- Automotive Components & Materials

- Automotive Engine Oil Market

Automotive Engine Oil Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Automotive Engine Oil Market by Product Type (Mineral Engine Oil, Synthetic Engine Oil, Semi‑Synthetic Engine Oil, Bio‑Based Engine Oil), Viscosity Grade (0W‑20, 0W‑30, 5W‑20, 5W‑30, 5W‑40, 10W‑30, 10W‑40, 15W‑40, Others), Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, Two Wheelers, Off‑road Vehicle), Distribution Channel, and Regional Analysis for 2026 - 2033

Automotive Engine Oil Market Share and Trends Analysis

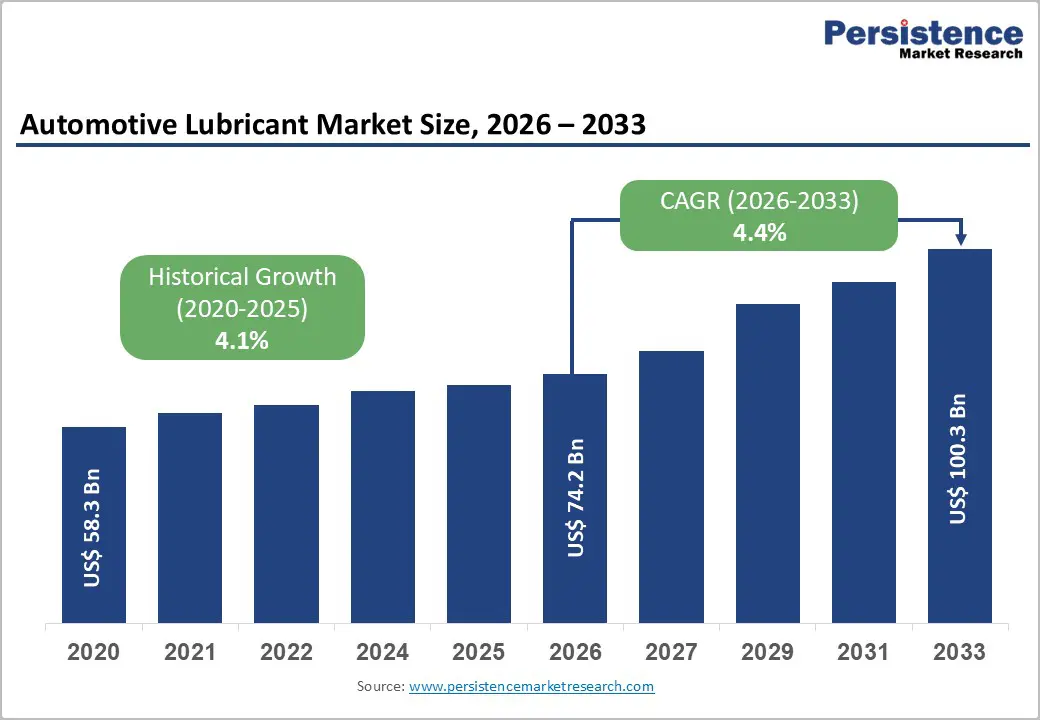

The global automotive engine oil market size is projected at US$45.2 billion in 2026 and is projected to reach about US$60.7 billion by 2033, growing at a CAGR of around 4.3% between 2026 and 2033.

Demand is anchored by a large in-use vehicle parc, especially in emerging markets, and rising consumer awareness regarding preventive maintenance and drain interval optimization. OEM engine downsizing and tighter emission norms increase reliance on higher-performance lubricants, including synthetic and low-viscosity grades. Asia Pacific’s dominant vehicle base and expanding two-wheeler and passenger car segments underpin sustained volume demand, while premium formulations drive value growth.

Key Industry Highlights:

- The Automotive Engine Oil market is projected to grow from about US$45.2 billion in 2026 to roughly US$60.6 billion by 2033, at around 4.3% CAGR.

- Mineral Engine Oil leads with around 48% share, while Bio-Based Engine Oil is the fastest-growing product type at approximately 7.2% CAGR.

- 5W-30 holds about 23% share, and 0W-20 is the fastest-growing viscosity grade, expanding at roughly 6.2% CAGR as OEMs adopt low-viscosity oils.

- Passenger Vehicles account for around 53% of demand, while Two Wheelers show the highest growth at approximately 5.2% CAGR.

- The Aftermarket channel commands about 72% share, with OEM distribution growing at nearly 3.9% CAGR.

- Asia Pacific leads with around 43% share and is the fastest-growing region, while North America and Europe together account for a substantial proportion of premium oil consumption.

- Recent developments include capacity expansions, new synthetic and bio-based formulations, and deeper OEM alliances among major oil companies.

| Key Insights | Details |

|---|---|

|

Automotive Engine Oil Market Size (2026E) |

US$ 45.2 Billion |

|

Market Value Forecast (2033F) |

US$ 60.6 Billion |

|

Projected Growth CAGR (2026-2033) |

4.3% |

|

Historical Market Growth (2020-2025) |

3.9% |

Market Dynamics Analysis

Drivers - Expanding global vehicle parc and usage intensity

Global light-duty vehicle stock surpassed 1.4 billion units mid-decade, with additional growth coming from commercial vehicles and two-wheelers in emerging markets. The International Energy Agency notes that road transport continues to account for the largest share of oil demand, with developing economies contributing most of the incremental mileage. This expanding, aging vehicle parc sustains high replacement demand for engine oil, as even modest annual mileage generates frequent oil change requirements across passenger vehicles, light and heavy commercial fleets, and two-wheelers, stabilizing base-load consumption. Rising urbanization, e-commerce logistics expansion, and growing ride-sharing fleets further increase vehicle utilization rates, resulting in shorter maintenance intervals and higher recurring demand for automotive engine oils across global transportation networks.

Stringent emission and fuel-efficiency regulations

Tighter tailpipe emission and CO- standards in North America, Europe, China, and India compel OEMs to adopt advanced engine designs, turbocharging, and aftertreatment systems that require low-viscosity, high-performance lubricants. Regulatory regimes such as Euro 6 emissions standard, Corporate Average Fuel Economy standards, and China VI emissions standard demand improved fuel economy and lower particulate emissions, which are partly delivered through optimized friction characteristics and cleanliness offered by synthetic and semi-synthetic oils. This structurally shifts demand toward premium formulations, raising average value per litre even where overall volumes grow moderately. As regulatory timelines tighten toward next-generation standards, lubricant manufacturers are accelerating development of ultra-low-viscosity and additive-enhanced formulations to meet OEM approval requirements.

Restraints - Electrification and improvements in engine technology

Long-term electrification trends, particularly in Europe and China, gradually reduce demand for conventional engine oils as battery electric vehicles do not require crankcase lubricants. Even within internal combustion platforms, higher-quality synthetics and engine design improvements enable extended drain intervals, lowering per-vehicle consumption over time. These shifts cap volume growth and intensify competition in mature markets, forcing suppliers to rely more on value-added formulations and emerging-market vehicle parc expansion to offset declining fill volumes per vehicle.

Environmental pressures and waste-oil management

Stricter environmental policies around used oil collection, disposal, and carbon footprints increase compliance costs for producers and distributors. Regulators promote recycling and re-refining of waste lubricants, while consumer and fleet preferences slowly move toward lower-impact formulations, including bio-based and low-SAPs products. Producers that lag in developing sustainable portfolios risk losing share, and failure to meet evolving standards in key markets can restrict product approvals, posing structural barriers to sales growth.

Opportunity - Growth of bio-based and low-emission engine oils

Bio-based lubricants remain a small but fastest-growing niche as fleets and regulators seek lower lifecycle emissions and reduced dependence on petroleum feedstocks. With the user-provided estimate of bio-based engine oil growing at about 7.2% CAGR, incremental revenue potential can reach hundreds of millions of dollars by 2033 if penetration rises in sensitive applications and public fleets. Investments in stable base stocks, OEM endorsements, and competitive pricing could accelerate adoption beyond currently limited high-awareness segments. Advances in biodegradable additives, stronger environmental policies, and public procurement mandates are expected to further enhance demand, especially in government fleets, urban transport systems, and environmentally regulated industries worldwide.

Premium low-viscosity oils for fuel-efficient engines

Low-viscosity grades such as 0W-20 and 5W-30 are expanding rapidly as OEMs specify them to reduce friction and deliver measurable fuel-efficiency gains. The user-provided data indicates 5W-30 holds about 23% share, while 0W-20 is the fastest-growing grade with a CAGR of roughly 6.2%, reflecting OEM factory-fill trends and aftermarket pull-through. As automakers in Asia Pacific, North America, and Europe converge on such specifications, premium low-viscosity oils represent a multi-billion-dollar opportunity by 2033. Increasing hybrid vehicle adoption, stricter fuel-economy regulations, and extended oil-drain intervals will continue encouraging motorists and fleet operators to shift toward advanced synthetic low-viscosity lubricants across developed and emerging automotive markets.

Category-wise Analysis

Product Type Insights

Mineral Engine Oil is the leading product type, accounting for around 48% of the global Automotive Engine Oil market, supported by price-sensitive customers and large legacy vehicle fleets in Asia Pacific, Africa, and parts of Latin America. It remains dominant in older passenger cars, commercial vehicles, and two-wheelers where OEM requirements and usage patterns still allow conventional formulations, particularly in markets with lower average ticket sizes and limited awareness of synthetic benefits.

The Bio-Based Engine Oil segment is the fastest growing, with a user-indicated CAGR of about 7.2%, driven by corporate sustainability goals, government procurement standards, and specialized applications requiring improved biodegradability. Growth is also supported by technology advances in bio-based base oils and additive packages that close performance gaps with mineral and synthetic products.

Viscosity Grade Insights

The 5W-30 viscosity grade leads the market with an estimated 23% share, reflecting its widespread OEM recommendation for modern gasoline and light-duty diesel engines in Europe, North America, and increasingly Asia. It balances cold-start performance and high-temperature protection, making it a default choice for many factory fills and aftermarket services in passenger vehicle segments seeking fuel efficiency and durability.

The 0W-20 grade is the fastest-growing viscosity segment, expanding at an estimated CAGR of about 6.2% as OEMs prioritize fuel economy and lower emissions through ultra-low-viscosity lubricants. Its adoption is particularly strong in newer gasoline engines and hybrid vehicles, where reduced internal friction translates directly into measurable efficiency improvements.

Vehicle Type Insights

Passenger Vehicles are the leading vehicle type, contributing around 53% of Automotive Engine Oil consumption, according to user data, due to their dominant share of global vehicle parc and more frequent oil changes in many ownership models. High passenger car densities in Asia Pacific, Europe, and North America, combined with widespread reliance on internal combustion powertrains, underpin this category’s central role in the market’s revenue base.

The Two Wheelers segment is the fastest growing, with a user-indicated CAGR of about 5.2%, driven by large and expanding motorcycle and scooter fleets in Asia Pacific and parts of Latin America and Africa. Rising urbanization and affordable two-wheeler ownership maintain strong lubricant replacement cycles despite relatively low oil volumes per unit.

Distribution Channel Insighths

The Aftermarket is the leading distribution channel, representing around 72% of global Automotive Engine Oil sales, reflecting the large in-use vehicle base serviced through independent workshops, quick-lube centers, and retail outlets. This channel is especially critical in emerging markets, where vehicle owners often rely on non-dealer service points and brand choice is influenced by local availability, pricing, and mechanics’ recommendations.

The Aftermarket also shows the fastest growth momentum overall, while the OEM channel is expected to grow at a CAGR of about 3.9%, supported by rising new-vehicle sales and extended service contracts. OEM-approved oils secure early brand exposure at factory fill, with potential for long-term loyalty when combined with dealer maintenance programs.

Regional Market Insights

North America Automotive Engine Oil Market Trends

North America accounts for roughly 24% of the global Automotive Engine Oil market, supported by a large light truck and SUV parc in the United States and Canada and relatively high annual vehicle miles traveled. The region features strong penetration of synthetic and semi-synthetic oils, with consumers and fleets valuing extended drain intervals and cold-start performance in varied climates. Regulatory frameworks such as U.S. fuel-economy and emissions standards drive adoption of lower-viscosity OEM-specified oils, while a mature quick-lube and aftermarket service ecosystem sustains robust replacement volumes.

Growth in North America is expected to be moderate but stable, supported by continued use of internal combustion and hybrid vehicles even as battery electric vehicles gain share. Investment opportunities include premium synthetic products, OEM co-branded lines, and data-enabled service offerings that enhance customer retention and optimize oil-change timing for commercial fleets.

Europe Automotive Engine Oil Market Trends

Europe represents a significant share of global Automotive Engine Oil demand, with strong contributions from Germany, the U.K., France, Spain, and Italy, underpinned by a large passenger car parc and premium vehicle mix. The region’s stringent Euro emissions standards and widespread adoption of diesel and gasoline direct-injection technologies have long favored high-performance synthetic and low-SAPs formulations. Harmonized ACEA specifications and OEM approvals shape product qualification, while well-developed dealer networks and independent workshops provide multiple routes to market.

European demand is projected to grow at around 3.8% CAGR as provided by the user, with volume growth constrained by efficiency improvements and gradual electrification, but value supported by premium product penetration. Investment opportunities center on hybrid-ready oils, bio-based and low-carbon formulations, and advanced engine oils supporting extended-service intervals under demanding driving and regulatory conditions.

Asia Pacific Automotive Engine Oil Market Trends

Asia Pacific is the leading and fastest-growing region, holding approximately 43% of the global Automotive Engine Oil market, driven by large and expanding vehicle and two-wheeler fleets in China, India, ASEAN, and other emerging economies. Regional consumption growth is fuelled by rising incomes, urbanization, and strong new-vehicle sales, particularly in compact cars, motorcycles, and light commercial vehicles. China remains the largest market, while India and Southeast Asia provide strong incremental demand, including rapid uptake of synthetic and semi-synthetic oils.

With Asia Pacific engine oil markets expected to grow faster than global averages, investment opportunities span localized blending and packaging, tailored two-wheeler products, and OEM partnerships for new factories and service programs. The region’s manufacturing advantages and government support for automotive industries also underpin export potential and platform-led lubricant strategies.

Competitive Landscape

Leading Automotive Engine Oil companies pursue innovation-driven, cost-competitive, and regionally tailored strategies, focusing on synthetic and low-viscosity formulations, OEM approvals, and strong aftermarket branding. Key differentiators include robust global supply chains, technical service support, co-engineering with OEMs, and sustainability credentials. Emerging models emphasize digital marketing, subscription-based maintenance packages, and channel partnerships that integrate lubricants into holistic vehicle-care ecosystems.

Strategic Developments

- In February 2024, Shell launched next-generation synthetic automotive engine oils with improved fuel-efficiency and low-emission performance, targeting OEM-approved specifications for modern passenger cars and hybrids across major markets.

- In June 2024, BP (Castrol) introduced an upgraded range of low-viscosity engine oils aligned with evolving OEM requirements for downsized turbocharged engines, emphasizing extended drain intervals and CO- reduction benefits.

- In June 2024, TotalEnergies introduced its Quartz EV3R and Rubia EV3R lubricant ranges, formulated using high-quality regenerated base oils. The initiative supports circular economy goals through the “Reduce, Reuse, Regenerate” approach while maintaining OEM-approved performance and using packaging made with 50% recycled plastic.

Companies Covered in Automotive Engine Oil Market

- Shell plc

- ExxonMobil Corporation

- BP plc (Castrol)

- TotalEnergies SE

- Chevron Corporation

- Valvoline Inc.

- PetroChina Company Limited

- Sinopec Limited

- Indian Oil Corporation Limited

- Hindustan Petroleum Corporation Limited

- Bharat Petroleum Corporation Limited

- Fuchs Petrolub SE

- ENEOS Holdings Inc.

- Phillips 66

- Petronas Lubricants International

Frequently Asked Questions

The Automotive Engine Oil Market is projected to reach around US$45.2 billion in 2026 and approximately US$60.6 billion by 2033, reflecting steady global demand from a large and aging vehicle parc.

Growth is driven by expansion of the global vehicle parc, stricter fuel‑efficiency and emission standards requiring higher‑performance lubricants, and rising adoption of synthetic and low‑viscosity oils in both developed and emerging markets.

Between 2026 and 2033, the Automotive Engine Oil Market is anticipated to grow at around 4.3% CAGR, supported by value‑led product mix upgrades despite electrification‑related headwinds.

Key opportunities include bio‑based and low‑carbon engine oils, premium low‑viscosity grades such as 0W‑20 and 5W‑30, and expanding aftermarket and OEM programs in high‑growth Asia Pacific and other emerging regions.

Major players include Shell, ExxonMobil, BP (Castrol), TotalEnergies, Chevron, Valvoline, PetroChina, Sinopec, Indian Oil, HPCL, BPCL, and Fuchs, which collectively shape technology, branding, and supply dynamics worldwide.