- Mining & Services

- Mining Robotics Market

Mining Robotics Market Size, Share, and Growth Forecast 2026 - 2033

Mining Robotics Market Size, Share, and Growth Forecast 2026 – 2033 by Mining Technique (Open‑Pit Mining, Underground Mining), by Application (Drilling and Blasting, Hauling, Exploration, Excavation, Inspection and Maintenance, Others), by Regional Analysis, 2026 - 2033

Mining Robotics Market Size and Trend Analysis

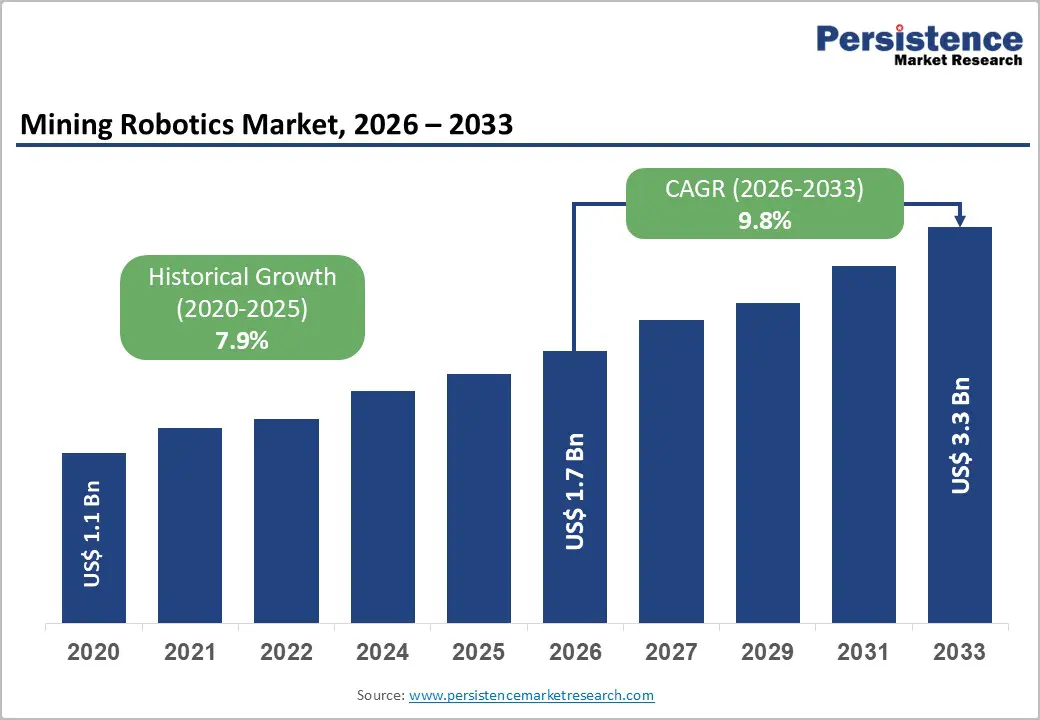

The global mining robotics market size is likely to be valued at US$ 1.7 Billion in 2026 and is expected to reach US$ 3.3 Billion by 2033, growing at a CAGR of 9.8% during the forecast period from 2026 to 2033. This expansion is underpinned by rising demand for automation in hazardous mining environments, persistent labor shortages, and the need to improve operational efficiency and safety across both open-pit and underground mines.

Key Market Highlights

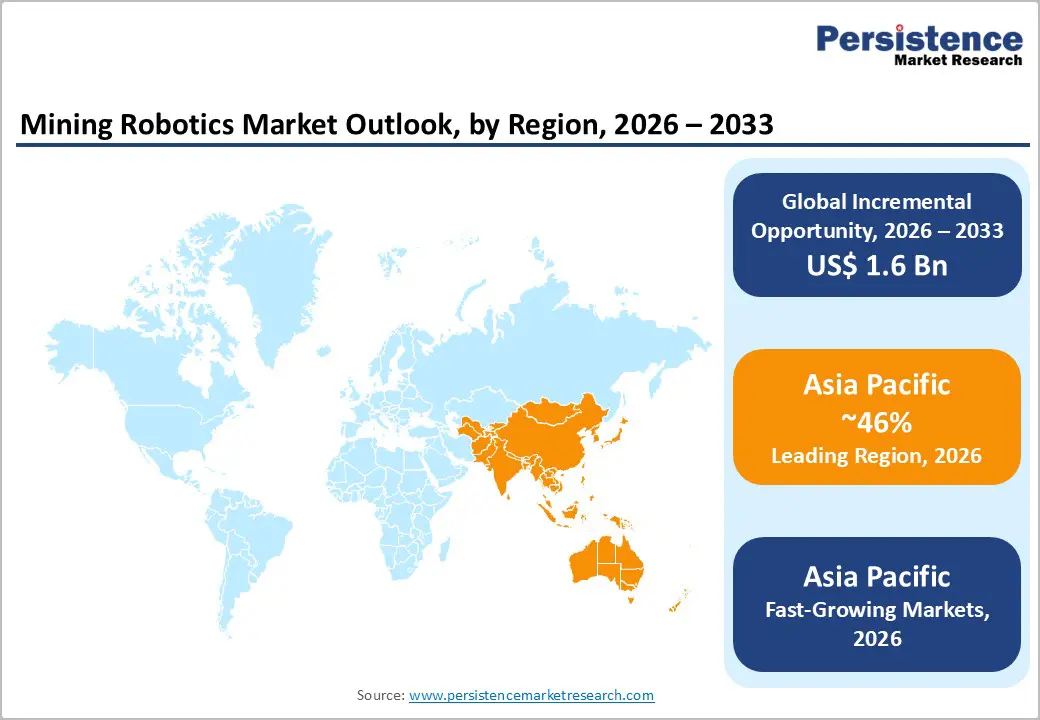

- Leading region: Asia Pacific dominates the mining robotics market, accounting for over 46% of the market share in 2025, driven by large-scale mining projects, government-backed automation initiatives, and rising mineral demand in China, India, and Australia.

- Fastest Growing Region: Asia Pacific is also the fastest-growing region, supported by rapid industrialization, labor shortages, and strong investments in smart mining and robotic exploration technologies.

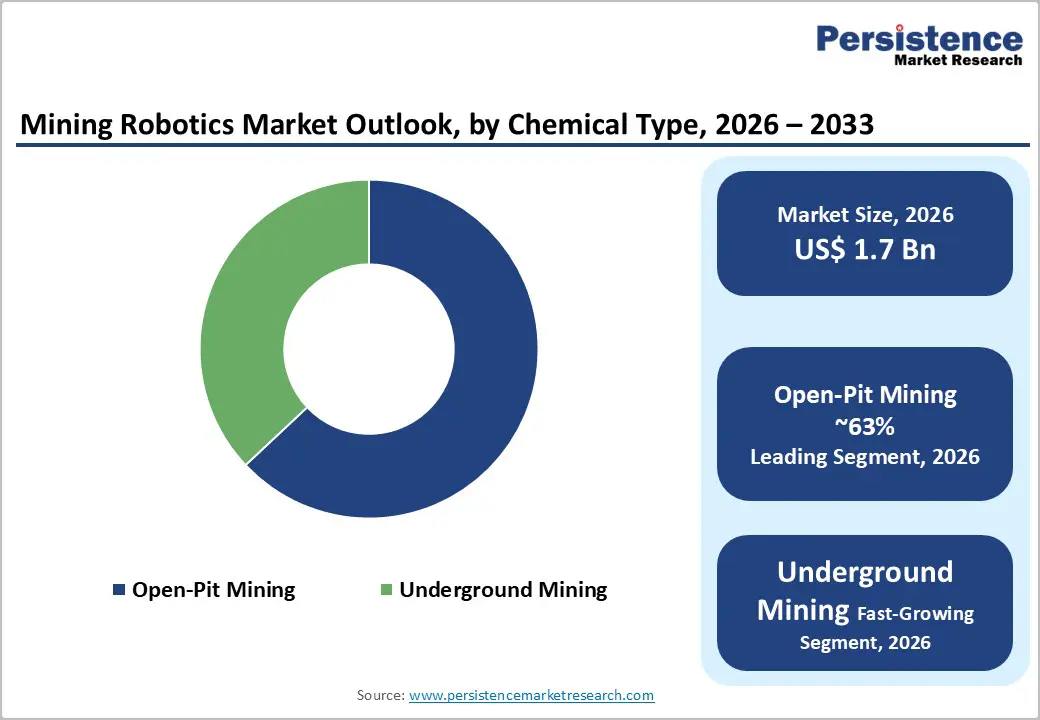

- Dominant Segment: Open-pit mining is the dominant segment by mining technique, accounting for approximately 63% of the market share in 2025 due to its suitability for large-scale autonomous haulage, drilling, and excavation.

- Fastest Growing Segment: Exploration is one of the fastest-growing application segments, as autonomous drones, AI-powered mapping, and robotic surveying tools accelerate mineral discovery for critical raw materials.

- Key Market Opportunity: The expansion of autonomous haulage, robotic drilling, and inspection and maintenance systems in open-pit and underground mines offers a major opportunity to improve safety, productivity, and sustainability across the mining robotics market.

| Key Insights | Details |

|---|---|

|

Mining Robotics Market Size (2026E) |

US$ 1.7 Billion |

|

Market Value Forecast (2033F) |

US$ 3.3 Billion |

|

Projected Growth CAGR (2026–2033) |

9.8% |

|

Historical Market Growth (2020–2025) |

7.9% |

Market Dynamics

Market Growth Drivers

Rising Safety and Regulatory Pressure in Hazardous Mining Environments

The mining robotics market is being propelled by intensifying safety and regulatory pressure in hazardous mining operations, where manual work exposes workers to rockfalls, gas hazards, and high-energy equipment. The U.S. Mine Safety and Health Administration (MSHA) recorded 31 mining fatalities in fiscal year 2024, sustaining a fatal-injury rate of 0.0110 per 200,000 hours worked, which has prompted regulators and operators to deploy autonomous haul trucks, remote-controlled drilling rigs, and inspection drones to reduce human exposure in open-pit and underground mines.

By automating high-risk tasks such as drilling and blasting, hauling, and inspection and maintenance, mining robotics can lower accident rates, cut insurance and compliance costs, and align with frameworks such as the Federal Mine Safety and Health Act, thereby creating a durable tailwind for the mining robotics market.

Labor Shortages and Productivity-Driven Automation in Large-Scale Mines

Persistent labor shortages and the need for continuous, high-throughput operations are accelerating automation in large-scale mining, making mining robotics a strategic lever for productivity. Studies on mining automation indicate that autonomous and semi-autonomous systems can increase productivity by 20% in mines that have implemented them, while also mitigating the effects of an aging workforce and declining interest in hazardous underground work. In North America and Australia, operators such as Rio Tinto have deployed mixed fleets of autonomous and manned haul trucks in open-pit operations.pit operations, achieving safer and more predictable cycle times.

In the Asia Pacific, countries like China and India face acute labor-supply constraints in coal, iron ore, and bauxite mining, which is pushing companies to adopt robotic loaders, autonomous haulage systems, and AI-driven fleet-management platforms. As mines seek to operate 24/7 without human fatigue and to stabilize output amid volatile commodity prices, demand for mining robotics in drilling, hauling, and excavation is expected to remain structurally elevated.

Market Restraints

High Capital Expenditure and Long Payback Periods

One of the primary restraints on the mining robotics market is the high upfront capital expenditure required for autonomous haul trucks, robotic drilling systems, and AI-powered monitoring platforms, which can be prohibitive for mid-sized and junior mining companies. The substantial cost of advanced autonomous machinery and the need to upgrade infrastructure, such as high-precision GPS, fiber-optic networks, and centralized control rooms, add to the financial burden, particularly in emerging markets with limited access to project financing.

Long payback periods, often stretching beyond five years, and fluctuating commodity prices can deter investment, especially when mines face electricity shortages or declining production volumes, as seen in parts of South Africa, where mining output fell by 7.7% year-on-year in recent data. These factors collectively slow the pace of adoption and constrain the addressable market for mining robotics among smaller operators.

Harsh Operating Conditions and Integration Complexity

Extreme environmental conditions and integration complexity also pose key restraints on the mining robotics market. Mines frequently operate in high-temperature, dusty, and corrosive environments that accelerate wear on robotic components, reduce reliability, and increase maintenance costs. Uneven terrain, narrow tunnels, and limited space in underground and open-pit mines complicate mobility and payload management, whereas payload limitations can reduce the cost-effectiveness of robotic systems relative to conventional heavy equipment.

In addition, integrating robotic fleets into legacy workflows, such as manual dispatch systems, mixed manned–autonomous traffic, and existing safety protocols, requires extensive re-engineering and workforce training, which can delay deployment timelines and raise operational risk. Until robust, modular, and interoperable mining robotics platforms are more widely standardized, these technical and operational hurdles will continue to constrain growth.

Market Opportunities

Expansion of Autonomous Haulage and Drilling in Open-Pit Mines

A major opportunity in the mining robotics market lies in the expansion of autonomous haulage and robotic drilling in open-pit mines, where large-scale, repetitive material-handling tasks offer the highest immediate return on automation. Open-pit mining accounted for over 63% of the mining robotics market share in 2025, driven by the need to automate hauling, drilling, and excavation in bulk-commodity operations such as coal, iron ore, and copper. In Australia, Rio Tinto operates one of the world’s largest fleets of autonomous haul trucks in the Pilbara region, achieving safer and more efficient transport of ore over long distances.

In China, a smart coal-mining project in the northwest set a global record for autonomous driving in 2024, with a mixed fleet of 56 driverless trucks and more than 800 manned vehicles operating safely since June 2024. As operators seek to reduce fuel consumption, optimize load cycles, and comply with carbon-intensity targets, investments in autonomous haulage systems and precision drilling robots are expected to grow rapidly, creating a substantial revenue pocket within the Mining Robotics Market.

Growth of Inspection, Exploration, and Underwater Robotics

Another significant opportunity stems from the growth of inspection, exploration, and underwater robotics, in which advanced AI, remote sensing, and submersible platforms are opening new frontiers in mineral discovery and asset integrity management. Exploration is among the fastest-growing applications in the mining robotics domain, driven by the need to identify critical raw materials such as lithium, cobalt, and rare earths for electric vehicles and renewable energy infrastructure.

Autonomous drones, ground-based inspection robots, and remote-controlled underwater vehicles (ROVs) are increasingly used for site surveys, geological mapping, and underwater mineral extraction, reducing exploration time and costs while minimizing environmental disruption. In India and Southeast Asia, mechanization of coal, iron ore, and bauxite mines is driving demand for robotic inspection systems that provide real-time monitoring of ventilation, slope stability, and equipment health. As governments and miners prioritize sustainable mining and deeper-resource access, the mining robotics market is well-positioned to capture value in inspection and maintenance, exploration, and subsea robotics.

Category-wise Insights

By Mining Technique Analysis

Within the mining technique category, open-pit mining is the leading segment, accounting for approximately 63% of the mining robotics market share in 2025. Is this dominance attributable to the widespread use of open-pit methods for extracting bulk commodities such as coal, iron ore, and copper, where large-scale, repetitive tasks are highly amenable to automation. Open-pit mines benefit from easier access to deposits, broader haul roads, and relatively predictable geometries, which facilitate the deployment of autonomous haul trucks, robotic drill rigs, and AI-enabled fleet-management systems.

Operators in Australia and North America have demonstrated that autonomous haulage systems can improve fuel efficiency and cycle-time consistency while reducing drivers' exposure to dust, noise, and fatigue-related risks. As global demand for bulk minerals remains robust and mines seek to extend the life of existing assets through higher-precision extraction, open-pit mining will continue to anchor the Mining Robotics Market.

By Application Analysis

Within the application category, hauling is the leading segment, accounting for approximately 33% of the mining robotics market share in 2025. This leadership reflects the critical role of material transportation in mine productivity and the strong economic case for autonomous haulage systems in large-scale open-pit operations. Hauling involves moving large volumes of ore and waste over long distances, often under harsh conditions, where autonomous trucks can operate 24/7 without driver fatigue, reduce fuel consumption through optimized routing, and lower labor costs.

Rio Tinto’s Pilbara operations in Australia have demonstrated that mixed fleets of autonomous and manned haul trucks can achieve higher utilization rates and safer traffic management. In China, the smart coal mining project with 56 driverless trucks illustrates how hauling robotics can scale across complex, multi-shift environments. As mines pursue carbon-intensity reduction and operational resilience, hauling will remain the dominant application segment in the mining robotics market .

Regional Insights

North America Mining Robotics Market Trends

North America leads the Mining Robotics Market in terms of technological maturity and regulatory-driven adoption, with the United States at the forefront of autonomous haulage, robotic drilling, and digital-mine initiatives. The U.S. Mine Safety and Health Administration (MSHA) has recorded 31 mining fatalities in fiscal year 2024, sustaining a fatal-injury rate of 0.0110 per 200,000 hours worked, which has intensified pressure on operators to deploy robotic systems that minimize human exposure in open-pit and underground environments.

Major miners such as Caterpillar, Komatsu, and Epiroc are collaborating with technology partners to roll out autonomous haul trucks, remote-controlled loaders, and AI-enabled fleet-management platforms across coal, copper, and gold operations. In Canada, the Survey of Advanced Technology indicated that only about 2.0% of Canadian enterprises had adopted robotics technologies as of 2022, highlighting a substantial untapped opportunity as labor costs rise and the workforce ages. The region’s strong innovation ecosystem, supported by national laboratories, universities, and venture capital, continues to drive advancements in AI-driven autonomy, sensor fusion, and edge-computing for mining robotics.

Europe Mining Robotics Market Trends

Europe is witnessing a steady expansion of the Mining Robotics Market, driven by advanced R&D ecosystems, sustainability mandates, and harmonized regulatory frameworks across key markets, including Germany, the United Kingdom, France, and Spain. The European Union has prioritized sustainable mining and circular-economy objectives, encouraging operators to adopt robotic systems that reduce energy consumption, minimize waste, and lower emissions.

In Germany, companies such as ABB, KUKA AG, and HollySys are integrating industrial robotics and automation into underground and surface mining workflows, while in Scandinavia, Epiroc and Sandvik AB are deploying autonomous drilling rigs and remote-controlled loaders in deep--evil iron ore and base-metal mines. The EU’s focus on critical raw materials and strategic autonomy is further accelerating investments in robotic exploration, inspection, and maintenance technologies. As environmental compliance requirements tighten and mines seek to operate in deeper, more complex geologies, Europe is expected to maintain a strong, innovation-driven presence in the Mining Robotics Market.

Asia Pacific Mining Robotics Market Trends

Asia Pacific is projected to account for over 46% of the mining robotics market share in 2025, making it the largest regional market and a key growth engine for the mining robotics market . Is China actively transitioning many open-pit coal operations to underground methods to reduce environmental impact and improve efficiency, while simultaneously investing in smart mining projects that integrate autonomous haul trucks, robotic drill rigs, and AI-driven monitoring systems. A smart coal mining project in northwest China set a global record for autonomous driving in 2024, with 56 driverless trucks and over 800 manned vehicles operating safely since June 2024, showcasing the scalability of mining robotics in large-scale operations.

In Japan, a startup has developed a mine-clearing support robot using compressed-air excavation technology, which has been trialed in Cambodia and is slated for deployment in Ukraine, demonstrating the cross-border applicability of mining robotics. In India, mechanization of coal, iron ore, and bauxite mines, coupled with labor shortages and heightened safety concerns, is driving demand for robotic loaders, autonomous haulage, and inspection drones. The region’s manufacturing advantages, government-backed industrial modernization programs, and growing mineral demand position Asia-Pacific as the fastest-growing hub for the deployment of mining robotics.

Competitive Landscape

The mining robotics market is moderately consolidated, with leading players such as Sandvik AB, ABB, Komatsu Ltd., Caterpillar, Epiroc, Hitachi Construction Machinery Co., Ltd., Rockwell Automation, HollySys, Cognex Corporation, KUKA AG, Hexagon AB, and Autonomous Solutions, Inc. collectively holding a significant share of the market. The top players account for over 40% of the market in 2024, indicating a consolidated but innovation-driven structure. Companies are pursuing AI-enabled autonomy, electrification, and advanced sensor integration to differentiate their offerings, while also emphasizing modular robotics platforms that lower deployment and maintenance costs.

Strategic moves include joint ventures, technology partnerships, and acquisitions to strengthen software capabilities, cloud-based analytics, and digital-twin solutions. Emerging business models such as robotics-as-a-service (RaaS) and performance-based contracts are gaining traction, enabling smaller miners to access mining robotics without large upfront investments. As regulatory pressure, sustainability goals, and labor-cost dynamics intensify, competition is shifting from hardware alone to integrated solutions that combine robotics, AI, and data analytics.

Key Market Developments

- In June 2024: A smart coal mining project in northwest China deployed a mixed fleet of 56 driverless trucks alongside over 800 manned vehicles, setting a global benchmark for autonomous mining scalability in large open-pit operations.

- In March 2025, Rio Tinto expanded its autonomous haulage system in the Pilbara, adding more autonomous haul trucks to its mixed fleet, boosting fuel efficiency, safety, and operational continuity in one of the world’s largest iron-ore mining regions.

- In October 2024: A Japanese startup, IOS Inc., introduced a compressed-air excavation mine-clearing support robot successfully trialed in Cambodia and slated for deployment in Ukraine, demonstrating robotics’ potential to improve safety and efficiency in dangerous demining operations.

Companies Covered in Mining Robotics Market

- Sandvik AB

- ABB

- Komatsu Ltd.

- Caterpillar

- Epiroc

- Hitachi Construction Machinery Co., Ltd.

- Rockwell Automation

- HollySys

- Cognex Corporation

- KUKA AG

- Hexagon AB

- Autonomous Solutions, Inc.

- Others

Frequently Asked Questions

The global mining robotics market is projected to be valued at US$1.6 Bn in 2025.

The need for enhanced safety, operational efficiency, and productivity in hazardous mining environments is a key driver of the market.

The mining robotics market is poised to witness a CAGR of 9.8% from 2025 to 2032.

Advancements in autonomous robotics and AI-driven systems are creating strong growth opportunities.

Sandvik AB, ABB, Komatsu Ltd., Caterpillar, Epiroc, Hitachi Construction Machinery Co., Ltd., Rockwell Automation, HollySys are among the leading key players.