- Processed Food

- Seafood Market

Seafood Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Seafood Market By Product Type (Fish, Crustaceans, Mollusks, Others), Form (Fresh/Live, Frozen, Canned, Dried, Others), Source (Wild-caught, Farmed/Aquaculture), and by Regional Analysis, 2026-2033

Seafood Market Share and Trends Analysis

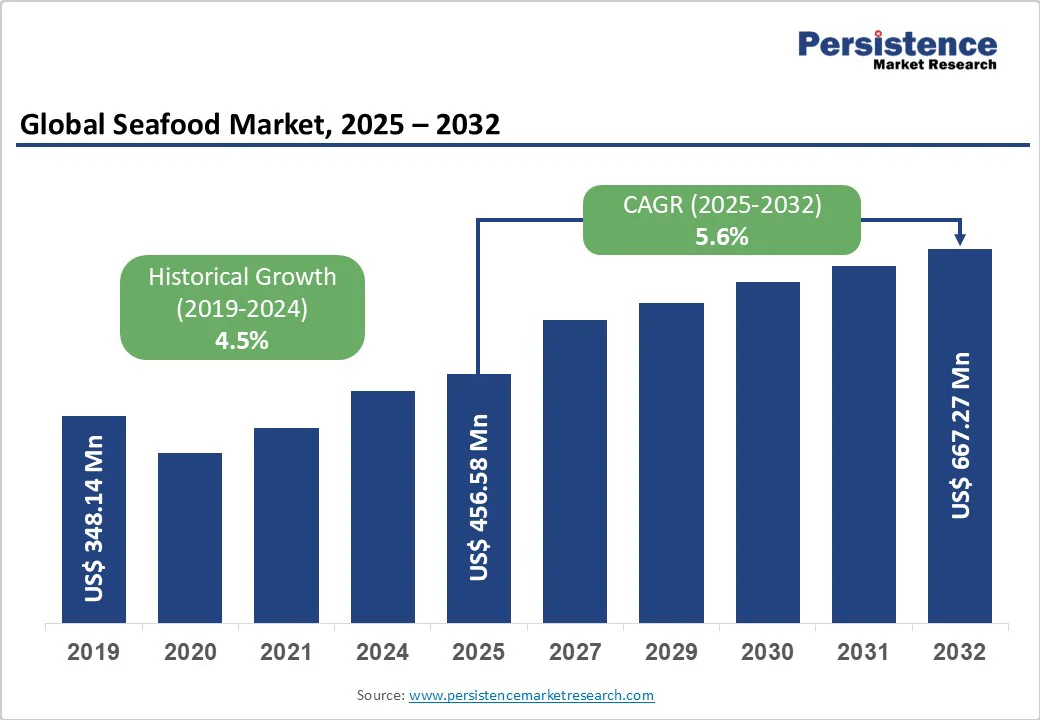

The global Seafood Market is expected to be valued at US$ 409.1 billion in 2026 and projected to reach US$ 611.1 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033

Global seafood markets are being reshaped by technology, sustainability mandates, and shifting protein consumption patterns. From AI-powered aquaculture to value-added convenience formats, competitive intensity is accelerating across regions and categories.

Key Industry Highlights

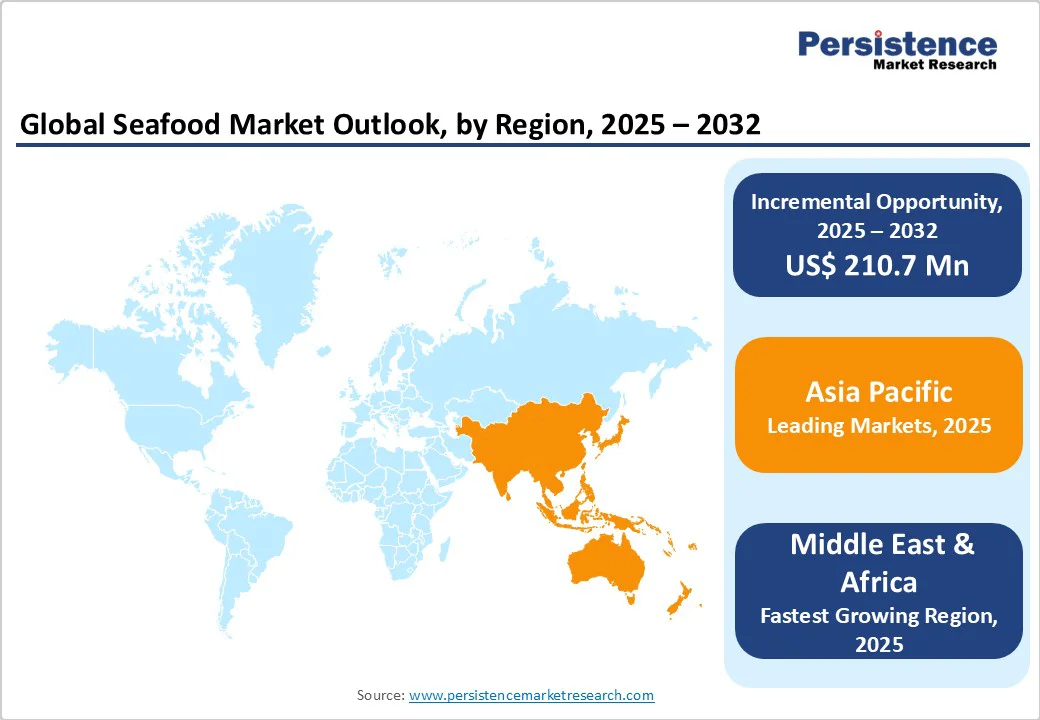

- Leading Region: Asia Pacific, accounting for approximately 43% market share in 2025, driven by deep-rooted seafood consumption culture, large-scale aquaculture output, rising middle-class demand, and strong export-oriented processing ecosystems.

- Fastest-Growing Product Type Segment: Crustaceans, projected to expand rapidly due to premium pricing power, rising global appetite for shrimp and lobster, and aquaculture expansion across Asia Pacific and Latin America.

- Market Drivers: Adoption of smart aquaculture technologies, AI-enabled feeding systems, traceability tools, and sustainability certifications strengthening productivity, risk mitigation, and premium market access.

- Opportunities: Expansion of ready-to-cook, frozen, and value-added processed seafood formats targeting urban consumers seeking convenience, health, and longer shelf life.

- Key Developments: In January 2026, Maruha Nichiro announced its corporate rebranding to Umios effective March 1, 2026. In November 2025, Atlantic Fish Co. raised US$1.2 million to advance cultivated whitefish and pursue U.S. regulatory approval.

| Key Insights | Details |

|---|---|

| Global Seafood Market Size (2026E) | US$ 409.1 Bn |

| Market Value Forecast (2033F) | US$ 611.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Driver – Rise of Smart Aquaculture and Technological Integration

The seafood industry is experiencing transformative growth through the integration of smart aquaculture technologies, which optimize productivity while enhancing sustainability. Industry leaders such as Cermaq and Grieg Seafood are deploying AI-enabled feeding systems, real-time water quality monitoring, and precision harvesting to stabilize output and minimize ecological impact.

These innovations are critical as climatic events such as El Niño disrupt traditional supply chains by altering ocean conditions and fish migration patterns, causing production volatility. Smart aquaculture helps mitigate such risks by enabling proactive health management and environmental control, reducing yield unpredictability. Sustainability-aligned technologies attract premium markets valuing traceability and eco-certifications.

Restraints – Supply Chain Disruptions from Climatic and Geopolitical Instability

Structural challenges in seafood supply chains are intensifying due to climate variability and geopolitical tensions, which impose operational risks and cost barriers on producers and exporters. Elevated ocean temperatures disrupt breeding and growth cycles, leading to decreased export volumes and increased price volatility.

Tariffs in key import markets such as the U.S. are inflating costs for major exporters such as Vietnam and India, potentially suppressing demand and forcing market realignments. These disruptions undermine supply chain predictability, increasing dependence on costly technology and diversification strategies to maintain volume and quality.

Consequently, industry participants face heightened risk exposure that demands adaptive investment in supply chain resilience, price risk management, and regulatory navigation to sustain competitive positioning.

Opportunity – Growth in Ready-to-Cook and Convenience Seafood Products

Increasing consumer demand for convenience foods amid urbanization and busy lifestyles presents a lucrative growth opportunity within processed seafood formats such as frozen, canned, and ready-to-cook products. Advancements in food processing technologies and cold chain infrastructure are enabling longer shelf life and preservation of nutritional quality, aligning well with millennials and working populations seeking healthy yet time-efficient meal options.

The processed seafood segment is expanding rapidly, supported by product innovation exemplified by flavored canned tuna and unique frozen offerings that cater to evolving tastes. Capitalizing on this trend through strategic product development and distribution channel expansion can capture unmet consumer needs while diversifying revenue streams.

Category-wise Analysis

Product Type Insights

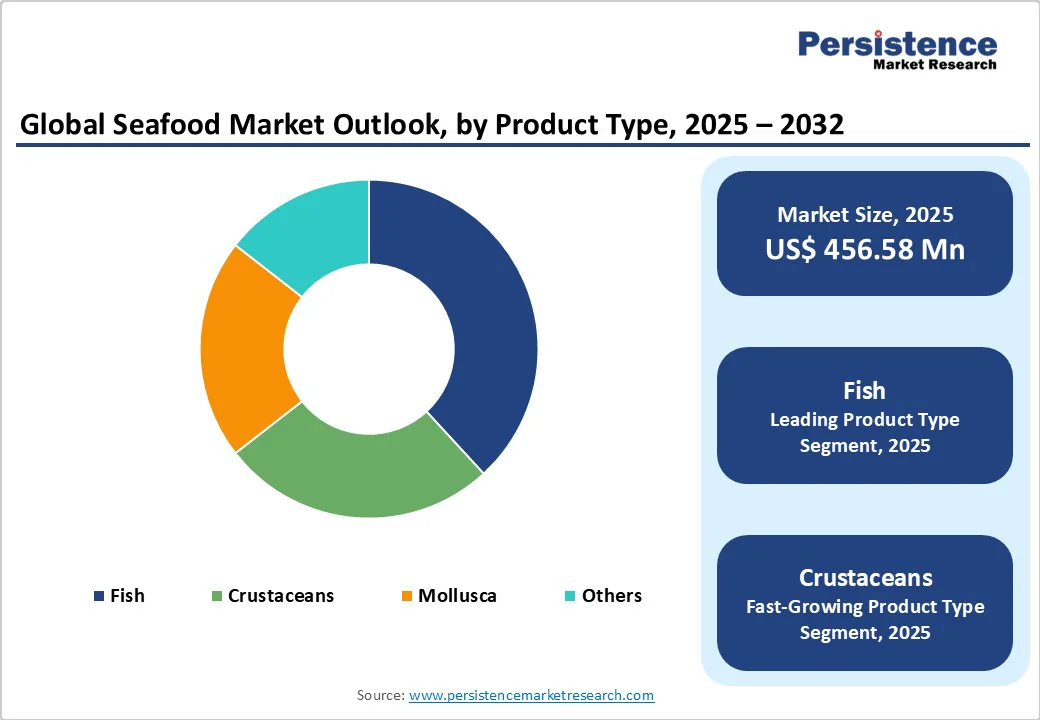

Fish remains the cornerstone of the market, accounting for an estimated 46% market share in 2025 due to its nutritional profile, versatile culinary uses, and established supply ecosystems. Varieties such as salmon, tuna, and cod lead in revenue contribution, supported by both traditional wild-caught fisheries and increasingly sophisticated aquaculture operations. This segment benefits from broad consumer awareness of health benefits, including omega-3 fatty acids, driving steady demand within both retail and foodservice channels.

Crustaceans are emerging as the dynamic growth engine, expected to register a robust CAGR of approximately 7.2% through 2033. Drivers for this segment include increasing consumer preference for shellfish in gourmet and casual dining, coupled with expanded aquaculture farming of shrimp and lobster in Asia Pacific and Latin America.

Premium pricing and the rising global middle class’s affinity for luxury seafood dishes underpin this segment’s accelerated trajectory. Economic growth in emerging markets is anticipated to further solidify the position of crustaceans, creating lucrative opportunities for exporters and processors.

Form Analysis

Fresh seafood is likely to dominate with around 61% of the revenue share in 2025, reflecting consumer preference for natural flavor, superior texture, and higher perceived nutritional value. The market leadership of this segment is reinforced by expanding cold chain infrastructure, especially in developed economies, which preserves freshness across distribution networks.

Processed seafood, including frozen, canned, and ready-to-cook formats, is the fastest-growing form segment from 2026 to 2033. This growth is driven by the massive scale of urbanization, increasingly busy lifestyles, and technological improvements in packaging and preservation that extend product shelf life without compromising quality. Accelerating demand among millennials and Gen Z consumers for convenience foods underpins this trend, prompting seafood producers to innovate product portfolios.

Region-wise Insights

North America Seafood Market Trends and Insights

North America is expected to command an estimated 18.5% of the seafood market share in 2025, predominantly driven by the U.S., which represents over 72% of regional consumption. Market growth in this region is supported by a robust innovation ecosystem emphasizing sustainable practices, traceability, and premiumization, alongside increased consumer engagement with the health functionalities of seafood proteins.

Regulatory enforcement by bodies such as the U.S. Food and Drug Administration (FDA) and the National Oceanic and Atmospheric Administration (NOAA), guiding product safety, import standards, and environmental conservation, though these factors also elevate compliance complexity and costs for businesses.

E-commerce and direct-to-consumer models are expanding rapidly, enhancing accessibility. The seafood market in North America is forecasted to grow at a CAGR of approximately 5.1% from 2026 to 2033, driven by increasing demand for diversified seafood formats and sustainability credentials. Investments are also channeled into aquaculture technologies and cold chain improvement to manage supply chain risks.

Europe Seafood Market Trends and Insights

From North Sea trawlers to Mediterranean fish counters, Europe’s seafood market is being reshaped by sustainability, premiumization, and shifting protein preferences. In the UK, retailers are expanding chilled ready-to-cook seafood lines and investing in traceability tools to reassure post-Brexit consumers. France continues to value fresh fish through traditional markets, while demand for responsibly sourced shellfish and Label Rouge-certified products strengthens premium positioning. Germany’s market shows steady growth in frozen and convenience seafood, reflecting busy urban lifestyles and rising flexitarian diets. In Spain, high per capita seafood consumption sustains strong demand for cephalopods and canned tuna, while Italy is witnessing renewed interest in regional species and aquaculture-backed sea bream and sea bass.

Policy modernization is reinforcing these structural shifts. The European Commission has proposed a new regulation to simplify and streamline the collection of fisheries and aquaculture statistics in the EU, aiming to improve data consistency and evidence-based stock management. This regulatory push supports transparency, sustainability benchmarking, and long-term resource planning across member states.

Asia Pacific Seafood Market Trends and Insights

Asia Pacific leads the global seafood market in 2025 with an estimated 43% share, supported by strong consumption across China, Japan, India, and ASEAN economies. Deep-rooted seafood traditions, accelerating urbanization, and rising household incomes continue to stimulate both fresh and processed seafood demand. Expanding retail infrastructure and e-commerce penetration further strengthen regional distribution networks.

The region’s dominance is reinforced by its aquaculture scale, contributing more than 60% of global aquaculture output, largely driven by China and Vietnam. India is also emerging as a strategic powerhouse; as per IBEF, India is the second largest fish producing nation globally, accounting for 8% of total world fish production and generating 58 lakh employment opportunities as of December 2024. Cost-efficient processing, supportive export policies, and government-backed modernization initiatives are attracting sustained investments. Growing middle-class preference for convenient, protein-rich seafood, alongside tightening food safety and sustainability regulations, is accelerating innovation, traceability adoption, and value-added product expansion across the region.

Market Competitive Landscape

The global seafood market is moderately fragmented, with multinational processors competing alongside strong regional exporters and aquaculture specialists. Leading companies are expanding vertically through hatcheries, feed mills, and advanced processing facilities to secure traceability and margin control. Rapid aquaculture growth is reshaping supply, while tighter regulations on deep-sea fishing and quotas aim to protect endangered species such as bluefin tuna and certain shark varieties. Certifications including MSC and ASC are becoming commercial necessities as retailers demand verified sourcing standards.

Strategic collaborations between seafood firms, technology providers, and retailers are accelerating innovation across farming and distribution. AI-enabled monitoring systems are being deployed in aquaculture to optimize feed conversion, detect disease early, and improve yield predictability. Companies are investing in value-added processing hubs and shifting toward recyclable, low-impact packaging formats. Direct-to-consumer channels and online retail platforms are expanding market reach, allowing brands to build transparency narratives, premium positioning, and stronger consumer loyalty worldwide.

Key Developments:

- In January 2026, Japanese seafood major Maruha Nichiro announced it will change its corporate name to Umios effective March 1, 2026, marking a significant brand transformation aligned with its long-term growth vision and global positioning strategy.

- In November 2025, Atlantic Fish Co., a U.S.-based food tech startup, raised US$1.2 Million to develop cultivated whitefish, enhance fillet quality, and pursue U.S. regulatory approval, addressing overfishing, sustainability, and climate challenges in the US$400 Billion seafood market.

- In October 2025, Highland Group, in partnership with Lulu Group, launched its exclusive seafood brand Aqua Fair and shipped the first consignment of premium shrimp to Lulu retail outlets across the Middle East.

Companies Covered in Seafood Market

- Mowi ASA

- Nippon Suisan Kaisha Ltd (Nissui)

- Maruha Nichiro Corporation

- Thai Union Group

- Cermaq Group AS

- Grieg Seafood ASA

- Bumble Bee Foods LLC

- SalMar ASA

- Dongwon Industries Co., Ltd.

- Faroe Seafood Company

- Clearwater Seafoods

- Cooke Aquaculture Inc.

- Ocean Choice International

- High Liner Foods Inc.

- Pacific Seafood Group

- Others

Frequently Asked Questions

The global Seafood market is projected to be valued at US$ 409.1 Bn in 2026.

Rise of Smart Aquaculture and Technological Integration is a major factor driving global seafood market.

The Global Seafood market is poised to witness a CAGR of 5.9% between 2026 and 2033

Expansion of Ready-to-Cook and Value-Added Convenience Seafood Product represents a significant market opportunity for companies in the seafood market.

Major players in the Global Seafood market include Mowi ASA, Nippon Suisan Kaisha Ltd (Nissui), Maruha Nichiro Corporation, Thai Union Group, SalMar ASA, Dongwon Industries Co., Ltd., Cooke Aquaculture Inc., Clearwater Seafoods, and others