- Medical Devices

- Hearing Aids Market

Hearing Aids Market Size, Share, and Growth Forecast 2026 - 2033

Hearing Aids Market by Product Type (Behind-the-Ear (BTE), Receiver-in-the-Ear (RIE), In-the-Ear (ITE), In-the-Canal (ITC), Completely-in-the-Canal (CIC), Others), Technology (Conventional Hearing Aids, Digital Hearing Aids), Sales Channel (Pharmacy Stores, Audiology Clinics, Online Stores, Retail Stores, Others), and Regional Analysis, 2026 - 2033

Hearing Aids Market Share and Trends Analysis

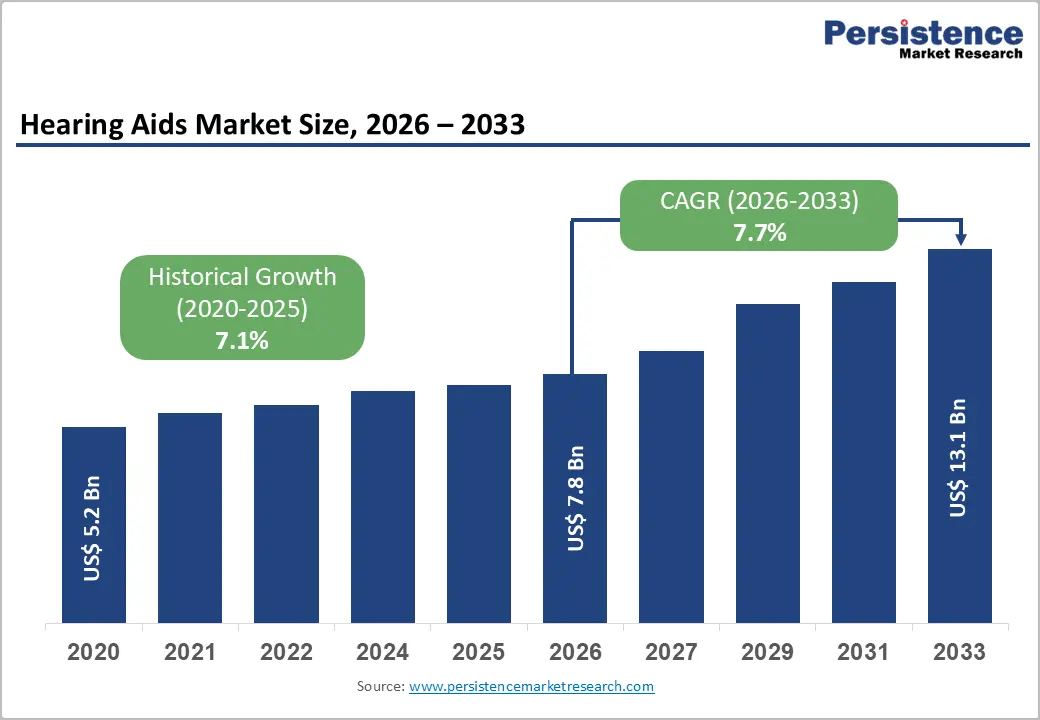

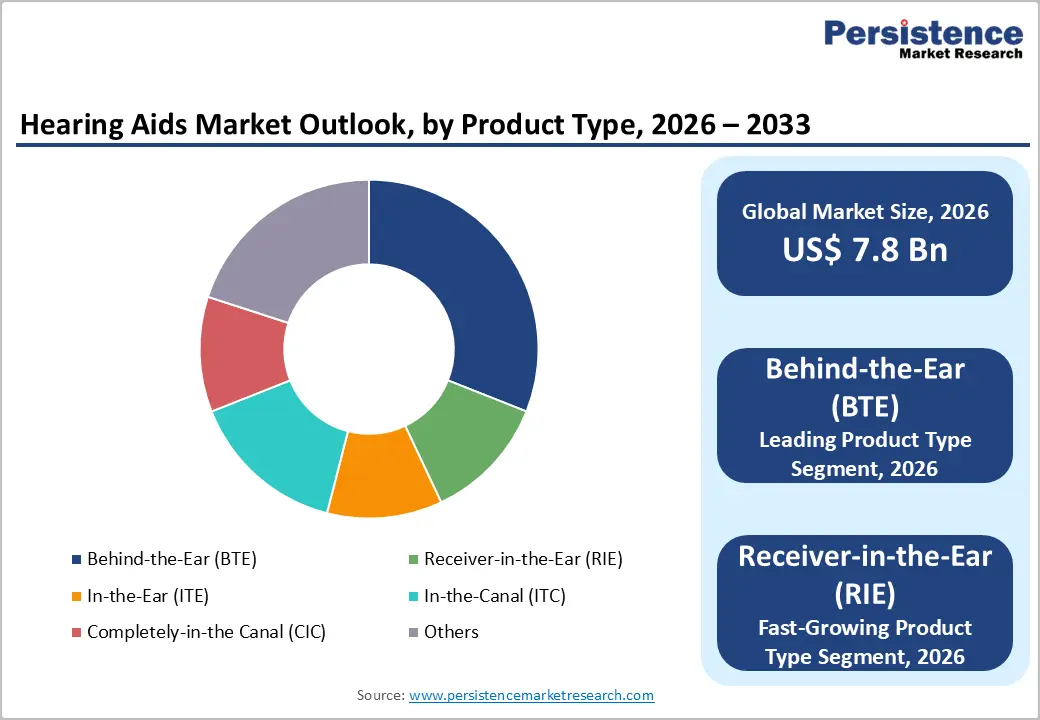

The global hearing aids market size is expected to be valued at US$ 7.8 billion in 2026 and projected to reach US$ 13.1 billion by 2033, growing at a CAGR of 7.7% between 2026 and 2033.

This expansion is primarily driven by the surging global prevalence of hearing loss, the accelerating adoption of advanced digital hearing aid platforms, and transformative regulatory changes that have democratized device access.

The World Health Organization (WHO) estimates that over 1.5 billion people worldwide live with some degree of hearing loss, with this figure projected to rise to 2.5 billion by 2050. From a base of US$ 5.2 billion in 2020, the market has grown at a historical CAGR of 7.1% through 2025, underscoring the consistent demand momentum entering the forecast period. The landmark FDA Over-the-Counter (OTC) Hearing Aid Rule of 2022 has further expanded the addressable consumer base by eliminating prescription barriers for adults with mild-to-moderate hearing loss in the United States.

Key Industry Highlights:

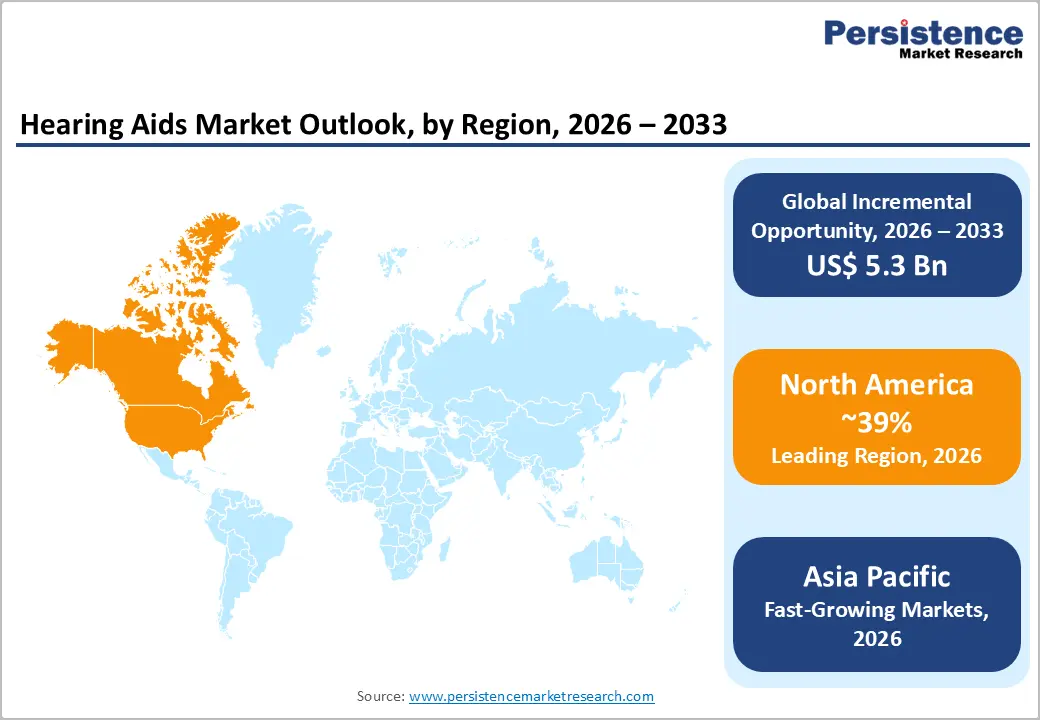

- Leading Region: North America leads the global hearing aids market with approximately 39% share in 2025, driven by the FDA OTC hearing aid rule, 4.4 million annual U.S. device dispensings, and expanding Medicare Advantage hearing benefit inclusion.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, fueled by China's 27.8 million hearing-impaired population with under 5% device penetration, India's NPPCD program, and rapidly expanding private audiology infrastructure across Southeast Asia.

- Dominant Segment: Behind-the-Ear (BTE) devices lead with 31% product type share in 2025, valued for their versatility across all severities of hearing loss, ease of handling for elderly users, and compatibility with high-power amplification platforms.

- Fastest Growing Segment: Receiver-in-the-Ear (RIE) is the fastest-growing product type, driven by AI sound processing integration, Bluetooth LE Audio connectivity, rechargeable battery adoption, and discreet aesthetics attracting a younger hearing aid user demographic.

Market Dynamics

Drivers - Surging Global Prevalence of Age-Related and Noise-Induced Hearing Loss

The global hearing loss burden is escalating at an unprecedented pace, creating a structural, long-term demand tailwind for hearing aid manufacturers. According to the WHO, approximately 430 million people currently require rehabilitation for disabling hearing loss, a figure concentrated disproportionately among older adults. With the global population aged 60 and above projected to double to 2.1 billion by 2050 (United Nations), age-related hearing loss (presbycusis) will drive substantial procedural and device demand.

Simultaneously, the WHO's Make Listening Safe initiative warns that approximately 1.1 billion young people aged 12-35 are at risk of noise-induced hearing loss from recreational sound exposure, broadening the demographic reach of hearing aid adoption beyond traditional older-adult markets.

OTC Hearing Aid Legislation and Expanding Market Access in the United States

The U.S. Food and Drug Administration (FDA)'s implementation of the Over-the-Counter Hearing Aid Rule in October 2022 represents the most significant regulatory shift in the hearing aid industry in decades. By enabling adults with perceived mild-to-moderate hearing loss to purchase hearing aids directly without a prescription, audiological exam, or fitting appointment, the rule has dramatically lowered cost and access barriers.

The President's Council of Advisors on Science and Technology (PCAST) estimated that OTC access could reduce the average cost of a hearing aid by as much as 90% compared to prescription channels. This policy change is expected to unlock millions of previously unserved consumers, stimulating intense competition in the consumer electronics and retail segments and driving overall market volume expansion.

Restraints - High Out-of-Pocket Costs and Limited Insurance Reimbursement

Despite the introduction of OTC options, premium prescription hearing aids remain costly, with prices ranging from US$ 1,000 to over US$ 7,000 per pair in the United States. Medicare, the primary payer for elderly Americans, has historically excluded hearing aid coverage, although the Hearing Loss Association of America (HLAA) continues to advocate for legislative reform. Globally, reimbursement inconsistency across national health systems constrains adoption in markets where out-of-pocket expenditure remains the primary financing mechanism, particularly in low- and middle-income countries where hearing loss prevalence is high, but device use remains critically low.

Social Stigma and Low Hearing Aid Adoption Rates Among Eligible Users

Despite widespread availability, hearing aid adoption rates among eligible individuals remain remarkably low. The WHO estimates that fewer than 17% of people who could benefit from a hearing aid actually use one. In the United States, the National Institute on Deafness and Other Communication Disorders (NIDCD) reports that among adults aged 70 and older with hearing loss, only about 30% have ever used a hearing aid. Persistent social stigma, denial of hearing loss, device discomfort, and a lack of awareness about available solutions continue to suppress market penetration, representing a structural challenge that manufacturers must address through consumer education and design innovation.

Opportunities - Receiver-in-the-Ear (RIE) Segment Growth Driven by Miniaturization and Connectivity

Receiver-in-the-Ear (RIE) hearing aids, also known as RITE or RIC (receiver-in-canal) devices, represent the fastest-growing product segment, driven by their superior combination of acoustic performance, discreet form factor, and wireless connectivity features. The integration of Bluetooth Low Energy (BLE) and Made for iPhone (MFi) protocols allows RIE devices to stream audio directly from smartphones, televisions, and other devices, significantly improving the user experience for tech-savvy consumers.

Leading manufacturers, including Sonova Holding AG and GN Hearing, have invested heavily in AI-powered sound processing algorithms for their RIE platforms. The American Academy of Audiology (AAA) reports that RIE/RITE styles now represent the majority of new hearing aid fittings in clinical settings, a trend expected to continue through 2033 as connectivity demands escalate.

Artificial Intelligence and Rechargeable Platform Innovation

The integration of artificial intelligence (AI) and machine learning into hearing aid sound processing represents a transformative opportunity for premium product differentiation. AI-powered hearing aids can adapt to acoustic environments in real time, distinguishing speech from background noise, recognizing sound scenes, and personalizing amplification profiles, delivering substantially improved speech intelligibility compared to traditional digital signal processing. Starkey Laboratories's Genesis AI platform and Demant A/S's Oticon Intent exemplify this trend.

Simultaneously, the transition to rechargeable lithium-ion battery platforms, eliminating the need for disposable zinc-air batteries, is improving device convenience and sustainability appeal, with Sonova reporting that rechargeable models now account for the majority of its premium device sales. These twin innovations are commanding higher average selling prices and driving market value expansion.

Category-wise Analysis

Product Type Insights

Behind-the-Ear (BTE) hearing aids hold the leading position in the product type category, commanding approximately 31% of the global hearing aids market in 2026. BTE devices sit behind the ear and deliver amplified sound through a tube connected to an ear mold or dome, making them suitable for a broad spectrum of hearing loss severities from mild to profound. Their versatility, ease of handling, and compatibility with assistive listening devices make them particularly well-suited for pediatric patients and elderly users with dexterity limitations.

According to the American Speech-Language-Hearing Association (ASHA), BTE devices are the most widely prescribed style globally due to their robustness and ability to accommodate powerful amplification levels. The availability of BTE models across a wide price spectrum, from basic analog devices to premium AI-powered rechargeable platforms, further underpins segment leadership.

Technology Insights

Digital hearing aids constitute the dominant technology segment, representing approximately 90% of global hearing aid sales in 2026. Digital signal processing (DSP) technology enables sophisticated sound customization, noise reduction, feedback suppression, and directional microphone functionality that conventional analog devices cannot replicate.

The National Institute on Deafness and Other Communication Disorders (NIDCD) notes that virtually all hearing aids sold today in developed markets are digital, with ongoing innovation focused on AI-enhanced processing, direct audio streaming, and over-the-air (OTA) firmware updates enabling remote fine-tuning by audiologists. The near-complete transition to digital technology in developed markets, combined with accelerating digital adoption in emerging markets, ensures the segment's sustained dominance through the forecast period.

Sales Channel Insights

Audiology clinics represent the leading sales channel, accounting for approximately 45% of global hearing aid revenue in 2026. Audiologists serve as the primary point of contact for hearing loss diagnosis, hearing aid fitting, and post-purchase follow-up care, ensuring that clinics capture a disproportionate share of premium device sales. The personalized fitting and programming services provided at audiology clinics command significant added-value revenue, typically bundled into total device pricing.

Leading networks such as Demant A/S's Hearing Care Alliance and Sonova's AudioNova operate thousands of clinics globally, creating vertically integrated distribution moats. However, the FDA OTC rule is accelerating online and retail channel growth, gradually eroding the clinic channel's dominant share among mild-to-moderate hearing loss consumers.

Regional Insights

North America Hearing Aids Market Trends and Insights

North America leads the global hearing aids market with approximately 39% of total revenue in 2025, driven by high awareness of hearing health, widespread audiologist infrastructure, and the catalytic impact of the FDA's OTC hearing aid regulations. The region is witnessing rapid growth of direct-to-consumer retail and online channels as technology companies, including Apple, Samsung, and Bose, enter the self-fitting hearing assistance device segment.

U.S. Hearing Aids Market Size

The United States accounts for over 87% of the North American market revenue, with approximately 4.4 million hearing aids dispensed annually, according to the Hearing Industries Association (HIA). The OTC reform is projected to expand the addressable market by millions of new first-time users, while rising Medicare Advantage plan inclusion of hearing benefits is improving access for the 65+ demographic.

Europe Hearing Aids Market Trends and Insights

Europe is the second-largest hearing aids market, characterized by strong public reimbursement frameworks, established audiology clinic networks, and high penetration of premium digital devices. Scandinavian countries and Germany lead in per-capita hearing aid adoption due to generous statutory reimbursement. European manufacturers, including Demant A/S, Sonova, WS Audiology, and GN Hearing, maintain global R&D leadership from their European headquarters, shaping worldwide product innovation roadmaps.

Germany Hearing Aids Market Size

Germany is Europe's largest hearing aid market, representing approximately 22% of regional revenue. The statutory health insurance system (GKV) provides hearing aid reimbursement of up to €784.94 per ear for standard devices, ensuring high utilization rates. Over 3.7 million hearing aids are dispensed annually in Germany, making it one of the world's highest-volume markets and a bellwether for European adoption trends.

U.K. Hearing Aids Market Size

The United Kingdom represents approximately 14% of the European hearing aids market revenue. The National Health Service (NHS) provides free BTE hearing aids to eligible patients, supporting high-volume dispensing. The Action on Hearing Loss (RNID) reports over 12 million people in the UK are affected by hearing loss, with growing demand for premium private-pay devices driving a parallel commercial market alongside NHS provision.

Asia Pacific Hearing Aids Market Trends and Insights

Asia Pacific is the fastest-growing regional market, propelled by a massive and underpenetrated hearing loss population, rapidly improving healthcare infrastructure, and rising middle-class disposable incomes. China is the region's dominant national market, with the China Disabled Persons' Federation reporting over 27.8 million people with hearing disabilities, yet hearing aid penetration rates remain below 5%, signaling vast untapped demand. Government-led subsidized hearing aid programs and expanding domestic manufacturing are accelerating regional adoption.

India Hearing Aids Market Size

India represents approximately 9% of the Asia Pacific hearing aids market revenue. The National Programme for Prevention and Control of Deafness (NPPCD) under the Ministry of Health provides free hearing aids to below-poverty-line beneficiaries, while Ayushman Bharat coverage is expanding private hospital audiology services. India's large young-adult population at risk of noise-induced hearing loss is emerging as an incremental demand segment.

Competitive Landscape

The hearing aids market is highly competitive, driven by continuous innovation in digital sound processing, wireless connectivity, rechargeable batteries, and AI-enabled hearing solutions. Companies focus on developing discreet, comfortable, and high-performance devices that improve speech clarity and user convenience. Strategic collaborations with audiology clinics, hospitals, and retail hearing centers strengthen distribution networks and customer reach. Expansion into emerging markets, rising adoption of over-the-counter hearing aids, and increasing demand from the aging population further intensify competition.

Key Developments:

- In April 2026, Oticon launched the Verit hearing aid family, a new premium range of zinc-air battery-powered hearing aids designed for users who preferred disposable batteries over rechargeable options.

- In March 2026, GN launched the expanded “New Norm Vol. 2” image library to address the lack of representation of people with hearing loss in mainstream media.

- In September 2025, Audien Hearing launched the Atom X, the world’s first touchscreen-controlled over-the-counter hearing aid, designed to simplify hearing aid usage and improve accessibility.

Hearing Aids Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.2 billion |

| Current Market Value (2026) | US$ 7.8 billion |

| Projected Market Value (2033) | US$ 13.1 billion |

| CAGR (2026 - 2033) | 7.7% |

| Leading Region | North America, 39% market share (2025) |

| Dominant Category (Product Type) | Behind-the-Ear (BTE), 31% market share (2025) |

| Top-ranking Category (Technology) | Digital Hearing Aids, 90% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 5.3 billion |

Companies Covered in Hearing Aids Market

- Audina Hearing Instruments

- Starkey Laboratories, Inc.

- Demant A/S

- BHM-Tech Produktionsgesellschaft GmbH

- GN Hearing

- Microson

- Sonova Holding AG

- WS Audiology A/S

- Horentek Hearing Diagnostics

- Cochlear Ltd.

Frequently Asked Questions

The global hearing aids market is valued at US$ 7.8 billion in 2026.

The primary demand drivers are the rapidly escalating global burden of hearing loss projected to affect 2.5 billion people by 2050 (WHO) the FDA's landmark OTC Hearing Aid Rule (2022), eliminating prescription barriers in the U.S., and the AI and Bluetooth LE Audio technology revolution in hearing aid devices.

North America is the leading region with approximately 39% of the global market share in 2025. The United States dominates, accounting for the bulk of North American revenue with approximately 4.4 million annual device dispensings (Hearing Industries Association). The FDA OTC reform, expanding Medicare Advantage hearing benefits, and strong audiologist infrastructure collectively underpin North America's market leadership.

The integration of AI-powered neural processing chips and Bluetooth LE Audio (Auracast) connectivity in next-generation hearing aids represents the most transformative commercial opportunity, enabling premium pricing and expanding appeal to tech-savvy users.

The global hearing aids market is led by a concentrated group of European and American manufacturers. Key players include Sonova Holding AG (Phonak, Unitron), Demant A/S (Oticon, Bernafon), WS Audiology A/S (Signia, Widex), GN Hearing (ReSound), Starkey Laboratories, Cochlear Ltd., Audina Hearing Instruments, and BHM-Tech Produktionsgesellschaft GmbH.