosystems and Connected Kitchen Technology

The rapid expansion of smart home ecosystems is significantly accelerating demand for smart kitchen appliances across residential and commercial environments. Consumers increasingly expect seamless connectivity between kitchen devices and broader home automation platforms, positioning smart refrigerators, ovens, and dishwashers as integral components of connected living. The ability to control, monitor, and automate kitchen appliances through centralized platforms enhances convenience, efficiency, and overall user experience, supporting growing adoption across global markets.

Continuous improvements in wireless connectivity and cloud-based platforms have further strengthened market penetration. Faster and more reliable communication between appliances and mobile devices enables features such as remote operation, real-time monitoring, and predictive maintenance. These advancements have made smart kitchen appliances more user-friendly and reliable, encouraging adoption across both developed and emerging economies.

Energy Efficiency Mandates and Sustainability Consciousness Among Consumers

Increasing regulatory focus on energy conservation and rising consumer awareness around sustainability are key drivers supporting smart kitchen appliance adoption. Consumers are increasingly preferring appliances that deliver energy-efficient performance, intelligent operation, and reduced environmental impact, prompting manufacturers to integrate advanced sensors and optimization technologies into product designs.

Smart kitchen appliances support efficient resource utilization through adaptive operating modes, real-time monitoring, and automated adjustments based on usage patterns. These features help reduce unnecessary energy and water consumption while maintaining performance and convenience. As sustainability becomes a central consideration in household purchasing decisions, smart kitchen solutions are increasingly viewed as practical investments that align long-term cost efficiency with environmental responsibility.

Restraint - High Initial Capital Investment and Premium Product Pricing

The high upfront cost of smart kitchen appliances compared to conventional alternatives remains a key restraint limiting widespread adoption. Premium pricing, driven by embedded connectivity, advanced sensors, and software-enabled features, often places smart appliances beyond the reach of price-sensitive consumers. Additional expenses related to installation, integration with existing kitchen infrastructure, and compatibility upgrades further elevate the total cost of ownership, discouraging first-time buyers.

While consumers increasingly recognize the long-term convenience and efficiency benefits of smart kitchen solutions, affordability concerns continue to outweigh perceived value for many households. This challenge is particularly pronounced in emerging economies, where discretionary spending capacity is limited. As a result, adoption remains concentrated in higher-income urban segments, restricting broader market penetration and slowing volume-driven growth.

Data Privacy Concerns and Interoperability Fragmentation Across Manufacturer Ecosystems

Data privacy concerns and limited interoperability across manufacturer ecosystems present significant barriers to smart kitchen appliance adoption. Many connected appliances operate within proprietary platforms, restricting seamless communication between devices from different brands and complicating integration within broader smart home environments. This fragmentation undermines the promise of unified control and convenience that smart kitchens are expected to deliver.

Growing consumer awareness around data security has heightened concerns related to appliance monitoring, usage tracking, and personal behavior data collection. The need to manage multiple applications, user accounts, and software updates further adds complexity, particularly for non-technical users. These issues reduce consumer confidence and dampen adoption rates, especially among older demographics and households prioritizing simplicity and privacy.

Opportunity - Commercialization of Smart Kitchen Solutions in Foodservice and Hospitality Operations

The foodservice and hospitality sectors represent a high-growth opportunity for smart kitchen appliance manufacturers, driven by increasing focus on operational efficiency, cost optimization, and food safety compliance. Commercial kitchens are increasingly adopting smart ovens, intelligent refrigeration systems, and connected dishwashers to improve workflow efficiency and reduce downtime through predictive maintenance capabilities. Features such as real-time monitoring, automated alerts, and performance analytics help operators streamline kitchen operations while maintaining consistent output quality.

Smart kitchen solutions also support inventory management and waste reduction through sensor-enabled refrigeration and automated tracking systems. Hotels, restaurants, and catering services are leveraging these technologies to enhance service speed, reduce labor dependency, and standardize cooking outcomes. As foodservice operators prioritize efficiency and scalability, demand for advanced, connected kitchen solutions is expected to accelerate, creating strong growth avenues for manufacturers targeting commercial applications.

Expansion of Small Smart Kitchen Appliances and Integration with Voice-Activated Assistants

The expanding adoption of small smart kitchen appliances presents a significant growth opportunity within the smart kitchen ecosystem. Products such as smart coffee makers, air fryers, blenders, and toasters are gaining popularity due to their compact design, affordability, and ease of integration into daily routines. Voice assistant compatibility and app-based controls further enhance convenience, encouraging consumer uptake across diverse demographic groups.

Manufacturers are increasingly incorporating AI-driven features such as personalized presets, intelligent cooking guidance, and real-time monitoring to differentiate products and support premium positioning. Lower price points compared to large built-in appliances make small smart kitchen devices particularly attractive in emerging markets, where they serve as entry points into kitchen automation. This segment also enables brands to build early customer engagement and foster long-term ecosystem adoption.

Category-wise Analysis

Product Type Insights

Large smart kitchen appliances dominate the market, with smart refrigerators accounting for approximately 39% market share, reflecting their central role in food storage and household management. Refrigeration remains the primary entry point for smart kitchen adoption, supported by advanced features such as internal cameras, food recognition, expiration tracking, and recipe suggestions. Continuous innovation in cooling technologies and AI-driven optimization reinforces refrigerator leadership within both premium and mid-range residential kitchens.

Small smart kitchen appliances represent the fastest-growing product category, driven by affordability, compact design, and ease of standalone operation. Smart air fryers, coffee makers, and blenders are gaining traction as entry-level automation solutions, particularly in urban households. Rapid product innovation, app-based controls, and voice assistant compatibility are expanding use cases and accelerating adoption across emerging and developed markets alike.

Connectivity Insights

Wi-Fi connectivity leads the smart kitchen appliances market with a 63.3% share, establishing itself as the dominant standard due to superior range, high data transmission capability, and seamless integration with home networks and mobile applications. Wi-Fi enables reliable remote access, real-time monitoring, firmware updates, and cloud-based analytics, making it essential for large appliances such as refrigerators, ovens, and dishwashers requiring continuous connectivity.

Interoperability-focused connectivity frameworks represent the fastest-growing technology trend. Emerging protocols are enabling smoother cross-brand communication and reducing ecosystem fragmentation, enhancing user experience across multi-device smart homes. These developments are particularly important for complex kitchen environments where appliances must coordinate functions, paving the way for broader ecosystem adoption and simplified device integration in the coming years.

Application Insights

Residential applications dominate the smart kitchen appliances market, holding 57.9% revenue share, driven by widespread household adoption. Consumers prioritize convenience, automation, and lifestyle enhancement, fueling demand for features such as remote monitoring, voice control, personalized cooking assistance, and energy optimization. Smart kitchens increasingly function as connected hubs within homes, integrating appliances with broader automation systems to improve daily efficiency.

Commercial applications represent the fastest-growing usage segment, supported by rising adoption across restaurants, hotels, catering facilities, and institutional kitchens. Foodservice operators are deploying smart appliances to improve consistency, reduce labor dependency, and enhance operational visibility. Growing emphasis on efficiency, predictive maintenance, and food safety compliance continues to accelerate smart kitchen deployment across commercial environments globally.

Distribution Channel Insights

Offline retail channels maintain market leadership with a 65.4% share, reflecting consumer preference for in-person product evaluation and professional consultation. Brick-and-mortar appliance stores, kitchen showrooms, and home improvement retailers play a critical role by offering demonstrations, installation guidance, and after-sales support. The high-value and integration-intensive nature of smart kitchen purchases reinforces reliance on physical retail expertise.

Online distribution channels are the fastest-growing route to market, driven by digital-native consumers and expanding direct-to-consumer strategies. Improved logistics, virtual demonstrations, and bundled installation services are reducing traditional online adoption barriers. Manufacturers are increasingly adopting omnichannel approaches, blending digital storefronts with selective physical presence to maximize reach and purchasing flexibility.

Regional Insights

North America Smart Kitchen Appliances Market Trends

North America leads the global smart kitchen appliances market with a commanding 46.9% share in 2024, driven by technological sophistication, high disposable incomes, and mature smart home infrastructure. The U.S. market, valued at US$ 6.11 Billion in 2023, shows strong adoption of smart refrigerators and intelligent ovens featuring AI-powered food management, voice assistant integration, and remote monitoring. Consumer familiarity with Amazon Alexa and Google Home accelerates adoption of connected kitchen solutions across households.

Canada supports regional growth with a CAGR of 17.65% through 2030, driven by urbanization, rising incomes, and product availability. Energy efficiency standards, including EPA Energy Star certifications, encourage adoption, while innovation hubs in cities like Toronto, New York, and San Francisco foster continuous product development, reinforcing technological leadership and premium appliance demand.

Europe Smart Kitchen Appliances Market Trends

The European smart kitchen appliances market is projected to grow at a CAGR of 13.2%, supported by strong regulatory backing for energy efficiency and high consumer environmental awareness. Consumers increasingly prefer appliances offering remote control, voice activation, and seamless integration with smart home systems. Advanced home automation infrastructure and engineering expertise enable sophisticated appliance development, making Europe a hub for innovation in smart kitchen technology.

Innovation centers across major cities drive continuous advancement in smart kitchen appliances, focusing on energy optimization, convenience, and lifestyle-enhancing features. The combination of regulatory incentives and consumer demand for sustainable, connected appliances encourages manufacturers to deliver advanced solutions compatible with comprehensive smart home ecosystems, strengthening market expansion and adoption across residential and commercial segments.

Asia Pacific Smart Kitchen Appliances Market Trends

Asia Pacific is the fastest-growing regional market with 36.8% share, fueled by urbanization, rising middle-class populations, growing disposable incomes, and expanding digital infrastructure. China dominates manufacturing and consumption, supported by hubs in Shanghai, Shenzhen, and Beijing. Japan’s adoption is driven by efficiency-focused consumer behavior and an aging population requiring assistance technologies. South Korea serves as an innovation hub for AI-integrated and voice-controlled appliances, while India and ASEAN countries represent emerging growth markets.

Adoption is supported by e-commerce expansion, increasing familiarity with smart home ecosystems, and willingness to invest in premium appliances. Manufacturers prioritize Asia Pacific for both commercial and residential deployments, leveraging technology-forward consumer behavior and robust urbanization trends.

Competitive Landscape

The smart kitchen appliances market exhibits moderate consolidation, with a handful of major players controlling significant market share through global manufacturing networks, extensive distribution channels, and substantial investments in AI, IoT, and smart home connectivity. Market leaders differentiate products through advanced features, rapid innovation cycles, and strategic expansion initiatives, including proprietary platform development and integration of AI-powered functionalities, creating premium pricing opportunities.

Emerging competitors, particularly in emerging markets and small appliance segments, challenge incumbents with aggressive pricing and high-specification offerings. Competitive strategies focus on predictive maintenance, voice assistant compatibility, sustainability, energy efficiency, intuitive user interfaces, and design aesthetics, fostering continuous innovation and establishing technological leadership in a rapidly evolving market.

Key Market Developments:

- In December 2024, Samsung Electronics introduced revolutionary refrigerators featuring AI Hybrid Cooling, combining traditional compressors with Peltier modules and intelligent algorithms, expanding interior capacity by 25 liters while maintaining energy efficiency at CES 2025, exemplifying market commitment to advanced climate control innovation.

- In May 2025, BSH Hausgeräte GmbH announced comprehensive Matter protocol compatibility across all 2025 United States refrigerator models, establishing industry leadership in smart home interoperability standardization and positioning the company as a connectivity innovation leader.

- In June 2025, Samsung Electronics unveiled an expanded Bespoke AI appliance lineup across India, introducing integrated AI Home displays on refrigerators and laundry equipment with advanced voice intelligence capabilities, demonstrating a strategic commitment to emerging market penetration and demonstrating AI integration potential in developing economy segments.

Companies Covered in Smart Kitchen Appliances Market

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Whirlpool Corporation

- Electrolux AB

- Haier Group Corporation

- BSH Hausgeräte GmbH

- Panasonic Corporation

- Miele & Cie. KG

- Koninklijke Philips N.V.

- Midea Group

- Breville Group Limited

- Xiaomi Corporation

- Sub-Zero Group, Inc.

- Groupe SEB

- Arçelik A.Ş.

Frequently Asked Questions

The global smart kitchen appliances market is likely to be valued at US$ 25.9 Billion in 2026 and expected to reach US$ 57.6 Billion by 2033, growing at a CAGR of 12.1%, driven by smart home integration, energy efficiency mandates, and AI/IoT innovations.

Growth is fueled by rising smart home adoption (300 million smart homes by 2025), energy-efficient solutions saving 15-30% electricity, voice assistant integration, and AI-powered personalization with predictive maintenance.

Smart refrigerators dominate with approximately 39% market share, driven by advanced features including AI Vision Inside food recognition technology recognizing 37+ food items, remote interior viewing, expiration date tracking, and recipe recommendations.

North America commands global market leadership with 46.9% market share in 2024, driven by technological sophistication, high consumer incomes, and established smart home infrastructure supporting connected appliance proliferation.

Commercial kitchens report 20%+ cost reductions, 25% energy savings, and 15% downtime reduction, while small smart appliances enable emerging market adoption in India, Southeast Asia, and Latin America.

Major companies dominating the market include Samsung Electronics, LG Electronics, Whirlpool Corporation, Electrolux AB, Haier Group, and BSH Hausgeräte.