- Transportation & Logistics

- Forklift Trucks Market

Forklift Trucks Market Size, Share, and Growth Forecast 2026 - 2033

Forklift Trucks Market by Load Capacity (Below 5 Ton, 5–15 Ton, Above 16 Ton), Technology (Electric Motor Forklift Trucks, IC Engine Forklift Trucks), Class (Class 1 Forklift Trucks, Class 2 Forklift Trucks, Class 3 Forklift Trucks, Class 4&5 Forklift Trucks), End-user (Mining, Manufacturing, Retail & Wholesale, Logistics, Construction, Automotive, Food & Beverages, Chemical), and Regional Analysis for 2026 - 2033

Forklift Trucks Market Size and Trend Analysis

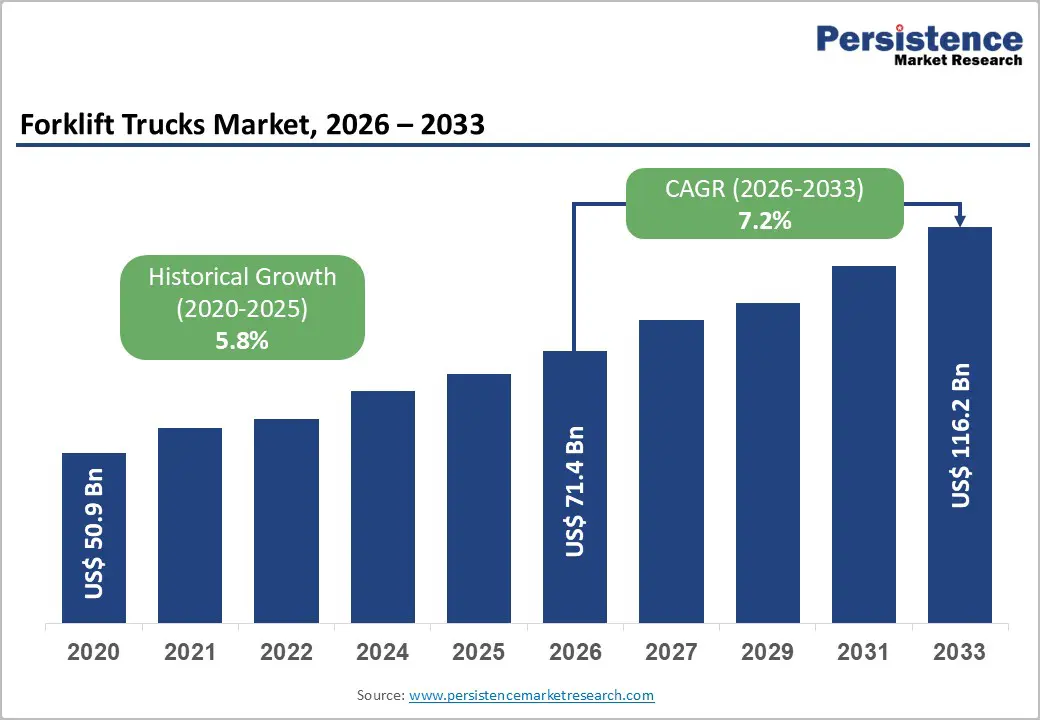

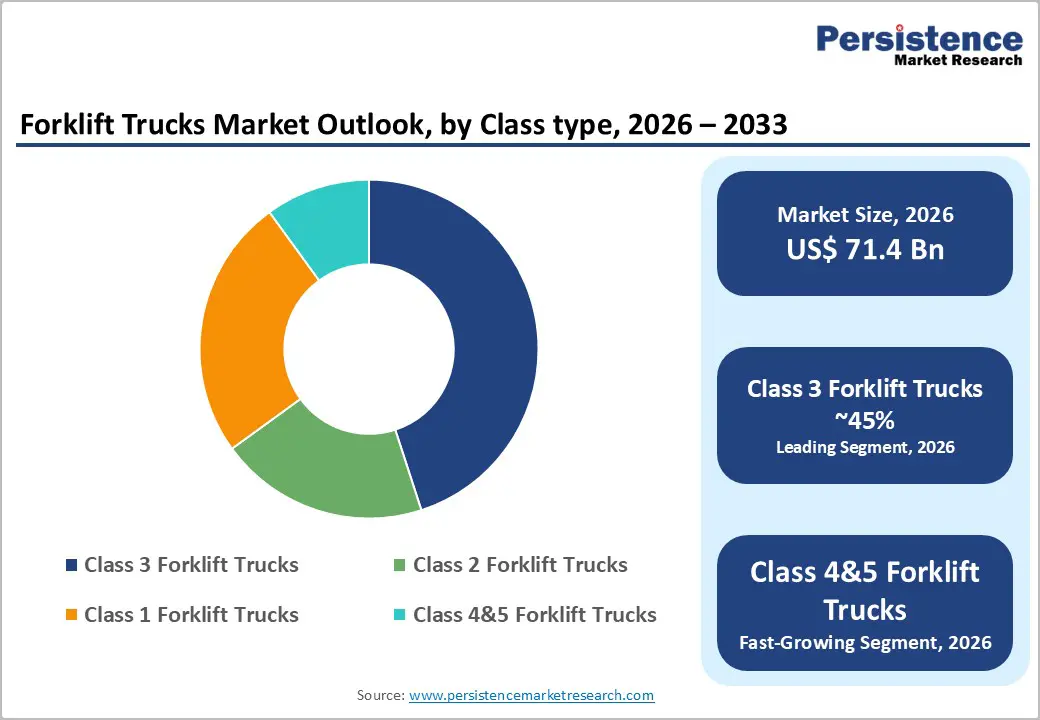

The global Forklift Trucks market is valued at US$ 71.4 billion in 2026 and is projected to reach US$ 116.2 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033. The market's sustained expansion is primarily driven by the accelerating growth of global e-commerce and warehouse automation, rising industrialization in emerging economies, and increasingly stringent emission regulations compelling fleet operators to transition from IC-engine to electric forklifts.

Key Market Highlights

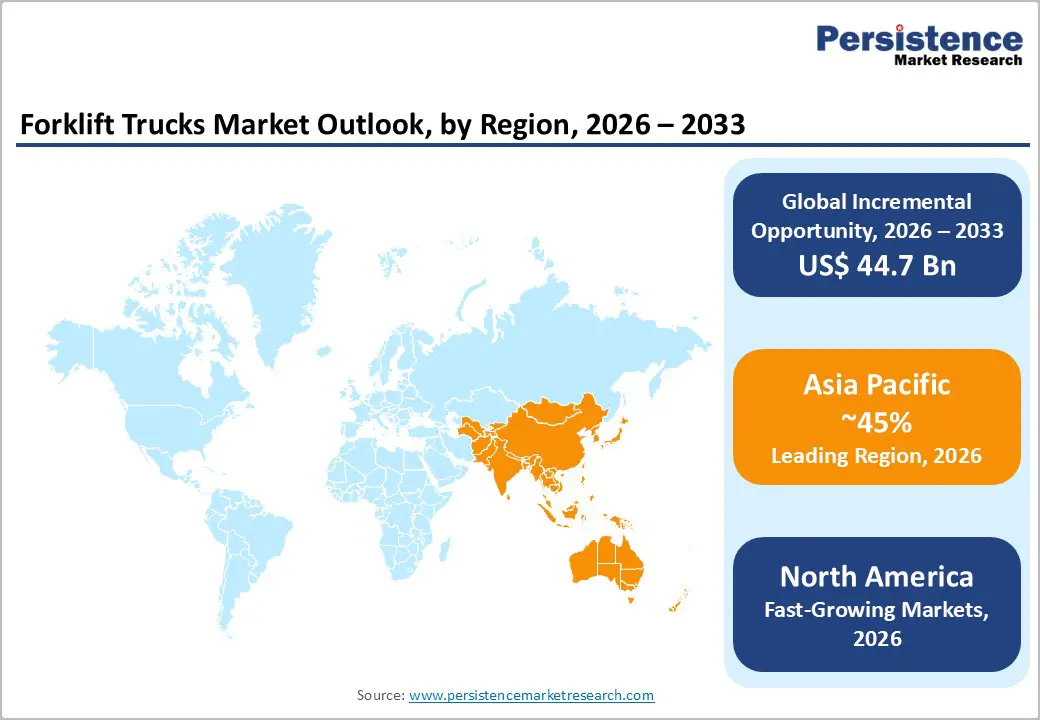

- Leading Region – Asia Pacific dominates the global Forklift Trucks Market with approximately 45% revenue share in 2025, anchored by China's massive manufacturing base and India's rapidly expanding logistics and infrastructure investment landscape.

- Fastest Growing Region – India is the fastest-growing national market, projected at approximately 18.0% CAGR through 2034, driven by infrastructure spending, manufacturing growth, and increasing adoption of electric forklifts in logistics operations.

- Dominant Segment – Electric Motor Forklift Trucks command approximately 68% of 2025 global shipments, underpinned by zero-emission mandates, lithium-ion cost reductions, and superior operational efficiency in modern warehouses.

- Fastest Growing Segment – Autonomous forklifts represent the fastest-growing technology sub-segment, projected at a CAGR of 9.3% through 2032, driven by labour shortages, AI-LiDAR navigation advances, and warehouse automation investment globally.

- Key Market Opportunity – Infrastructure investment-driven demand in India, Southeast Asia, and Latin America combined with electric and autonomous forklift adoption curves presents the most significant revenue-generating opportunity through 2033.

| Key Insights | Details |

|---|---|

|

Forklift Trucks Market Size (2026E) |

US$ 71.4 Bn |

|

Market Value Forecast (2033F) |

US$ 116.2 Bn |

|

Projected Growth CAGR (2026–2033) |

7.2% |

|

Historical Market Growth (2020–2025) |

5.8% |

Market Dynamics

Drivers - E-Commerce Boom and Warehouse Automation Driving Unprecedented Forklift Demand

The exponential growth of global e-commerce remains the single most powerful demand catalyst in the Forklift Trucks Market. According to the U.S. Census Bureau, retail e-commerce sales in the United States reached US$ 305.9 Bn in Q4 2024, a 2.7% sequential increase. The global third-party logistics (3PL) market reached US$ 1.5 trillion in 2024 and is anticipated to grow at a CAGR of 10.1% through 2034. Players such as Amazon, Walmart, and Alibaba continue expanding fulfillment centre operations. Amazon India opened three new fulfillment centres in Delhi NCR, Guwahati, and Patna in September 2024, with total storage area exceeding 1.2 million cubic feet. This warehouse densification directly translates into higher electric and automated forklift fleet adoption.

Rapid Electrification and Lithium-Ion Battery Technology Advancements

Stringent emission norms including California's Advanced Clean Fleets Rule and China's Air Pollution Prevention and Control Action Plan mandating zero-emission non-road machinery in major cities, are accelerating the displacement of IC-engine forklifts by electric alternatives. In 2025, electric units accounted for approximately 67.7% of global forklift shipments. Jungheinrich AG reports that over 90% of its trucks are now lithium-ion battery-powered. In March 2024, Jungheinrich AG introduced the EJC 1i series lithium-ion-powered warehouse trucks available in five battery capacities from 50 Ah to 200 Ah. In February 2024, KION North America launched the Linde Series 1293 electric forklift, offering lifting capacity of 4,000–5,000 lbs powered by lithium-ion batteries. Falling Li-ion costs and battery-as-a-service (BaaS) models are further accelerating fleet replacement.

Restraints - High Initial Capital Investment and Total Cost of Ownership

A critical barrier to widespread forklift adoption, particularly for electric and autonomous variants is the substantially higher upfront investment relative to conventional IC-engine models. Advanced lithium-ion electric forklifts command significant price premiums, and the capital expenditure required for supporting charging infrastructure adds further cost. For small and medium enterprises (SMEs) in cost-sensitive markets across South Asia and Sub-Saharan Africa, these barriers are prohibitive. A 2024 Jungheinrich AG survey noted that rising inquiries for autonomous solutions are frequently stalled at budget approval stages. The ancillary costs of specialized maintenance, operator training, and cybersecurity for connected fleets compound the overall cost-of-ownership challenge.

Skilled Labor Shortages and Operator Certification Challenges

The growing complexity of electric and autonomous forklift systems demands a skilled and certified operator pool that remains in short supply globally. The European Commission has identified a critical skills gap in material handling across Germany, France, and the Nordic countries, with a significant number of certified operators positions unfilled. In Norway, the required certification process involves lengthy waits owing to instructor shortages. Germany has seen a notable decline in logistics apprenticeship enrolments in recent years. These labour constraints slow fleet utilization rates, increase downtime, and raise operational costs, dampening the pace of market expansion, particularly for high-throughput warehouse operators.

Opportunity - Autonomous and AI-Integrated Forklift Adoption in Logistics and Warehousing

The convergence of artificial intelligence, LiDAR, cameras, and real-time IoT data processing is creating a compelling growth opportunity in autonomous forklift solutions. The global autonomous forklift market was valued at US$ 2.73 Bn in 2025 and is projected to reach US$ 5.07 Bn by 2032, growing at a CAGR of 9.3%. In March 2025, Toyota Material Handling launched its self-driving electric reach truck in the United States. In January 2025, KION Group partnered with NVIDIA and Accenture at CES 2025 to showcase a Physical AI-powered digital twin warehouse. Hyundai Motor Group reduced order processing times by 22% in 2025 after integrating AI-based forklifts into its Uiwang smart logistics hub illustrating the transformative efficiency gains that autonomous forklift adoption can deliver at scale.

Infrastructure Spending and Industrialization in Emerging Economies

Rapidly expanding infrastructure investment and industrial capacity buildup in emerging economies represent a sizeable, underserved opportunity for forklift manufacturers. Infrastructure spending in India is projected to grow at a CAGR of 9.3% through 2030, fueling robust demand for heavy-capacity construction-grade forklifts. China's forklift production volume is projected to reach 66,170 units by 2026, reflecting sustained manufacturing output growth. U.S. construction spending reached US$ 2.19 trillion in December 2024, a 4.3% annual increase, supporting demand for above-5-ton capacity forklifts in construction and manufacturing contexts. As Southeast Asia, Latin America, and Middle East and Africa attract foreign direct investment and build out logistics parks and special economic zones, new fleet procurement cycles present significant revenue opportunities for the Forklift Trucks Market.

Category-wise Analysis

Load Capacity Insights

Among load capacity segments, the 5–15 Ton bracket commands the leading market share, accounting for approximately 41% of global revenues. This segment's dominance reflects its optimal versatility these mid-range forklifts are suitable for both indoor and outdoor environments and can be powered by liquefied petroleum gas, natural gas, or electricity, making them the most deployed class across manufacturing, ports, and medium-scale logistics operations. They handle heavy pallets, steel coils, and bricks with precision and speed, bridging the operational gap between light-duty warehouse trucks and specialized heavy-lift equipment. Their compatibility with a wide range of attachments including rotators, fork positioners, and clamps further extends their applicability across automotive, construction, and food and beverage end-user verticals, reinforcing the segment's leadership position.

Technology Analysis

The Electric Motor Forklift Trucks segment has emerged as the dominant technology category, representing approximately 68% of global shipments in 2025. This supremacy is driven by zero-emission mandates, the falling cost of lithium-ion battery packs, and the operational advantages of electric drivetrains in enclosed warehouse environments including lower noise, reduced maintenance, and superior torque consistency. California's Advanced Clean Fleets Rule, China's non-road emission standards, and the European Union's industrial emissions directives are each compelling large fleet operators to accelerate their transition from IC-engine models. The battery-as-a-service (BaaS) financing model is further reducing the upfront cost barrier for electric adoption, reinforcing the segment's dominant and expanding position through the forecast horizon.

Class Insights

Within the vehicle class segmentation, Class 3 Forklift Trucks (electric motorized hand trucks and walkie pallet trucks) hold the leading market share at approximately 45% of 2025 volumes. These hand-controlled, tiller-operated forklifts are pervasive in high-turnover dock operations, retail distribution centres, and food and beverage warehouses due to their compact footprint, ease of manoeuvrability, and low operating cost. They are purpose-built for floor-level transfers and low-raise applications tasks that dominate order-picking workflows in modern omnichannel fulfillment environments. Class 1 (electric rider trucks) are positioned as the fastest-growing class at a CAGR of 4.25%, gaining traction as warehouses pursue ventilation-free, high-throughput operations in tandem with autonomous guided vehicle (AGV) integration strategies.

End-user Insights

The logistics segment is the dominant end-user category, commanding approximately 38% of global forklift demand in 2025. The segment's leadership is underpinned by the relentless expansion of e-commerce fulfillment, third-party logistics (3PL) networks, and last-mile delivery infrastructure. In North America, logistics dominates with a 36% market share in 2024 and is projected to grow at a CAGR exceeding 8% through 2034. As fulfillment centres push for narrower aisles, taller racking systems, and 24/7 operational uptime, the demand for electric Class I–III forklifts purpose-built for automated warehouse environments continues to intensify.

Regional Insights

North America Forklift Trucks Market Trends

North America is a leading revenue-generating region for the global Forklift Trucks Market, with the United States accounting for approximately 40% of world forklift sales in 2024. U.S. forklift revenues reached approximately US$ 9.9 Bn in 2024, driven by robust construction expenditure which hit US$ 2.19 trillion and a highly active e-commerce and 3PL sector. Toyota Material Handling broke ground in May 2024 on a 295,000-square-foot electric lift truck manufacturing facility near Columbus, Indiana, representing a US$ 100 million investment, highlighting the region's strategic importance.

From a regulatory perspective, California's Advanced Clean Fleets Rule is a pivotal policy accelerating fleet electrification. Logistics operators are responding by procuring compact Class I–III electric forklifts designed for automated fulfillment environments. Crown Equipment Corporation recently launched the Proximity Assist System, using LiDAR sensing for operator-assist safety.

Europe Forklift Trucks Market Trends

Europe is a high maturity yet actively innovating market, with key demand hubs in Germany, the United Kingdom, France, and Spain. The European forklift market was estimated at US$ 18.2 Bn in 2024, growing at a projected CAGR of 6.3% through 2034. Jungheinrich AG allocated over EUR 100 million for R&D in FY2023–2024, focusing on lithium-ion battery technology and autonomous forklifts. KION Group AG reported consolidated revenues of EUR 11.5 Bn in 2024, with adjusted EBIT rising to EUR 917 million.

Regulatory harmonization under the EU Sustainable Products Regulation and the European Green Deal is compelling manufacturers to invest in hydrogen fuel cell and battery-electric solutions. KION Group has been producing 24-volt fuel cell systems for warehouse trucks since 2023 and is developing state-funded hydrogen refuelling infrastructure.

Asia Pacific Forklift Trucks Market Trends

Asia Pacific is the dominant regional market for forklift trucks, holding approximately 45% of global revenues in 2025. China drives much of this share through its vast manufacturing and export-oriented logistics base, with domestic forklift production projected at approximately 63,020 units in 2025. China's Ministry of Ecology and Environment mandates zero-emission non-road machines in key cities under its Air Pollution Prevention and Control Action Plan, strongly driving electrification.

In Japan, Toyota Industries Corporation launched a new line of AI-powered forklifts in 2024 targeting aging logistics facilities, responding to acute labour shortages. Japan's Ministry of Economy is advancing robotic material-handling technologies through industrial digitalization programs. ASEAN markets including Vietnam, Thailand, and Indonesia are emerging as high-growth demand zones as global manufacturers near-shore production from China.

Competitive Landscape

The global forklift trucks market is moderately consolidated, with the top five players Toyota Industries Corporation, KION Group AG, Jungheinrich AG, Mitsubishi Logis next Co., Ltd., and Crown Equipment Corporation holding approximately 50% of global market share. Key differentiators include lithium-ion ecosystem integration, proprietary warehouse management system (WMS) connectivity, autonomous navigation capabilities, and aftermarket service networks. Emerging business model trends encompass fleet-as-a-service (FaaS), battery-as-a-service (BaaS), and AI-driven predictive maintenance platforms.

Key Market Developments

- In November 2025, Noblelift conducted a product launch event targeting the Asian market, unveiling several new offerings, including a 10-ton lithium model forklift, new Automated Guided Vehicle Systems (AGVS), reach trucks, and Mobile Elevating Work Platforms (MEWPs). The company introduced it’s A Series forklift, its first dual-power option model, which supports both lithium-ion and diesel/LPG systems.

- In April 2025, At Bauma 2025, PALFINGER AG showcased its new center-seat truck-mounted forklift, featuring modular components, emphasizing improved ergonomics and visibility. This innovation showcases PALFINGER's dedication to enhancing material handling solutions by prioritizing operator comfort and operational efficiency.

Companies Covered in Forklift Trucks Market

- Sumitomo Heavy Industries, Ltd.

- Toyota Material Handling

- BYD

- Manitou Group

- Kalmar (Cargotec Finland Oy)

- V. Mariotti S.r.l.

- Doosan Corporation (Industrial Vehicle)

- MiMA forklift

- AUSA

- Mitsubishi Nichiyu Forklift Co., Ltd.

- Crown Equipment Corporation

- Anhui HeLi Co., Ltd.

- CLARK Material Handling Co., Ltd.

- Kion Group AG

- Jungheinrich AG

- Other Key players

Frequently Asked Questions

The global Forklift Trucks Market, valued at US$ 71.4 Bn in 2026, is projected to reach US$ 116.2 Bn by 2033, growing at a CAGR of 7.2% during the forecast period.

The key demand drivers include the global e-commerce boom with the U.S. e-commerce reaching US$ 305.9 Bn in Q4 2024the rapid electrification of forklift fleets driven by emission mandates, advancements in lithium-ion battery technology, and rising warehouse automation adoption across logistics, manufacturing, and retail end-users globally.

The Electric Motor Forklift Trucks segment leads the technology category with approximately 68% of global shipments in 2025. Growth is driven by zero-emission mandates such as California's Advanced Clean Fleets Rule, declining lithium-ion battery costs, and operational advantages in enclosed warehouse settings including lower maintenance, reduced noise, and compatibility with autonomous guided vehicle (AGV) systems.

Asia Pacific leads the global Forklift Trucks Market with approximately 45–47% revenue share in 2025. China's vast manufacturing and export-oriented logistics infrastructure anchors the region's dominance, while India's rapidly expanding construction, logistics, and manufacturing sectors make it the fastest-growing individual national market at a projected CAGR of ~18.0% through 2034.

Leading companies include Toyota Material Handling, KION Group AG, Jungheinrich AG, Crown Equipment Corporation, Mitsubishi Nichiyu Forklift Co., Ltd., Anhui HeLi Co., Ltd., CLARK Material Handling Co., Ltd., Doosan Corporation (Industrial Vehicle), Manitou Group, and Kalmar (Cargotec Finland Oy). The top five players collectively hold approximately 55–60% of global market revenues.