- Processed Food

- Canned Food Market

Canned Food Market Size, Share, and Growth Forecast, 2026 – 2033

Canned Food Market by Product Type (Canned Fruits, Canned Vegetables, Canned Meat, Canned Seafood, Canned Ready Meals, Canned Soups, Canned Pet Food), Packaging Type (Metal Cans, Aluminum Cans, Composite Cans), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores), and Regional Analysis for 2026-2033

Canned Food Market Share and Trends Analysis

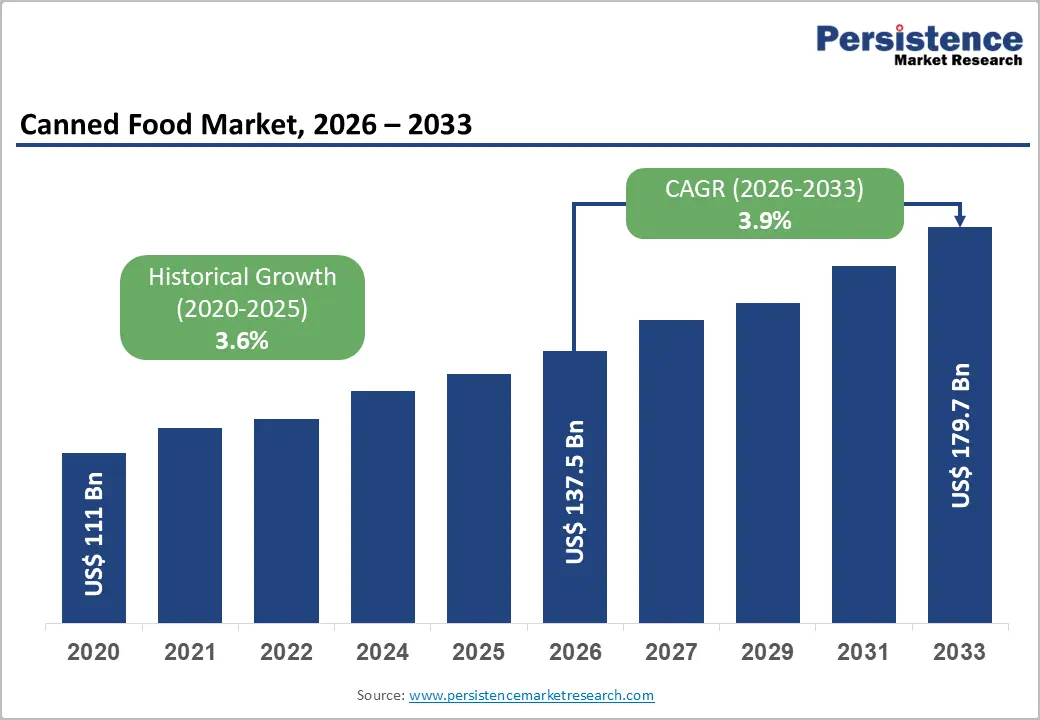

The global canned food market size is likely to be valued at US$ 137.5 billion in 2026, and is projected to reach US$ 179.7 billion by 2033, growing at a CAGR of 3.9% during the forecast period 2026−2033. Population growth and urbanization are primary drivers for the expansion of this market, along with a surging demand for convenient, long-shelf-life food products. Aging populations and changing household compositions have shifted consumption patterns toward canned foods due to their reliability and accessibility.

Technological advancements in preservation, packaging, and distribution enhanced product quality and reduced spoilage, facilitating wider adoption. Increased awareness of nutritional content and safety standards has strengthened consumer confidence in canned food. Retail expansion and digital commerce channels are improving market accessibility and supporting consistent growth across diverse demographics. Evolving regulatory frameworks on food safety and labeling further reinforce market credibility.

Key Industry Highlights

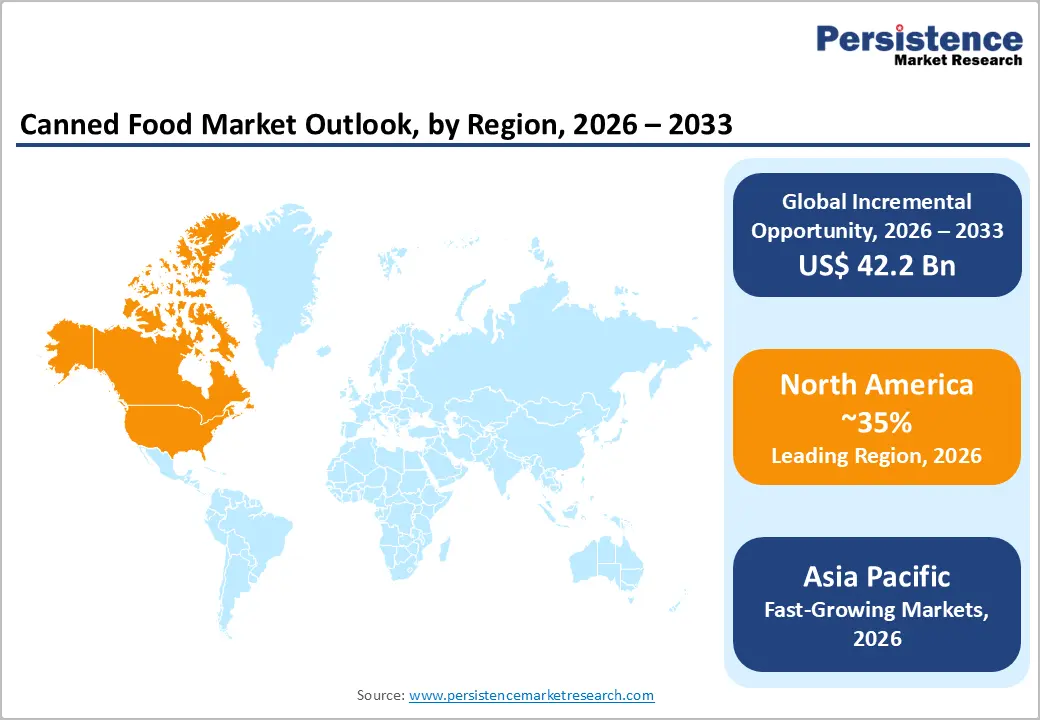

- Dominant Region: By 2026, North America is projected to lead with approximately 35% share, supported by advanced food-processing infrastructure and strong penetration of organized retail.

- Fastest-growing Regional Market: Asia Pacific is projected to be the fastest-growing market between 2026 and 2033, driven by rapid urbanization and expansion of modern and digital retail.

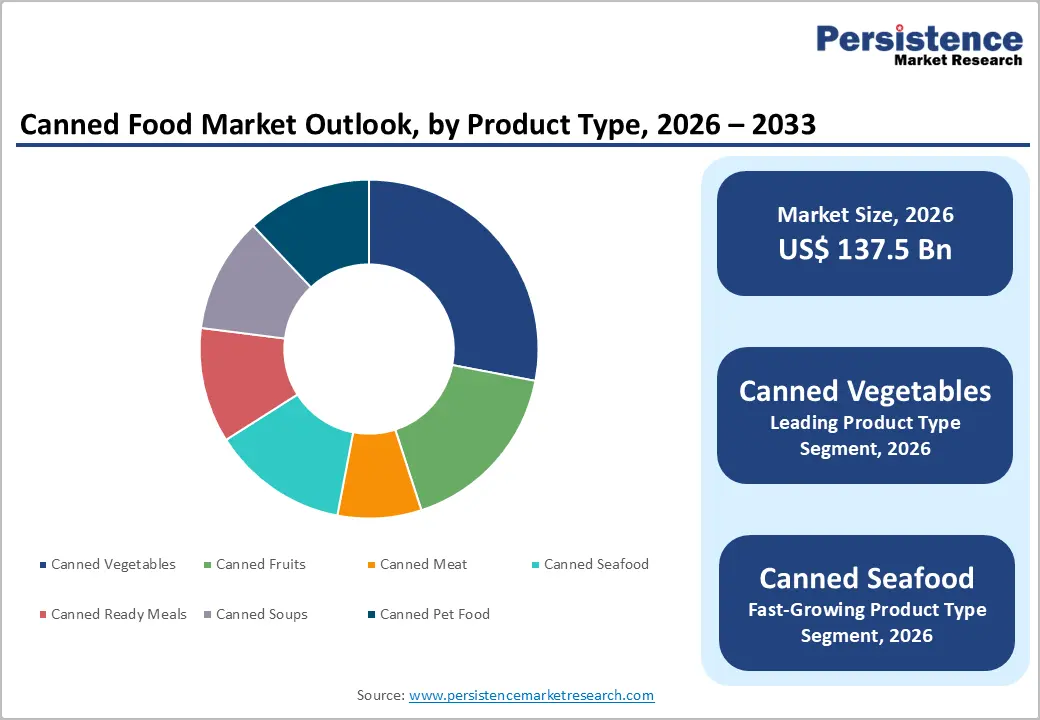

- Leading Product Type: Canned vegetables are expected to lead the market, accounting for about 28% of revenue in 2026, driven by broad consumer acceptance, convenience, and nutritional reliability.

- Fastest-growing Product Type: Canned seafood is expected to grow the fastest through 2033, boosted by advanced preservation techniques and convenient packaging innovations.

| Key Insights | Details |

|---|---|

| Canned Food Market Size (2026E) | US$ 137.5 Bn |

| Market Value Forecast (2033F) | US$ 179.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Urban Expansion and Lifestyle Evolution

Rapid urban development has altered consumption patterns, creating a preference for foods that align with fast-paced routines. Population growth in urban centers leads to increased demand for ready-to-use, shelf-stable food options suitable for working individuals and households with limited time for meal preparation. Urban dwellers face space constraints, limiting storage of perishable goods, which elevates reliance on preserved food solutions. Analyses by the United Nations indicate that over 55% of the global population resides in urban areas, a trend projected to rise to 68% by 2050, highlighting the structural shift in consumer behavior toward convenience-focused diets.

Changing lifestyle priorities influence purchasing behavior, where convenience, nutrition, and reliability dominate decision-making. Dual-income households and increased workforce participation result in higher consumption of long-lasting, easy-to-store foods that require minimal preparation. Retail expansion and accessibility of processed foods within urban markets amplify exposure and adoption, while technological integration in packaging and preservation ensures consistent quality and safety standards. Supply chain efficiencies, including cold chain systems, support timely distribution, meeting the expectations of urban consumers for readily available food products.

Health Concerns over Additives

Chemical additives in canned foods have become a strategic concern due to rising scrutiny over their potential impact on human health. Compounds used in can linings and preservatives can migrate into food during processing and storage, creating exposure pathways that attract regulatory and public attention. A large cohort study tracking dietary exposure found that consumption of two or more canned foods was associated with up to a 54% increase in urinary bisphenol A (BPA) concentrations compared with no canned food consumption, indicating substantial internal exposure to this endocrine active compound. This measurable uptake of a known industrial chemical drives consumer perception that canned products carry hidden health risks. Market data show that informed consumers, particularly those in higher income segments or with health oriented preferences, increasingly pivot away from food products associated with synthetic additives and toward fresh or minimally processed alternatives. The shifting preference presents a tangible demand headwind for products perceived as containing higher levels of chemical residues.

From an operational standpoint, legislative bodies and food safety authorities are strengthening frameworks for permissible additive levels and labelling transparency. Retailers and food service chains adjust sourcing strategies to align with evolving standards and customer expectations, prompting producers to invest in reformulation, substitute materials, or third party certification. Risk management costs rise when brands must substantiate claims of safety or defend against adverse publicity. These factors reduce pricing flexibility and compress margins in categories where legacy products rely on additive based shelf life extensions.

Product Innovation and Health-Oriented Offerings

Rising consumer focus on wellness and convenience is reshaping demand toward offerings that deliver both nutritional value and ease of use. Urban consumers increasingly prioritize time-efficient solutions without compromising dietary standards, creating demand for products with reduced sodium, sugar, and preservatives, as well as fortified options enriched with vitamins, minerals, and protein. Manufacturers responding to these preferences differentiate their portfolios through innovative packaging, functional ingredients, and flavor diversification. This approach strengthens brand positioning, encourages repeat purchase, and enhances perceived value among health-conscious segments, generating new revenue streams and improving customer loyalty.

Emerging dietary trends such as plant-based diets, clean-label preferences, and specialized nutrition for active lifestyles are influencing product development strategies. Firms introducing solutions aligned with these trends capture a growing segment seeking functional benefits, convenience, and transparent ingredient sourcing. Investment in research and development enables faster adaptation to shifting consumption patterns, while collaborations with nutrition experts or certification bodies reinforce credibility and trust. Innovation that integrates health benefits with taste and convenience fosters competitive advantage, enhances portfolio relevance, and drives adoption across diverse demographic segments, creating sustainable growth opportunities.

Category-wise Analysis

Product Type Insights

Canned vegetables are expected to be the leading segment, accounting for 28% of revenue in 2026, due to their widespread acceptance, consistent nutritional value, and versatility across household and institutional applications. Consumers prefer canned vegetables for convenience, extended shelf life, and reliability in meeting dietary requirements. Retail availability in supermarkets, convenience stores, and online platforms ensures accessibility. Government nutrition programs often emphasize vegetable intake, supporting steady demand. Technological improvements in canning preserve color, texture, and nutrient content, reinforcing adoption. Institutional buyers, including hospitals and educational institutions, rely on canned vegetables for predictable quality and storage efficiency, contributing to revenue stability.

Canned seafood is expected to witness the fastest growth between 2026 and 2033, as consumer preference shifts toward protein-rich and omega-3-fortified options. Advances in preservation techniques, including vacuum sealing and temperature-controlled logistics, maintain freshness and reduce spoilage. Expanding global trade networks enable cross-border distribution, meeting rising demand in regions with limited local seafood production. Health-conscious consumers and specialty diet trends support growth. Packaging innovations, such as easy-open and portion-controlled cans, enhance convenience and adoption rates.

Packaging Type Insights

Metal cans are poised to lead, with a forecasted over 60% share of the canned food market revenue in 2026, owing to durability, long shelf life, and consumer trust. The robust construction of metal cans ensures protection against physical damage during handling and transportation, reducing product losses and returns. Their ability to maintain optimal food safety standards and preserve flavor integrity enhances consumer confidence. Retailers value metal cans for efficient storage, uniform stacking, and standardization across multiple product lines, which simplifies inventory management. Regulatory approval for food-grade metals further reinforces credibility. Sustainability initiatives, including high recyclability rates, appeal to environmentally conscious consumers and support corporate responsibility goals, while compatibility with automated filling and sealing systems drives operational efficiency.

Composite cans are anticipated to be the fastest-growing segment between 2026 and 2033, driven by lightweight design, eco-friendly materials, and compatibility with digital commerce logistics. Their reduced weight makes them easier to transport and handle, reducing shipping costs and carbon emissions. Consumers increasingly prefer portable, easy-to-store packaging that suits on-the-go lifestyles and limited household storage space. Composite cans offer flexibility in shape, design, and branding, improving shelf presence and product differentiation. Energy-efficient manufacturing reduces production costs and environmental footprint, supporting sustainability initiatives. The expansion of online retail and direct-to-consumer channels is stimulating demand for protective, lightweight packaging, enhancing the appeal of composite cans amid evolving distribution and consumption patterns.

Distribution Channel Insights

Supermarkets and hypermarkets are the leading segment, accounting for nearly 50% of the canned food market share in 2026, supported by wide distribution reach, organized retail systems, and bulk purchasing capacity. Extensive shelf management strategies and visually appealing promotional displays drive product visibility and consumer engagement. Partnerships with logistics providers optimize stock replenishment and ensure timely product availability across multiple locations. Consumer confidence in pricing, quality, and standardized shopping experiences is reinforced through consistent retail practices. The expansion of hypermarket chains and retailer consolidation enables cost efficiencies, improved supply chain coordination, and streamlined procurement processes.

Online retail is expected to emerge as the fastest-growing segment between 2026 and 2033, driven by digital adoption, convenience, and accessibility. E-commerce platforms offer personalized promotions, subscription-based services, and direct engagement with consumers, enhancing loyalty and repeat purchases. Advanced logistics networks, including cold-chain integration and last-mile delivery optimization, maintain product quality and reliability. Growing urbanization and increasing mobile device penetration drive digital purchasing to improve time efficiency and access a wider range of products. User-friendly mobile applications and seamless digital payment systems simplify transactions and increase adoption rates.

Regional Insights

North America Canned Food Market Trends

By 2026, North America is expected to lead with an estimated 35% of the canned food market share, supported by mature food processing infrastructure, high penetration of organized retail, and strong consumer reliance on shelf-stable food products. Established manufacturing clusters enable large-scale production, consistent quality control, and cost-efficient operations, reinforcing competitive pricing and steady supply. Advanced ambient logistics and warehousing systems ensure nationwide distribution with minimal spoilage risk. Purchasing behavior favors convenience, extended shelf life, and regulatory compliance, aligning closely with canned food attributes. High penetration of private-label products across large retail chains strengthens volume movement and category stability.

Market leadership is further reinforced by strong brand consolidation, innovation capacity, and institutional demand channels. Leading producers maintain diversified portfolios across proteins, vegetables, and ready meals, enabling optimized shelf placement and cross-category efficiencies. Automation, predictive inventory management, and data-driven demand forecasting enhance operational resilience and margin stability. Public food programs, foodservice procurement, and emergency preparedness stockpiling generate recurring bulk demand independent of retail seasonality. Regulatory clarity around packaging, labeling, and food safety accelerates product commercialization and reduces compliance risk, sustaining long-term dominance in value and volume performance.

Europe Canned Food Market Trends

Europe is expected to occupy a pivotal place in the market for canned food products through 2033 due to strong regulatory frameworks, sustainability-driven consumption patterns, and consistent demand for high-quality preserved food products. Strict food safety and labeling standards reinforce consumer confidence and support long-term adoption across organized retail channels. High penetration of private-label offerings enables competitive pricing while maintaining quality benchmarks. Emphasis on environmentally responsible packaging accelerates use of recyclable metal formats and low-impact materials. Consumption trends reflect preference for portion-controlled, nutritionally balanced products aligned with smaller household sizes and aging demographics, sustaining steady category relevance.

Market performance is further supported by operational efficiency, product refinement, and integrated trade networks. Manufacturers prioritize clean-label formulations, reduced sodium content, and organic-certified options to address health-oriented purchasing behavior. Advanced logistics infrastructure facilitates efficient cross-border distribution, reducing supply chain friction and inventory risk. Retailers apply data-driven category management to optimize shelf space and improve turnover rates. Institutional demand from hospitality, public catering, and public supply programs provides volume stability beyond household consumption.

Asia Pacific Canned Food Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market for canned food from 2026 to 2033, stimulated by accelerated urban expansion, rising workforce participation, and increasing preference for time-efficient food solutions. Dense urban populations and longer commuting patterns elevate demand for shelf-stable products that support consistent meal planning and reduced preparation time. Expansion of modern retail chains and convenience store formats improves penetration across metropolitan and tier-two cities, strengthening volume throughput. Localized manufacturing investments enhance supply reliability and price competitiveness, while reduced dependence on imports shortens lead times. Rapid growth of digital grocery platforms increases product visibility and enables efficient demand aggregation, reinforcing sustained consumption growth.

Growth momentum is further reinforced by adaptive product strategies and evolving food security priorities. Manufacturers align formulations, portion sizes, and flavor profiles with domestic dietary habits, improving acceptance and repeat purchase rates. Public initiatives focused on food safety, emergency preparedness, and reduction of agricultural waste indirectly support preserved food formats. Rising awareness of hygiene standards shifts demand toward packaged alternatives with verified quality controls. Capital deployment into processing automation, packaging efficiency, and shelf-life optimization improves operational scalability.

Competitive Landscape

The global canned food market structure exhibits moderate consolidation, with leading players such as Nestlé S.A., Conagra Brands, Inc., Hormel Foods Corporation, The Campbell's Company, and Thai Union Group PCL collectively accounting for an estimated 45% of total value share. Competitive positioning is driven by extensive product portfolios spanning vegetables, ready meals, proteins, and seafood, supported by large-scale processing capabilities and global sourcing networks. Continuous investment in product reformulation, shelf-life optimization, and packaging efficiency strengthens brand relevance across retail and foodservice channels. Advanced manufacturing automation, standardized quality controls, and procurement scale enable cost efficiency and consistent supply, creating entry barriers for smaller producers and reinforcing leadership positions.

Competitive intensity and concentration vary by geography and channel structure. Large multinational players dominate organized retail and institutional supply chains through strong distributor relationships, private-label partnerships, and high-volume contracts. In emerging consumption centers, regional and local producers maintain presence through localized flavors, price-sensitive offerings, and shorter supply chains. Strategic priorities increasingly focus on health-oriented formulations, sustainability-aligned packaging, and portfolio premiumization to protect margins amid input cost volatility. Expansion of digital commerce, foodservice recovery, and emergency stockpiling programs creates diversified demand streams.

Key Industry Developments

- In January 2026, Fresh Del Monte Produce announced that it will be acquiring the packaged and prepared food assets of California-based former canned food giant Del Monte Foods for US$ 285 million, reuniting the iconic Del Monte brand under one owner for the first time in nearly 40 years as part of a court-supervised bankruptcy sale.

- In October 2025, Tiger Brands’ former Langeberg & Ashton Foods canned fruits facility in Ashton, South Africa, reopened under new ownership as Langeberg Foods (Pty) Ltd, securing operations and preserving over 3,000 jobs after a multi-year sale process involving local fruit growers and Norfund.

- In May 2025, Portland-based canned food startup Heyday Canning Co. introduced a new seasoned bean line called Perfectly Seasoned Beans featuring varieties such as chickpeas, black beans, pinto beans, and cannellini beans designed to elevate home cooking with ready-to-use, flavorful ingredients.

Companies Covered in Canned Food Market

- Nestlé S.A.

- Conagra Brands, Inc.

- Hormel Foods Corporation.

- The Campbell's Company.

- Thai Union Group PCL.

- Del Monte Foods Corporation II Inc.

- Kraft Heinz, Inc.

- Ajinomoto Co., Inc.

- Bolton Group

- Princes Group plc.

- Ardo

Frequently Asked Questions

The global canned food market is projected to reach US$ 137.5 billion in 2026.

Soaring demand for long shelf life, convenience, food safety, affordability, and evolving urban consumption patterns are driving the market.

The market is poised to witness a CAGR of 3.9% from 2026 to 2033.

Key market opportunities arise from product innovation, health-oriented formulations, sustainable packaging adoption, and expansion of digital and modern retail distribution channels in developing economies.

Some of the key market players include Nestlé S.A., Conagra Brands, Inc., Hormel Foods Corporation, The Campbell's Company, and Thai Union Group PCL.