- Renewable Energy

- Hydrogen Refueling Stations Market

Hydrogen Refueling Stations Market Size, Share, Trends, Growth, Forecasts 2025 - 2032

Hydrogen Refueling Stations Market by Fuel Type (Gas, Liquid), by Mode of Operations (On-site, Off-site), by Station Type (Stationary, Mobile), by End-use (Automotive, Marine, Railway, Aviation), and Region Analysis for 2025 - 2032

Hydrogen Refueling Stations Market Size and Trends

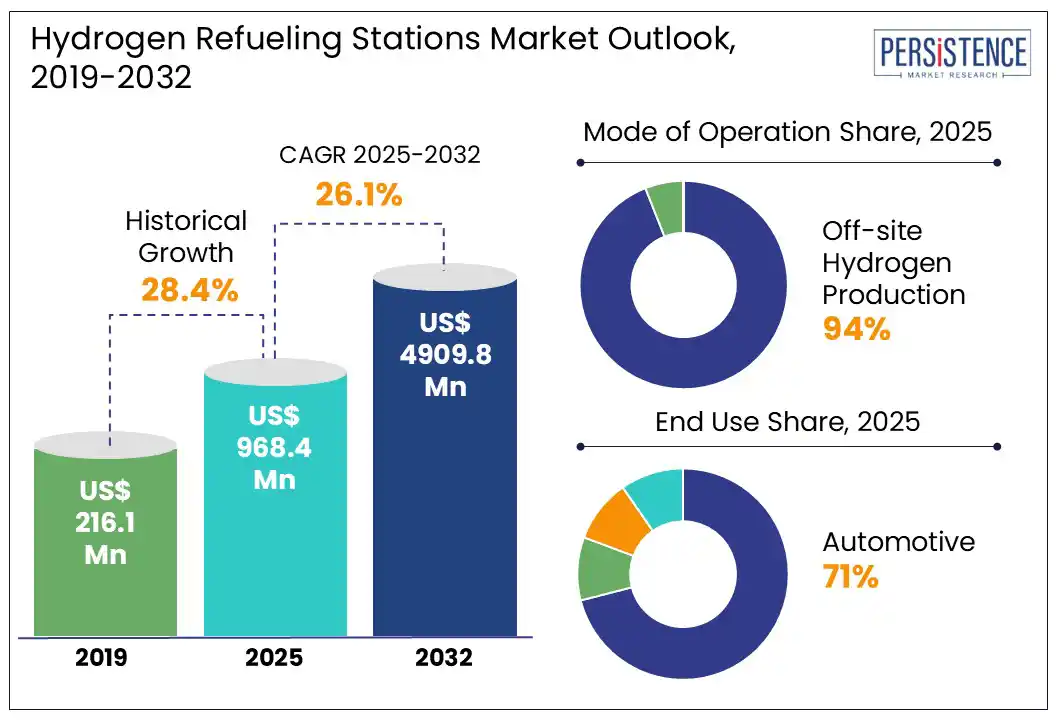

The hydrogen refueling stations market size is likely to be valued at US$ 968.4 Mn in 2025 and is expected to reach US$ 4,909.8 Mn in 2032, growing at a CAGR of 26.1% during the forecast period 2025-2032.

As the global race to decarbonize transport accelerates, hydrogen refueling stations are rapidly moving from niche pilot projects to key infrastructure assets shaping the future of mobility. These stations are now becoming strategically embedded into national energy policies, logistics corridors, and even airport ecosystems. Backed by multi-billion-dollar investments and regulatory mandates, hydrogen refueling infrastructure is undergoing a dramatic transformation. Key expansions in South Korea, Germany, and California are pointing toward the shift from experimental deployment to commercially viable networks.

Key Industry Highlights:

- The development of hydrogen corridors for heavy-duty transport and airport-based hydrogen hubs is unlocking new commercial potential.

- High-capacity stations for commercial fleets and integration with renewable-powered electrolyzers are transforming the hydrogen refueling landscape.

- Oil and gas companies are entering the hydrogen field, leveraging existing fuel station networks for rapid scale-up.

- Mobile hydrogen refueling stations are being deployed for fleet trials and remote applications.

- Off-site hydrogen production is leading as it eliminates the requirement for complex on-site equipment, lowering station setup and maintenance costs.

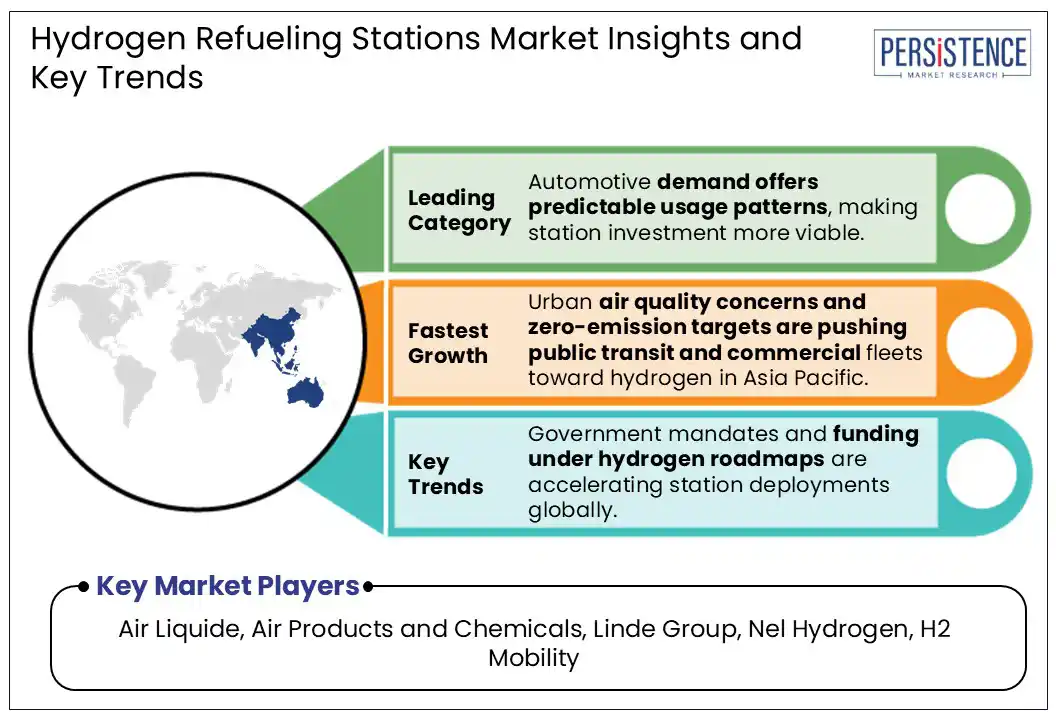

- Automotive will likely hold nearly 71% share in 2025 due to hydrogen’s fast refueling and long range, which give it a competitive edge in taxi, fleet, and long-haul trucking segments.

- Local automakers in Asia Pacific, such as Hyundai and Toyota, are now deploying hydrogen vehicles, pushing infrastructure requirements.

|

Global Market Attribute |

Key Insights |

|

Hydrogen Refueling Stations Market Size (2025E) |

US$ 968.4 Mn |

|

Market Value Forecast (2032F) |

US$ 4,909.8 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

26.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

28.4% |

Market Dynamics

Driver - Emission Pressures and BEV Limitations Fuel Demand

Rising concerns and stringent regulations regarding the harmful emissions from the transportation industry are expected to push the hydrogen refueling stations market growth. The global automotive market is witnessing a shift toward zero-emission mobility solutions such as Electric Vehicles (EVs) and Fuel Cell Electric Vehicles (FCEVs). While EVs are leading the market intrusion in two-wheeler, three-wheeler, and passenger cars segments, hydrogen-powered FCEVs are dominating in heavy-duty and public transport automotive segments.

A study by Clean Air Task Force (CATF), for example, revealed that a single refueling FCEV truck can travel 2.5X more distance than Battery Electric Vehicle (BEV) trucks, simultaneously saving about 14 hours of charging time per refueling. The global on-road fleet of FCEVs grew from 25,212 units in 2019 to 34,804 units in 2020, representing 38% Y-o-Y growth. With the forecast projecting 200,000 units of FCEVs on the road by this decade, demand for supporting infrastructure is anticipated to rise significantly. Hence, installations of hydrogen refueling stations, both stationary and mobile-operated are predicted to accelerate over the next ten years.

Restraint - Fossil-based Hydrogen Supply and Poor Coordination Impede Growth

The deployment of sustainable hydrogen refueling stations is a cost-intensive process and poses some standardization challenges. The design and cost as well as the environmental impact, depend on how hydrogen is produced and delivered to stations. For example, if hydrogen is produced with a renewable route, then the operations are likely to have a minimal environmental impact. However, across the globe, only one percent of hydrogen is generated from renewable energy, while the rest is based on more energy-intensive processes that use fossil fuels.

Another challenge for the development of hydrogen infrastructure is the lack of coordination between different countries and manufacturers to assign appropriate codes for the co-evolution of refueling networks and FCEVs. Different organizations across the globe, including the Department of Energy, Hydrogen Associations, and Automotive Manufacturers, are collaborating to develop standards and codes for hydrogen infrastructure.

Opportunity - Aviation industry eyes hydrogen fuel to cut emissions

Hydrogen as a fuel is not only powering the automotive industry but also prevailing as a key zero-emission fuel for aviation, marine, and railway industries. In the aviation industry, the development and adoption of hydrogen-powered aircraft is gaining traction due to its high energy storage and zero emissions. Burning hydrogen as a fuel in jet engines often results in water vapor as a byproduct, causing no harm to the environment.

Key aircraft manufacturers are investing in research and development to create propulsion engines based on hydrogen as an alternative fuel to power long flights and reduce environmental impact. For instance, Airbus launched the ZEROe program, where it has invested in developing hydrogen-powered aircraft. The company emphasizes liquid hydrogen, which requires 80% less space compared to gaseous hydrogen to generate the same amount of energy.

Category-wise Analysis

Mode of Operation Insights

By mode of operation, the market is bifurcated into on-site and off-site hydrogen production. Among these, off-site hydrogen production is predicted to hold nearly 94% share in 2025, backed by its scalability, cost-effectiveness, and ability to comply with green hydrogen goals. One key factor is the economic advantage of centralized production, where hydrogen can be generated in bulk using large-scale electrolysis or steam methane reforming facilities and then transported to refueling stations via tube trailers or pipelines. This model significantly reduces the capital expenditure required at individual station sites, especially in urban or space-constrained areas.

On-site hydrogen production is gaining significance owing to its potential to reduce logistics costs, enhance energy independence, and ensure uninterrupted fuel availability. These systems enable immediate generation and dispensing, optimizing the entire supply chain. It is particularly valuable in remote or urban areas where delivery infrastructure is limited or vulnerable to disruption. In Norway, for instance, Hynion has deployed electrolysis-based on-site production at its refueling stations to support local hydrogen bus fleets.

End-use Insights

By end use, the market is divided into automotive, marine, railway, and aviation. Out of these, the automotive segment will likely account for approximately 71% of the hydrogen refueling stations market share in 2025 due to the increasing deployment of FCEVs in both public and commercial transportation fleets. The push from governments and OEMs to decarbonize transport without compromising on range or refueling speed is another key driver. Leading automakers such as Toyota, Hyundai, and Honda are also expanding their hydrogen portfolios, pushing governments and energy companies to accelerate station deployment.

The aviation sector is emerging as a key frontier for hydrogen refueling infrastructure due to the industry's emphasis on decarbonization. While commercial hydrogen flights are not yet mainstream, groundwork for airport-based hydrogen ecosystems is accelerating. One of the primary drivers is the European Union's Clean Aviation initiative and the Hydrogen Airports roadmap under the Clean Hydrogen Partnership. It aims at designing at least 10 airports for hydrogen refueling operations by 2030.

Region Insights

North America Hydrogen Refueling Stations Market Trends

North America’s market is still in its nascent stage, heavily concentrated in California. As of early 2025, the state had around 62 operational hydrogen stations, with an additional 30 to 40 in various stages of planning and construction. This limited but developing infrastructure is primarily focused on serving FCEVs such as the Toyota Mirai and Hyundai Nexo. However, the expansion of these stations has faced setbacks due to supply chain disruptions and maintenance issues, prompting consumer complaints about station downtime and hydrogen shortages.

Beyond California, the rollout remains minimal. There are, however, signs of progress. In Canada, Québec is emerging as a focal point due to the country's abundant hydroelectric power. In the U.S. hydrogen refueling stations market, the strategy is shifting toward heavy-duty hydrogen transportation, specifically for freight and commercial fleets. Nikola Corporation, for insurance, has partnered with Voltera to build up to 60 hydrogen stations across the U.S. by 2026, targeting key logistics routes.

Europe Hydrogen Refueling Stations Market Trends

Europe’s market is steadily expanding, backed by strong government support, EU funding, and coordinated cross-border initiatives. As of early 2025, there are over 186 public hydrogen refueling stations across Europe. H2 MOBILITY Deutschland has played a key role in the rollout across Germany, partnering with Shell, TotalEnergies, and Air Liquide to standardize and expand access. These stations primarily support fuel cell passenger vehicles and buses.

France is aggressively scaling up, with the government’s France 2030 plan allocating €7 Bn for hydrogen development, part of which targets the deployment of 100 new hydrogen stations by 2027. In January 2025, TotalEnergies opened its first high-capacity 700-bar hydrogen refueling station for trucks along the A6 highway, signaling a shift from urban installations to long-haul corridors. The Netherlands, through the HyTrucks initiative, is creating a transnational corridor for hydrogen trucks connecting Rotterdam, Antwerp, and Duisburg. It plans to develop more than 30 high-flow stations by 2026.

Asia Pacific Hydrogen Refueling Stations Market Trends

In 2025, Asia Pacific is expected to account for approximately 68% of share due to various national strategies, state funding, and industrial partnerships. In Japan, the government aims to reach 320 stations by 2030 through its updated Basic Hydrogen Strategy (2023) to support a projected fleet of 200,000 FCEVs. Companies such as Iwatani Corporation and JX Nippon Oil & Energy dominate this field, investing in high-utilization stations with quick dispensing and on-site storage technologies.

Hyundai Motor Group’s based in South Korea, supports massive hydrogen ecosystem strategy. Under the government’s Hydrogen Economy Roadmap, the country targets over 310 stations by 2030. For instance, in March 2024, Hyundai inaugurated a hydrogen station in Ulsan designed specifically for its XCIENT Fuel Cell trucks, featuring a 1,000 kg/day capacity. In addition, the country is integrating hydrogen refueling within its smart city initiatives.

Competitive Landscape

The hydrogen refueling stations market is currently defined by fragmented regional leadership, strategic partnerships, and infrastructure expansion propelled by energy giants and mobility-focused start-ups. In Europe, companies such as Air Liquide are leading the charge with joint ventures to standardize station networks and offer cross-border hydrogen fueling access. Asia Pacific is also witnessing a strong push from government-backed players, including Japan’s JXTG Nippon Oil & Energy and South Korea’s Hyundai Oilbank. They are primarily scaling networks, often supported by national hydrogen roadmaps and subsidy programs.

Key Industry Developments

- In July 2025, FNM completed the construction of Lombardy's first hydrogen refueling station on Milan's eastern ring road in Carugate. It is a part of a US$ 60.4 Mn five-station network financed through PNRR and EU funds.

- In May 2025, a new high-capacity hydrogen refueling station entered operation in Düsseldorf. As per the project’s lead developer H2 MOBILITY, it is currently the most powerful facility of its kind in Europe. It has a daily refueling capacity of up to five tons of hydrogen.

Companies Covered in Hydrogen Refueling Stations Market

- Air Liquide

- Air Products and Chemicals

- Linde Group

- Nel Hydrogen

- H2 Mobility

- TotalEnergies

- Colruyt Group

- McPhy Energy SA

- Greenpoint

- SK Plug Hyverse

- ENEOS

- Japan H2 Mobility

- Sinopec

- Hynet

- Others

Frequently Asked Questions

The hydrogen refueling stations market is projected to reach US$ 968.4 Mn in 2025.

Decarbonization targets in transport and innovations in hydrogen storage technologies are the key market drivers.

The hydrogen refueling stations market is poised to witness a CAGR of 26.1% from 2025 to 2032.

Integration of digital tools for station monitoring and development of cross-border hydrogen mobility corridors are the key market opportunities.

Air Liquide, Air Products and Chemicals, and Linde Group are a few key market players.