- Hardware & Software IT Services

- Cybersecurity Market

Cybersecurity Market Size, Share, and Growth Forecast 2026 - 2033

Cybersecurity Market by Component (Hardware, Software, Services), Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security, IAM, Others), Deployment (Cloud-based, On-premises, Hybrid), Enterprise Size (SMEs, Large Enterprise), Industry (BFSI, Government, IT & Telecom, Retail & E-commerce, Manufacturing, Healthcare, Aerospace & Defense, Energy & Utilities, Transportation, Others), and Regional Analysis, 2026 - 2033

Cybersecurity Market Size and Trend Analysis

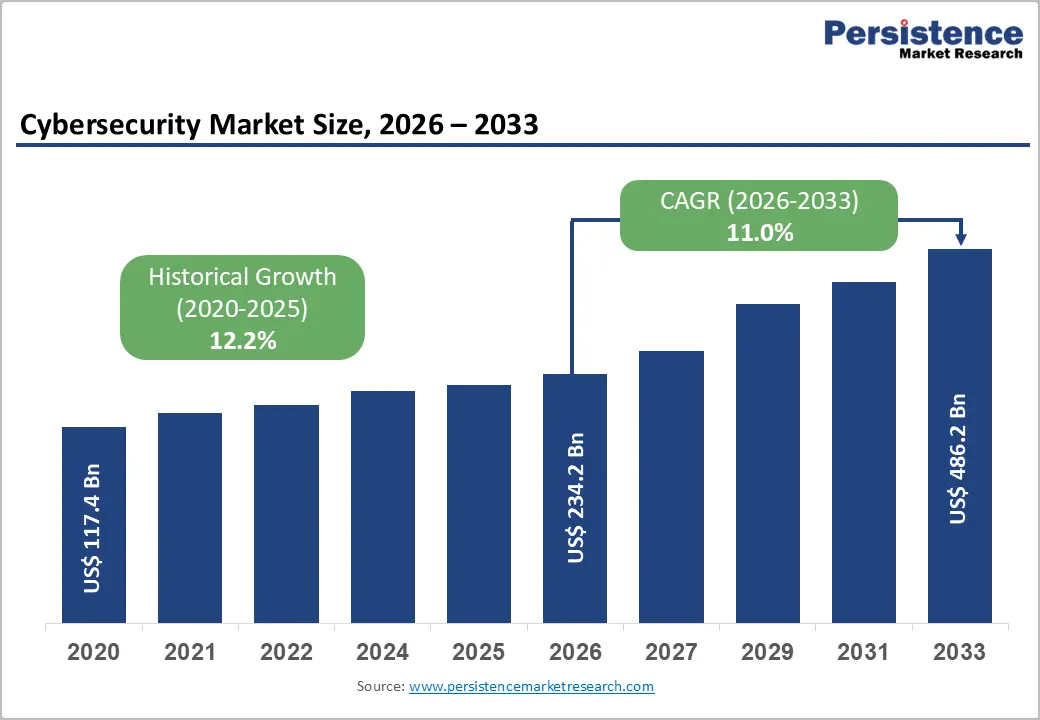

The global cybersecurity market size is expected to be valued at US$ 234.2 billion in 2026 and projected to reach US$ 486.2 billion by 2033, growing at a CAGR of 11.0% between 2026 and 2033. This robust expansion is driven by an unprecedented surge in sophisticated cyberattacks targeting critical infrastructure, accelerating cloud migration, and binding regulatory compliance mandates across financial services, healthcare, and government sectors globally.

The market grew from US$ 117.4 billion in 2020 at a historical CAGR of 12.2%, propelled by the COVID-19 pandemic's rapid digitalization of work and commerce that massively expanded enterprise attack surfaces, the proliferation of ransomware-as-a-service criminal ecosystems inflicting hundreds of billions in damages annually, and government-mandated zero-trust architecture transitions across public sector organizations in the U.S., EU, and Asia Pacific.

Key Industry Highlights:

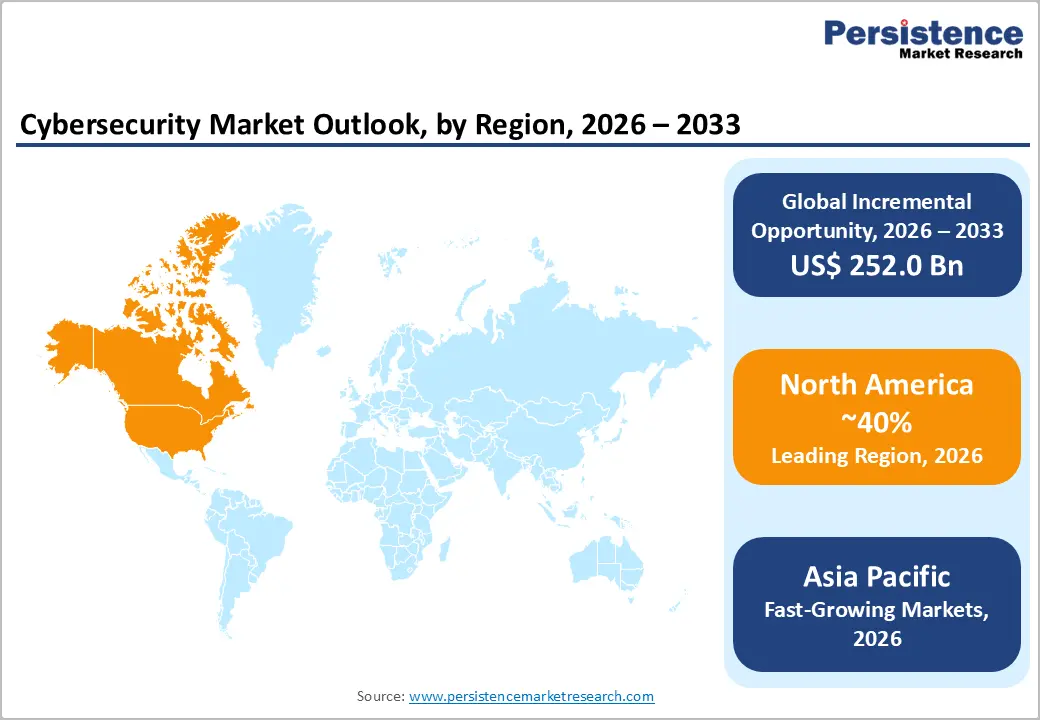

- Leading Region: North America commands 40% global cybersecurity market share in 2025, anchored by the world's largest enterprise security spending base, U.S. Executive Order 14028 zero-trust mandates, CISA managing 200,000+ annual incidents, and the highest concentration of cybersecurity vendors and investment globally.

- Fastest Growing Region: Asia Pacific is the fastest growing cybersecurity region at 13.2% CAGR through 2033, driven by India's DPDP Act 2023, China's Cybersecurity Law, CERT-In reporting 1.4M+ Indian incidents in 2022, and Southeast Asia's digital economy projected to exceed US$ 1 trillion by 2030.

- Dominant Component: Software holds 45% component market share in 2025, driven by NIST Cybersecurity Framework compliance mandates, cloud-native SaaS delivery enabling subscription recurring revenue, and Microsoft, CrowdStrike, and Palo Alto Networks platform consolidation strategies replacing multi-vendor point solution architectures.

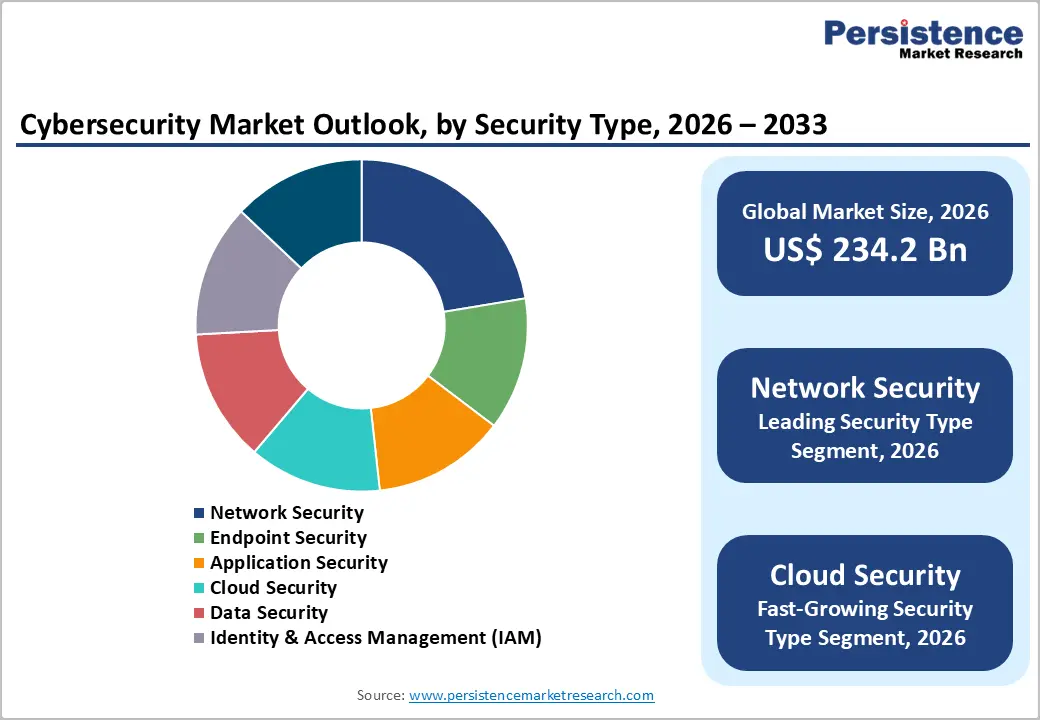

- Fastest Growing Security Type: Cloud security and XDR are the fastest growing segments, driven by hybrid work attack surface expansion, CSA-documented cloud misconfiguration breaches, and Microsoft Defender for Cloud, Palo Alto Prisma Cloud, and CrowdStrike Falcon platform adoption at above-market growth rates.

- Key Market Opportunity: GenAI integration in cybersecurity, through Microsoft Security Copilot, CrowdStrike Charlotte AI, and Palo Alto Cortex XSIAM, enables autonomous threat detection and analyst workflow automation, addressing the 4 million professional workforce gap documented by ISC2 through 2033.

Market Dynamics

Drivers - Escalating Ransomware and Nation-State Cyberattack Frequency Driving Emergency Security Investment

The exponential increase in ransomware attacks and nation-state-sponsored cyber operations is compelling enterprises and governments to escalate cybersecurity investment as a business continuity and national security imperative. The FBI's Internet Crime Complaint Center (IC3) reported that cyber-enabled financial losses exceeded US$ 12.5 billion in the U.S. alone in 2023, a record high. The Cybersecurity and Infrastructure Security Agency (CISA) has documented exponential growth in ransomware incidents targeting critical infrastructure, including hospitals, utilities, and financial institutions.

Globally, the Interpol's IGCI Cybercrime Report identifies ransomware-as-a-service as the dominant threat vector enabling non-technical criminal organizations to launch sophisticated attacks. Each major breach catalyzes immediate security budget increases across entire industry sectors, creating a reinforcing cycle of attack-response investment that structurally sustains double-digit cybersecurity spending growth.

Regulatory Compliance Mandates and Zero-Trust Architecture Transitions Driving Platform Investment

Stringent government cybersecurity regulations are creating non-discretionary, compliance-driven procurement demand across financial services, healthcare, and critical infrastructure sectors globally. The U.S. Executive Order 14028 on Improving the Nation's Cybersecurity mandated zero-trust architecture adoption across all federal agencies, directly driving multi-billion dollar security software procurement.

The EU's Network and Information Security 2 (NIS2) Directive expands mandatory cybersecurity obligations to over 160,000 entities across 18 critical sectors in EU member states. In financial services, DORA (Digital Operational Resilience Act) mandates ICT risk management and incident reporting across EU financial institutions from January 2025. These regulatory frameworks collectively generate mandatory technology investment across SIEM, IAM, endpoint detection, and data loss prevention software platforms that represent recurring, policy-anchored revenue streams for cybersecurity solution providers.

Restraints - Global Cybersecurity Talent Shortage Limiting Solution Deployment and Management

The global cybersecurity workforce gap represents one of the most significant structural constraints on market growth, as organizations cannot fully utilize purchased security technologies without trained personnel to configure, monitor, and respond to alerts. The ISC2 Cybersecurity Workforce Study estimates the global cybersecurity workforce gap at approximately 4 million professionals in 2023, with demand consistently outpacing supply. This talent shortage results in security tool underutilization, delayed deployment timelines, and increased managed security service dependence, limiting the revenue upside achievable from expanding security software adoption.

Complexity and Integration Challenges of Multi-Vendor Security Architectures

Enterprise security environments often comprise 30-70+ discrete security tools from multiple vendors, creating significant integration complexity, alert fatigue, and visibility gaps that paradoxically reduce security effectiveness despite high investment levels. IBM Security's Cost of a Data Breach Report consistently identifies security complexity as a factor that increases breach costs by millions of dollars per incident. The challenge of consolidating fragmented security architectures drives demand for integrated platforms but also creates organizational inertia that slows adoption of next-generation security solutions.

Opportunities - AI-Powered Security Operations and Autonomous Threat Detection: Fastest Growing Technology

Artificial intelligence and machine learning integration in cybersecurity platforms is the fastest growing technology category, enabling security operations centers to process threat intelligence at machine speed, detect behavioral anomalies across billions of events, and automate threat response that would require thousands of human analysts. Microsoft's Security Copilot and CrowdStrike's AI-native Falcon platform represent the commercial frontier of AI-powered security operations. The U.S. Department of Defense's (DoD) Zero Trust Strategy and CISA's AI cybersecurity guidelines are directing federal procurement toward AI-enhanced security platforms.

Extended Detection and Response (XDR) platforms integrating AI across endpoint, network, and cloud telemetry are projected to be the fastest growing software segment, with enterprises prioritizing unified visibility over fragmented point solutions as the attack surface complexity of hybrid multi-cloud environments escalates.

Cloud Security and SASE Architecture Adoption: Addressing the Hybrid Work Attack Surface

The permanent shift to hybrid work models and multi-cloud enterprise IT architectures has fundamentally expanded the enterprise security perimeter, creating sustained structural demand for cloud-native security solutions, including Secure Access Service Edge (SASE), Cloud Access Security Broker (CASB)), and cloud workload protection platforms (CWPP). The Cloud Security Alliance (CSA) reports that cloud security misconfigurations represent the leading cause of cloud data breaches, sustaining compliance-driven demand for automated cloud security posture management (CSPM) solutions.

Palo Alto Networks' Prisma Cloud, Microsoft's Defender for Cloud, and Fortinet's cloud security portfolio are capturing this high-growth demand segment. The Gartner-coined SASE framework, converging network and security capabilities in cloud-delivered architecture, is driving major enterprise procurement programs across financial services, technology, and healthcare sectors globally.

Category-wise Analysis

Component Insights

Software represents the leading Component segment, accounting for approximately 45% market share in 2025. Cybersecurity software, encompassing IAM, SIEM, XDR, DLP, and encryption platforms, commands the highest revenue share because software licenses and subscriptions are recurring, scalable, and increasingly delivered as cloud-native SaaS solutions with expanding feature sets that grow average contract values over time. The NIST Cybersecurity Framework and ISO 27001 compliance requirements mandate deployment of multiple software control categories across enterprise environments, creating compliance-driven adoption floors. Leading software providers, including Microsoft, Palo Alto Networks, CrowdStrike, and IBM Security are consolidating enterprise security software footprints through platform strategies that bundle multiple capabilities, accelerating both revenue growth and competitive moat development.

Security Type Insights

Network security represents the leading security type segment, accounting for approximately 22% market share in 2025. Network security, encompassing next-generation firewalls, intrusion detection/prevention systems, network traffic analysis, and VPN infrastructure, remains the foundational security investment for organizations of all sizes because every cyber threat ultimately traverses network infrastructure.

The Ponemon Institute's annual survey consistently identifies network perimeter protection as a top three enterprise security spending priority. Cisco Systems, Fortinet, Palo Alto Networks, and Check Point Software Technologies collectively control the largest revenue share in network security infrastructure, with next-generation firewalls providing the broadest enterprise revenue stream within this dominant segment.

Deployment Analysis

Cloud-based deployment is the leading and fastest growing deployment segment, accounting for approximately 52% share in 2025. The shift to cloud-delivered security solutions is driven by the elimination of on-premises hardware procurement and maintenance overhead, immediate scalability for dynamic enterprise environments, and the ability to deliver continuous feature updates and threat intelligence feeds without manual patching cycles.

The Cloud Security Alliance (CSA) documents consistent enterprise preference for cloud-native security platforms, with SaaS delivery enabling faster deployment, lower total cost of ownership, and superior integration with cloud workloads versus legacy on-premises security appliances. Leading cloud security providers, including Microsoft, CrowdStrike, and Zscaler have demonstrated the model's commercial viability through subscription revenue growth rates exceeding 30% annually.

Enterprise Size Insights

Large enterprises are dominant, accounting for approximately 68% market share in 2026. Large enterprises face significantly larger and more complex attack surfaces, spanning multi-cloud environments, thousands of endpoints, and extensive third-party supply chain relationships, requiring comprehensive, multi-layered security architectures that generate substantially higher per-organization spending than SMEs. Regulatory requirements including SOX, HIPAA, PCI DSS, and sector-specific mandates, disproportionately affect large enterprises with complex compliance obligations. IBM Security's Cost of a Data Breach Report documents average breach costs of over US$ 4.4 million for large organizations, a figure that creates compelling economic justification for substantial preventive security investment programs.

Industry Insights

BFSI (Banking, Financial Services, and Insurance) is the dominant Industry vertical, accounting for approximately 24% of the total cybersecurity market share in 2026. Financial institutions face the highest intensity of cyberattacks among all industry sectors, the Financial Services Information Sharing and Analysis Center (FS-ISAC) documents financial services experiencing attack volumes 300 times higher than other industries.

Mandatory compliance frameworks including PCI DSS, DORA), FFIEC guidelines, and central bank cybersecurity requirements globally mandate specific security controls, creating non-negotiable technology investment floors. BFSI organizations also have the highest cybersecurity budgets as a percentage of IT spend among all verticals, with leading financial institutions investing 10-12% of IT budgets in security programs.

Regional Insights

North America leads the global cybersecurity market with approximately 40% market share in 2025, while Asia Pacific is the fastest growing region, projected to record the highest CAGR of approximately 13.2% through 2026 - 2033.

North America Cybersecurity Market Trends and Insights

North America is the most mature and highest-spending cybersecurity market globally, anchored by the world's largest concentration of digital-native enterprises, the most stringent federal and state cybersecurity regulatory frameworks, and the highest density of cybersecurity vendors, research institutions, and talent ecosystems. U.S. Executive Order 14028 and CISA's Shields Up program have catalyzed significant federal and private sector security investment, while SEC cybersecurity disclosure rules effective 2024 create C-suite accountability for breach reporting.

The region leads globally in zero-trust architecture adoption, AI-powered SOC deployment, and managed detection and response (MDR) service consumption, all driving sustained premium security spending well above global average growth rates.

U.S. Cybersecurity Market Size

The United States accounts for approximately 82% of North American cybersecurity market revenue in 2025, making it the world's single largest national cybersecurity market by a substantial margin. With the IC3 reporting US$ 12.5 billion in cyber-enabled financial losses in 2023, the U.S. National Cybersecurity Strategy 2023 mandating technology provider security liability, and CISA managing over 200,000 cyber incidents annually, the demand base is structurally expanding and projected to grow at approximately 10.3% CAGR through 2033.

Europe Cybersecurity Market Trends and Insights

Europe's cybersecurity market is experiencing its fastest growth phase, driven by the mandatory compliance wave from NIS2 Directive, DORA, GDPR enforcement, and the EU's Cyber Resilience Act (CRA) requiring security-by-design in connected products. The European Union Agency for Cybersecurity (ENISA) documents consistent year-over-year increases in European cyber incident volumes, sustaining emergency security investment across public and private sectors. Cross-border regulatory harmonization is creating demand for unified compliance platforms.

Germany Cybersecurity Market Size

Germany holds approximately 22% of European cybersecurity market revenue in 2025. The Bundesamt für Sicherheit in der Informationstechnik (BSI) is one of Europe's most active cyber agencies, with NIS2 compliance mandating security investments across Germany's extensive critical infrastructure, automotive supply chains, and industrial manufacturers. Germany's IT-Sicherheitsgesetz 2.0 imposes additional sector-specific requirements driving enterprise security platform adoption.

U.K. Cybersecurity Market Size

The United Kingdom represents approximately 17% of European cybersecurity market revenue in 2025. The UK's National Cyber Security Centre (NCSC) and Cyber Essentials certification scheme drive SME and enterprise security investment. The UK government's National Cyber Strategy 2022 targets making the UK a leading cyber power by 2030, with significant public and private sector investment programs. Post-Brexit, the UK maintains its own GDPR-equivalent regulations sustaining compliance-driven security demand.

France Cybersecurity Market Size

France accounts for approximately 11% of European cybersecurity market revenue in 2025. ANSSI (Agence Nationale de la Sécurité des Systèmes d'Information) coordinates French national cybersecurity policy, with the NIS2 transposition and Loi de Programmation Militaire driving defense sector and OES (operators of essential services) security investment. France's growing technology and financial services sectors sustain premium cybersecurity solution adoption.

Asia Pacific Cybersecurity Market Trends and Insights

Asia Pacific is the fastest growing cybersecurity region globally, with China, the region's largest market at approximately 35% of regional revenue, driving massive security investment under the Cybersecurity Law of the People's Republic of China and Data Security Law mandates. Japan's Cybersecurity Strategy 2022, India's Digital India initiative, and ASEAN's digital economy growth are all generating rapidly expanding cybersecurity demand across the region.

India Cybersecurity Market Size

India represents approximately 14% of Asia Pacific cybersecurity market revenue in 2025. India's CERT-In (Indian Computer Emergency Response Team) reported over 1.4 million cybersecurity incidents in 2022. The Digital Personal Data Protection Act 2023 and RBI cyber risk guidelines are driving BFSI and enterprise security investment. India is projected at approximately 15.2% CAGR through 2033, reflecting accelerating digital infrastructure vulnerability exposure.

Japan Cybersecurity Market Size

Japan contributes approximately 11% of Asia Pacific cybersecurity market revenue in 2025. Japan's Cybersecurity Basic Act and NISC (National center of Incident readiness and Strategy for Cybersecurity) coordinate national cyber defense programs. Japan's advanced manufacturing and financial sectors drive enterprise security investment, while the country's Cybersecurity Strategy 2022 targets significant defense sector cybersecurity capability expansion. Japan is projected at approximately 11.5% CAGR through 2033.

Southeast Asia Cybersecurity Market Size

Southeast Asia collectively accounts for approximately 12% of Asia Pacific cybersecurity market revenue in 2025. Rapid digital economy expansion, with Google, Temasek, and Bain's e-Conomy SEA Report projecting the region's digital economy exceeding US$ 1 trillion by 2030, is dramatically expanding the attack surface. National cybersecurity agencies across Singapore (CSA), Malaysia (CyberSecurity Malaysia), and Indonesia are scaling investment programs, driving above-regional-average growth.

Competitive Landscape

The global cybersecurity market reflects a moderately consolidated structure at the platform level, where a few large players dominate through integrated, end-to-end security ecosystems, while the broader landscape remains fragmented with numerous niche vendors offering specialized solutions. Competition is increasingly centered on platform depth, AI-driven threat detection, real-time intelligence capabilities, and the ability to deliver unified security across cloud, network, and endpoint environments.

From a strategic perspective, the market is shifting toward platform consolidation, replacing multi-vendor architectures with unified solutions to reduce complexity and improve response times. Managed detection and response (MDR) services are gaining traction as organizations outsource security operations, while the integration of generative AI into threat analysis and automation is enhancing operational efficiency. Additionally, large-scale acquisitions and ecosystem partnerships are reshaping the competitive landscape by combining infrastructure, cloud, and cybersecurity capabilities, enabling providers to offer more comprehensive and scalable security frameworks.

Key Developments

- April 2026: UK’s National Cyber Security Centre (NCSC) launched the SilentGlass device, a plug-and-play hardware solution that blocks malicious activity across HDMI and DisplayPort connections, targeting high-threat environments and enabling secure display links through global commercialization partnerships.

- April 2026: NWN launched a new AI-enabled cybersecurity offering integrating managed security operations, platform integrations, and strategic partnerships, leveraging its Experience Management Platform to enhance threat detection, reduce response times, and streamline security operations for enterprise customers.

- March 2026: Databricks entered the cybersecurity market with its Lakewatch platform, an open, agentic SIEM that unifies enterprise data for AI-driven threat detection and response, enabling large-scale security analytics while reducing costs and eliminating vendor lock-in.

Cybersecurity Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 117.4 Billion |

| Current Market Value (2026) | US$ 234.2 Billion |

| Projected Market Value (2033) | US$ 486.2 Billion |

| CAGR (2026 - 2033) | 11.0% |

| Leading Region | North America, 40% market share (2025) |

| Dominant Component | Software, 45% market share (2025) |

| Top-Ranking Security Type | Network Security, 22% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 252.0 Billion |

Companies Covered in Cybersecurity Market

- Microsoft Corporation

- Broadcom Inc.

- Cisco Systems, Inc.

- Palo Alto Networks

- Fortinet

- IBM Corporation

- Check Point Software Technologies

- Sophos Ltd.

- Trend Micro Incorporated

- FireEye (Trellix)

- Juniper Networks

- CrowdStrike

- McAfee (Trellix / McAfee Enterprise)

- Forcepoint

- Zscaler

- SentinelOne

- Cloudflare

- Databricks

- NWN

Frequently Asked Questions

The cybersecurity market is projected to reach US$ 234.2 billion in 2026.

Demand is driven by rising cyberattacks, regulatory compliance mandates, and increasing digitalization.

North America leads, accounting for around 40% of the market share.

The key opportunity lies in AI-powered security operations and cloud security solutions.

Leading players include Microsoft, Palo Alto Networks, CrowdStrike, Fortinet, Cisco Systems, Broadcom, IBM Security, Check Point Software Technologies, Trend Micro, Zscaler, SentinelOne, and Cloudflare.