- Telecommunications

- Telecom Tower Market

Telecom Tower Market Size, Share, and Growth Forecast, 2025 - 2032

Telecom Tower Market by Tower Type (Lattice tower, Guyed tower, Monopole tower, Camouflage towers, Mobile (vehicle-mounted) tower), Installation (Rooftop, Ground-based), Fuel (Renewable, Non-Renewable), and Regional Analysis for 2025 - 2032

Telecom Tower Market Size and Trends Analysis

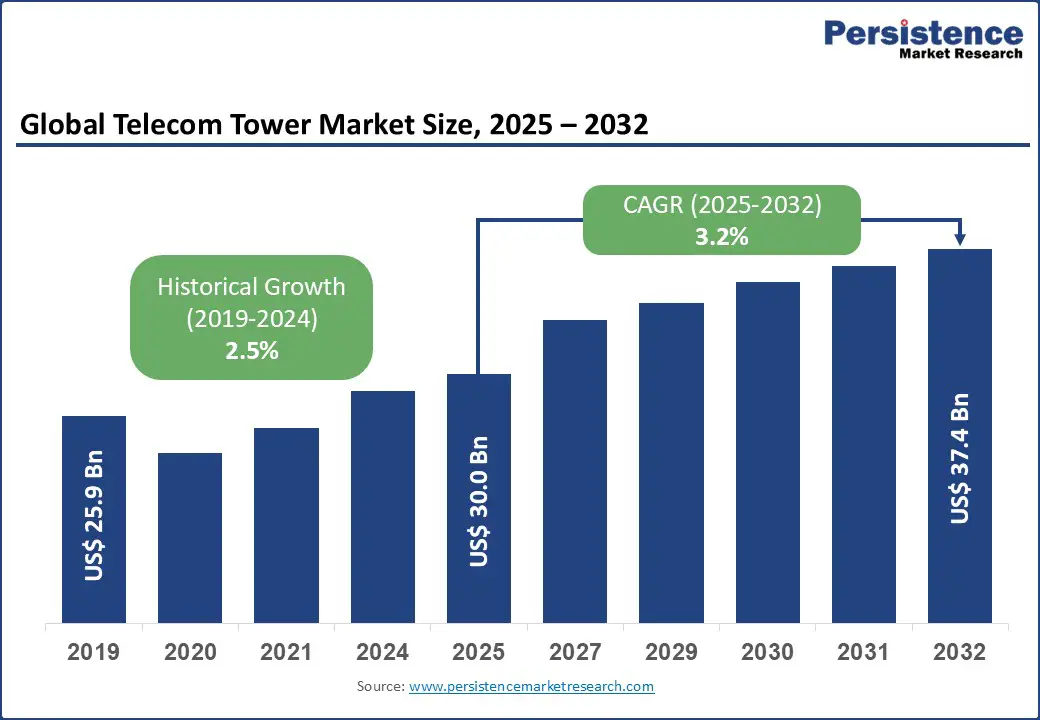

The global telecom tower market size is likely to be valued at US$30.0 Bn in 2025 and is expected to reach US$37.4 Bn by 2032, registering a CAGR of 3.2% during the forecast period from 2025 to 2032.

The telecom tower market has experienced robust growth, driven by the rising demand for enhanced mobile connectivity, advancements in 5G network technologies, and the increasing need for reliable telecommunications infrastructure. The industry expansion is further supported by global efforts to bridge digital divides and improve connectivity, particularly in the Asia Pacific, which leads the industry.

Key Industry Highlights:

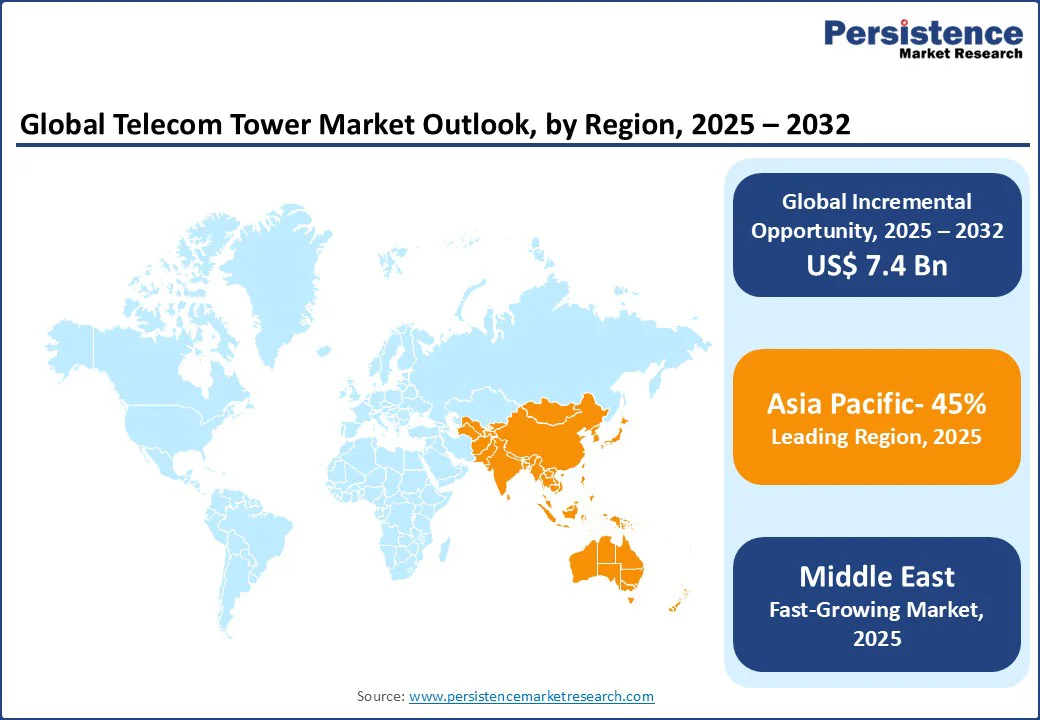

- Leading Region: Asia Pacific holds a 45% market share in 2025, driven by expansive telecommunications infrastructure, high mobile penetration rates, and widespread adoption of 5G technologies.

- Fastest-growing Region: Middle East, propelled by increasing investments in digital infrastructure, smart city initiatives, and expanding telecom facilities in countries such as Saudi Arabia and the UAE.

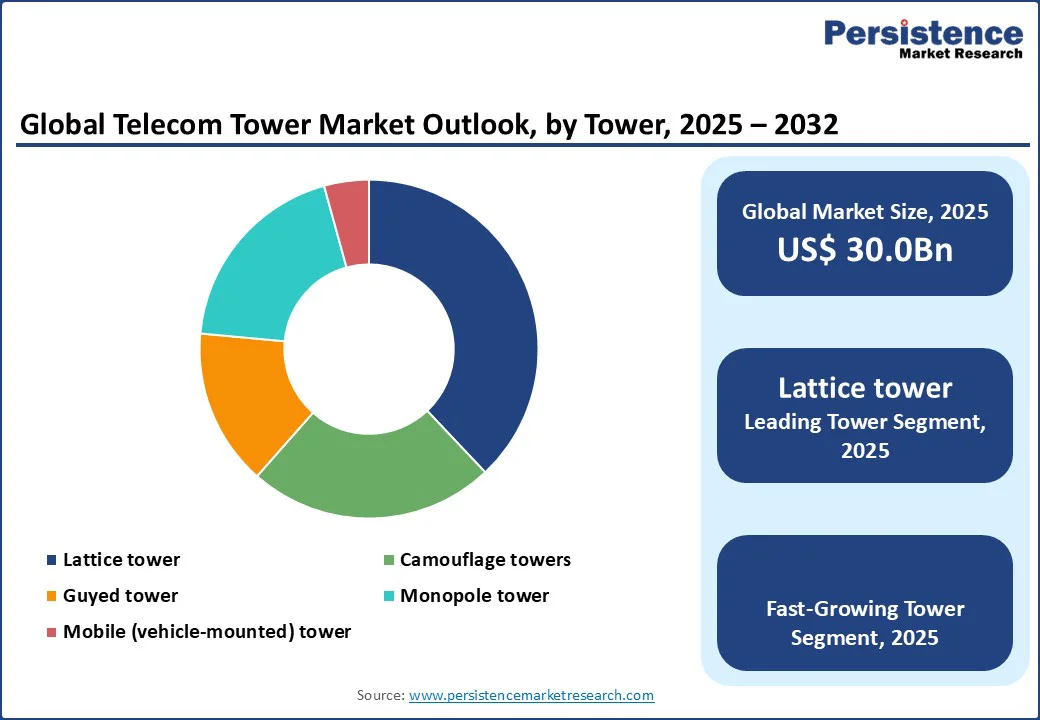

- Dominant Tower Type: Lattice tower accounts for approximately 35.5% of the telecom tower market share in 2025, driven by its cost-effective production.

- Leading Installation: Ground-based leads with a 38% share, reflecting its widespread use in rural and expansive network settings.

| Key Insights | Details |

|---|---|

| Telecom Tower Market Size (2025E) | US$30.0 Bn |

| Market Value Forecast (2032F) | US$37.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.5% |

Market Dynamics

Driver - Global Surge in Telecommunications Demand

The global surge in telecommunications demand is a primary driver of the telecom tower market. According to the International Telecommunication Union (ITU), it is estimated that approximately 5.5 Bn people, or 68 per cent of the world’s population, are using the Internet in 2024, with data traffic increasing by over 50% annually due to streaming, IoT applications, and remote work trends.

This rising demand, particularly in regions with high population density and digital transformation initiatives, underscores the need for robust telecom towers, which provide essential infrastructure for signal transmission and network coverage.

The rollout of 5G networks, requiring denser tower deployments to support higher frequencies and lower latency, has led to significant investments in tower infrastructure. For instance, in the Asia Pacific, government programs such as India’s Digital India and China’s 5G Action Plan are accelerating tower installations to achieve nationwide coverage, with China expected to deploy over one Mn new towers by mid-decade.

The proliferation of smartphones is projected to exceed several billion units globally by the same period, further amplifying the need for expanded tower networks to handle the huge bandwidth requirements. The COVID-19 pandemic underscored the importance of reliable connectivity for education, healthcare, and business continuity, prompting accelerated deployments.

In the Middle East, Saudi Arabia’s Vision and the UAE’s smart city initiatives drive tower growth to support IoT and 5G applications. Environmental considerations are also gaining traction, with operators adopting energy-efficient towers to reduce operational costs, particularly through hybrid power systems integrating renewables.

Restraint - High Costs and Regulatory Approval Requirements Restrict Adoption

High capital expenditures and regulatory hurdles pose significant restraints to the industry. Constructing a single tower can be very costly, depending on type and location, with additional ongoing expenses for site leasing, power supply, and compliance with safety standards. In urban areas, land acquisition and zoning permits often delay projects by months or even years, increasing costs.

Regulatory challenges, such as environmental impact assessments and community opposition to tower aesthetics, further complicate deployments. For example, strict height restrictions and electromagnetic field (EMF) emission regulations in regions such as the Middle East and Europe can lead to project cancellations or redesigns, substantially inflating costs.

In emerging markets, inadequate infrastructure, such as unreliable power grids or poor road access, makes rural expansion challenging. The transition to 5G requires retrofitting existing towers, demanding skilled labor and specialized equipment, which are often scarce.

Economic uncertainties, including fluctuating prices for steel and concrete, add to the financial burden. These restraints disproportionately affect smaller operators and new entrants, limiting market entry and slowing growth despite strong demand.

Opportunity - Innovation in Sustainable Systems and Multi-Tenant Use Boosts Consumption

The telecom tower market presents significant opportunities through innovations in sustainable and multi-tenant tower designs. The push for green energy solutions, such as solar-powered towers, reduces dependency on diesel generators, which contribute substantially to operational costs in remote areas.

Integrating renewable fuels such as solar and wind aligns with global sustainability goals under the Paris Agreement, lowering carbon emissions and operational expenses. Multi-tenant models, where multiple operators share a single tower, optimize resource utilization and can significantly cut construction costs, particularly in urban areas with limited space.

Emerging technologies such as small cells and distributed antenna systems (DAS) enable denser networks without requiring large towers, creating new growth avenues. In underserved regions, government subsidies and public-private partnerships, such as those under Saudi Arabia’s Vision, encourage tower deployments to bridge digital divides.

The rise of edge computing and IoT applications demands localized towers, boosting demand for mobile and camouflage designs. Strategic mergers among tower companies enhance efficiency by consolidating assets. These opportunities are poised to drive market expansion by addressing environmental and cost concerns, fostering long-term growth through the next decade.

Category-wise Analysis

Tower Type Insights

The global telecom tower market is segmented into lattice tower, guyed tower, monopole tower, camouflage towers, and mobile (vehicle-mounted) tower. Lattice tower dominates, holding approximately 35.5% share in 2025, due to its cost-effective production and scalability for high-capacity and rural applications.

Camouflage towers emerged as the fastest-growing segment, fueled by rising demand for aesthetically pleasing and discreet structures in urban areas and regulated environments. Their design blends with the surroundings, minimizing visual impact while supporting efficient network expansion and enhanced connectivity.

Installation Insights

The global telecom tower market is segmented into rooftop and ground-based towers. Ground-based leads with a 38% share in 2025, driven by its widespread use in expansive and rural network settings, supporting wide coverage and reliable connectivity.

Rooftop towers are the fastest-growing segment, propelled by their ability to maximize limited urban space and reduce land acquisition costs. This efficiency allows operators to rapidly expand network coverage, deploy infrastructure more economically, and meet rising connectivity demands in densely populated areas.

Fuel Insights

The telecom tower market is segmented into renewable and non-renewable power sources. Non-renewable dominates with a 55% share in 2025, driven by its critical role in providing a reliable power supply for remote locations and ensuring uninterrupted network operations.

Renewable power towers are the fastest-growing segment, driven by sustainability initiatives and the potential for significant energy cost savings. Adoption of solar, wind, and hybrid systems enables operators to reduce carbon emissions while lowering operational expenses and supporting green infrastructure goals.

Regional Insights

Asia Pacific Telecom Tower Market Trends

Asia Pacific dominates the global telecom tower market, expected to account for 45% of market share in 2025, riven by rapid urbanization, widespread mobile adoption, and substantial investments in 5G infrastructure across key countries such as China and India.

In China, government initiatives such as the national five-year development plan prioritize comprehensive 5G network coverage, resulting in massive tower deployments to support high-speed connectivity and advanced digital services. India’s rural connectivity programs, including initiatives to expand broadband access, are significantly increasing telecom tower installations, ensuring that even remote areas gain reliable network coverage.

Countries such as Japan and South Korea are at the forefront of advanced telecommunications technologies, propelled by strong adoption of IoT applications, smart city projects, and other digital innovations. The combination of government support, growing subscriber bases, and technology-driven demand is accelerating infrastructure expansion, solidifying Asia Pacific’s position as a leading region in the global market.

North America Telecom Tower Market Trends

North America holds a significant share of the global telecom tower market, driven by widespread 5G network expansions and integration with data centers. In the U.S., major investments under initiatives such as the Infrastructure Investment and Jobs Act have allocated substantial funding to expand broadband access, particularly in underserved regions, boosting tower deployments.

Urban areas, including cities such as New York and Los Angeles, are witnessing rapid small cell installations to support dense populations, fueled by increasing demands for streaming, cloud services, and remote work solutions.

Canadian telecom providers are pursuing expansion strategies, focusing on enhancing rural connectivity and bridging the digital divide. The region’s strong emphasis on modernizing telecommunications infrastructure, coupled with technological advancements and supportive government policies, continues to drive growth in tower construction, small cell networks, and integrated solutions.

Middle East Telecom Tower Market Trends

The Middle East is emerging as the fastest-growing region in the global telecom tower market, driven by ambitious digital transformation strategies and large-scale smart city initiatives in key countries such as Saudi Arabia and the UAE.

Saudi Arabia’s Vision actively promotes the adoption of advanced technologies, including 5G and the Internet of Things (IoT), resulting in extensive tower deployments to support nationwide high-speed connectivity, digital services, and industrial automation.

The UAE, particularly through its Dubai Smart City initiative, is investing heavily in telecom infrastructure to enable intelligent urban planning, enhanced public services, and seamless connectivity across commercial and residential areas.

These initiatives are complemented by strong regulatory frameworks and active public-private partnerships, which help streamline approvals, reduce deployment timelines, and improve operational efficiency.

Additionally, government incentives encourage private sector participation, accelerating the construction of both macro towers and small cell networks to meet growing data and connectivity demands. Combined, these factors are driving robust network expansion, enhancing digital inclusion, supporting technological innovation, and positioning the Middle East as a leading hub for next-generation telecommunications infrastructure.

Competitive Landscape

The global telecom tower market is highly competitive, with both global and regional players striving to gain market share through innovation, cost-effective solutions, and reliable services. Growing demand for sustainable and multi-tenant towers intensifies rivalry, while strategic partnerships, mergers, and timely regulatory approvals serve as critical differentiators, enabling companies to strengthen their market position and address evolving industry requirements.

Key Developments:

- June 2025: Indus Towers generated USD 1.57 Bn in free cash flow in Q1 2025, supported by collections from Vodafone Idea receivables. The company announced plans for extensive upgrades, including solar and lithium-ion installations across 249,305 sites, enhancing sustainability and operational efficiency nationwide.

- May 2025: Cellnex reported strong organic growth in Q1 2025 and reaffirmed its positive full-year guidance, maintaining confidence despite ongoing macroeconomic uncertainties. The company highlighted robust operational performance and strategic initiatives as key drivers supporting sustained expansion across its tower infrastructure portfolio.

Companies Covered in Telecom Tower Market

- American Tower Corporation

- AT&T, Inc.

- Cellnex Telecom S.A.

- China Tower Corporation Limited

- Crown Castle

- GTL Infrastructure Limited

- Helios Towers Plc

- IHS Holding Limited

- Indus Towers Limited

- SBA Communications Corporation

- Telesites S.A.B.

- Viom Networks

- ABB Ltd.

- STMicroelectronics N.V.

- Schneider Electric

Frequently Asked Questions

The telecom tower market is projected to reach US$30.0 Bn in 2025.

Rising telecommunications demands, technological advancements in 5G, and government initiatives for digital connectivity are key drivers.

The industry is poised to witness a CAGR of 3.2% from 2025 to 2032.

Innovations in sustainable systems and multi-tenant solutions present significant growth opportunities.

American Tower Corporation, China Tower Corporation Limited, and Crown Castle are among the leading players.