- Renewable Energy

- Hydrogen Electrolyzer Market

Hydrogen Electrolyzer Market Size, Share, and Growth Forecast, 2025 - 2032

Hydrogen Electrolyzer Market By Technology (Alkaline Electrolyzer, Others), Power Rating (Below 500 kW, 500 kW - 2 MW, 2 MW - 10 MW, Others), End-user Industry (Energy & Utilities, Chemical & Petrochemical, Others), and Regional Analysis for 2025 - 2032

Hydrogen Electrolyzer Market Size and Trends Analysis

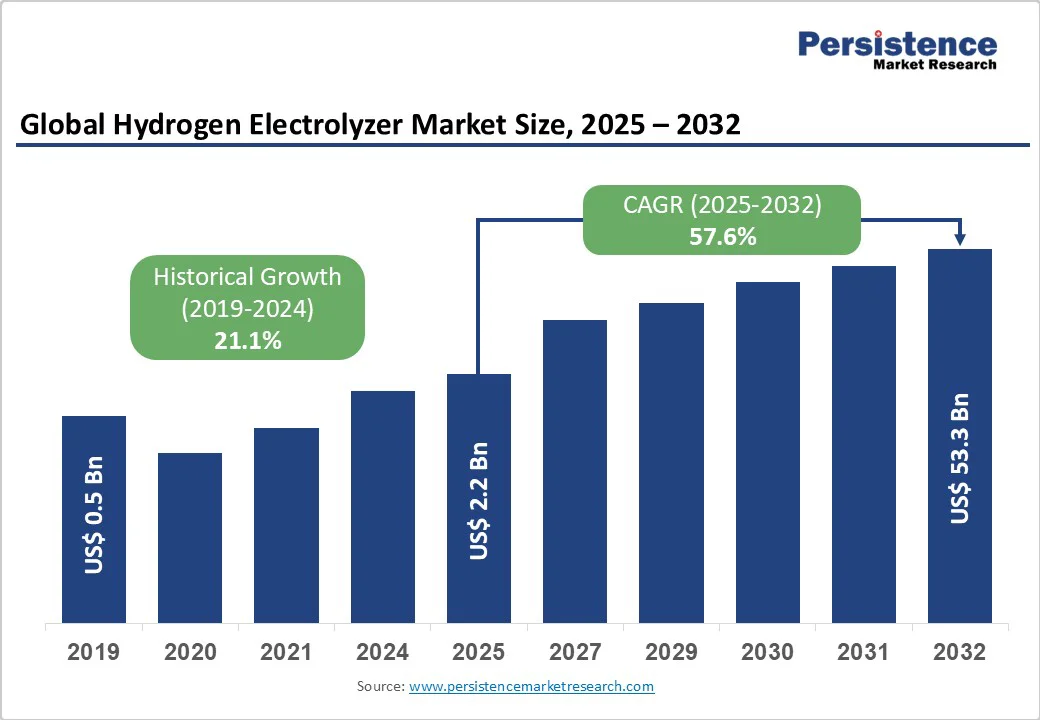

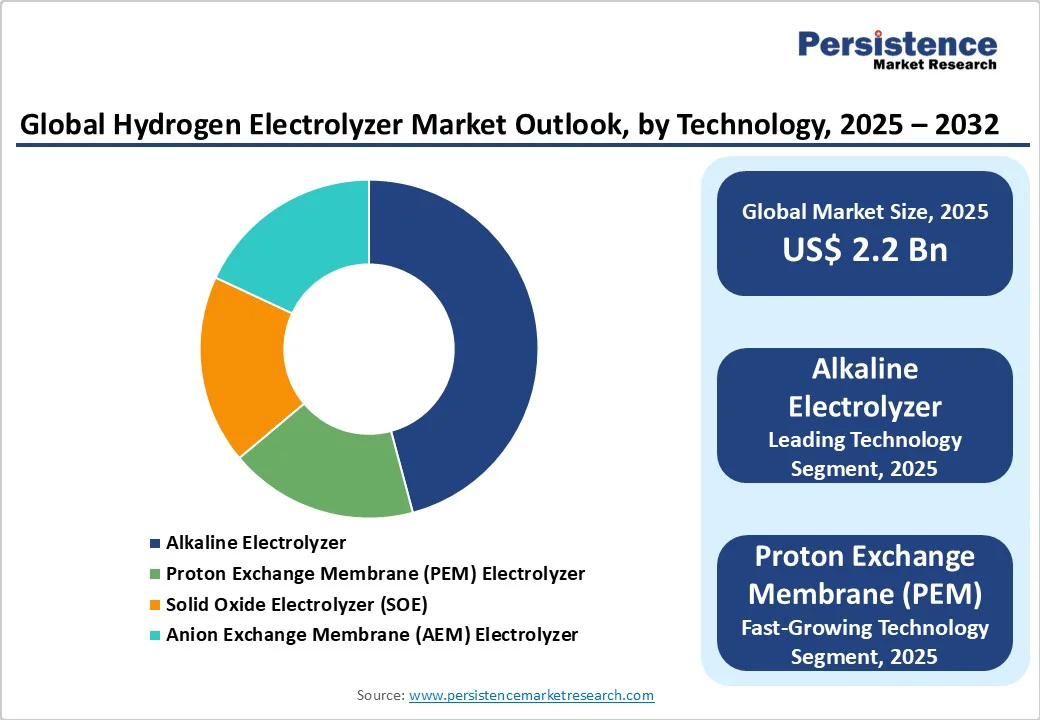

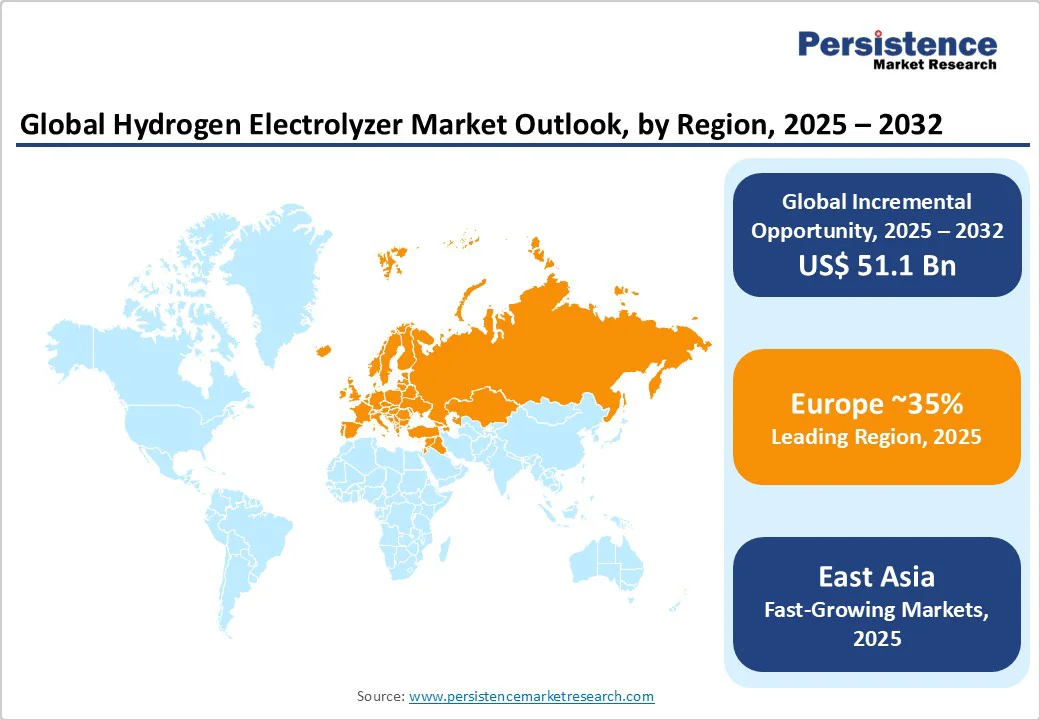

The global hydrogen electrolyzer market size was valued at US$2.2 billion in 2025 and is projected to reach US$53.3 billion by 2032, growing at a CAGR of 57.6% between 2025 and 2032, driven by the surging demand for clean energy, policy-driven incentives, large-scale integration of renewables, and technological advancements. By 2025, installed water electrolyzer capacity is estimated to reach 5 GW, with China leading in manufacturing and deployment.

Decarbonization initiatives across industrial sectors, sharply rising investment commitments, and innovation in electrolyzer technologies underpin a transformative market shift for low-emissions hydrogen, with final investment decisions on major projects growing rapidly.

Key Industry Highlights

- Leading Region: Europe is anticipated to dominate with a 35% market share, backed by strong policy incentives, industrial hydrogen hubs, and renewable energy integration.

- Fastest-growing Region: East Asia, driven by China’s dominance, accounting for nearly 70% of committed capacity, while leading manufacturers in China, Japan, and South Korea rapidly deploy PEM and alkaline projects for industrial and mobility applications.

- Dominant Component Type: Alkaline electrolyzers are anticipated to lead the market with a 49% market share in 2025, supported by large-scale industrial deployment and lower CAPEX.

- Fastest-growing Component Type: PEM electrolyzers are anticipated to hold a 34% market share in 2025, and represent the fastest-growing technology, driven by flexibility and renewable power integration.

- Key Driver: Industrial decarbonization in steel and chemicals drives major electrolyzer demand, especially for large-scale hydrogen substitution.

- Trend: Integrated renewable hydrogen projects are positioning electrolyzers as core assets in global clean energy transition strategies.

| Key Insights | Details |

|---|---|

|

Hydrogen Electrolyzer Market Size (2025E) |

US$2.2 Bn |

|

Market Value Forecast (2032F) |

US$53.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

57.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

21.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Policy Incentives and Decarbonization Mandates

Ambitious government agendas and policy frameworks have emerged as a primary force in market acceleration. The EU Hydrogen Strategy and the U.S. Inflation Reduction Act (IRA) Production Tax Credits exemplify regulatory efforts to stimulate clean hydrogen deployment.

In 2024, North America accounted for over 90% of low-carbon hydrogen capacity past FID, catalyzed by incentives such as the 45Q tax credit. Europe's policy support drove a fourfold increase in project FIDs recently, with the continent producing a total of 7.86 Mt of hydrogen in 2024, including 42.81 kt from electrolysis. These interventions are fostering project rapidity, streamlining capital flow, and ameliorating cost barriers, thereby unlocking global scalability for electrolyzer deployment.

Technological Advancements and Manufacturing Scale-Up

Rapid innovation in electrolyzer technologies, including advanced PEM and scalable alkaline units, has driven capacity expansion and cost optimization. Electrolyzer manufacturing capacity doubled in 2023 to 25 GW/year, with China commanding 60% global capacity and Europe reaching 10.6 GW by May 2025.

Companies such as Hysata, Thyssenkrupp Nucera, Siemens Energy, and John Cockerill Hydrogen have launched modular, high-efficiency units, as highlighted by recent investments such as Hysata's US$111 million Series B. Mass-manufacturable designs, lower CAPEX, and improved energy efficiency enable both large-scale and distributed hydrogen production, supporting decarbonization across the steel, chemicals, and heavy transport sectors.

Demand Diversification and Industrial Uptake

The emergence of industrial hubs and sectoral switch-over to green hydrogen is facilitating broader market adoption. By 2030, low-emissions hydrogen production from announced projects could reach 49 Mtpa, up from 38 Mtpa the previous year, with steel, chemicals, and petrochemicals representing the primary offtakes.

Major industrial projects such as Cepsa’s Andalusian Green Hydrogen Valley and Thyssenkrupp Nucera’s deployment for H2 Green Steel demonstrate successful alignment with renewable energy targets and climate goals. Offtake agreements, carbon contracts for difference, and increasing operational infrastructure (e.g., Europe’s 1,636 km of hydrogen pipelines and 186 Hrs) are catalyzing demand for electrolyzer-based hydrogen, stimulating further investments and technology diffusion.

Barrier Analysis - High Production Costs for Clean Hydrogen

The cost barrier for renewable hydrogen persists, with production averaging 6.7 EUR/kg in Europe (2024) compared to 3.3 EUR/kg for conventional SMR. Electrolysis-driven hydrogen remains 1.5 to 6 times costlier than fossil-based alternatives, constraining large-scale adoption.

While aggressive scaling and mass production offer potential for reductions, the IEA projection of US$2-9/kg H2 by 2030, immediate market penetration is hampered by significant capital requirements and dependency on low-cost renewable electricity.

Regulatory Uncertainty and Supply Chain Constraints

Market participants face risks from ambiguous regulatory timelines, e.g., pending RED III in the EU, evolving 45V standards in the U.S., and supply chain limitations.

Macroeconomic pressures, rising inflation, interest rates, and disruptions in renewable electricity markets have led to delays and cancellations in several renewable hydrogen projects globally, with actual FID-backed deployment expected to reach only 12 18 Mtpa of the 48 Mtpa announced capacity by 2030. This volatility challenges consistency in market expansion and dampens investment confidence across regions.

Opportunity Analysis - Regional Expansion in Emerging Markets

Latin America’s abundant renewable resources and decarbonized energy mix present strategic openings for electrolyzer deployment. By 2030, the region may produce over 7 Mtpa of hydrogen with carbon intensity below 3 kg CO2-eq/kg H2, aligning with international standards.

Initial projects in refining and ammonia support scalable domestic applications, setting the stage for hydrogen hubs and export-oriented supply to Europe and Asia, thereby addressing global decarbonization objectives and securing diversified market access. This opportunity is bolstered by phased infrastructure expansion, starting from demonstration-scale investments and gradually enhancing grid, transmission, and export capacity. Such approaches mitigate risks and accelerate operational readiness for larger investments, while providing regulatory clarity and export alignment.

Technological Convergence and Innovation Partnerships

Cross-industry collaborations and technology convergence are generating novel solutions for efficiency, scalability, and cost reduction. Notable partnerships such as Thyssenkrupp Nucera’s acquisition of modular high-pressure electrolysis assets, Siemens Energy’s joint ventures for manufacturing scale-up, and Samsung E&A’s strategic stake in Nel ASA highlight a shift toward integrating digitization, automation, and modularity across the value chain.

These alliances facilitate rapid innovation, enable adaptation to multiple industrial contexts, and reinforce the market's capability to meet specialized demand trends in sectors such as steelmaking, e-fuels, and mobility.

Category-wise Analysis

Technology Insights

Alkaline electrolyzers form the backbone of global capacity, holding 49% market share in 2025. Well-established in industrial applications, alkaline units demonstrate high reliability and lower capital expenses (CAPEX: 1,666 €/kW in Europe for 2023).

Standardized module design, such as Thyssenkrupp Nucera’s “scalum,” has enabled multi-megawatt installations, including the 700 MW deployment for green steel in Europe, supporting large-scale decarbonization with robust efficiency and cost performance.

Their functional flexibility favors integration with existing industrial facilities, such as refineries and ammonia plants, underscoring relevance for captive and merchant hydrogen production. The modular capacity of alkaline systems enables phased expansion, supporting both localized and large-scale hydrogen economies.

Proton Exchange Membrane (PEM) Electrolyzer is the fastest-growing technology, with significant deployment in Europe, the U.S., and East Asia. Projects such as Plug Power’s 10 MW GenEco™ PEM system in Portugal highlight PEM’s suitability for flexible, high-purity hydrogen production.

PEM electrolyzers support integration with variable renewable energy, providing rapid response to intermittent electricity availability and enabling hydrogen production for energy storage and mobility applications.

Power Rating Insights

The below 500 kW category dominates with 43% market share in 2025, serving distributed and on-site industrial needs. These units are widely applied in chemical, electronics, and local utility sectors, offering flexible integration with grid-connected and renewable energy sources. Their lower CAPEX and streamlined installation requirements make them ideal for decentralized hydrogen generation, supporting merchant and captive usages.

The 500 kW - 2 MW is the fastest-growing segment, holding 27% of the market share in 2025. Suitable for medium-scale industrial and municipal energy projects, this range balances capacity with operational efficiency. Deployment in Europe, India, and the U.S. demonstrates scalability for clusters and energy parks, supporting integration with solar and wind power and providing reliable hydrogen for multiple end-uses.

End-user Industry Insights

Energy & utilities are anticipated to command the largest market share of 45% in 2025, with aggressive integration of hydrogen into power generation, grid stabilization, and energy storage. Sector leaders such as Cepsa, Shell, and Stegra have adopted multi-hundred MW electrolyzer systems, ramping scale in alignment with utility decarbonization mandates. Hydrogen enables flexible backup capacity for renewables, provides grid-balancing capabilities, and expands options for low-carbon electricity generation.

Steel & metal processing is the fastest-growing end-user segment in 2025, underpinned by high-profile projects such as H2 Green Steel’s 700 MW deployment and Thyssenkrupp Nucera’s ramp-up to 5 million tons of green steel by 2030.

The adoption of electrolyzer-based hydrogen enables up to 95% reduction in carbon emissions, transforming traditional steel manufacturing. The transition sector is bolstered by regulatory compliance requirements, carbon contracts, and funding for green industrial clusters, positioning steel and metals for large-scale decarbonization and innovation investments.

Regional Insights

Europe Hydrogen Electrolyzer Market Trends

Europe holds 35% of the global hydrogen electrolyzer market share, supported by strong policy mandates and deep integration of renewable energy sources. In 2024, 7.86 Mt of hydrogen were produced, with clean hydrogen representing 42.81 kt from water electrolysis.

Electrolyzer manufacturing capacity reached 10.60 GW by May 2025, with 142.85 MW newly deployed. Germany, France, and the Netherlands lead with high-profile green steel and renewable integration projects.

Regulatory momentum driven by the EU Hydrogen Strategy and carbon contracts for difference is enabling cross-border hydrogen trade, amounting to 18.21 kt in 2024, and supporting infrastructure expansion, with 186 hydrogen refueling stations (HRS) in operation and 1,636 km of pipelines developed.

Market competition is characterized by consolidation around leading technology firms such as Thyssenkrupp Nucera, Siemens Energy, and John Cockerill Hydrogen. Investment trends favor large-scale renewable projects and industrial decarbonization, with strategic opportunities in mobility, steelmaking, and green ammonia. Production costs for clean hydrogen remain elevated, highlighting the continued need for investment and innovation.

North America Hydrogen Electrolyzer Market Trends

North America represents 25% of the global share, driven by the U.S. IRA incentives and large-scale renewable hydrogen deployments. Strong policy frameworks have shifted the region’s share of low-carbon hydrogen capacity past FID above 90%, accelerating construction and planned installations from 116 MW to 4,524 MW by 2030. Investment focuses on supply-side projects, with end-use industrial hubs in steel and refining.

Project pipeline maturity has improved, with committed-stage projects rising from less than 10 to nearly 100 between 2020 and 2024. Competitive dynamics favor technology innovation and geographic expansion, with companies forming strategic alliances to advance hydrogen manufacturing capacity, while infrastructure build-out supports scaling deployments across key industrial sectors.

East Asia Hydrogen Electrolyzer Market Trends

East Asia holds 20% of the global market share, with China accounting for nearly 70% of the committed electrolyzer capacity. Leading manufacturers in China, Japan, and South Korea are deploying PEM and alkaline electrolyzer projects for industrial and mobility applications. Regional focus is on integrating hydrogen with transport and semiconductor manufacturing, evidenced by Siemens Energy’s green hydrogen deployment for quartz glass production in Japan.

Manufacturing scale and cost optimization drive competitive advantage, with China supporting mass production via domestic supply chains and policy incentives. Investment trends favor giga-scale projects, while coordinated efforts are underway to broaden applications in mobility, steel, and electronics.

Competitive Landscape

The global hydrogen electrolyzer market exhibits a moderately consolidated structure, with major players commanding significant market share through their advanced technology portfolios and strategic partnerships. Leading industry giants Thyssenkrupp Nucera, Siemens Energy, Nel ASA, John Cockerill Hydrogen, Plug Power, and ITM Power dominate the competitive landscape, collectively representing over 60% of market concentration globally.

The market is characterized by intense competition focused on technological innovation, cost reduction, manufacturing scale-up, and strategic acquisitions to strengthen market positioning. The industry is witnessing rapid consolidation through mergers, acquisitions, and strategic partnerships as companies seek to achieve economies of scale and enhance their competitive edge in the rapidly expanding green hydrogen economy.

Key Industry Developments

- In October 2025, Plug Power delivered its first 10 MW GenEco™ PEM electrolyzer to Galp’s Sines Refinery in Portugal, marking the start of Europe’s largest 100 MW PEM project and enabling significant refinery decarbonization with an estimated 110,000 tons of CO2 reduction per year.

- In October 2024, John Cockerill Hydrogen received India’s largest electrolyzer order from AM Green for a 1.3 GW green ammonia project in Kakinada, deploying 640 MW advanced pressurized alkaline electrolyzers and planning a 2 GW/year manufacturing plant, supporting India’s National Green Hydrogen Mission.

Companies Covered in Hydrogen Electrolyzer Market

- Thyssenkrupp Nucera AG

- John Cockerill Hydrogen

- Nel ASA

- Plug Power Incorporated

- Siemens Energy AG

- Enapter S.r.l.

- Cummins Inc.

- ITM Power PLC

- McPhy Energy S.A.

- Haldor Topsoe A/S

Frequently Asked Questions

The hydrogen electrolyzer market is projected to be valued at US$2.2 Billion in 2025.

Alkaline electrolyzers are expected to hold 49% market share in 2025, maintaining their position as the leading technology segment due to proven maturity and cost-effectiveness.

The hydrogen electrolyzer market is poised to witness a CAGR of 57.6% from 2025 to 2032.

The hydrogen electrolyzer market growth is driven by decarbonization policies, government incentives, technological advancements, and renewable energy integration.

The key opportunities lie in emerging markets, industrial hubs, technology partnerships, and manufacturing scale-up.

The top key market players in the hydrogen electrolyzer market include Thyssenkrupp Nucera, Siemens Energy, Nel ASA, John Cockerill Hydrogen, Plug Power, and ITM Power.