- Medical Devices

- Hospital Equipment and Supplies Market

Hospital Equipment and Supplies Market Size, Share, and Growth Forecast 2026 - 2033

Hospital Equipment and Supplies Market by Product (Sterilization Consumables, Wound Care Products, Dialysis Products, Infusion Products, Hypodermic & Radiology Products, Intubation & Respiratory Supplies, Surgical Procedure Kits & Trays, General Disposable Products, Equipment), Application, End- User, and Regional Analysis, 2026 - 2033

Hospital Equipment and Supplies Market Size and Trend Analysis

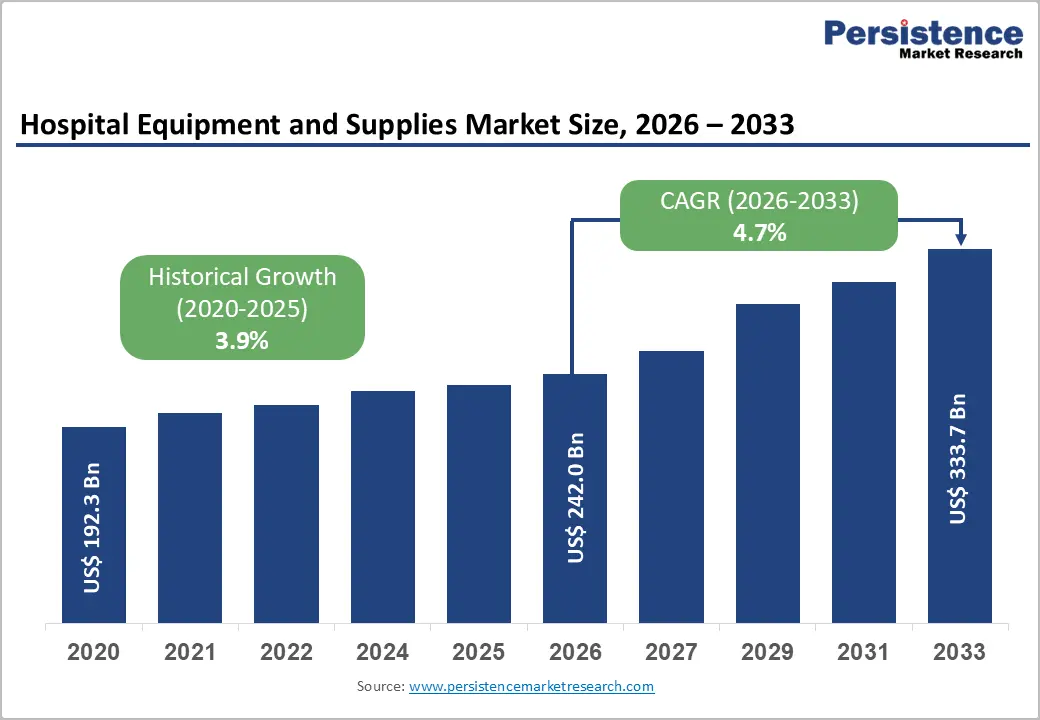

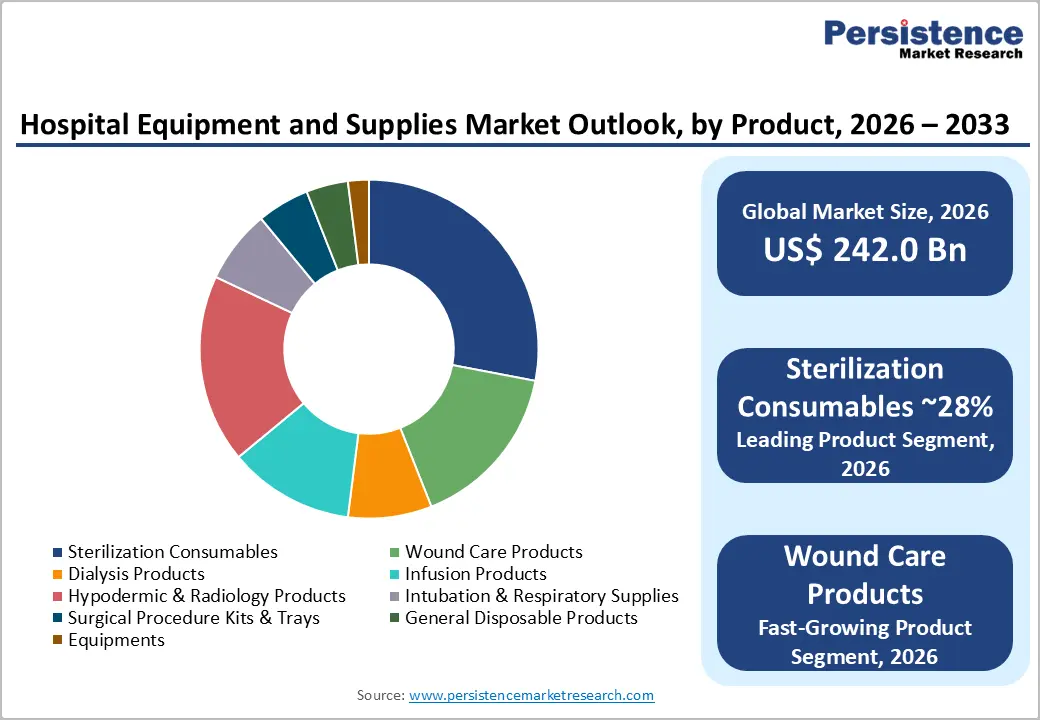

The global hospital equipment and supplies market size is expected to be valued at US$ 242.0 billion in 2026 and projected to reach US$ 333.7 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

Rise in global healthcare infrastructure investments, a rapidly aging population, and the accelerating adoption of single-use and infection-control products are the primary growth catalysts for the hospital equipment and supplies market. According to the World Health Organization (WHO), global health spending surpassed US$ 9 trillion in 2020 and continues to grow, with emerging economies significantly expanding hospital infrastructure.

The persistent burden of hospital-acquired infections (HAIs), chronic disease prevalence, and rising surgical procedure volumes are sustaining robust demand for disposable medical supplies, advanced wound care solutions, and sterilization consumables across both developed and developing healthcare systems.

Key Industry Highlights:

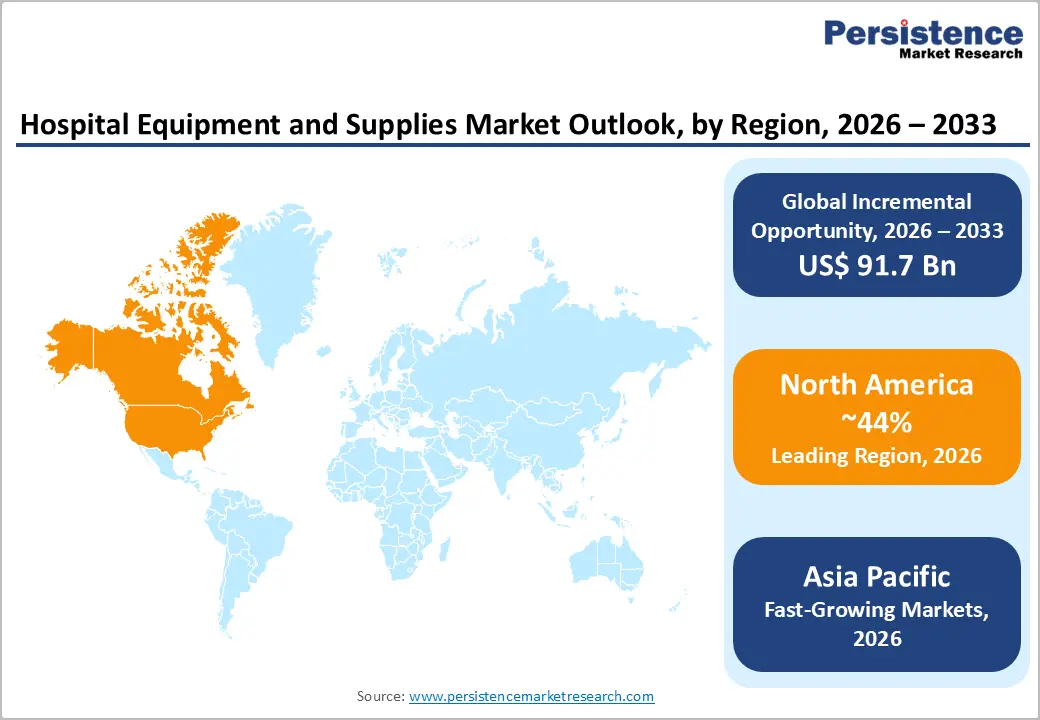

- Leading Region: North America leads with 44% share due to high healthcare spending, advanced hospital infrastructure, and strict infection control regulations.

- Fastest Growing Region: Asia Pacific is likely to reach a fast-growth, driven by expanding hospital infrastructure, rising chronic disease burden, and increasing surgical procedure volumes.

- Dominant Products: Sterilization consumables dominate with 28% share supported by mandatory sterility compliance and widespread adoption of single-use products.

- Fast-Growing Segment: Wound care products are likely to witness fast-growth due to increasing chronic wound cases, advanced wound care adoption, and strong clinical healing outcomes.

- Key Opportunity: Expanding Ambulatory Surgical Centers create major opportunities for surgical kits, sterile consumables, and infection prevention product manufacturers.

Market Dynamics

Drivers - Emergence of Smart Hospital Beds and IoT-enabled Equipment to Push Growth Amid Move toward Smooth Workflow

The hospital equipment and supplies market is experiencing rapid transformation due to developments in medical technology. Innovations such as AI-powered diagnostic tools, robotic-assisted surgeries, smart monitoring systems, and IoT-enabled hospital equipment are reshaping healthcare operations. For example, GE HealthCare Technologies reported higher-than-expected Q3 profits in 2024, augmented by increased demand for diagnostic imaging, ultrasound, and surgical equipment in the U.S.

According to the World Health Organization (WHO), the adoption of AI-driven medical devices will increase by 45% in global healthcare facilities in 2024. AI-powered diagnostic imaging and robotic surgeries reduce errors and improve efficiency, a key technological aid for the market. Smart hospital beds and automated monitoring systems enhance hospital workflow, enhancing the market's growth.

Healthcare providers are investing heavily in digital transformation, thereby increasing demand for high-tech medical supplies. As hospitals and clinics adopt these technologies, demand for novel medical equipment will continue to rise, pushing market growth forward.

Restraints - Lack of Training among Doctors and Nurses May Hinder Use of High-tech Medical Equipment

Medication errors, risks associated with medical supplies, and a shortage of skilled healthcare professionals are key challenges for the global market. These challenges can have serious consequences for patient safety and hospital efficiency. For instance, according to a report by Johns Hopkins, in 2023, incorrect labelling of medical products can lead to serious medication errors, contributing to up to 250,000 deaths annually in the U.S. alone. Medical supplies and consumables, including wound care dressings, infusion supplies, surgical tools, and diagnostic equipment, play a critical role in healthcare delivery. However, improper use, contamination, or human error can lead to serious complications, infections, or even fatal medical mistakes.

Another leading restraint on the market is the shortage of trained medical professionals, including doctors, nurses, and medical technicians. As aging populations and chronic disease cases rise, demand for skilled healthcare workers exceeds supply. For example, the World Health Organization (WHO) predicts a global shortage of 10 million healthcare workers by 2030. In 2024, the U.S. alone is set to face a shortage of 200,000+ nurses, which will likely impact hospital staffing and patient care.

Opportunities - MedTech Start-ups to Come up with Affordable Yet Intelligent Medical Equipment to Attract Clients

Significant investments to fund MedTech start-ups is expected to unveil new opportunities in the coming years. Investors are allocating billions to novel healthcare technology, bolstering innovation and transforming the future of medical equipment and hospital supplies. For example, MedTech start-ups in the U.S. and Europe secured US$ 4 billion in the first half of 2024.

Medical device IPOs and acquisitions are anticipated to rise by 25% in 2025 as several start-ups transition from development to commercialization. AI-driven healthcare solutions are garnering unprecedented investments, facilitating the entry of new competitors into the hospital equipment sector. Hospitals pursue economical, high-efficiency medical solutions to improve patient care and save operational expenses.

Start-ups focused on AI-driven diagnostics, robotic-assisted operations, and intelligent medical devices are acquiring a competitive advantage over traditional providers. With rising funding, the market is poised for a surge of groundbreaking technologies that will likely revolutionize patient care and enhance healthcare efficiency.

Category-wise Analysis

Product Insights

Sterilization consumables lead the hospital equipment and supplies market, commanding 29.8% of global market share in 2026. This dominance is rooted in the non-negotiable requirement for sterility across all surgical and clinical procedures, driving consistent high-volume procurement of single-use sterilization wraps, sterile containers, sterilization paper bags, and sterile indicator tapes. The CDC guidelines on sterilization and disinfection in healthcare facilities mandate rigorous sterilization standards, creating a permanent, regulation-driven demand floor for these products.

The COVID-19 pandemic further amplified institutional commitment to sterility assurance, leading hospitals globally to increase safety stock and standardize sterilization protocols. Leading suppliers, including Cardinal Health, 3M, and Medline Industries, have strengthened their sterilization consumables portfolios to serve this consistently high-demand segment.

End-user Insights

Hospitals constitute the dominant end-user segment for hospital equipment and supplies, representing 55% of total demand in 2025. Hospitals are the primary procurement centers for the full spectrum of medical supplies and equipment, from sterilization consumables and wound care to dialysis products and surgical kits, owing to their role as the central venue for complex inpatient procedures, emergency care, and critical care services. The American Hospital Association (AHA) reports that there are 6,120 registered hospitals in the United States alone, collectively handling hundreds of millions of patient encounters annually.

Globally, the WHO estimates there are 136,000 hospitals worldwide. This scale of institutional infrastructure underpins consistently high and diversified demand for hospital supplies across all product categories, securing hospitals' position as the market's primary demand driver.

Regional Insights

North America Hospital Equipment and Supplies Market Trends and Insights

North America leads the global hospital equipment and supplies market with 44% market share in 2025, driven by advanced healthcare infrastructure, high per-capita healthcare expenditure, stringent infection control mandates, and a robust regulatory environment administered by the FDA. The region benefits from consistently high procedural volumes, strong ASC growth, and deep penetration of advanced wound care and dialysis products across both hospital and outpatient settings.

U.S. Hospital Equipment and Supplies Market Size

The United States accounts for 85% of North America's market, reflecting its position as the world's largest healthcare economy. According to the CMS data, U.S. hospital care expenditure exceeded US$ 1.35 trillion in 2022. High surgical volumes, aging demographics, chronic disease prevalence, and mandatory sterility and infection control standards under CDC and Joint Commission guidelines sustain robust demand across all supply categories.

Europe Hospital Equipment and Supplies Market Trends and Insights

Europe represents the second-largest regional market, supported by universal healthcare systems, strong regulatory harmonization under the EU Medical Device Regulation (MDR 2017/745), and high standards of hospital infection control. Demand is particularly strong in Western Europe, where aging populations, high chronic disease burden, and government-mandated procurement standards for medical supplies drive consistent volume. The shift toward outpatient and ambulatory care settings is also accelerating demand for disposable and single-use products.

Germany Hospital Equipment and Supplies Market Size

Germany accounts for 24% of Europe's hospital equipment and supplies demand, positioning it as the region's largest national market. Germany's Gesundheitsversorgungsstärkungsgesetz healthcare reform and investment in digitalized hospital infrastructure, combined with a high rate of surgical procedures per capita, sustain robust procurement of sterilization consumables, infusion products, and surgical kits from suppliers including B.Braun SE.

UK Hospital Equipment and Supplies Market Size

The UK represents 15% of European market demand, anchored by the National Health Service (NHS) one of the world's largest public healthcare systems managing over 1.2 million patient contacts daily. The NHS's centralized procurement framework through NHS Supply Chain ensures consistent, large-volume procurement of hospital supplies, while ongoing NHS infrastructure modernization programs are supporting demand growth for advanced wound care and sterile products.

Asia Pacific Hospital Equipment and Supplies Market Trends and Insights

Asia Pacific is the fast-growing market in the global hospital equipment and supplies market, propelled by massive healthcare infrastructure expansion, rising surgical volumes, and increasing government health spending across China, India, Japan, and ASEAN nations. China leads regional demand, with the National Health Commission of China reporting over 36,000 hospitals nationwide and ongoing investment in Healthy China 2030 initiatives that prioritize hospital modernization and infection control standards. The region's cost-sensitive procurement landscape is driving strong demand for locally manufactured disposable supplies.

India Hospital Equipment and Supplies Market Size

India is among the fastest-growing individual country markets, representing 8% of Asia Pacific's hospital supply demand. The Indian government's Ayushman Bharat-Pradhan Mantri Jan Arogya Yojana (PM-JAY) scheme, covering over 500 million beneficiaries, is driving significant hospital capacity expansion, increasing procurement of disposable surgical and infection-control supplies. Rising medical tourism volumes further amplify demand for high-quality hospital equipment and supplies.

Japan Hospital Equipment and Supplies Market Size

Japan accounts for 18% of Asia Pacific's market, reflecting its mature and highly sophisticated healthcare system with over 8,200 hospitals. Japan's rapidly aging population, with 29% of its citizens aged 65 or above according to the Statistics Bureau of Japan, sustains high chronic disease treatment rates and demand for dialysis products, wound care supplies, and long-term care consumables, supporting consistent market performance despite overall population decline.

Competitive Landscape

The global hospital equipment and supplies market is moderately consolidated, with multinational players including Medtronic, Cardinal Health, Johnson & Johnson, 3M, GE Healthcare, and B.Braun SE holding significant combined market share through diversified product portfolios, extensive distribution networks, and strong institutional relationships. Market leaders differentiate through regulatory compliance capabilities, supply chain resilience, private-label programs, and integrated digital procurement solutions.

Emerging trends include the adoption of vendor-managed inventory (VMI) systems, sustainability-focused product redesigns, and strategic acquisitions of niche specialty suppliers. Mid-tier and regional players compete through cost leadership and locally tailored product offerings.

Key Developments

- In January 2025, Montagu signed a definitive agreement to acquire Tyber Medical, which offers private-label development and manufacturing services to med-tech OEMs.

- In October 2024, Mölnlycke Health Care, a global leader in wound care, announced a research collaboration with Transdiagen (TDG) to explore the use of TDG's novel wound gene signatures with Mölnlycke products.

- In August 2024, Baxter International Inc. announced a definitive agreement for Carlyle to acquire Baxter's Kidney Care segment, renamed Vantive, for US$ 3.8 Bn.

Hospital Equipment and Supplies Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 192.3 Billion |

| Current Market Value (2026) | US$ 242.0 Billion |

| Projected Market Value (2033) | US$ 333.7 Billion |

| CAGR (2026 - 2033) | 4.7% |

| Leading Region | North America, 44% market share (2025) |

| Dominant Product Category | Sterilization Consumables, 28% market share (2025) |

| Top-Ranking Application | Cardiovascular, 26% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 91.7 Billion |

Companies Covered in Hospital Equipment and Supplies Market

- Medtronic

- Cardinal Health

- 3M

- Halyard

- Medline Industries, LP.

- MCKESSON CORPORATION

- Sempermed

- GE Healthcare

- Johnson & Johnson

- ThermoFisher Scientific Inc.

- Honeywell International Inc.

- Prestige Ameritech

- Mucambo S.A. (Newell Co.)

- B.Braun SE

- Others

Frequently Asked Questions

The global market is estimated to be valued at US$ 242.0 billion in 2026.

Major growth opportunity lies in expanding ASCs, advanced wound care adoption, and increasing demand for outpatient-focused medical consumables globally.

North America leads the global market with 44% market share in 2025.

Rising chronic diseases, stricter infection control protocols, increasing hospital admissions, and expanding healthcare infrastructure significantly drive market demand globally.

Leading companies in the market include Medtronic, Cardinal Health, 3M, Johnson & Johnson, GE Healthcare, Medline Industries, LP, McKesson Corporation, Baxter International Inc., and Becton, Dickinson and Company (BD), among others.