- Energy Storage Solutions

- Fuel Cell Market

Fuel Cell Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Fuel Cell Market by Product Type (Proton Exchange Membrane, Solid Oxide, Molten Carbonate, Phosphoric Acid, Alkaline, and Others), by Application (Transportation, Portable Power, and Stationary Power Generation), and Regional Analysis for 2026 - 2033

Fuel Cell Market Size and Trends Analysis

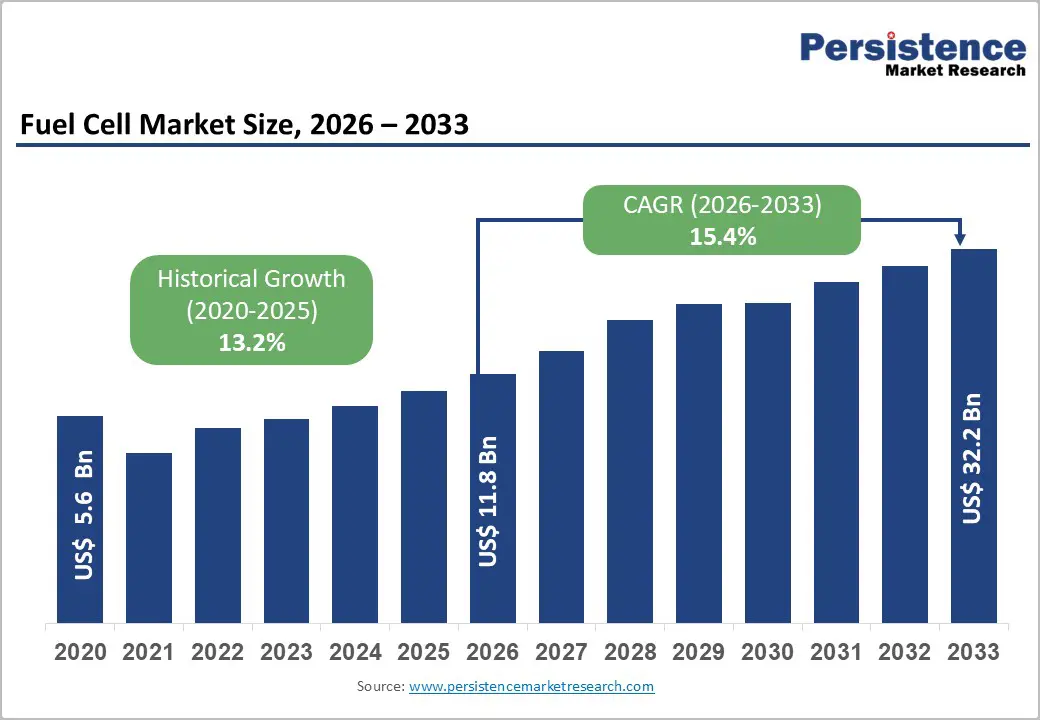

The global fuel cell market size is likely to be valued at US$11.8 billion in 2026 and is projected to reach US$32.2 billion by 2033, growing at a CAGR of 15.4% during the forecast period from 2026 to 2033.

This substantial growth trajectory reflects accelerating demand driven by three primary catalysts: the global transition toward decarbonization and clean energy adoption, technological advancements reducing fuel cell production costs and improving efficiency metrics, and regulatory frameworks mandating zero-emission transportation solutions across developed and emerging markets. The market's historical CAGR of 13.2% underscores consistent investor confidence and technology maturation, while the projected acceleration to 15.4% through 2033 demonstrates increasing commercial viability and market penetration across multiple application segments.

Key Industry Highlights:

- Product Type Analysis: Proton Exchange Membrane market dominance combined with Solid Oxide growth: PEM fuel cells maintain above 80% revenue share while Solid Oxide fuel cells expand at 16.3% CAGR, representing the fastest-growing technology segment driven by stationary power and industrial heat applications.

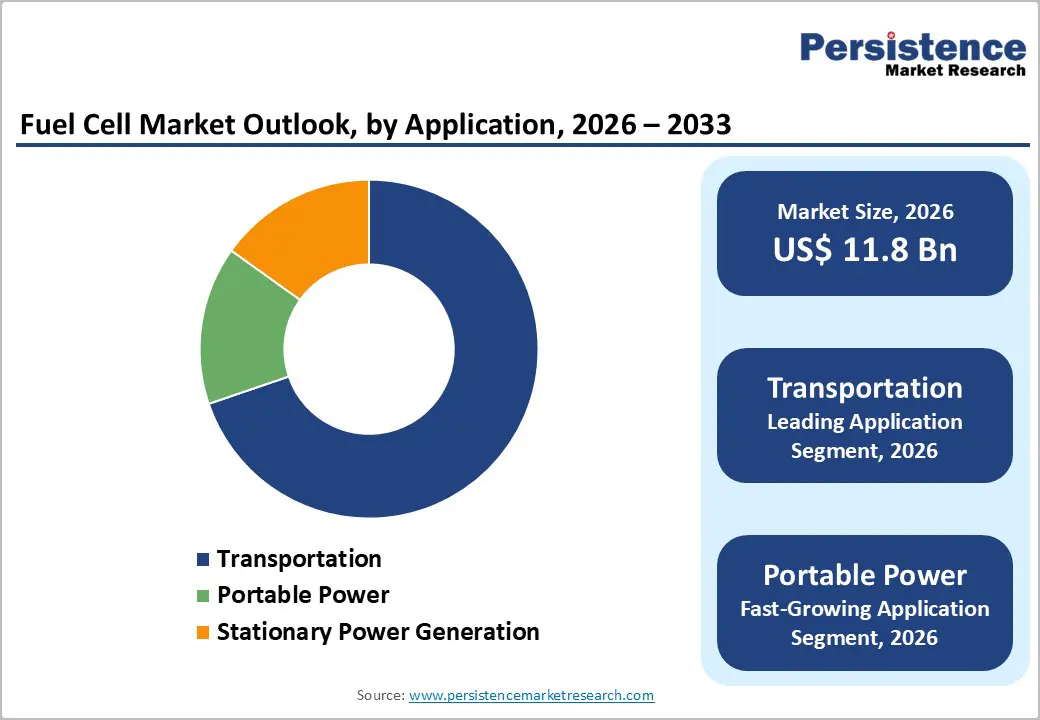

- Application Analysis: Transportation leadership and portable power acceleration: Transportation applications command above 75% market share, while portable power generation represents the fastest-growing segment with 16.5% CAGR expansion, driven by emerging commercial and consumer applications.

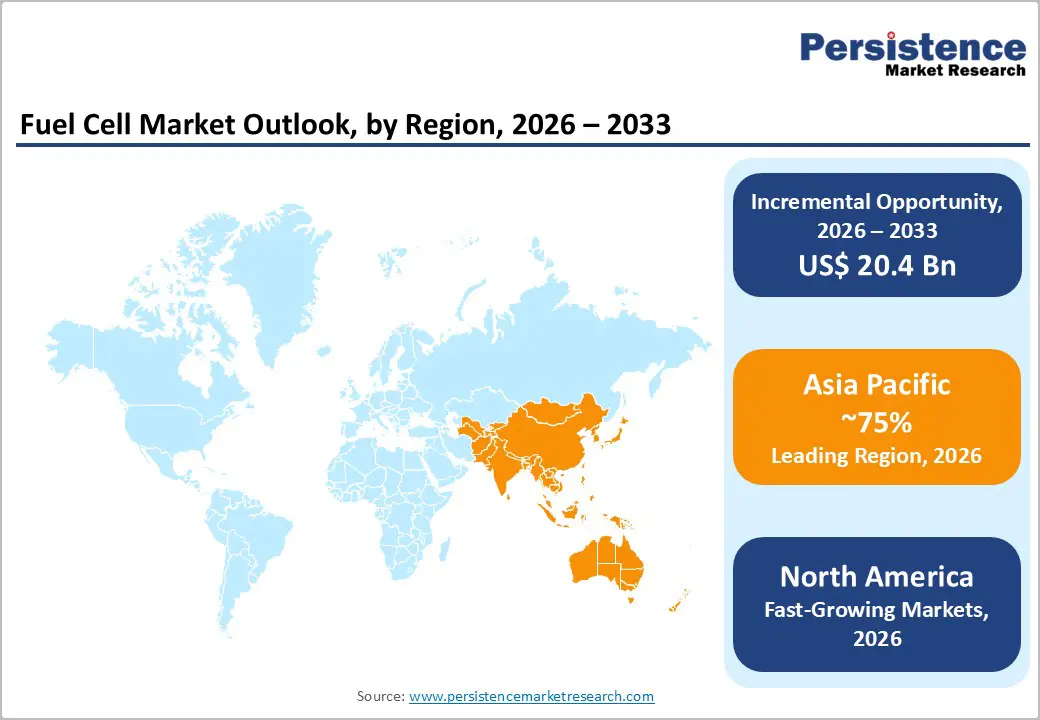

- Regional Analysis: Asia-Pacific regional leadership with North American acceleration: Asia-Pacific maintains a dominant regional position with above 75% revenue share while North America demonstrates the fastest growth at 16.7% CAGR, driven by regulatory incentives and technology commercialization investments.

- Strategic market consolidation and partnership development: Recent strategic partnerships, including Doosan Fuel Cell utility collaborations, EKPO technology advancements, and Cummins' Hydrogenics consolidation, signal market maturation and support ecosystem development, enabling accelerated technology commercialization.

- Technological advancement reducing cost barriers: Recent innovations in hydrogen production materials, PEM stack efficiency, and SOFC performance demonstrate cost reduction and performance improvement trajectories supporting market adoption across multiple application categories.

- Regulatory environment providing near-term demand certainty: Government hydrogen strategies, clean energy subsidies exceeding US$ 100 billion globally, and vehicle emissions standards create immediate market opportunities supporting infrastructure development and technology commercialization investments.

| Key Insights | Details |

|---|---|

| Fuel Cell Market Size (2026E) | US$ 11.8 Bn |

| Market Value Forecast (2033F) | US$ 32.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.2% |

Market Dynamics

Drivers - Regulatory Mandates and Climate Commitments Accelerating Clean Energy Transition

Government regulations and international climate agreements have emerged as the primary growth catalyst for the fuel cell market. The European Union's Green Hydrogen Strategy and the United States' Inflation Reduction Act provide substantial subsidies and tax incentives for hydrogen production and fuel cell commercialization. China's national hydrogen strategy, unveiled in 2020, aims to develop a hydrogen-based energy economy with specific targets for fuel cell vehicle deployment.

These regulatory frameworks create immediate market opportunities while establishing long-term competitive advantages for early-stage technology providers. The alignment of fuel cells with carbon neutrality targets in major economies directly translates to increased capital allocation toward hydrogen infrastructure development, demonstrating quantifiable market impact through government funding mechanisms and investment tax credits.

Restraint - Initial Capital Requirements and Cost Competitiveness Pressures

Despite technological improvements, fuel cell systems remain significantly more expensive than conventional combustion engines and increasingly competitive battery-electric alternatives. The manufacturing complexity of fuel cell stacks, platinum catalyst requirements, and specialized component sourcing create persistent cost structures that limit price competitiveness in cost-sensitive market segments.

Additionally, the immature supply chain and limited manufacturing scale compared to established automotive technologies result in higher production expenses. These economic barriers disproportionately impact developing economies and smaller enterprises, restricting market participation and slowing adoption rates in price-sensitive customer segments.

Opportunity - Stationary Power Generation and Industrial Heat Applications

The transition from fossil fuels to clean energy sources in industrial heat generation and combined heat and power (CHP) applications represents a substantial market expansion opportunity. Recent announcements of solid oxide fuel cells achieving 90% combined heat and power efficiency demonstrate technological viability for displacing conventional boilers and CHP systems.

Industrial facilities, data centers, and commercial buildings seeking decarbonization solutions represent addressable markets currently underpenetrated by fuel cell technology. The estimated addressable market for stationary applications alone exceeds US$ 6 billion by 2033, supported by industrial decarbonization mandates and energy efficiency regulations across developed economies.

Category-wise Analysis

Product Type Insights - PEM Fuel Cells Dominate Revenue While SOFCs Drive Fastest Market Growth

Proton Exchange Membrane (PEM) fuel cells continue to dominate the global fuel cell market, accounting for over 80% of total revenue, reflecting their advanced technological maturity, scalable manufacturing base, and broad application versatility. PEM fuel cells are widely adopted across transportation, portable power, and distributed stationary power systems due to their rapid start-up, high power density, and operational flexibility. A well-established manufacturing ecosystem for PEM stacks, supported by validated supply chains for critical components such as platinum-based catalysts and proton-exchange membranes, reinforces their leadership position.

Extensive support from research institutions and consistent investments by major automotive OEMs further strengthen commercialization. Large-scale deployment across passenger vehicles, buses, forklifts, and stationary installations has provided strong market validation, with the global installed base of PEM fuel cell systems now exceeding 500 megawatts of cumulative capacity, underscoring customer confidence and long-term reliability.

In contrast, solid oxide fuel cells (SOFCs) represent the fastest-growing product segment, expanding at a CAGR exceeding 16.3% over the forecast period. SOFC technology offers distinct advantages, including superior electrical efficiency, internal fuel reforming capability, and high tolerance for diverse fuels, making it well suited for stationary power generation and industrial heat applications.

Recent advances in stack architecture and manufacturing processes have reduced costs and extended operating lifetimes, improving commercial viability. Achievements such as 60% electrical efficiency and up to 90% combined heat and power efficiency highlight technology maturation, driving adoption across data centers, industrial facilities, and distributed energy systems.

Application Insights - Transportation Dominates Fuel Cell Demand While Portable Power Emerges as Fastest-Growing Segment

Transportation remains the dominant application segment in the global fuel cell market, accounting for over 75% of total revenue, underscoring its central role in decarbonizing mobility systems worldwide. This leadership is driven primarily by heavy-duty commercial vehicles such as long-haul trucks, buses, and specialized logistics fleets, where fuel cell technology offers clear operational advantages over battery-electric alternatives. These include extended driving range, rapid refueling times comparable to conventional fuels, and minimal impact on payload capacity, all of which are critical for commercial fleet efficiency.

Leading OEMs such as Daimler, Volvo, and Hyundai have made long-term commitments to hydrogen fuel cell vehicle platforms, moving beyond pilot programs to establish commercial production capabilities. Their investments signal growing confidence in technology maturity and cost-reduction trajectories. Additionally, supportive government policies, including purchase subsidies and public procurement programs for fuel cell buses in major urban centers, are accelerating adoption and helping manufacturers achieve economies of scale, further reinforcing transportation’s market dominance.

In contrast, portable power generation represents the fastest-growing application segment, expanding at a CAGR exceeding 16.5%. Growth is fueled by rising demand for reliable power in emergency response, remote and off-grid locations, defense operations, and professional field equipment. Advances in fuel cell stack miniaturization and compact hydrogen cartridge systems have enabled new use cases that were previously impractical. Military and disaster-response agencies are acting as early adopters, validating performance and supporting supply chain development. Collectively, the portable fuel cell power market is projected to exceed US$ 1.2 billion by 2033.

Regional Insights

Asia Pacific Leads Global Fuel Cell Market Through Policy Support and Manufacturing Scale

Asia Pacific dominates the global fuel cell market, accounting for over 75% of total revenue and establishing clear leadership across multiple fuel cell technologies. This dominance is underpinned by strong government support, manufacturing scale, and technological maturity across key economies. China benefits from being the world’s largest hydrogen producer, supported by long-term policy commitment toward hydrogen as a strategic energy carrier. Japan has demonstrated advanced commercialization through fuel cell vehicles and stationary power systems, reflecting high consumer acceptance and technological readiness.

South Korea further strengthens regional leadership through its national hydrogen strategy, combining government-backed R&D with large-scale commercial manufacturing capacity in PEM and SOFC technologies.

The region enjoys significant manufacturing cost advantages, with production expenses typically 15-20% lower than Western counterparts, supported by established supply chains for critical materials such as platinum catalysts, carbon paper, and specialized polymers. Heavy investment in hydrogen infrastructure-including refueling networks, renewable-powered hydrogen production, and storage facilities-continues to accelerate adoption across transport, stationary, and portable applications. Emerging markets such as India and ASEAN countries add incremental growth potential as clean energy policies gain momentum.

Cumulative government hydrogen investments exceed US$ 20 billion, reinforced by clear regulatory frameworks including China’s 10-Year Hydrogen Plan, Japan’s Basic Hydrogen Strategy, and South Korea’s Hydrogen Economy Roadmap. The competitive landscape is led by Asian manufacturers such as Doosan Fuel Cell, Ballard’s Asian operations, Hydrogenics Asia, and rapidly scaling Chinese players like HTCERA and SinoHytec, supported by strategic automotive partnerships and rising venture capital activity.

North America’s Regulatory Support and OEM Investments Accelerate Hydrogen Fuel Cell Commercialization

North America represents the fastest-growing regional market for hydrogen and fuel cell technologies, expanding at a CAGR exceeding 16.7%, underpinned by a robust and supportive regulatory framework. Growth is primarily driven by the U.S. Inflation Reduction Act, which allocates more than US$ 30 billion in tax credits and subsidies for hydrogen production and fuel cell commercialization, alongside over US$ 8 billion in federal funding dedicated to hydrogen infrastructure development. These measures significantly lower investment risk and accelerate market entry for technology providers and system integrators. At the state level, policies such as California’s Low Carbon Fuel Standard and Zero Emission Vehicle mandates create technology-specific incentives that directly support commercial deployment of fuel cell vehicles and clean hydrogen production.

North America also benefits from a dense concentration of fuel cell developers, hydrogen infrastructure specialists, and automotive manufacturers, enabling rapid technology transfer and commercialization. Major OEMs including General Motors, Hyundai North America, and Toyota Motor North America have committed to hydrogen fuel cell vehicle platforms, establishing pilot-to-commercial production capacity and strengthening regional supply chains. Real-world validation is evident in projects such as the Port of Long Beach’s Tri-gen hydrogen system, which demonstrates the viability of fuel cells for ports, logistics, and industrial operations. The competitive landscape is led by established players such as Plug Power, Ballard Power Systems, FuelCell Energy, and Cummins, supported by sustained public-private investment and annual venture capital funding exceeding US$ 1 billion.

Competitive Landscape

The global fuel cell market demonstrates characteristics of a consolidating industry transitioning from fragmentation toward concentrated competition among established technology providers. The top five manufacturers-including Ballard Power Systems, Plug Power, Doosan Fuel Cell, Hydrogenics (Cummins subsidiary), and FuelCell Energy-collectively command approximately 60% of the global fuel cell market, establishing clear competitive dominance. This concentration reflects significant capital requirements for technology development, manufacturing scale investments, and supply chain integration necessary for commercial success.

Emerging manufacturers, particularly Asian companies including SinoHytec and Chinese-based fuel cell developers, challenge established market positions through lower-cost manufacturing and government-backed development programs. The competitive landscape favors integrated technology providers capable of delivering complete system solutions spanning fuel cell stacks, balance-of-system components, and aftermarket service capabilities.

Key Industry Developments:

- In June 2025, Doosan Fuel cell signed a MOU with Seorabeol City Gas and GnC Energy at its Dongdaemun Doosan Tower to collaborate on 'Energy Business to Boost Regional Energy Welfare.' Under the MOU, Doosan Fuel Cell will provide fuel cells supply and Long term service agreement services, while Seorabeol City Gas will supply city gas within the region.

- In April 2025, EKPO to unveil powerful fuel cell technology, the NM20 stack module, for sustainable mobility and stationary applications. Delivering up to 400 kW, it is EKPO’s most powerful model yet and has been designed particularly with heavy-duty traffic and stationary applications in mind. The stack boasts a high level of efficiency, reduced hydrogen consumption, the capacity to work at higher temperatures, recyclability, and a long service life.

- In June 2025, according to Industrial Cooperation & Research Planning team, Hanyang University ERICA, Researchers in South Korea have developed a powerful and affordable new material for producing hydrogen, a clean energy source key for the fuel cells. By fine-tuning boron-doping and phosphorus levels in cobalt phosphide nanosheets, the process can generate scalable, low-cost hydrogen for the fuel cells.

- In May 2024, Japan-based Mitsubishi Electric Mobility and AISIN reached a basic agreement to establish a joint venture company for handling products for next generation EVs. The joint venture will offer new and attractive products to a wide range of customers. It would help in maximizing the synergy of Mitsubishi Electric Mobility’s traction motors, power converters, and control optimization technologies, as well as boost AISIN’s integration technology.

- In September 2024, Germany-based EKPO Fuel Cell Technologies GmbH, a leading full-service supplier of PEMFC stack modules and components, started focusing its business on hydrogen mobility in the commercial vehicle segment. Delivering up to 400 kW, it is EKPO’s most powerful model yet and has been designed particularly with heavy-duty applications in mind.

- In August 2024, California-based Bloom Energy announced a hydrogen solid oxide fuel cell with 60% electrical efficiency and 90% high-temperature combined heat and power efficiency.

- In June 2023, Cummins Inc., based in Indiana, announced the buyout of Air Liquide’s 19% interest in Hydrogenics Corporation. The former acquired Hydrogenics in 2019, adding key fuel cell and electrolyzer technologies to its portfolio. Cummins’ buyout reinforces its commitment to these technologies and the increasing importance they will play in creating value for all stakeholders and decarbonizing the world.

- In 2023, Doosan Fuel Cell collaborated with Kolon Global to develop a hydrogen fuel cell business model using biogas. Under this partnership, Doosan Fuel Cell manages the hydrogen fuel cell supply and Long-Term Maintenance (LTSA).

- In 2023, FuelCell Energy, Inc. and Toyota Motor North America announced the completion of Tri-gen system at Toyota's Port of Long Beach operations. Tri-gen is an example of FuelCell Energy's ability to scale hydrogen-powered fuel cell technology.

Companies Covered in Fuel Cell Market

- AISIN Corporation

- Cummins Inc.

- Mitsubishi Heavy Industries

- Toshiba Corporation

- KYOCERA Corporation

- Fuji Electric Co Ltd

- ElringKlinger AG

- Bloom Energy

- Plug Power Inc

- Doosan Fuel Cell Ltd

- SFC Energy AG

- FuelCell Energy Inc

- Ballard Power System

- Ceres Power

- Solid Power

- Other Market Players

Frequently Asked Questions

The Fuel Cell market is estimated to be valued at US$ 11.8 Bn in 2026.

The key demand driver for the Fuel Cell market is strong government policy support and decarbonization mandates aimed at reducing greenhouse gas emissions across transportation, power generation, and industrial sectors.

In 2026, Asia Pacific is likely to dominate with an exceeding 75% revenue share in the global fuel cell market.

Among applications, transportation enjoys the highest preference, capturing beyond 21% of the market revenue share in 2026, surpassing other applications.

AISIN Corporation, Cummins Inc., Mitsubishi Heavy Industries, Toshiba Corporation KYOCERA Corporation and Fuji Electric Co Ltd. There are a few leading players in the Fuel Cell market.