- Beverages

- Plant-based Milk Market

Plant-based Milk Market Size, Share, and Growth Forecast 2026 - 2033

Plant-based Milk Market by Product Type (Soy, Almond, Coconut, Rice, Oat, Others), Nature (Organic, Conventional), End User (Food & Beverage Industry, Infant Formula, Retail/Household, Foodservice Industry), Distribution Channel (Business to Business, Business to Consumer), by Regional Analysis, 2026 - 2033

Plant-based Milk Market Share and Trends Analysis

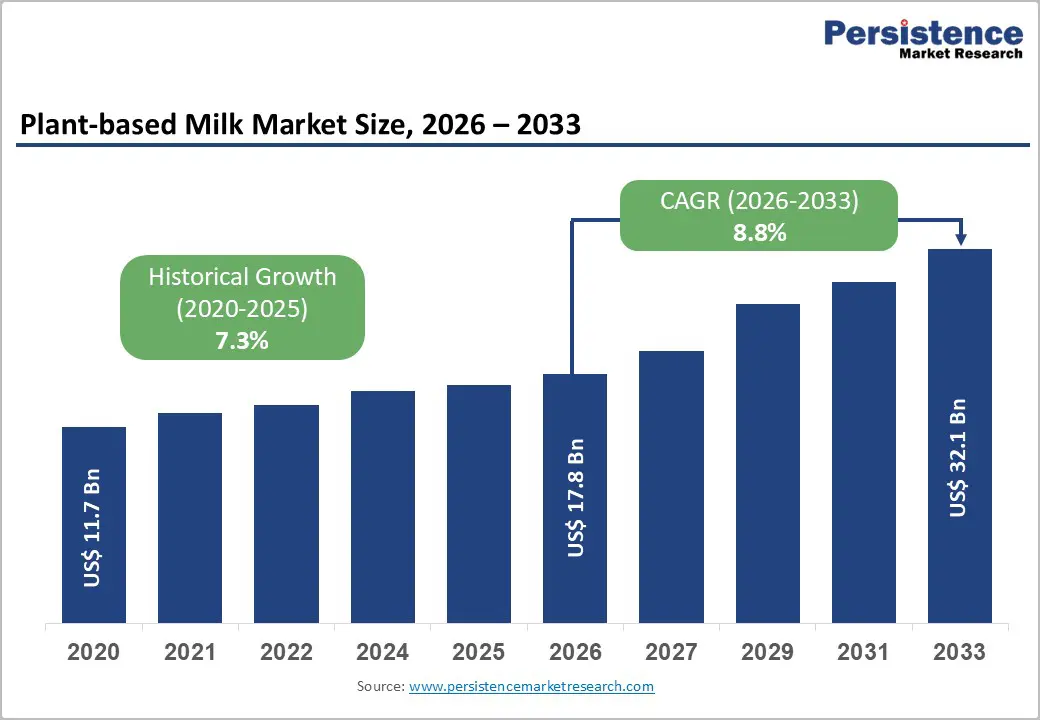

The global plant-based milk market size is expected to be valued at US$ 17.8 billion in 2026 and projected to reach US$ 32.1 billion by 2033, growing at a CAGR of 8.8% between 2026 and 2033. Growth is propelled by accelerating consumer adoption of dairy alternatives, rising lactose intolerance and dairy allergies, and heightened focus on sustainability, which together are shifting milk consumption patterns toward plant-based options.

Industry data from the Plant Based Foods Association (PBFA) and The Good Food Institute (GFI) indicate that plant-based milk already accounts for about 16% of all U.S. retail milk dollar sales and is purchased by roughly 42% of households, underscoring broad mainstream penetration beyond vegan and vegetarian consumers. Globally, GFI estimates put retail plant-based milk sales at around US$ 18.7 billion in 2023, with Asia Pacific leading and North America in second place, highlighting strong geographic diversification and providing a robust base for continued mid to high-single-digit volume growth and premiumization.

Key Industry Highlights:

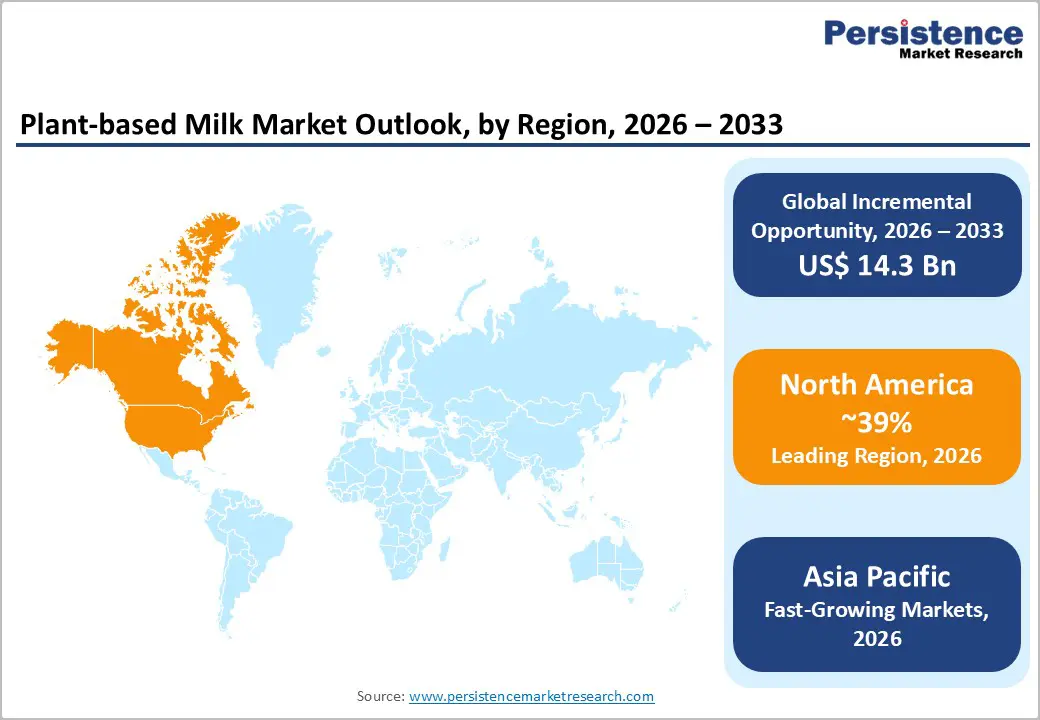

- Regional Leadership: North America remains the leading regional market for plant-based milk by value, with the United States generating around US$ 2.6–2.9 billion in retail sales and plant-based milk accounting for roughly 16% of all retail milk dollar sales and over 40% household penetration.

- Fast-growing Market: Asia Pacific is the fastest-growing region, underpinned by entrenched soy milk consumption, rising urban incomes, and rapid adoption of almond and oat milks, resulting in regional plant-based milk retail sales of about US$ 9.8 billion and continued expansion in China, Japan, India, and ASEAN markets.

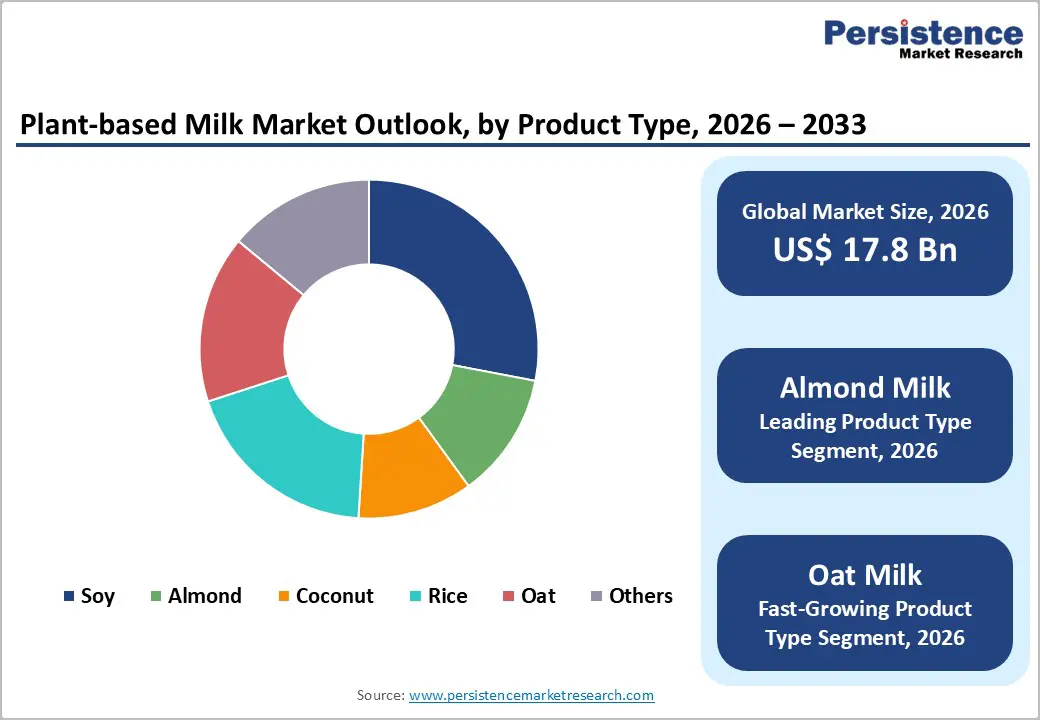

- Leading Nature Type: Almond milk is the dominant product segment, representing roughly 28% of global plant-based milk sales and over 55% of U.S. category revenue, while oat milk is the fastest-growing type, expanding from near-zero share in 2018 to around the mid-teens percentage of sales.

- Dominant End-user: Retail/household consumption via business-to-consumer channels currently drives the bulk of volume, but business-to-business sales into foodservice and food and beverage manufacturing are growing faster as plant-based milks become standard in cafés, ready-to-drink coffees, and dairy-alternative foods.

- Opportunities: Key opportunities include fortified, functional, and low-sugar formulations, as well as premium organic and clean-label offerings, and deeper integration into foodservice and emerging markets, while addressing price premiums, nutritional communication, and clean-label expectations.

| Key Insights | Details |

|---|---|

|

Plant-based Milk Market Size (2026E) |

US$ 17.8 billion |

|

Market Value Forecast (2033F) |

US$ 32.1 billion |

|

Projected Growth CAGR (2026–2033) |

8.8% |

|

Historical Market Growth (2020–2025) |

7.3% |

Market Dynamics

Drivers - Health, lactose intolerance, and flexitarian dietary shifts

Rising health consciousness and widespread lactose intolerance are core structural drivers for plant-based milk adoption worldwide. Estimates suggest that around 65–70% of the global adult population exhibits some degree of lactose malabsorption, while guidelines from bodies such as the World Health Organization (WHO) emphasize reducing saturated fat and added sugars, encouraging consumers to explore low-cholesterol, plant-based beverages in place of full-fat dairy. In the United States, plant-based milk now represents about 16% of all retail milk dollar sales, with almond milk leading and oat milk rapidly gaining share, while cow’s milk dollar sales continue to decline. Flexitarian consumers, who still eat some animal products but aim to lower their environmental footprint and improve long-term health, increasingly view soy, almond, oat, and pea-based milks as convenient, nutritious substitutes in coffee, breakfast cereals, smoothies, and cooking.

Sustainability, animal welfare, and innovation in plant-based beverages

Environmental and ethical considerations significantly reinforce demand for plant-based milk, as lifecycle assessments consistently show lower greenhouse gas emissions and land use compared with dairy milk. Analyses drawing on FAO and academic data estimate that global dairy production (milk and associated meat) contributes around 4% of total anthropogenic greenhouse gas emissions, while plant-based milks typically generate between one-half and one-third of the emissions per liter and use substantially less land. Studies cited by organizations such as the World Resources Institute (WRI) and climate-focused NGOs indicate that shifting from dairy to oat, soy, or coconut milk can cut beverage-related emissions by more than 60–70%, and campaigns highlight that oat and soy milks also require significantly less water than dairy milk on a per-glass basis. These sustainability advantages, combined with rapid innovation in barista-style, fortified, and flavored plant-based milks from brands such as Danone (Silk, Alpro), Oatly Group AB, and Blue Diamond Growers, underpin strong premium demand across retail and foodservice.

Restraints - Price premium and inflationary pressures on consumers

One of the principal restraints for the plant-based milk market is the price premium over conventional dairy milk, which has been exacerbated by commodity and logistics inflation in recent years. Trade association data for the U.S. market show that between 2021 and 2023, plant-based categories, including milk, experienced retail price increases often exceeding those of animal-based counterparts, prompting some price-sensitive shoppers to trade down or reduce purchase frequency. While value sales of plant-based milk continued to edge upward, reaching about US$ 2.9 billion in the United States in 2023, unit volumes declined, highlighting consumer sensitivity to shelf price gaps, especially in mainstream supermarkets. In emerging markets, where absolute price levels and income constraints are more acute, premiums for imported or branded plant-based milks can limit penetration beyond affluent urban segments, slowing category expansion.

Nutritional perception gaps and clean-label scrutiny

Another challenge is lingering consumer skepticism about the nutritional adequacy and processing level of some plant-based milks. The US Food and Drug Administration (FDA) has noted in draft guidance that many plant-based milk alternatives contain lower levels of key nutrients such as protein, calcium, and vitamin D than cow’s milk unless they are fortified, prompting calls for clearer front-of-pack disclosures and voluntary nutrient comparison statements. Some products rely on added sugars, oils, stabilizers, and flavorings to achieve sensory parity with dairy, which can conflict with consumer interest in short, clean ingredient lists. Nutrition experts and regulators emphasize that plant-based milks should not be seen as nutritionally identical to dairy by default, and this nuance may slow adoption among parents of young children and health professionals unless formulations and communication continue to improve.

Opportunities - Fortified, functional, and low-sugar plant-based milks

There is a substantial opportunity in developing fortified and functional plant-based milks that address nutritional gaps and align with evolving dietary guidelines. Many health agencies stress the need to reduce saturated fat, added sugars, and sodium while maintaining adequate protein, calcium, iodine, and vitamin B12 intakes, creating space for plant-based milks fortified to match or exceed dairy’s micronutrient profile with fewer calories and less saturated fat. Companies such as Danone, Nestlé S.A., Califia Farms, LLC, and Ripple Foods are investing in higher-protein pea and blend-based milks, no-added-sugar variants, and products enriched with omega-3s, fiber, or probiotics targeted at specific segments such as children, athletes, and older adults. As consumers increasingly look for beverages that combine hydration, nutrition, and health benefits, well-positioned plant-based milks can capture share from both dairy and other functional drink categories, particularly in refrigerated and on-the-go formats.

Geographic expansion and foodservice integration

Geographic white spaces and deeper integration into foodservice channels present another major opportunity for market participants. Good Food Institute’s global assessments show that plant-based milk retail sales reached about US$ 18.7 billion in 2023, with Asia Pacific leading in dollar sales at around US$ 9.8 billion, followed by Europe at roughly US$ 4.1 billion and North America at about US$ 3.6 billion, signaling ample room for growth in Latin America and the Middle East & Africa. As coffee chains, quick-service restaurants, and workplace cafeterias increasingly offer soy, almond, oat, and coconut milks as standard options, often at price parity with dairy plant-based beverages, they become embedded in daily routines, driving habitual consumption beyond the home. Strategic partnerships between global brands such as Oatly Group AB, Vitasoy International Holdings Ltd, and large coffee chains, as well as localized collaborations in Asia and Latin America, are expected to accelerate penetration in out-of-home channels over the coming decade.

Category-wise Analysis

Product Type Insights

Among product types, almond milk is the leading segment, accounting for an estimated 28% of global plant-based milk sales in 2025, and significantly higher shares in mature markets such as North America. U.S. retail data from SPINS and PBFA show that almond milk alone represents about 55–59% of the country’s plant-based milk category by dollar sales, with brands such as Blue Diamond Growers’ Almond Breeze, Danone’s Silk, and various private labels capturing substantial share. Is oat milk the fastest-growing segment globally, with U.S. sales increasing more than 50% in a recent 12-month period to surpass US$ 500 million, and its share rising from virtually zero in 2018 to a mid-teens percentage of category sales. Soy milk remains important in Asia Pacific and among long-time plant-based consumers, but has ceded share to almond and oat in Western markets, while coconut, rice, pea, and blend-based milks address specific taste, allergen, or nutritional niches.

Nature Insights

By nature, conventional plant-based milks currently dominate global volumes, reflecting their broader price accessibility and distribution in mainstream retail channels. However, organic variants are expanding rapidly, particularly in North America and Europe, where organic food markets have grown at mid-single-digit rates and organic drinks benefit from strong health and sustainability associations. Trade and industry sources indicate that organic products now account for roughly 6% or more of total U.S. food sales and a higher share in several European countries, with organic beverages and plant-based categories outpacing overall grocery growth. As consumers adopt more holistic definitions of wellness that include farming practices, pesticide reduction, and biodiversity, organic soy, almond, oat, and coconut milks from brands such as Earth’s Own, THE BRIDGE S.R.L, and specialist private labels are gaining shelf space and loyalty in premium and health-oriented channels.

Distribution Channel Insights

In distribution-channel terms, business-to-consumer (B2C) sales through supermarkets, hypermarkets, convenience stores, specialty retailers, and e-commerce currently generate the majority of plant-based milk revenue. Plant-based beverages are among the most developed categories within the broader plant-based foods sector, capturing roughly 35–36% of total plant-based retail dollar sales and benefiting from prominent placements, multi-pack promotions, and cross-merchandising with coffee and breakfast products. Business-to-business (B2B) channels, including sales to cafés, quick-service restaurants, institutional caterers, and food and beverage manufacturers, are expanding faster as plant-based milks become the default options in coffee chains and are used as inputs in value-added foods. As large brands optimize pack formats (barista cartons, bag-in-box, concentrates) and build direct relationships with foodservice operators, the B2B segment is expected to deliver above-average growth, even as B2C remains the dominant revenue contributor.

Regional Insights

North America Plant-Based Milk Market Trends and Insights

North America is currently the leading regional market for plant-based milk, accounting for an estimated 39% share of global value in 2025, with the United States as the primary growth engine. Data from PBFA, GFI, and SPINS show that plant-based milk reached about US$ 2.6–2.9 billion in U.S. retail sales in recent years, representing roughly 16% of total retail milk dollar sales and achieving household penetration of over 40%. Almond milk remains the category leader, accounting for around 55–59% of sales, while oat milk has grown from virtually negligible levels in 2018 to roughly 17% of the category, reflecting strong uptake among younger, urban consumers and in specialty coffee channels.

Regulatory and innovation ecosystems further support the North American market. The US Food and Drug Administration (FDA) issued draft guidance in 2023 on the labeling of plant-based milk alternatives, recognizing that consumers understand these products do not contain cow’s milk and recommending voluntary nutrient statements comparing plant-based and dairy milks. This clarity reduces legal uncertainty and encourages innovation in nutrient-fortified formulations. At the same time, strong venture and corporate investment, particularly in oat, pea, and blend-Based on milks, has enabled brands such as Oatly Group AB, Califia Farms, LLC, and Ripple Foods to expand distribution across retail, foodservice, and direct-to-consumer channels. Together, these factors position North America as the benchmark region for category sophistication, branding, and multiproduct plant-based dairy portfolios.

Asia Pacific Plant-based Milk Market Trends and Insights

Asia Pacific is the fastest-growing regional market for plant-based milk, underpinned by longstanding consumption of soy beverages, rising incomes, and rapid urbanization in markets such as China, Japan, India, and the ASEAN bloc. Euromonitor data cited in industry analyses indicate that the Asia Pacific led the world in plant-based milk retail sales at around US$ 9.8 billion, surpassing both Europe and North America, although recent annual growth rates have moderated to the low single digits as the category matures in key East Asian markets. In China and Southeast Asia, soy milk has long been an everyday staple sold through street vendors, cafés, and packaged formats, creating a high baseline of familiarity, while newer almond, oat, and coconut milks are gaining traction among younger, health-conscious consumers and in specialty coffee chains.

Importantly, Asia-Pacific markets generally exhibit less controversy over the use of the term “milk” for plant-based beverages than the U.S. or the EU, with industry experts noting that consumers readily understand that the milk category encompasses both plant and animal products. Innovation hubs such as Singapore, Australia, and New Zealand are fostering alternative protein ecosystems, with governments providing funding and regulatory support for novel plant-based and hybrid products. Local champions like Vitasoy International Holdings Ltd and regional subsidiaries of multinationals are leveraging manufacturing advantages, established distribution in foodservice and retail, and strong brands to launch fortified, flavored, and barista-style plant-based milks tailored to regional taste preferences, setting the stage for continued above-average growth across the region.

Competitive Landscape

The plant-based milk market is highly fragmented and competitive, with the presence of numerous global and regional players alongside private-label brands. Companies compete primarily through product innovation, focusing on improving taste, texture, and nutritional value to match dairy alternatives. Strategies such as new product launches, clean-label formulations, and fortified offerings are widely adopted to attract health-conscious consumers. Expansion across retail and online distribution channels further intensifies competition.

Key Developments:

- In January 2025, Oat milk brand MYOM launched its premix pouches in Whole Foods Market stores across London, marking its first retail listing. The expansion brings MYOM’s sustainable and customizable oat milk solution to a broader consumer base, aligning with the growing demand for freshly made, dairy-free alternatives.

- In January 2024, Oatly introduced Unsweetened Oatmilk and Super Basic Oatmilk, both made with minimal ingredients, catering to consumers seeking low or no-sugar options

- In May 2024, Danone's Silk brand introduced Silk Kids, a plant-based milk specifically formulated for children. Made with oats and peas, the new product offers 8 grams of protein per serving, catering to growing consumer demand for nutritious, dairy-free options for kids.

Companies Covered in Plant-based Milk Market

- Danone, Oatly Group AB, Nestlé S.A.

- Blue Diamond Growers

- The Hain Celestial Group, Inc.

- SunOpta Inc.

- Vitasoy International Holdings Ltd

- Pacific Foods

- Califia Farms, LLC

- Ripple Foods

- Elmhurst Milked Direct LLC

- Sanitarium, Valsoia, Earth’s Own

- THE BRIDGE S.R.L

- Alpro

- Silk

- Almond Breeze

Frequently Asked Questions

The global plant-based milk market is expected to reach around US$ 17.8 billion in 2026, supported by rising lactose intolerance, growing flexitarian and vegan populations, and expanded retail and foodservice availability across North America, Europe, and Asia Pacific.

The primary demand driver is the combination of health and sustainability motivations: high lactose intolerance prevalence of about 65–70% globally, interest in lowering saturated fat and cholesterol intake, and evidence that plant-based milks generate significantly lower greenhouse gas emissions and land use than dairy milk.

North America currently leads the market by value, with the United States generating roughly US$ 2.6–2.9 billion in retail plant-based milk sales and plant-based milk accounting for around 16% of all retail milk dollar sales and more than 40% household penetration.

A major opportunity lies in fortified, functional, and low‑sugar plant-based milks that match or exceed dairy’s nutritional profile while delivering better environmental performance, as well as premium organic offerings and barista‑focused formats tailored for cafés and foodservice channels worldwide.

Key players include global and regional companies such as Danone, Oatly Group AB, Nestlé S.A., Blue Diamond Growers, The Hain Celestial Group, Inc., SunOpta Inc., Vitasoy International Holdings Ltd, Pacific Foods, Califia Farms, LLC, Ripple Foods, Elmhurst Milked Direct LLC, Sanitarium, Valsoia, Earth’s Own, and THE BRIDGE S.R.L.