- Retail

- Agarwood Chips Market

Agarwood Chips Market Size, Share, and Growth Forecast 2026 - 2033

Agarwood Chips Market by Nature (Organic, Conventional), by End Use (Incense Stick, Fragrances, Retail/Household, Specialty Clinics, Others), by Distribution Channel (Business to Business (B2B), Business to Consumers (B2C)), by Regional Analysis, 2026 - 2033

Agarwood Chips Market Size and Trend Analysis

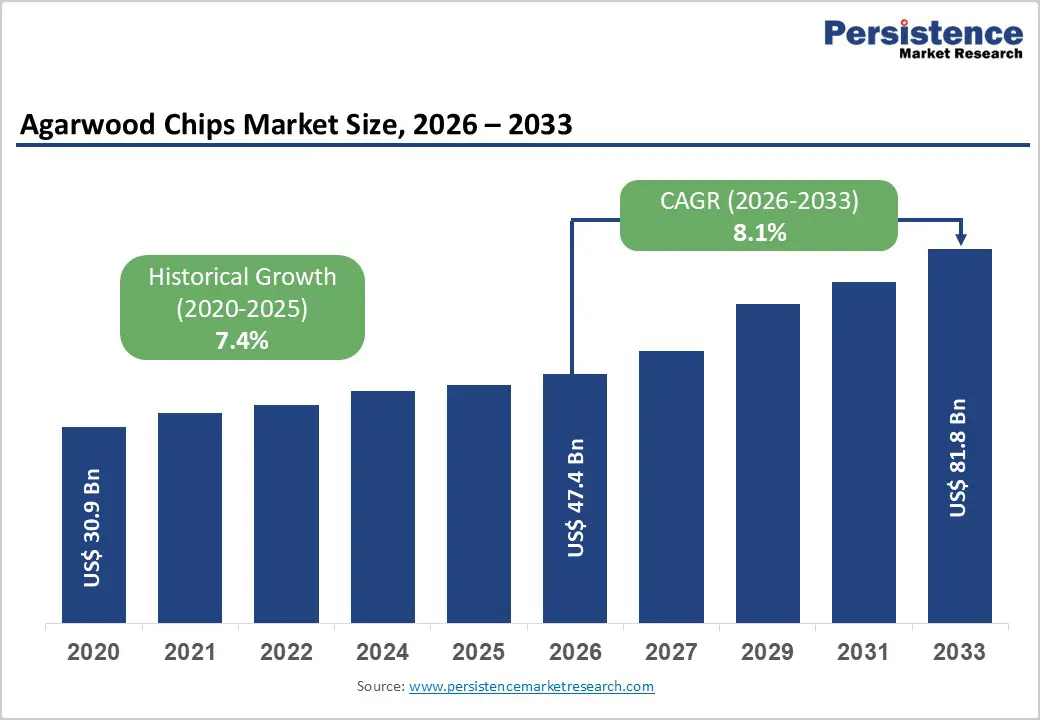

The global agarwood chips market size is expected to be valued at US$ 47.4 billion in 2026 and projected to reach US$ 81.8 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033.

This growth is driven by rising global demand for premium aromatics used in perfumery, incense, and spiritual rituals. Increasing disposable incomes in emerging economies, particularly across Asia and the Middle East, are strengthening demand for luxury fragrance products. Cultural revival of traditional incense practices further supports demand. Additionally, expanding cultivation initiatives and improving the export performance of essential oils enhance supply chain efficiency and reinforce the market’s long-term expansion outlook.

Key Industry Highlights:

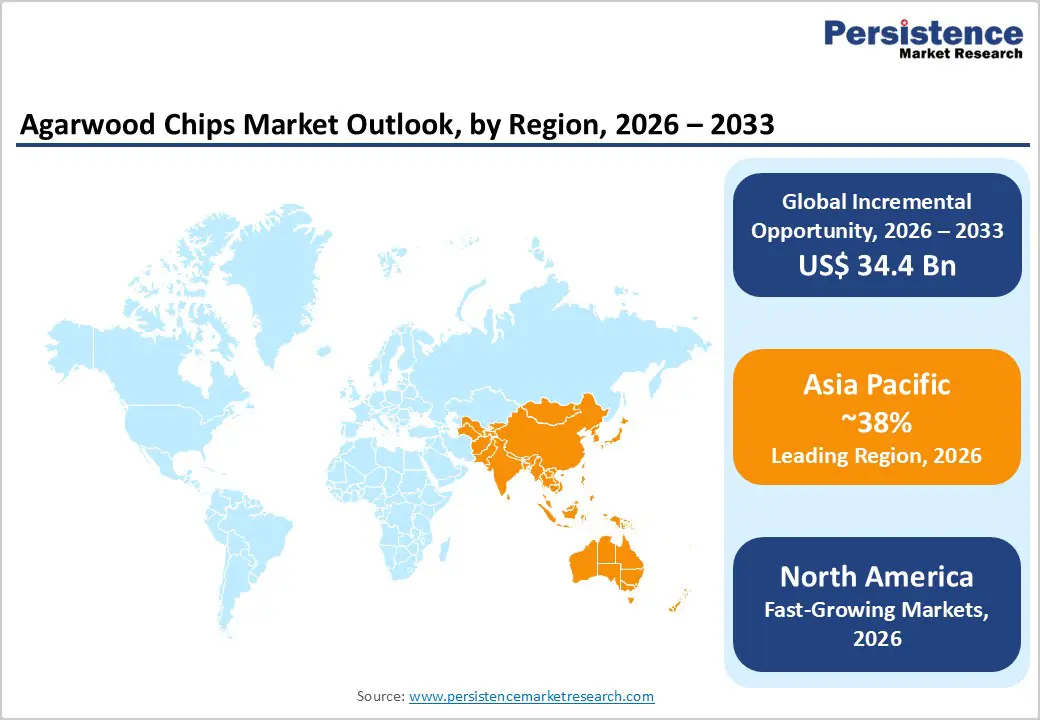

- Leading Region: Asia Pacific leads with 38% share in 2025, supported by dominant production bases and strong cultural and spiritual demand across China, India, and Southeast Asia.

- Fastest Growing Region: North America is projected to grow at a CAGR of 7.2% (2026 - 2033), driven by premium wellness adoption and expanding niche fragrance demand.

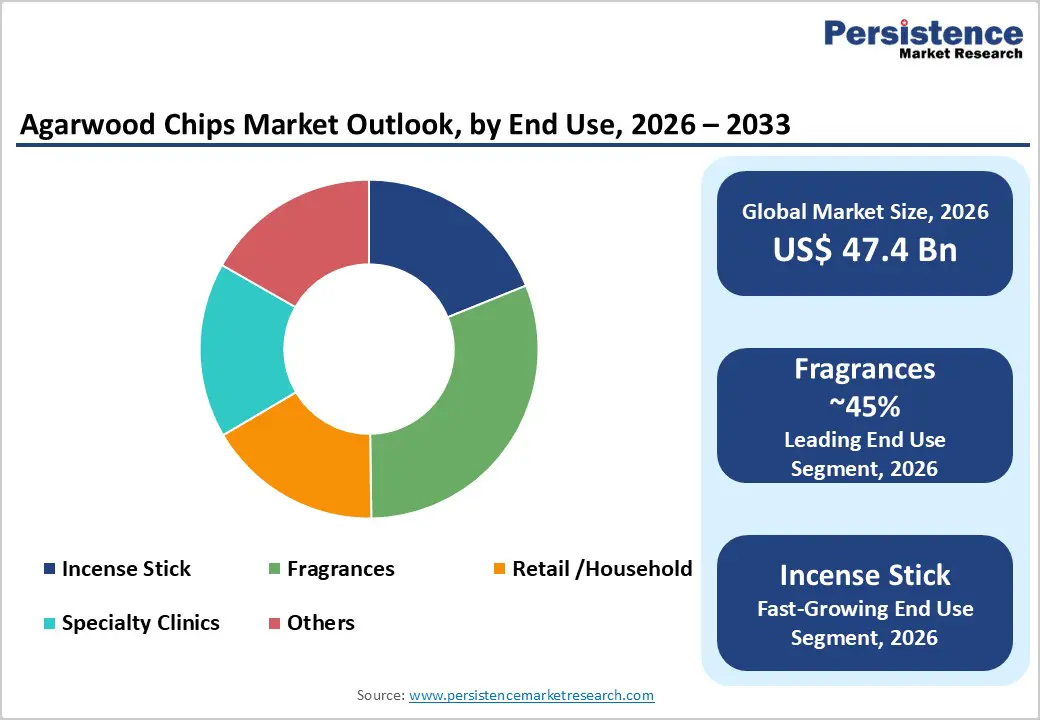

- Leading End-Use Segment: Fragrances hold 45% share in 2025, reflecting strong integration of oud notes in luxury and niche perfumery portfolios.

- Leading Distribution Channel: B2B accounts for 60% share in 2025, supported by bulk procurement contracts with incense manufacturers and perfume houses.

- Key Growth Opportunity: Organic-certified agarwood in wellness and spa applications presents major potential, aligning with expanding global holistic therapy demand.

| Key Insights | Details |

|---|---|

| Agarwood Chips Size (2026E) | US$ 47.4 billion |

| Market Value Forecast (2033F) | US$ 81.8 billion |

| Projected Growth CAGR (2026 - 2033) | 8.1% |

| Historical Market Growth (2020 - 2025) | 7.4% |

Market Dynamics

Drivers - Rising Demand in Luxury Fragrances and Perfumery

The escalating integration of agarwood chips into high-end perfumes is a key growth catalyst, as luxury fragrance houses increasingly seek authentic, resin-rich oud notes for premium scent portfolios. Global perfume exports expanded by 12% in 2024, according to International Trade Centre data, with agarwood-infused variants capturing higher-value segments due to their exclusivity and depth of aroma.

Consumer preference for natural and ethically sourced ingredients further accelerates demand. A 20% surge in natural fragrance sales highlights shifting millennial and Gen Z buying behavior. Additionally, regulated cultivation under CITES frameworks ensures traceable, sustainable supply, strengthening brand credibility and supporting broader market penetration across luxury retail channels.

Surge in Spiritual and Wellness Applications

Agarwood chips play a vital role in incense burning, meditation, and holistic wellness practices, particularly across Asia-Pacific markets. Traditional medicine industries are expanding at nearly 10% annually, with agarwood widely utilized in Ayurveda and Traditional Chinese Medicine for relaxation and stress management, reinforcing its relevance beyond perfumery.

Rising spiritual engagement also sustains steady consumption. Surveys indicate that a majority of Southeast Asian households regularly use incense for worship and rituals. Parallel sustainable cultivation programs promoted by environmental bodies encourage plantation-based sourcing, enabling scalable production while reducing pressure on wild forests to meet growing global wellness demand.

Restraints - Regulatory Hurdles and Sustainability Concerns

Stringent international trade regulations under CITES create operational bottlenecks, as Appendix II listings require mandatory export permits and documentation, often delaying shipments and increasing compliance costs. A significant share of agarwood species remains threatened, prompting production quotas in key exporting nations such as Indonesia and Vietnam, which restricted nearly one-quarter of shipments in 2024.

These regulatory requirements disproportionately impact small-scale producers lacking administrative capacity to meet complex documentation standards. Limited export approvals and quota systems tighten global supply, elevate raw material prices, and reduce accessibility for mid-tier buyers, including household incense retailers and regional fragrance manufacturers.

Supply Chain Vulnerabilities and Adulteration Risks

Illegal harvesting and adulteration present persistent challenges, undermining transparency and buyer confidence in international trade. A considerable portion of globally traded agarwood is estimated to be counterfeit or blended with lower-grade substitutes, eroding brand trust and increasing verification costs for importers and distributors.

Additionally, climate-related disruptions across major ASEAN producing regions have triggered production volatility, with output declines reported in 2025 due to extreme weather events. These vulnerabilities heighten procurement risks, complicate long-term supply contracts, and restrict expansion in highly regulated markets such as Europe and North America.

Opportunities - Expansion into Organic Certification and E-Commerce

Producers can unlock premium positioning by obtaining organic and sustainability certifications, as certified products often command price premiums of up to 30% in international markets. Growing consumer preference for traceable and eco-friendly aromatics strengthens opportunities for plantation-based agarwood suppliers aligned with global sustainability frameworks.

Simultaneously, rapid expansion of e-commerce platforms enables direct-to-consumer outreach, particularly among wellness-focused buyers seeking niche incense and oud products. Online retail for specialty aromatics is projected to grow steadily, while supportive policies under sustainability initiatives such as the EU Green Deal encourage certified sourcing and responsible trade practices.

Emerging Wellness and Spa Sector Demand

The expanding global wellness economy presents high-margin growth avenues for agarwood chip suppliers. With the wellness sector projected to reach multi-trillion-dollar valuation levels, spas and holistic therapy centers increasingly incorporate oud-based infusions and aromatic treatments to enhance premium service offerings.

Rising exports of herbal and traditional health products further indicate growing institutional demand. Hundreds of thousands of spas, alternative medicine centers, and specialty clinics worldwide are adopting natural aromatics in therapies, positioning agarwood chips as a valuable ingredient within relaxation, stress-relief, and luxury wellness experiences.

Category-wise Analysis

Nature Insights

The Organic segment dominates the agarwood chips market, accounting for 55% share in 2025, supported by rising consumer preference for chemical-free and sustainably sourced aromatics. Growing health consciousness and environmental awareness across Europe and North America reinforce this leadership position. Demand for certified organic essential oils continues to rise steadily, while global organic bodies report a significant transition of agarwood plantations toward certified cultivation practices by 2025.

The Conventional segment is projected to witness steady growth, particularly in price-sensitive markets across Asia and the Middle East. Lower production costs and easier certification processes make conventional agarwood more accessible for mass incense manufacturing and mid-tier perfumery. Expanding plantation cultivation and improved traceability standards are gradually enhancing product acceptance, supporting moderate yet consistent growth momentum.

End-user Insights

The fragrances segment leads with a 45% share in 2025, driven by strong integration of oud notes into luxury and niche perfume portfolios. International fragrance safety standards recognize agarwood as a compliant aromatic ingredient, encouraging adoption among premium perfume houses. Rising exports through Middle Eastern trade hubs further strengthen its dominance in high-value fragrance applications.

The Incense and Spiritual Use segment is expected to grow at the fastest pace, fueled by increasing participation in meditation, religious rituals, and wellness practices worldwide. Rising household incense consumption across Southeast Asia and expanding adoption in Western wellness communities are accelerating demand. Growth in yoga studios, home altars, and mindfulness practices further supports expanding application beyond traditional markets.

Distribution Channel Insights

The B2B segment holds a dominant 60% share in 2025, as bulk procurement remains essential for incense manufacturers, perfume houses, and essential oil distillers. Trade statistics indicate that most of the agarwood volume moves through structured B2B networks, supported by long-term contracts that ensure consistent quality, pricing stability, and regulatory compliance across ASEAN supplier ecosystems.

The B2C segment is emerging as the fastest-growing channel, driven by digital retail expansion and increasing consumer access to premium agarwood products. E-commerce platforms and specialty fragrance boutiques enable direct sales to wellness enthusiasts and luxury buyers. Growing brand storytelling around origin, sustainability, and authenticity is strengthening direct-to-consumer engagement globally.

Regional Insights

North America Agarwood Chips Market Trends

North America is projected to expand at a CAGR of 7.2% between 2026 and 2033, supported by strong regulatory oversight and premium wellness demand. The United States leads regional consumption, benefiting from streamlined import approvals and innovation in fragrance formulation. Rising patent activity related to agarwood applications reflects ongoing R&D, including synthetic blends addressing supply constraints.

Strict enforcement of CITES regulations by U.S. authorities ensures ethical sourcing and strengthens consumer confidence. Growing multicultural populations and increasing preference for natural incense and oud-based fragrances are accelerating retail sales. Expanding wellness, meditation, and niche perfumery markets continue to position North America as a stable, high-value growth region.

Europe Agarwood Chips Market Trends

Europe accounts for approximately 31% of the global agarwood chips market share in 2025, driven by structured regulatory frameworks and premium fragrance manufacturing hubs. Germany and France lead regional imports, supported by harmonized safety standards under REACH regulations. France’s Grasse region continues to anchor luxury perfumery demand, reinforcing steady consumption of oud-based ingredients.

Sustainability-focused policies under the EU Biodiversity Strategy further encourage certified sourcing and plantation cultivation. Increasing imports of natural aromatics and rising availability of certified products reflect strong eco-conscious consumer preferences. The United Kingdom and Spain are emerging contributors, supported by expanding niche fragrance brands and wellness retail channels.

Asia Pacific Agarwood Chips Market Trends

Asia Pacific holds the largest share, estimated at 38% in 2025, supported by deep-rooted cultural and spiritual traditions and perfumery applications. China and India are primary consumption centers, with China’s expanding luxury fragrance industry and India’s dominance in incense production driving regional demand.

Major producing nations such as Vietnam and Indonesia provide cost advantages and established plantation networks, ensuring supply continuity. Technological advancements in artificial inoculation and plantation management enhance yield efficiency. Additionally, Japan and ASEAN countries contribute by growing wellness exports, positioning Asia Pacific as both the leading consumer and the fastest-growing regional market.

Competitive Landscape

The agarwood chips market is highly fragmented, characterized by a large base of small-scale cultivators and regional traders operating alongside vertically integrated exporters. Competition centers on securing sustainable plantation sources, improving resin yield through advanced inoculation techniques, and maintaining strict compliance with international trade regulations. Certification, traceability, and quality grading standards play a critical role in differentiating suppliers in premium export markets. Market participants are increasingly investing in organic positioning, digital branding, and direct-to-consumer channels to strengthen margins and global visibility. E-commerce expansion and sustainability-driven marketing strategies are reshaping competition, while regulatory oversight continues to influence sourcing practices and long-term supply chain structuring.

Key Developments:

- In June 2025, Royal Aoud introduced a certified organic agarwood chips portfolio through strategic partnerships with Indonesian plantation operators, aiming to strengthen supply reliability and address rising EU demand for sustainably sourced, fully traceable aromatic raw materials across premium fragrance and incense applications.

- In March 2024, Oudh Arabia announced a 20% production capacity expansion supported by advanced biotechnology-based inoculation techniques, unveiled during the Dubai Expo, enhancing resin yield efficiency and reinforcing its competitive positioning within the global luxury oud and agarwood supply chain.

- In November 2023, Ensar Oud completed the acquisition of a Vietnam-based agarwood plantation to improve vertical integration, enhance traceability standards, and ensure stronger compliance with international CITES trade regulations amid tightening sustainability audits across major export markets.

Companies Covered in Agarwood Chips Market

- Grandawood Agarwood Australia

- Binh Nghia Agarwood Co., Ltd

- Hoang Giang Agarwood Ltd.

- Aalam Ul Oud

- KAB Industries

- Duy Hai AGARWOOD.

- Thien Phu agarwood Co.,Ltd

- Asia Plantation Capital Pte Ltd.

- Ori Oud Asia

- ASSAM AROMAS

- Sadaharitha plantations limited

- Green Agro

- Thai Borai Agarwood Co.,Ltd.

- KANHA AROMA

- Homegrown Concept Sdn Bhd (HGC)

Frequently Asked Questions

The global agarwood chips market is expected to reach US$ 47.4 billion in 2026, growing to US$ 81.8 billion by 2033 at 8.1% CAGR.

Key drivers include luxury fragrances and spiritual wellness applications, with 12% perfume export growth and 10% traditional medicine expansion per ITC and WHO.

Asia Pacific leads with a 38% market share in 2025, supported by dominant production hubs and strong cultural consumption across China, India, Vietnam, and Indonesia.

Expansion of organic-certified products, presents a major opportunity, particularly through wellness, spa, and e-commerce channels targeting premium consumers.

Leading companies include Grandawood Agarwood Australia, Binh Nghia Agarwood Co., Ltd, Hoang Giang Agarwood Ltd., Aalam Ul Oud, and KAB Industries, focusing on sustainable sourcing and innovation.