- Semiconductor Materials & Components

- Semiconductor Intellectual Property (IP) Market

Semiconductor Intellectual Property (IP) Market Size, Share, and Growth Forecast, 2026 - 2033

Semiconductor Intellectual Property (IP) market by IP Type (Processor IP, Interface IP, Memory IP, and Miscellaneous IP.) IP Source (Royalty, Licensing), Delivery Mode (Soft IP Core, Hard IP Core), Industry (Consumer Electronics, Automotive, Telecommunications / IT & Telecom, Healthcare & Medical Devices, Other Industrial), and Regional Analysis for 2026 - 2033

Semiconductor Intellectual Property (IP) Market Size and Trends Analysis

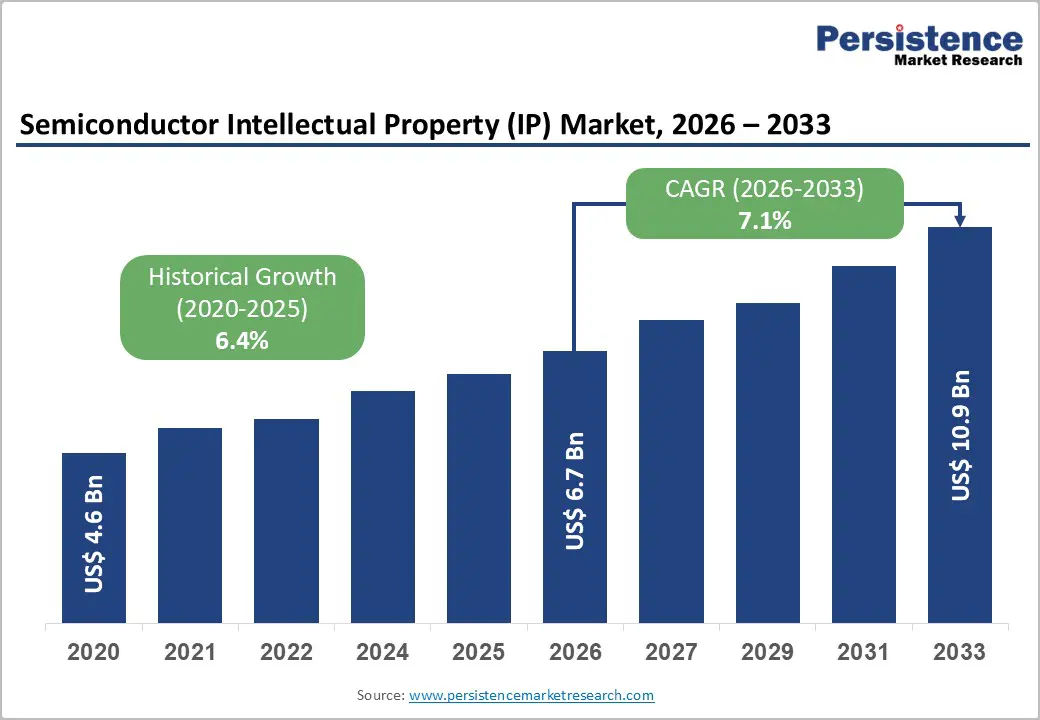

The global semiconductor intellectual property (IP) market size is likely to be valued at US$ 6.7 billion in 2026 and is projected to reach US$ 10.9 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

This measured growth trajectory reflects the maturation of the semiconductor IP ecosystem and the rising demand for specialized IP solutions across AI-driven chip design, automotive electronics, and advanced computing applications. The market's expansion is propelled by substantial government investments in semiconductor infrastructure through programs like the CHIPS and Science Act, allocating $52.7 billion toward U.S. semiconductor R&D and manufacturing, coupled with the exponential adoption of AI chips requiring advanced processor and memory IP, and the emergence of autonomous vehicle requirements driving automotive semiconductor complexity.

Global semiconductor sales reached $627.6 billion in 2024, representing 19.1% year-over-year growth with memory product sales surging 78.9% and DRAM products recording 82.6% growth, creating corresponding demand for memory IP and interface IP solutions supporting these high-performance applications.

Key Industry Highlights:

- AI and Data Center Demand Drives IP Growth - Exponential adoption of AI and hyperscale data centers is boosting demand for advanced processor and memory IP, with ARM Holdings reporting 23% YoY royalty growth in Q2 2025.

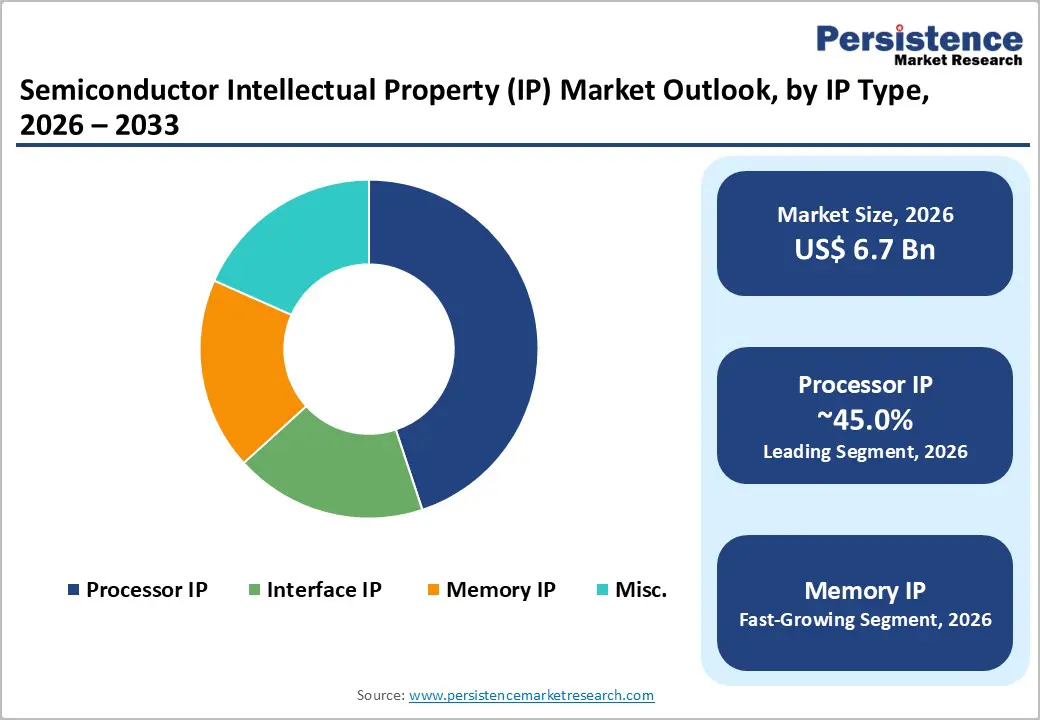

- Processor IP Leads Market Segments - Processor IP accounts for ~45% of the market in 2026, driven by advanced CPU architectures such as ARM Cortex-X925 and Cortex-A725, optimized for AI workloads.

- Memory IP Accelerates Innovation - Memory IP, including DRAM, NAND Flash, and advanced memory architectures, is the fastest-growing segment due to AI, cloud, and edge computing requirements.

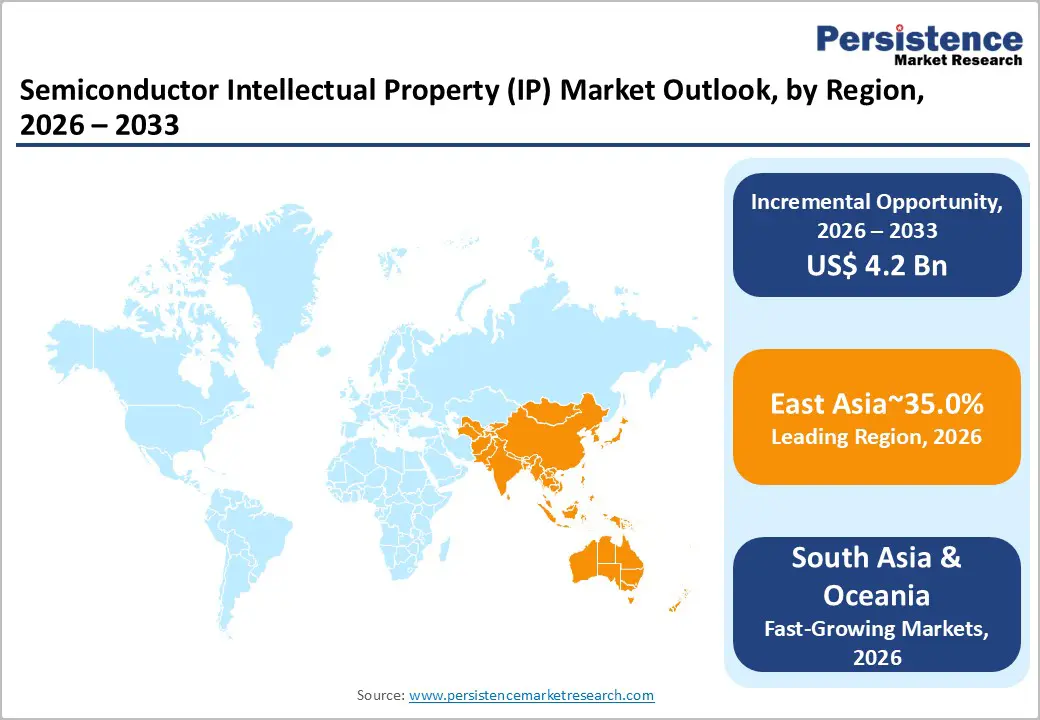

- Leading Region: Supported by CHIPS and Science Act investments, major IP players such as ARM, Synopsys, Cadence, Intel, and NVIDIA are driving regional semiconductor IP growth and innovation.

- Fast-growing Region: China, South Korea, and Taiwan dominate semiconductor IP development, with initiatives like "Made in China 2025" and strategic partnerships such as Cadence-TSMC enhancing AI and advanced chip designs.

- Key Opportunities in Emerging Hubs - China’s domestic IP development and India’s rising semiconductor design capabilities create strategic opportunities for IP licensing, cross-border collaborations, and the deployment of advanced processor, memory, and interface IP.

| Key Insights | Details |

|---|---|

| Semiconductor Intellectual Property (IP) Market Size (2026E) | US$ 6.7 Bn |

| Market Value Forecast (2033F) | US$ 10.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Dynamics

Growth Drivers - Exponential Growth in AI and Data Center Semiconductor Demand

The artificial intelligence revolution fundamentally transformed semiconductor IP requirements, driving substantial demand for advanced processors and memory IP solutions optimized for AI workloads. The AI semiconductor market is projected to grow from $150 billion in 2025 to $500 billion by 2028, driven by hyperscale data center expansion, edge computing deployment, and AI-enabled personal computing devices. ARM Holdings reported record Q2 2025 non-GAAP earnings per share of $0.30 with 23% year-over-year royalty revenue growth to $514 million, demonstrating the market's accelerating adoption of AI-focused processor IP architecture.

ARM's latest processor IP releases, including the Cortex-X925 and Cortex-A725 CPU designs for 3-nanometer nodes, embody the market's need for AI-optimized architecture and interface IP. The Semiconductor Intellectual Property (IP) Market has expanded substantially as organizations recognize that custom processor designs, optimized memory hierarchies, and specialized AI accelerator IP directly enable competitive advantages in AI chip development.

Major technology companies, including Google, are deploying ARM-based Axion processors that deliver 60% higher performance at the same power consumption as x86-based alternatives, validating the strategic importance of processor IP differentiation in data center markets.

Regulatory Mandates and Government Investment in Domestic Semiconductor Ecosystems

Governments worldwide have prioritized semiconductor IP development as a strategic national objective, with substantial financial commitments accelerating market expansion. The U.S. CHIPS and Science Act allocated $52.7 billion to strengthen U.S. semiconductor R&D, manufacturing, and intellectual property development, aiming to boost domestic chip production and enhance competitiveness against the Asia-Pacific and European regions.

The U.S. Patent and Trademark Office launched the Semiconductor Technology Pilot Program in November 2023 to support the CHIPS for America initiative, expediting examination of qualifying semiconductor patent applications and accelerating innovation in semiconductor device manufacturing.

India has emerged as a significant market, with the INR76,000-crore Production Linked Incentive scheme and the Design Linked Incentive program supporting domestic semiconductor innovation. ICEA's launch of the Semiconductor Product Design Leadership Forum in September 2025 exemplifies India's strategic effort to transform the country into a global hub for semiconductor design and intellectual property creation. The Semiconductor Intellectual Property (IP) Market benefits directly from these government initiatives, which establish regulatory frameworks that support IP protection, accelerate patent development, and facilitate cross-border collaboration in semiconductor innovation.

Memory Density and Advanced Data Storage Requirements

Memory IP represents one of the fastest-advancing segments within the Semiconductor Intellectual Property (IP) Market, driven by exponential demand for data storage and processing capabilities in AI, cloud computing, and edge computing applications. Global semiconductor memory product sales increased 78.9% in 2024 to $165.1 billion, with DRAM products achieving the highest percentage growth at 82.6%, directly reflecting demand for memory IP supporting these applications. High-performance computing environments, data centers, and cloud providers require increasingly sophisticated memory IP designs, including DRAM, NAND Flash, and advanced memory architectures that support higher storage density, faster access speeds, and improved power efficiency.

The prevalence of AI machine learning and big data analysis applications necessitates memory IP delivering superior performance within thermal and power constraints, creating specialized requirements for memory IP providers. Companies requiring memory IP increasingly demand DRAM technologies, including DDR4 and DDR5 implementations, SRAM configurations, and advanced memory interface protocols optimized for contemporary processors and graphic processing units.

Synopsys' comprehensive interface IP portfolio, which addresses memory-related protocols including CXL, Die-to-Die, and DDR, demonstrates how IP providers address escalating memory IP complexity supporting next-generation computing architectures.

Restraint - Rise in Licensing Costs and Complex Royalty Structures

High licensing costs associated with semiconductor IP represent a substantial barrier to adoption, particularly constraining smaller companies and emerging design organizations from accessing premium IP portfolios.

Acquiring comprehensive processors, memory, and interface IP requires substantial capital investment, with annual licensing fees for advanced architecture IP exceeding millions of dollars, depending on usage rights and manufacturing scale. The complexity of royalty structures where manufacturers pay fees based on per-unit production volumes, percentage of selling price, or hybrid arrangements creates uncertainty in cost modeling and constrains design decisions.

Semiconductor startups and fabless design companies often face difficulty justifying IP licensing investments during early commercialization stages when production volumes remain limited, effectively fragmenting the market and limiting accessibility. This cost barrier disproportionately affects emerging markets and smaller innovation hubs, reducing their ability to develop competitive chip designs and concentrating on IP market opportunities among large technology companies with substantial financial resources.

Opportunity - China's Domestic Semiconductor IP Development and Strategic Self-Sufficiency

China's strategic emphasis on developing indigenous semiconductor IP capabilities presents substantial opportunities within the Semiconductor Intellectual Property (IP) Market, driven by government investments, geopolitical tensions, and national technology leadership objectives.

China filed nearly 70,000 PCT patent applications in 2024, reflecting rapid growth in semiconductor-related IP development and maintaining China's global leadership in innovation volume. Chinese government initiatives including the "National IC Strategy" and "Made in China 2025" program, have prioritized establishing a fully closed-loop semiconductor ecosystem, reducing reliance on foreign technologies, and strengthening domestic IP portfolios.

Companies including Huawei HiSilicon and Biren are advancing competitive semiconductor designs for mobile and AI applications, while memory chip producers YMTC and CXMT have made substantial strides in mature-node semiconductor manufacturing. Huawei's patent portfolio exceeds 140,000 patents and the company is strategically leveraging IP to support international partnerships and risk management while advancing technological development.

The Semiconductor Intellectual Property (IP) Market benefits from increased Chinese investment in semiconductor IP licensing, domestic IP development, and strategic international collaborations addressing technology gaps. The March 2025 WIPO China roundtable highlighted how Huawei, Xiaomi, Alibaba, and BOE are leveraging intellectual property strategically to support enterprise innovation and international competitiveness in emerging technologies including semiconductors and AI.

China's emphasis on optimizing international IP strategies through WIPO systems, including PCT, Madrid, and Hague frameworks, demonstrates increasing sophistication in semiconductor IP portfolio management. As U.S.-China geopolitical tensions reshape technology landscapes, Chinese firms are increasingly developing alternative semiconductor IP designs and architectures reducing dependency on foreign technology providers, creating opportunities for IP providers serving Chinese enterprises and supporting dual-IP ecosystem development..

India's Emerging Semiconductor Design and IP Creation Capabilities

India has emerged as a rapidly advancing semiconductor design and IP innovation hub, with government-backed initiatives and substantial talent pools creating distinctive market opportunities. The Design Linked Incentive program and Production Linked Incentive scheme, totaling INR76,000 crore, represent substantial government commitments supporting domestic semiconductor innovation and design capability development.

SEMICON India 2025 highlighted India's accelerating role in the global semiconductor ecosystem, with companies including CG-Semi and Vervesemi Microelectronics driving domestic semiconductor innovation spanning design to end-to-end manufacturing and advanced applications in defense, aerospace, electric vehicles, and energy systems. India's first OSAT pilot line launch in Sanand, Gujarat, demonstrates the country's developing IP and manufacturing capabilities, signaling a strategic shift from semiconductor consumption to indigenous creation.

The semiconductor intellectual property (IP) market is expanding substantially as India develops competitive semiconductor design capabilities requiring advanced processor, memory, and interface IP solutions. The ICEA Semiconductor Product Design Leadership Forum, launched in September 2025, aims to establish India as a global hub for semiconductor design and intellectual property creation by fostering innovation, addressing structural design challenges, and enabling cross-border collaborations.

By promoting indigenous IP creation, enabling design-manufacturing integration, and facilitating international partnerships, India is positioning itself to develop globally competitive IP-rich semiconductor solutions. India's large semiconductor design talent pool, combined with government support and increasingly sophisticated IP infrastructure, creates opportunities for both IP providers serving Indian design firms and for collaborative IP development partnerships that accelerate India's semiconductor competitiveness.

Category-wise Analysis

IP Type Insights

Processor IP represents the largest segment within the Semiconductor Intellectual Property (IP) Market, commanding approximately 45% of market share in 2026. Processor IP encompasses CPU architectures, microprocessor designs, and specialized computing cores addressing diverse application requirements spanning mobile computing, high-performance computing, data centers, and edge computing environments. ARM Holdings has maintained market leadership through its processor IP portfolio, reporting record FYE25 revenues exceeding $4 billion with royalty revenues reaching $2 billion, driven by deployment of ARM Cortex-X925 and Cortex-A725 CPU IP for advanced AI workloads.

Processor IP demand is fundamentally driven by the exponential growth in AI semiconductor requirements, cloud computing expansion, and the proliferation of connected devices requiring specialized processing capabilities. Companies, including Synopsys and Cadence Design Systems, provide complementary processor verification and design tools that optimize processor IP implementation, while strategic partnerships between processor IP providers and technology companies validate the strategic importance of differentiated processor designs in competitive markets.

Memory IP represents the fastest-advancing segment within the Semiconductor Intellectual Property (IP) Market, reflecting exponential demand for advanced memory solutions supporting AI, data center, and high-performance computing applications.

Industry Insights

Consumer electronics represent the largest end-use industry segment within the Semiconductor Intellectual Property (IP) Market, commanding approximately 38% of market share in 2026. Consumer electronics applications, including smartphones, tablets, personal computers, gaming devices, and home entertainment systems, require diverse semiconductor IP that address performance optimization, power efficiency, and multimedia processing capabilities. Smartphone and tablet processors rely heavily on advanced processor IP, including ARM Cortex architectures, memory IP supporting high-performance DRAM and storage systems, and interface IP implementing wireless connectivity, sensor integration, and multimedia interfaces.

Automotive represents the fastest-advancing end-use industry segment within the Semiconductor Intellectual Property (IP) Market, driven by electrification, autonomous vehicle development, and advanced in-vehicle computing requirements.

Regional Insights and Trends

North America Semiconductor Intellectual Property (IP) Market Trends

North America commands approximately 30% of the global Semiconductor Intellectual Property (IP) Market and represents the second-largest regional market. The region's dominance reflects the substantial presence of semiconductor IP leaders, including ARM Holdings, Synopsys, and Cadence Design Systems, complemented by major semiconductor manufacturers and fabless design companies.

The CHIPS and Science Act's $52.7 billion investment to strengthen U.S. semiconductor R&D, manufacturing, and intellectual property directly impacts the development of the North American semiconductor IP market. The U.S. Patent and Trademark Office's Semiconductor Technology Pilot Program expedites patent examination for semiconductor applications, directly supporting North American IP protection and innovation acceleration. Major North American semiconductor companies, including Intel, Qualcomm, and NVIDIA, maintain substantial IP development investments, with industry analysis indicating that North American organizations account for approximately 25% of global semiconductor patent filings in specialized high-value categories.

Data center expansion across North American hyperscale cloud providers drives demand for advanced processor and memory IP, optimizing AI workload performance and power efficiency. The region's robust venture capital ecosystem supporting semiconductor startups and emerging design firms creates corresponding demand for accessible IP licensing arrangements and specialized IP addressing niche market requirements.

East Asia Semiconductor Intellectual Property (IP) Market Trends

East Asia commands approximately 35% of the global Semiconductor Intellectual Property (IP) Market and represents the largest regional market. The region's dominance reflects substantial semiconductor manufacturing infrastructure, consolidation among integrated device manufacturers, and concentration of large-scale fabless design companies.

China dominates semiconductor patent filings, accounting for over 88% of all annual filings and more than 20,000 applications in 2023, consolidating its position as a major innovation hub. Government initiatives including the "National IC Strategy" and "Made in China 2025" have prioritized semiconductor IP development, with hundreds of billions of dollars invested to foster a fully closed-loop semiconductor ecosystem. South Korea and Taiwan maintain substantial semiconductor manufacturing capabilities and chip design expertise, with companies including TSMC and Samsung advancing semiconductor innovation across advanced manufacturing nodes and specialized process technologies.

The Cadence Design Systems and TSMC strategic partnership announced in July 2024 to co-develop chiplet interconnect and 3D-stacking-optimized IP solutions exemplifies regional commitment to advancing semiconductor IP capabilities. India's emergence as a semiconductor design hub through initiatives including the Design Linked Incentive program and SEMICON India showcases the region's diversifying semiconductor IP ecosystem. East Asian semiconductor sales grew 12.5% year-over-year in 2024, with regional emphasis on AI semiconductors, advanced automotive applications, and specialized industry-specific chip designs directly driving demand for memory IP, processor IP, and interface IP.

Europe Semiconductor Intellectual Property (IP) Market Trends

Europe commands approximately 15% of the global Semiconductor Intellectual Property (IP) Market, representing a recovering regional market supported by EU Chips Act initiatives and semiconductor manufacturing expansion. European semiconductor sales declined 8.1% in 2024 compared to 2023, reflecting cyclical market conditions and competing regional investment priorities.

The European Commission's EU Chips Act, adopted in September 2023, supports semiconductor R&D collaboration and intellectual property strategy development among European companies, with pillar provisions enabling joint R&D initiatives and IP sharing arrangements. The regulation establishing AI gigafactories under the EuroHPC Joint Undertaking aims to strengthen European AI infrastructure and integrate governance requirements that support IP protection.

Competitive Landscape

The global Semiconductor Intellectual Property (IP) market is largely consolidated, with a few leading companies holding substantial market influence due to their advanced IP portfolios, technological expertise, and long-standing industry presence. Key players such as Arm Limited, Synopsys, Cadence Design Systems, Imagination Technologies, Rambus, and CEVA, Inc. dominate the market by offering a wide range of IP cores, design tools, and licensing solutions to semiconductor manufacturers worldwide. These companies leverage their strong R&D capabilities and established client networks to maintain leadership in high-demand segments like processor IP, memory IP, interface IP, and custom logic IP.

Competition in the market is driven primarily by innovation, product differentiation, and licensing models. Companies continuously enhance their IP portfolios to address emerging technological trends such as AI, 5G, automotive electronics, and low-power designs.

Firms like VeriSilicon, Analog Bits, and Dream Chip Technologies GmbH play a significant role in specialized niches, but the overall market remains dominated by the top-tier players, reflecting high entry barriers for new entrants due to IP complexity and development costs.

Key Industry Developments

- March 20, 2024 - Synopsys, Inc. completed the acquisition of Intrinsic ID, a leading provider of Physical Unclonable Function (PUF) IP, enhancing its semiconductor IP portfolio. This acquisition strengthens Synopsys’ SoC security capabilities by enabling unique chip identifiers for applications like identification and product tracking, while expanding its R&D presence in the Netherlands and establishing a center of excellence for PUF technology.

- August 14, 2023 - Intel and Synopsys expanded their long-standing IP and EDA strategic partnership with a multi-generational agreement to develop a portfolio of semiconductor IP for Intel 3 and Intel 18A process nodes. This collaboration enhances IP access for Intel Foundry Services customers, enabling faster design execution, optimized system-on-chip (SoC) performance, and accelerated delivery of AI-enabled and high-performance semiconductor products.

Companies Covered in Semiconductor Intellectual Property (IP) Market

- Arm Limited

- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Imagination Technologies

- CEVA, Inc.

- Rambus Inc.

- VeriSilicon

- Lattice Semiconductor

- eMemory Technology Inc.

- Achronix Semiconductor Corporation

Frequently Asked Questions

The global semiconductor intellectual property (IP) market is projected to be valued at US$ 6.7 Bn in 2026.

The Processor IP segment is expected to account for approximately 45.0% of the global Semiconductor Intellectual Property (IP) market by IP Type in 2026.

The semiconductor intellectual property (IP) market is expected to witness a CAGR of 7.1% from 2026 to 2033.

The global semiconductor intellectual property (IP) market growth is driven by rising AI and data center demand, government investments and regulatory support, and increasing memory and advanced data storage requirements.

Key market opportunities in the global semiconductor intellectual property (IP) market lie in China’s domestic IP development for self-sufficiency and India’s emerging semiconductor design and IP innovation ecosystem.

The key players in the Semiconductor Intellectual Property (IP) market include Microsoft Corporation, Google LLC (Alphabet), SAP SE, Oracle Corporation, Salesforce Inc., Truera Inc.