- Testing, Inspection, & Certification

- Life Insurance Policy Administration Systems Market

Life Insurance Policy Administration Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Life Insurance Policy Administration Systems Market by Component (Software, Services), Policy Type (Term Life Insurance, Whole Life Insurance, Misc.), Deployment Mode (On-Premises, Cloud/Hosted, Misc.), Application (New Business Processing, Underwriting, Policy Administration, Claims Management, Billing and Accounting) and Regional Analysis for 2026 - 2033

Life Insurance Policy Administration Systems Market Size and Trends Analysis

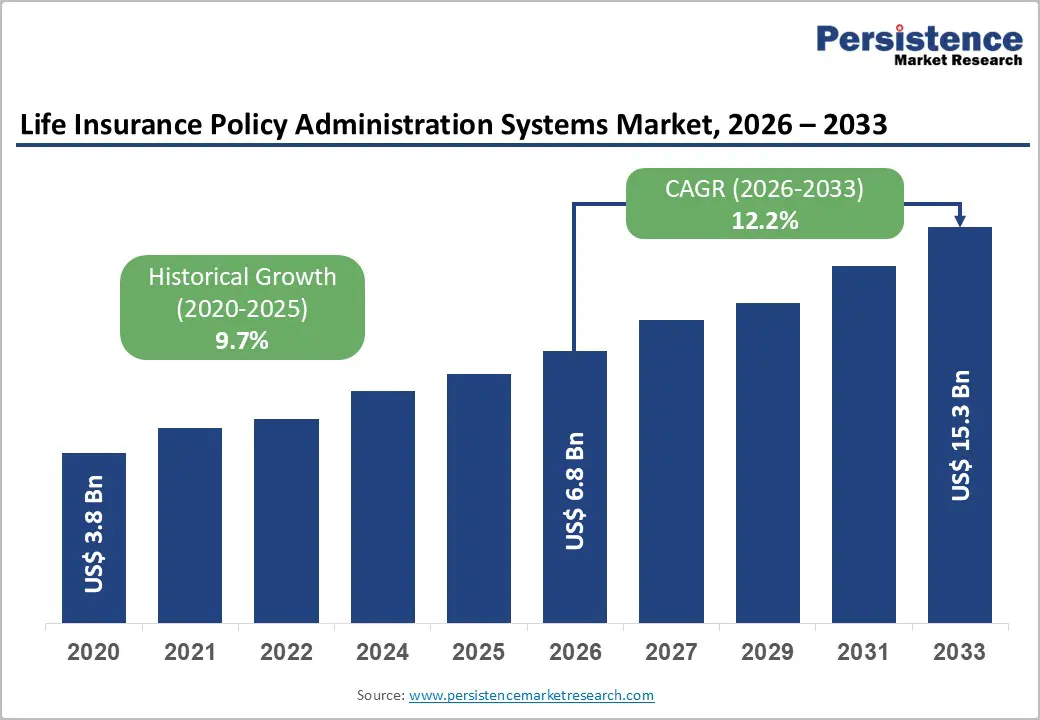

The Global Life Insurance Policy Administration Systems Market size was valued at US$ 6.8 billion in 2026 and is projected to reach US$ 15.3 billion by 2033, growing at a CAGR of 12.2% between 2026 and 2033.This represents a substantial acceleration from the historical CAGR of 9.7%, reflecting the sector's transition toward digital-first operational frameworks.

The market expansion is driven by three primary catalysts: the imperative shift toward regulatory compliance automation, the technological advancement in cloud-based infrastructure deployment, and the accelerating demand for operational efficiency across policy lifecycle management. These factors collectively position policy administration systems as essential infrastructure investments for global life insurers navigating complex regulatory environments and evolving customer expectations

Key Industry Highlights:

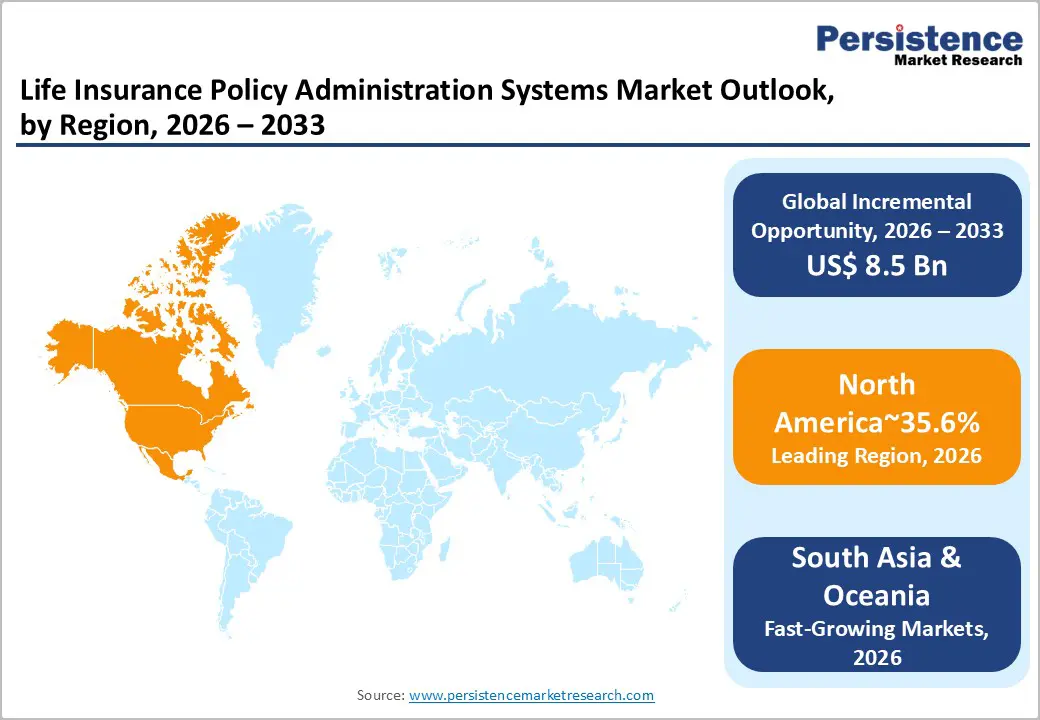

- Regional Leadership: North America leads the Global Life Insurance Policy Administration Systems Market with 35.6% share, supported by strong regulatory oversight, high insurance penetration, and sustained modernization investments.

- Strong European Market: Europe holds a significant 22% share, reinforced by Solvency II/GDPR-driven compliance modernization and API-based policy administration integrations.

- Rapid East Asia Expansion: East Asia represents a fast-expanding regional cluster with 18% share, driven by mobile-first insurance ecosystems, cloud adoption, and embedded insurance models.

- Dominant Component Segment: Software leads with 63.3% share, reflecting its central role in underwriting, policy servicing, billing, and compliance automation.

- Leading Policy Type: Term Life Insurance accounts for 46.7% share, driven by standardized underwriting, cost-efficient coverage, and faster digital issuance models.

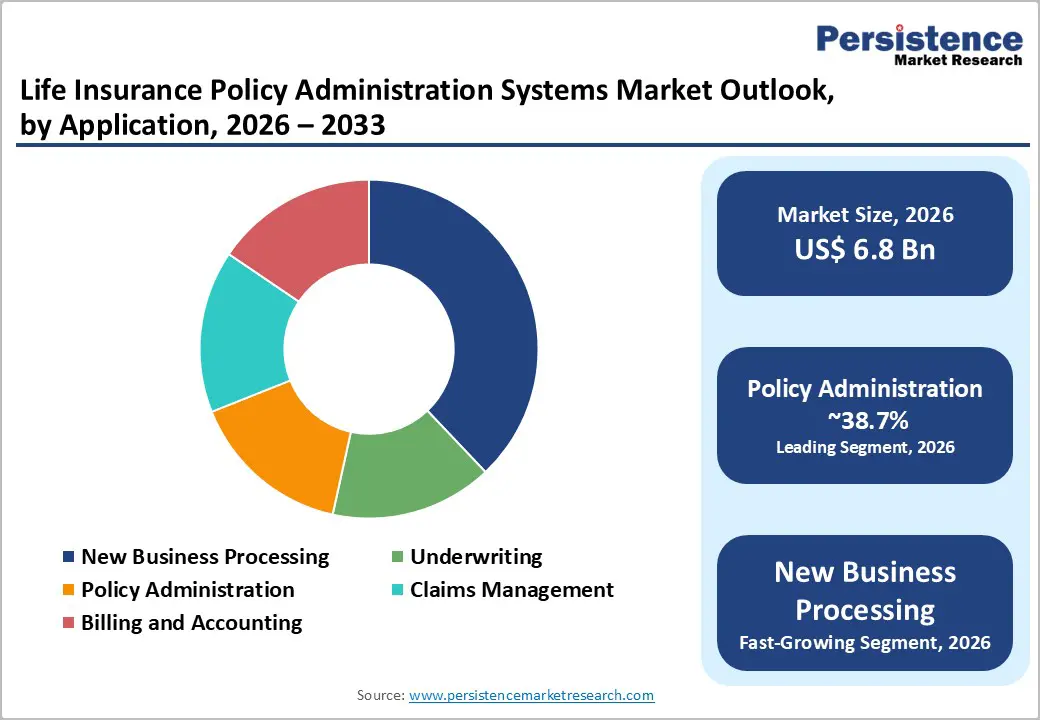

- Core Application Segment: Policy Administration dominates with 38.7% share, underscoring its foundational role in policy lifecycle servicing, renewal management, and regulatory alignment.

| Key Insights | Details |

|---|---|

| Life Insurance Policy Administration Systems Market Size (2026E) | US$ 6.8 Bn |

| Market Value Forecast (2033F) | US$ 15.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.7% |

Market Dynamics

Growth Drivers

Regulatory Compliance Complexity and Digitalization Mandates

Regulatory frameworks governing life insurance policy administration have fundamentally transformed operational requirements across global markets. Insurance regulators, through institutions such as the National Association of Insurance Commissioners (NAIC) and equivalent state-level authorities, have established mandatory compliance standards that necessitate sophisticated digital documentation, audit trails, and transparent reporting mechanisms. The Life Insurance Policy Administration Systems Market has become instrumental in meeting these compliance mandates, as regulatory bodies increasingly require demonstrable evidence of proper policy handling, claims documentation, and customer data protection protocols.

The shift toward digitalization is not discretionary but regulatory-driven. Insurance commissioners have recognized that digitalized policy administration creates verifiable compliance records, reduces administrative errors, and enables rapid response to regulatory inquiries. The NAIC's 2025 federal legislative priorities emphasize strengthening state-based insurance regulation through enhanced oversight mechanisms, a development that directly increases compliance demands on policy administration platforms. State insurance regulators supervise the largest and most competitive insurance sector globally, necessitating that insurers maintain sophisticated administrative systems capable of audit verification. Life Insurance Policy Administration Systems now function as critical compliance infrastructure, with regulatory authorities explicitly monitoring the technological robustness of backend systems managing policy data and claims processing.

The regulatory compliance driver transforms policy administration from operational necessity to strategic competitive advantage. Insurers investing in compliant, digitally native systems position themselves advantageously within regulatory environments that increasingly penalize non-compliance through licensing restrictions or operational sanctions.

Technological Convergence in Cloud-Native Architecture and AI-Driven Automation

The technological evolution of policy administration platforms has accelerated dramatically, with cloud-native architecture and artificial intelligence emerging as fundamental system components rather than peripheral enhancements. Modern Life Insurance Policy Administration Systems increasingly integrate cloud-based infrastructure with machine learning algorithms capable of automating underwriting assessments, claims validation, and policy issuance workflows. This technological convergence addresses a critical operational challenge: the massive volume of policy lifecycle transactions that manual processes cannot efficiently manage.

Digital transformation initiatives across the insurance sector have demonstrated measurable productivity improvements. Claims processing automation, powered by AI and digital document management, has reduced historically time-consuming assessment procedures significantly. Underwriting processes enhanced through predictive analytics enable more accurate risk assessment while reducing manual review cycles.

The integration of eSignatures and digital webforms has become standard practice for policy documentation, enabling faster policy issuance with legally compliant audit trails. The Life Insurance Policy Administration Systems Market reflects this technological maturation, with vendors increasingly embedding generative AI, embedded insurance capabilities, and modular API-driven architectures that provide operational agility. Cloud deployment models have become industry standard, with on-premises solutions transitioning toward hybrid and SaaS-based architectures that provide scalability, reduced capital expenditure, and enhanced system interoperability.

Market Restraining Factors

Legacy System Integration Complexity and Technological Lock-in

A substantial proportion of global insurance enterprises operate legacy policy administration systems implemented 15-20 years ago, often written in obsolete programming languages and architectures fundamentally incompatible with modern cloud-native or AI-capable platforms. Migration from these legacy systems presents extraordinary technical complexity: insurers must simultaneously maintain uninterrupted policy service for millions of active policyholders while transferring decades of accumulated policy data, claims history, and customer information to successor systems. The risk of data loss, policy processing failures, or customer service disruption during migration creates organizational paralysis, effectively trapping insurers within legacy system ecosystems despite documented operational inefficiencies.

Many legacy systems are so deeply integrated into supporting business processes that isolation and replacement become exceptionally costly. Vendor lock-in dynamics compound this problem: legacy system vendors often control proprietary data formats and integration protocols, making independent migration impossible without vendor cooperation and substantial additional implementation costs. Small and mid-sized insurers are particularly vulnerable to this restraint, lacking capital resources required for comprehensive system replacement. The direct result is delayed Life Insurance Policy Administration Systems investment, constraining market growth for newer technology vendors.

Implementation Cost Barriers and Capital Intensity of Modern Solutions

Modern cloud-native Life Insurance Policy Administration Systems involve substantial upfront capital investment infrastructure licensing, professional implementation services, internal staff training, and ongoing system customization often exceed US$ 5-15 million for mid-sized enterprises. For geographically distributed insurers operating across multiple regulatory jurisdictions, costs scale dramatically as each region may require customized configurations addressing local regulatory requirements. This capital intensity creates a material financial barrier, particularly for regional and smaller insurance enterprises.

Many vendors employ consumption-based pricing models where ongoing operational costs directly scale with policy volume and transaction throughput. Insurers cannot accurately forecast implementation timelines or total cost of ownership, creating budget uncertainty and procurement hesitation. The extended implementation periods further strain organizational resources, requiring sustained IT and business process expertise allocation without immediate revenue realization. These financial barriers directly constrain market growth, particularly in developing regions where insurance enterprises operate with more limited capital resources and ROI requirements are more stringent.

Key Market Opportunities

Embedded Insurance and Digital-First Distribution Channel Integration

Emerging insurance distribution models commonly termed "embedded insurance" or "insurance-as-a-service" represent a fundamental departure from traditional insurance distribution. In this model, insurance products are integrated within non-insurance digital platforms fintech applications, travel booking services, e-commerce marketplaces Has embedded functionality rather than standalone products. This convergence requires sophisticated policy administration systems capable of operating seamlessly within third-party technical ecosystems, managing real-time policy lifecycle events triggered by customer actions outside traditional insurance environments.

The Market faces significant opportunities from this distribution evolution. Embedded insurance requires dramatically different system architectures specifically, API-driven, microservices-based platforms capable of real-time integration with external systems. Traditional monolithic policy administration systems cannot address these architectural requirements. Insurance enterprises and technology vendors are investing substantially in development of embedded insurance-capable platforms, creating new market segments and technology categories. The embedded insurance opportunity is particularly acute in Asia-Pacific regions, where digital platform ecosystems are relatively more mature and economically substantial. Enterprise insurance deployments supporting embedded insurance models represent new revenue streams and differentiated market positioning for vendors capable of delivering appropriate technical capabilities.

Regulatory Technology (RegTech) Integration and Advanced Compliance Automation

Insurance regulatory environments have become progressively more complex, with compliance frameworks across major markets introducing sophisticated data protection requirements, anti-fraud mechanisms, and consumer protection standards. The integration of regulatory technology capabilities into policy administration systems particularly automated compliance verification, regulatory reporting automation, and advanced fraud detection represents a rapidly expanding market opportunity. Regulatory technology vendors have demonstrated measurable value in automating compliance processes, reducing compliance-related operational costs, and enabling proactive regulatory risk management.

Life Insurance Policy Administration Systems increasingly incorporate regulatory technology capabilities, enabling automated monitoring of policy conformance, digital-native audit trail generation, and real-time regulatory reporting integration. The opportunity extends beyond basic compliance automation; sophisticated RegTech implementations provide competitive advantages through enhanced risk management and accelerated new product deployment cycles. Enterprise insurers investing in RegTech-integrated policy administration systems can demonstrate regulatory alignment more effectively, potentially accelerating regulatory approval processes for new products or market entry strategies. Government regulators have signaled support for technology-driven compliance approaches, with regulatory frameworks increasingly providing favorable treatment for insurers demonstrating robust digital compliance capabilities.

Category-wise Analysis

Component Type Insights

Software comprises the dominant segment within the Life Insurance Policy Administration Systems Market, representing platforms and applications specifically engineered for policy administration functionality including underwriting platforms, claims management systems, policy issuance modules, and customer relationship management (CRM) tools integrated within comprehensive administrative ecosystems. The 63.3% market share reflects the fundamental role of software as the operational core of policy administration infrastructure.

The persistent dominance of software reflects the sector's relentless demand for continuous functional enhancement and process optimization. Software-based solutions enable rapid deployment of new policy types, regulatory-responsive process modifications, and integration with emerging technologies (AI, advanced analytics, blockchain verification mechanisms). Enterprise insurers have demonstrated sustained preference for modern software platforms over legacy systems, justifying significant capital investment in software migration projects despite associated implementation complexities. The software segment's dominance is projected to sustain through the forecast period, driven by accelerating cloud-native architecture adoption and integration of artificial intelligence capabilities into core administrative software modules.

Services encompassing implementation, integration, customization, training, and ongoing technical support represent the fastest-growing segment within the Life Insurance Policy Administration Systems Market. As enterprise insurers undertake modernization initiatives particularly cloud migration and legacy system replacement service requirements expand dramatically. Implementation services alone required to configure software platforms for specific regulatory environments, policy types, and operational workflows represent substantial market value and expand proportionally with the complexity of deployed solutions.

Policy Type Insights

Term life insurance policies represent the largest policy type by administrative system utilization within the Life Insurance Policy Administration Systems Market, comprising 46.7% of market applications. Term life dominance reflects demographic preferences particularly in North America and Western Europe favoring term products due to cost efficiency and straightforward underwriting compared to permanent insurance alternatives. From a system administration perspective, term policies involve relatively standardized underwriting processes, clearly defined policy periods, and straightforward claims validation procedures, making them well-suited to systematic policy administration.

The term life insurance segment supports substantial policy administration system deployment in high-volume environments, where administrative efficiency and automated underwriting directly impact competitive profitability. Modern term insurance distribution increasingly emphasizes digital-native, rapid underwriting models requiring sophisticated automation within policy administration platforms. The segment's leadership position continues through the forecast period, though policy type diversity as identified in the fastest-growing segment analysis is increasing industry complexity.

Whole life insurance policies including permanent insurance variants such as universal life (UL) and variable universal life (VUL) products represent the fastest-growing policy type requiring Life Insurance Policy Administration Systems support. Whole life insurance policies involve substantially greater administrative complexity than term products: they feature multiple embedded options, dynamic cash value calculations, variable investment components, and extended policy duration requiring long-term administrative system viability.

Application Insights

Policy administration encompassing core policy issuance, renewal processing, change management, and ongoing policy servicing represents the dominant application segment, accounting for 38.7% of Life Insurance Policy Administration Systems market applications. This dominance reflects the foundational role of policy administration functionality; without robust policy administration capabilities, insurance enterprises cannot effectively issue policies, track policy status, manage policy modifications, or respond to customer inquiries regarding policy specifics.

The policy administration segment's leadership position reflects architectural realities: policy administration functionality is non-discretionary, operationally critical, and directly affects customer experience and regulatory compliance. Every policy administration system must address policy administration functionality; vendors differentiate through quality of implementation, user interface sophistication, integration capabilities, and automation levels. The segment's sustained dominance through 2033 reflects the inherent primacy of policy administration within insurance enterprise operations.

New business processing encompassing underwriting automation, risk assessment, policy illustration generation, and digital policy issuance represents the fastest-growing application segment within Life Insurance Policy Administration Systems deployments. This accelerating growth reflects the competitive criticality of underwriting speed and accuracy in modern insurance markets. Digital-native competitors have established competitive advantages through dramatically accelerated underwriting timelines, often reducing underwriting periods from weeks to hours through automated risk assessment and simplified health assessment processes.

Regional Insights and Trends

North America Market Trend

North America holds a leading position in the Global Life Insurance Policy Administration Systems Market with 35.6% regional share, reflecting mature insurance penetration, regulatory depth, and strong enterprise IT investment capabilities. The United States drives most of this demand due to its multi-layered insurance regulatory environment, high policyholder density, and well-developed carrier infrastructure. This environment supports continuous modernization cycles as insurers adjust to compliance, operational efficiency, and customer experience requirements.

Regulatory initiatives form a core structural demand driver across the region, with state-level insurance commissioners and federal policy coordination reinforcing compliance workloads. The NAIC Cybersecurity Initiative and 2025 regulatory priorities illustrate an environment where data protection oversight, anti-fraud controls, and customer protection standards elevate technology requirements for carriers. These dynamics encourage modernization of core policy systems as insurers adapt to multi-jurisdiction operational realities.

The regional competitive environment is relatively concentrated, featuring established global solution vendors and a growing insurtech ecosystem. Capital allocation trends show insurers prioritizing cloud migration, API modernization, and AI-enabled underwriting and claims modules, alongside compliance automation capabilities. Investment patterns highlight hybrid deployment preferences and modernization of legacy environments to remain competitive against digital-native insurance entrants targeting North American markets.

East Asia Market Trend

East Asia represents the fastest-expanding regional cluster within the Life Insurance Policy Administration Systems Market, accounting for 18% of global share and demonstrating structural momentum through 2033. China, Japan, and South Korea underpin this position through high insurance penetration trajectories, government-backed insurance awareness initiatives, and reduced legacy system burden relative to Western markets. This environment enables faster adoption of cloud-native, API-driven, and AI-integrated policy administration platforms.

Regional market characteristics differ materially from North American models due to digital-native distribution. Mobile-first insurance, fintech partnerships, and embedded insurance channels maintain higher proportional distribution relevance across East Asia, shaping technology platform design expectations. Regulatory frameworks continue maturing, with distinctions in data residency requirements, product illustration formats, and beneficiary processes, necessitating localized compliance modules rather than Western regulatory templates.

Key developments from 2023–2026 indicate accelerated digital insurance adoption, with major regional technology companies entering insurance distribution through mobile platforms, elevating service-level expectations. Completion of cloud regulatory standards and data localization frameworks has reduced barriers for cloud deployment, supporting broader system modernization. Insurance consolidation trends and rising middle-class participation further reinforce system implementation demand, supporting sustained policy administration platform adoption across East Asian markets.

Europe Market Trend

Europe holds 22% of the Global Life Insurance Policy Administration Systems Market, supported by mature insurance penetration and deeply developed regulatory frameworks. The region is shaped by the European Union’s Solvency II framework and emerging Solvency III discussions, which impose rigorous capital adequacy, reporting, and asset-liability management requirements. These mandates create sustained demand for advanced policy administration platforms capable of supporting regulatory reporting automation and actuarial data integration.

GDPR enforcement has further shaped platform architecture across Europe by imposing strict data-access, data-protection, and data-erasure requirements. Insurers have allocated significant investment to system modernization between 2022–2025 to ensure GDPR alignment and mitigate compliance risk. Anticipated adjustments to GDPR and the expanding influence of GDPR-style global regulations indicate continued compliance-driven modernization across European carriers and intermediaries.

The competitive environment includes both multinational vendors and regional insurance system specialists, creating a diverse solution ecosystem. European insurers have demonstrated strong investment activity in API-driven, modular architectures, allowing integration with specialist underwriting, claims, and regulatory reporting systems rather than pursuing monolithic platform transitions. Replacement cycles accelerated post-2022 as insurers recognized legacy systems’ limitations in satisfying Solvency II, GDPR, and customer communication requirements, reinforcing sustained technology procurement momentum through the forecast horizon.

Competitive Landscape

The Global Life Insurance Policy Administration Systems Market is consolidated in nature, with a limited number of established enterprise software and IT service providers controlling a large portion of commercial deployments. Leading companies such as Oracle Corporation, DXC Technology, SAP SE, Majesco, Sapiens International Corporation, and Accenture maintain competitive positions through comprehensive product suites, deep insurance expertise, and strong global service networks. Their platforms cover end-to-end policy lifecycle operations and integrate with compliance, billing, claims, and analytics systems used by major insurers.

Competitive dynamics are shaped by long-term contracts, high switching costs, and continuous modernization cycles, which collectively reinforce vendor stickiness and market stability across core insurance technology environments.

Key Industry Developments

- Dec 3, 2025, DXC Technology announced that Canadian insurer ivari completed a large-scale migration of 732,000 life insurance policies from Ingenium to the DXC Assure Platform on AWS, modernizing its core policy administration system. The cloud transition enabled 22% lower operating costs, launch of four new products, and improved scalability for digital distribution and customer experience. This marks a notable modernization milestone in cloud-enabled life insurance policy administration transformation.

- On June 17, 2025, Sapiens International Corporation released an AI-powered upgrade to its CoreSuite life insurance policy administration system, incorporating generative AI chatbots, machine learning-driven lead generation, predictive analytics, and enhanced migration tools to streamline operations and improve customer experience.

Companies Covered in Life Insurance Policy Administration Systems Market

- Oracle Corporation

- Accenture plc

- InsPro Technologies LLC

- Concentrix Corporation

- DXC Technology Company

- Infosys Limited

- SAP SE

- Capgemini SE

- Mphasis Wyde

- EXL

- Sapiens International Corporation

- Majesco

- Andesa Services

- FAST Technology

- Others.

Frequently Asked Questions

The global Life Insurance Policy Administration Systems Market is projected to be valued at US$ 6.8 Bn in 2026

The Software segment is expected to account for approximately 63.3% of the Global Life Insurance Policy Administration Systems Market by Component in 2026.

The market is expected to witness a CAGR of 12.2% from 2026 to 2033

Regulatory compliance mandates and insurance sector digitalization requirements driven by evolving oversight frameworks and cloud-AI technology adoption drive Life Insurance Policy Administration Systems market growth.

Key market opportunities include embedded insurance and digital-first distribution integration, along with RegTech-enabled compliance automation within API-driven, cloud-native policy administration platforms.

Key players in the Life Insurance Policy Administration Systems Market include Oracle Corporation, DXC Technology, SAP SE, Majesco, Sapiens International Corporation, and Accenture.