- Automotive

- Heavy Trucks Market

Heavy Trucks Market Size, Share, and Growth Forecast, 2026-2033

Heavy Trucks Market by Truck Type (Tractor-Trailers, Rigid Trucks, Dump Trucks, Tanker Trucks, Refrigerated Trucks, Flatbed Trucks, Others), Powertrain (Diesel ICE, CNG/LNG, Hybrid Electric, Battery Electric, Hydrogen Fuel Cell, Renewable Fuels), Application (Long-Haul Freight Logistics, Regional Urban Freight Transport, Construction Mining Operations, E-Commerce, Municipal Services, Agriculture Off-Highway Applications), and Regional Analysis for 2026-2033

Heavy Trucks Market Share and Trends Analysis

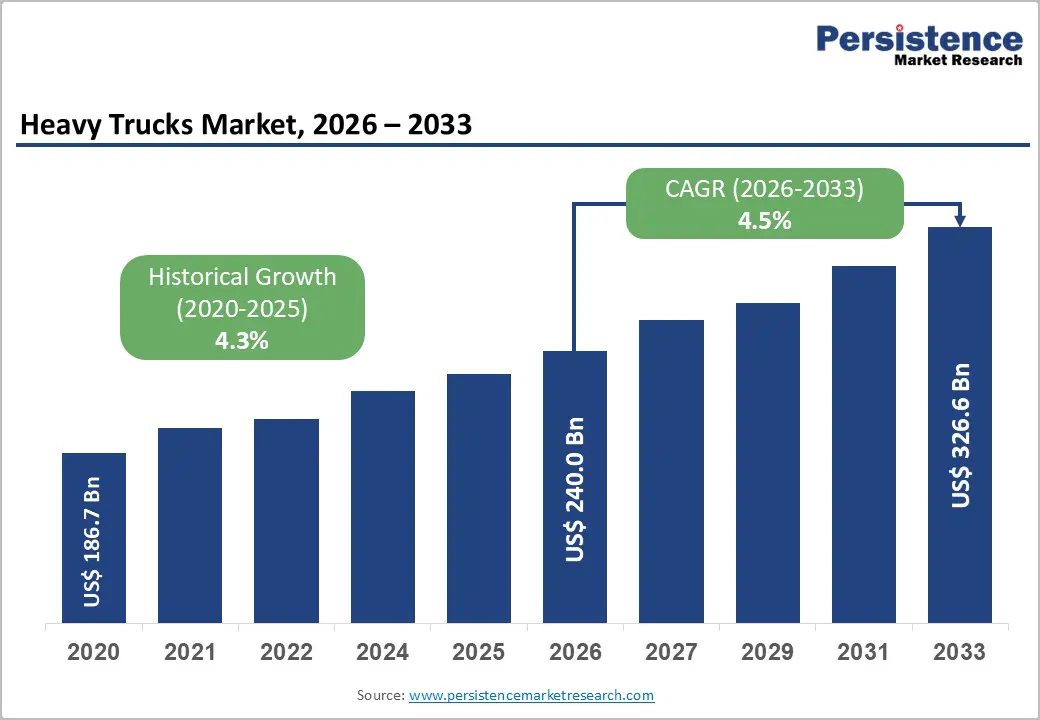

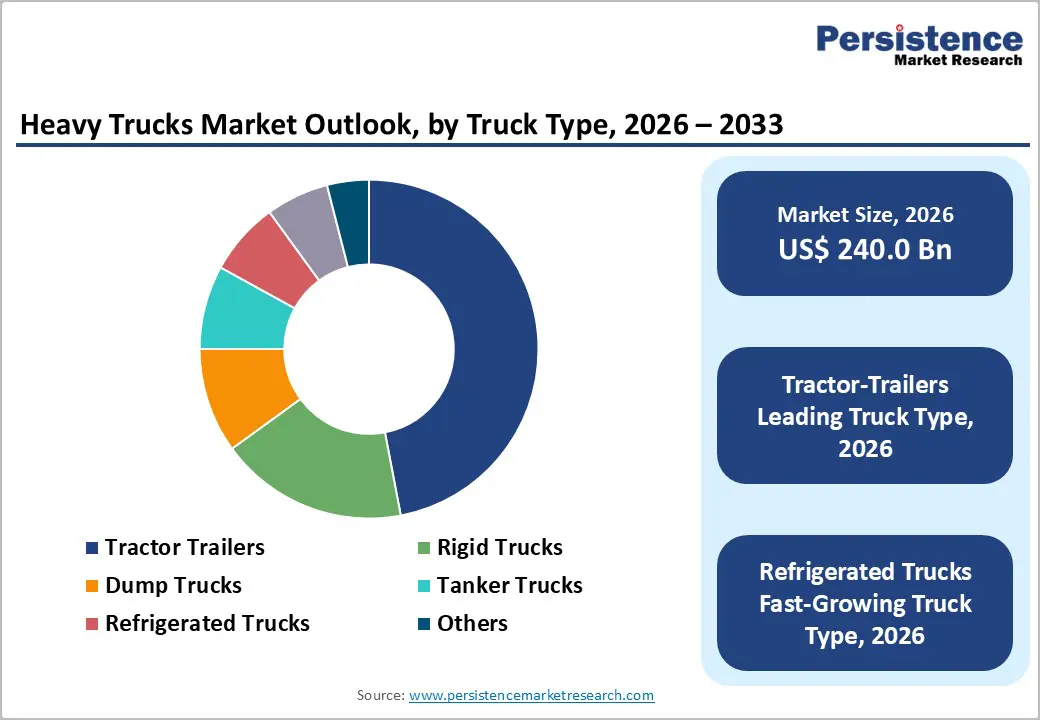

The global heavy trucks market size is likely to be valued at US$ 240.0 billion in 2026, and is projected to reach US$ 326.6 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026–2033.

Demand is soaring as freight volumes are increasing across domestic and cross-border trade corridors. Industrial output and infrastructure construction are sustaining transportation requirements in both advanced and emerging economies. Governments are investing in highways, logistics parks, and multimodal freight networks, which is strengthening demand for high-capacity vehicles. Regulatory authorities are enforcing stricter vehicle safety and emission standards, which is accelerating fleet renewal programs. As older trucks are being phased out to comply with updated norms, manufacturers are benefiting from replacement-driven sales. E-commerce expansion is increasing the need for reliable long-haul and regional transport solutions, reinforcing the role of heavy-duty trucks within supply chains. Technological evolution is reshaping product development and competitive positioning. Manufacturers are advancing powertrain electrification, natural gas variants, and alternative fuel systems while continuing to optimize internal combustion engine platforms. Diesel technology is maintaining near-term dominance due to infrastructure readiness and cost efficiency, yet electric and hybrid heavy trucks are gradually gaining commercial traction in urban and short-haul routes. Logistics companies are integrating telematics, route optimization software, and fleet management systems to enhance operational efficiency and reduce total cost of ownership. These digital solutions are improving asset utilization and predictive maintenance planning.

Key Industry Highlights

- Dominant Truck Type: Tractor-trailers are projected to lead with 47% revenue share in 2026, driven by long-haul freight dominance, while refrigerated trucks are expected to grow the fastest at roughly 6.2% CAGR through 2033 due to cold-chain expansion.

- Powertrain Leadership: Diesel trucks are anticipated to retain leadership with nearly 75% in 2026, supported by infrastructure maturity, whereas battery-electric trucks are forecast to be the fastest-growing at about 18.5% CAGR through 2033, led by decarbonization mandates.

- Application Dynamics: Long-haul freight logistics is expected to dominate with around 43% share in 2026, reflecting its role in national and cross-border trade, while e-commerce logistics is projected to expand at about 7.8% CAGR, driven by omnichannel fulfillment growth.

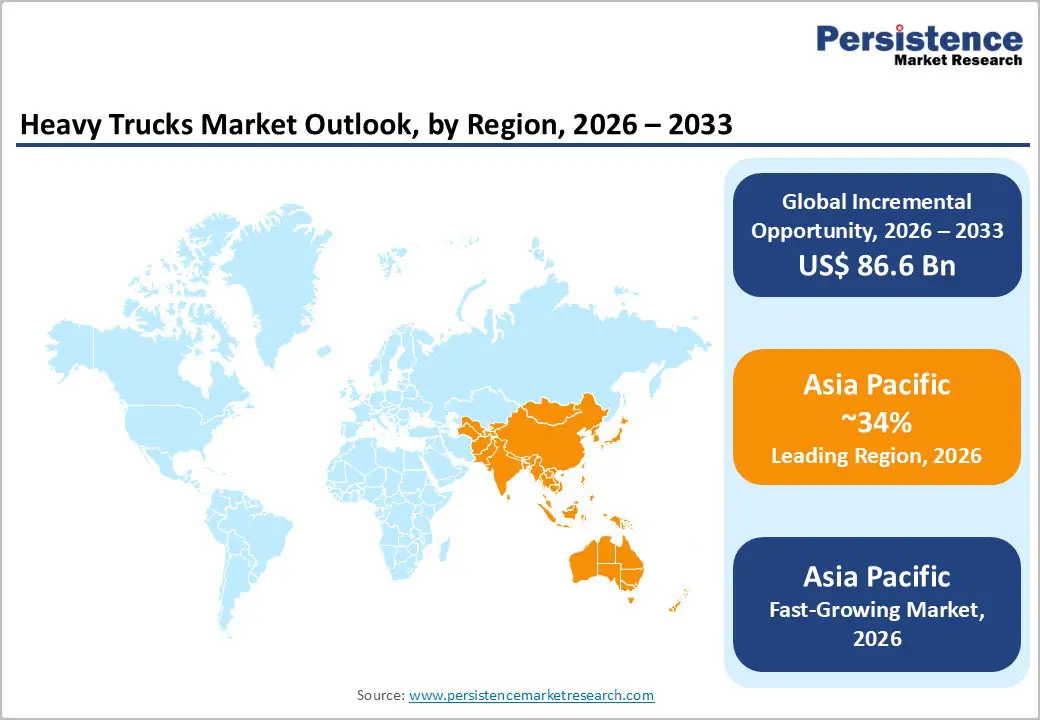

- Regional Leadership: Asia Pacific is estimated to account for 34% of demand in 2026 and register the fastest regional growth at around 6.1% CAGR during 2026–2033, supported by increasing infrastructure spending and manufacturing scale.

- Regulatory & Competitive Environment: Regulatory-driven fleet modernization is accelerating replacement demand, with stricter emission and safety standards pushing original equipment manufacturers (OEMs) toward electrification, platform upgrades, and capacity expansion.

| Key Insights | Details |

|---|---|

| Heavy Trucks Market Size (2026E) | US$ 240.0 Bn |

| Market Value Forecast (2033F) | US$ 326.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Structural Growth in Freight, Infrastructure, and Regulatory-Driven Fleet Renewal

The demand for heavy trucks continues to rise alongside expanding industrial activity, urbanization, and cross-border trade flows. Data from the World Trade Organization (WTO) indicates that merchandise trade volumes rebounded strongly after the pandemic and are expected to grow steadily over the coming decade. Heavy trucks remain the backbone of inland freight transport, particularly for routes exceeding 250 kilometers. In the United States, the American Trucking Associations (ATA) reports that trucks move over 70% of domestic freight by value. This sustained freight intensity directly reinforces demand for tractor-trailers and rigid heavy trucks. As a result, fleet operators are maintaining long-term procurement and replacement cycles to support rising freight volumes.

Large-scale infrastructure development and regulatory mandates are accelerating fleet utilization and renewal. Government-led investment programs such as the U.S. Infrastructure Investment and Jobs Act, the European Union (EU)’s Connecting Europe Facility, and major urban development projects across India and Southeast Asia are driving demand for dump trucks, tanker trucks, and flatbed trucks. The World Bank estimates infrastructure investment requirements exceed US$ 3 trillion annually through 2030, supporting higher equipment usage across construction and mining activities. In parallel, stricter emissions, safety, and fuel-efficiency regulations enforced by agencies such as the U.S. Environmental Protection Agency (EPA), the European Commission (EC), and China’s environmental authorities are shortening vehicle replacement cycles. These infrastructure spending and regulatory compliance are creating a stable, long-term demand base for modern heavy truck fleets.

Structural Barriers from Cost Pressures, Regulatory Complexity, and Operational Constraints

Heavy truck adoption continues to face structural headwinds driven by high capital intensity, operating cost uncertainty, and compliance complexity. Substantial upfront vehicle costs, often exceeding US$ 120,000 per unit, combined with elevated interest rates, limit purchasing flexibility for fleet operators, particularly small and mid-sized players. Tightening emissions and safety regulations further increase engineering requirements, certification timelines, and maintenance obligations. For instance, the phased implementation of stricter emission standards in the U.S. and Europe has compelled fleet owners to retire older vehicles earlier than planned, raising replacement costs and straining capital budgets. Fuel price volatility adds another layer of uncertainty to operating economics and contract pricing.

Operational challenges further constrain market momentum across multiple applications. Supply-chain disruptions affecting semiconductors, electronic control units, and advanced driver-assistance systems continue to extend vehicle lead times and disrupt production schedules. As an example, delivery delays for electronically controlled braking and safety systems have postponed fleet replacement programs for logistics operators, forcing extended use of aging vehicles. Limited charging and alternative-fuel infrastructure also restricts the scalable deployment of electric and hydrogen heavy trucks, particularly on long-haul routes. In parallel, persistent shortages of qualified drivers reduce fleet utilization and raise labor costs. Thus, these factors reinforce cautious procurement behavior and dampen near-term capacity expansion.

Electrification, Infrastructure Expansion, and Digitalization Unlocking New Growth Avenues

Decarbonization initiatives in urban freight corridors are creating a significant opportunity for battery electric and hydrogen fuel cell heavy trucks. Urban low-emission zones and procurement mandates are accelerating adoption among municipal fleets and last-mile logistics operators. According to the International Energy Agency (IEA), zero-emission trucks are projected to account for a meaningful share of new urban freight registrations by 2030 in Europe and China. These policy-driven shifts are reshaping fleet strategies in densely populated cities, favoring quieter, low-emission vehicles. Municipal and regional logistics operators are increasingly prioritizing zero-emission platforms. This combination of regulation and urban demand is generating a multi-billion-dollar opportunity for alternative powertrain heavy trucks.

The transport infrastructure expansion and digitalization are reinforcing demand across underpenetrated markets. Recent analyses indicate that Asia-Pacific requires approximately US$ 2.7 trillion per year between 2020 and 2035 for transport infrastructure, covering construction, maintenance, and modernization, which directly drives demand for heavy-duty trucks in agriculture, mining, and inter-city freight. The integration of telematics, predictive maintenance, and fleet analytics is enhancing fleet efficiency and lowering operating costs. OEM-embedded digital platforms and connected solutions enable data-driven procurement and maintenance planning. These large-scale infrastructure investment and connected truck adoption together creates recurring revenue streams while strengthening the long-term value proposition for fleet operators and manufacturers alike.

Category-wise Analysis

Truck Type Insights

Tractor-trailers are estimated to capture 47% of the heavy trucks market revenue share in 2026, due to their pivotal role in long-haul freight and cross-border logistics. Their high payload capacity, flexible cargo handling, and extended duty cycles continue to make them preferred for large fleets. Industry trends indicate that new launches, such as the Mack Pioneer™ Class 8 introduced in 2025, reinforce OEM focus on premium tractor platforms that improve fuel efficiency, cab comfort, and long-distance performance. These developments suggest sustained adoption in regions with high freight density and mature logistics networks. Fleet planners are likely to continue prioritizing tractor-trailers for operational reliability and total cost efficiency.

Refrigerated trucks are projected as the fastest-growing truck type, with an estimated CAGR of 6.2% through 2033, reflecting rising demand for cold-chain logistics across pharmaceuticals, perishable food, and e-commerce grocery segments. Illustrative deployments, such as DHL’s planned delivery of Mercedes-Benz eActros 600 electric trucks between 2025 and 2026 for temperature-sensitive freight, underscore the growing focus on urban and regional refrigerated transport. Increasing regulatory pressure on food safety and the expansion of last-mile delivery networks are expected to drive adoption. Technological integration, including IoT-enabled temperature monitoring, may further enhance operational efficiency.

Powertrain Insights

Diesel internal combustion engine (ICE) trucks are projected to maintain dominance in 2026 with an estimated 75% revenue share in 2026, supported by established fueling infrastructure, long operational range, and lower upfront cost. Diesel remains the default choice for long-haul and heavy payload applications, particularly in regions with limited electric or alternative fuel networks. Ongoing upgrades to engine efficiency and emissions compliance suggest diesel’s leadership is likely to persist through the forecast period. Operators continue to value predictability in maintenance, repair cycles, and overall lifecycle costs, reinforcing adoption in both emerging and mature markets.

Battery-electric trucks are expected to be the fastest-growing powertrain segment, likely to register a 2026-2033 CAGR of 18.5%, driven by urban emission restrictions, declining battery costs, and subsidy programs. Illustrative industry activity includes Mack Trucks announcing plans for a battery-electric Pioneer™ in 2025, and the launch of Montra’s Rhino 5538 EV tractor-trailer in India the same year. These examples indicate an increasing shift toward electrification, particularly for regional and municipal applications with predictable routes. Growth is likely to be concentrated in fleets seeking low-emission compliance, operational efficiency, and energy cost reduction.

Application Insights

Long-haul freight logistics is likely to dominate with approximately 43% of the heavy trucks market shar in 2026. This dominance is reflecting sustained industrial production, intercity goods movement, and expanding national distribution networks. Manufacturers are improving fuel efficiency, aerodynamic design, cab ergonomics, and drivetrain durability to strengthen fleet economics. Operators are prioritizing vehicles that enhance uptime and reduce maintenance intervals, as long-haul routes demand consistent performance over extended distances. New truck platforms are incorporating advanced driver assistance systems and telematics integration to improve safety and route optimization. These product upgrades are reinforcing confidence in total cost of ownership calculations among fleet managers. Stable freight demand across manufacturing, agriculture, and construction sectors is supporting continued volume deployment in this segment.

E-commerce logistics is poised to be the fastest-growing application, expanding at an estimated CAGR of 7.8% through 2033. Rapid urban fulfillment expansion, omni-channel retail growth, and rising consumer expectations for shorter delivery windows are driving this acceleration. Logistics providers are investing in battery-electric heavy trucks to serve regional distribution hubs and last-mile consolidation centers. DHL has deployed Mercedes-Benz eActros 600 battery-electric trucks, and Jawaharlal Nehru Port Authority (JNPA) in India is implementing battery-swappable heavy electric vehicle (EV) fleets to support intermodal transport. These deployments are demonstrating the commercial viability of electric platforms in structured logistics networks. Fleet operators are integrating telematics systems to optimize routing, energy consumption, and asset utilization. Urban regulatory frameworks are encouraging low-emission transport solutions, which is further accelerating electrification adoption.

Regional Insights

North America Heavy Trucks Market Trends

North America is anticipated to remain a critical regional market for heavy trucks, led by the United States due to its mature freight corridors, extensive highway infrastructure, and dense logistics networks. Replacement demand is continuing to support unit sales as fleets modernize aging Class 8 vehicles to comply with updated safety and emission requirements. Investment in vehicle technology is strengthening operational efficiency across long-haul and regional distribution segments. In early 2026, autonomous freight company Gatik secured approximately US$ 600 million in contracted revenue and began operating fully driverless trucks on commercial routes in Texas, signaling a transition from controlled pilots to revenue-generating autonomous deployment. Fleet operators are evaluating automation to increase delivery frequency, minimize labor constraints, and improve schedule predictability. This transition is indicating gradual commercialization of autonomous systems within structured freight corridors.

Although freight volumes have experienced short-term volatility, OEMs are projecting stabilization and moderate growth in heavy-duty segments driven by ongoing fleet renewal. Operators are balancing diesel platform reliability with pilot programs in battery-electric and hybrid configurations to manage total operating cost structures. Capital expenditure is increasingly targeting telematics integration, predictive maintenance systems, and digital fleet management platforms to improve asset utilization and reduce downtime. Public policy direction, infrastructure upgrades, and regulatory incentives are supporting modernization across interstate transport networks. Further investments in alternative powertrains and automation technologies are expected to enhance operational resilience and strengthened North America’s role as a leader in technology-enabled freight transportation.

Europe Heavy Trucks Market Trends

Europe is slated to maintain its position as a key market for heavy trucks through 2033, driven by Germany, the U.K., France, and Spain, with increasing focus on cross-border freight efficiency and regulatory compliance. Regional leadership was highlighted, when Volvo Trucks reported a 19% market share in Europe, supported by strong demand for advanced heavy truck models such as the Volvo FH Aero, featuring improved fuel efficiency and integrated digital technologies. This demonstrates the shift toward optimized long-distance and regional freight solutions, alongside stricter environmental and emissions regulations. Operators are prioritizing efficiency, uptime, and fleet modernization to meet regulatory requirements while sustaining competitiveness.

Momentum is also building around hydrogen and alternative fuels, with OEMs and energy partners collaborating on innovative fuel supply chains. For example, Daimler Truck partnered to develop subcooled liquid hydrogen (sLH2) refueling technology, planning to support early hydrogen heavy truck production starting in 2026 to expand zero-emission freight capacity across European corridors. European market growth is likely to follow a dual trajectory: conventional fleets focused on operational efficiency complemented by strategic deployment of zero-emission trucks in urban and intercity logistics. Policy support, infrastructure investment, and fleet electrification initiatives are expected to shape medium-term adoption trends.

Asia Pacific Heavy Trucks Market Trends

Asia Pacific is expected to be the leading and fastest-growing regional market for heavy trucks, holding an estimated 34% share in 2026 and posting an approximate CAGR of 6.1% during the 2026-2033 forecast period. The market here is primarily driven by industrial expansion, government-led fleet modernization, and rapid freight growth across China, India, Japan, and ASEAN economies. China continues to dominate regional production and adoption, while India demonstrates strong growth in construction, agricultural, and regional freight applications. Manufacturing cost advantages, urbanization, and rising domestic consumption underpin demand for heavy trucks. Fleet renewal programs and government incentives for electrified trucks are accelerating the shift toward low-emission and zero-emission fleets. OEMs are increasingly investing in local assembly and alternative powertrain technologies to capture market potential.

Illustrative of the rapid electrification trend, China registered 45,300 fully and partially electrified heavy-duty trucks, accounting for 54% of all heavy-duty truck sales in that month marking the first time electric trucks outsold diesel vehicles in the country. This milestone highlights both the accelerating adoption of battery-electric and hybrid trucks in commercial fleets and the effectiveness of policy incentives for fleet modernization. Regional infrastructure development, domestic manufacturing policies, and rising logistics demand are expected to sustain high adoption rates. Markets across India and ASEAN countries are poised to follow China’s lead, further reinforcing Asia Pacific as the primary growth engine for heavy trucks over the forecast period.

Competitive Landscape

The global heavy trucks market structure is moderately consolidated, with Daimler Truck, Volvo Trucks, PACCAR, Navistar, and MAN controlling a significant portion of global revenue. These established players leverage extensive dealer networks, long-standing fleet relationships, and expertise in regulatory compliance and emissions standards. They invest heavily in R&D and technology, focusing on advanced powertrains, telematics, autonomous driving systems, and electrification solutions to maintain a competitive edge. Integration of digital fleet management platforms and connected truck solutions is increasingly central to maintaining fleet loyalty and operational efficiency.

At the same time, regional and niche manufacturers such as Foton, Montra Electric, and Ashok Leyland are targeting specialized segments and emerging markets. Barriers including high capital investment, stringent safety and emissions regulations, and complex supply chains limit new entrants. However, trends in electrification, battery technology, and telematics are enabling software-focused and EV startups to participate via fleet-as-a-service models, partnerships, and localized production. Market consolidation is expected to gradually increase as leading OEMs acquire or collaborate with smaller players to expand geographically and technologically, particularly in electric and alternative powertrain development.

Key Industry Developments

- In January 2026, Kodiak AI scaled its autonomous trucking operations through a strategic partnership with Bosch, supplying automotive-grade sensors, steering systems, and vehicle control units to support production-ready autonomous hardware. This partnership positions the company to deploy driverless heavy trucks on U.S. highways at a commercial scale in 2026, transitioning from pilot programs to full operational operations.

- In October 2025, Toyota and Daimler Truck announced the formation of ARCHION Corporation, merging Hino Motors and Mitsubishi Fuso under a US$ 6.4 billion deal. The merger aims to strengthen CASE technologies (Connected, Autonomous, Shared, Electric), with a heavy focus on hydrogen fuel cell development. Operational synergies include consolidating five production sites into three by 2028 to enhance efficiency and global competitiveness.

- In September 2025, JNPA launched India’s first battery-swappable heavy truck fleet, initially deploying 50 trucks at the Nhava Sheva terminal, with plans to expand to 80 trucks by the end of 2025. Trucks feature 7-minute battery swaps, drastically reducing downtime compared to standard charging. Partners include Energy in Motion and Blue Energy Motors, under an “Energy as a Service” model.

Companies Covered in Heavy Trucks Market

- Daimler Truck AG

- Volvo Group

- Traton Group

- PACCAR Inc.

- Tata Motors

- Dongfeng Motor Corporation

- FAW Group

- Isuzu Motors

- Hino Motors

- Iveco Group

- Ashok Leyland

- Hyundai Motor Company

Frequently Asked Questions

The global heavy trucks market is projected to reach US$ 240.0 billion in 2026.

Rising freight demand, infrastructure development, fleet modernization, and adoption of alternative powertrains are key growth drivers.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Electrification of fleets, digital fleet management, and expansion in emerging logistics markets present major opportunities.

Daimler Truck, Volvo Trucks, PACCAR, Navistar, and MAN are some of the key players in the market.