- Technology

- System Integration Market

System Integration Market Size, Share, and Growth Forecast, 2025 - 2032

System Integration Market by Services (Infrastructure Integration Services, Application Integration Services, Consulting Services, Maintenance & Support Services, Others), Enterprise Size (Large Enterprises, Small & Medium Enterprises), Industry, and Regional Analysis for 2025 - 2032

System Integration Market Share and Trends Analysis

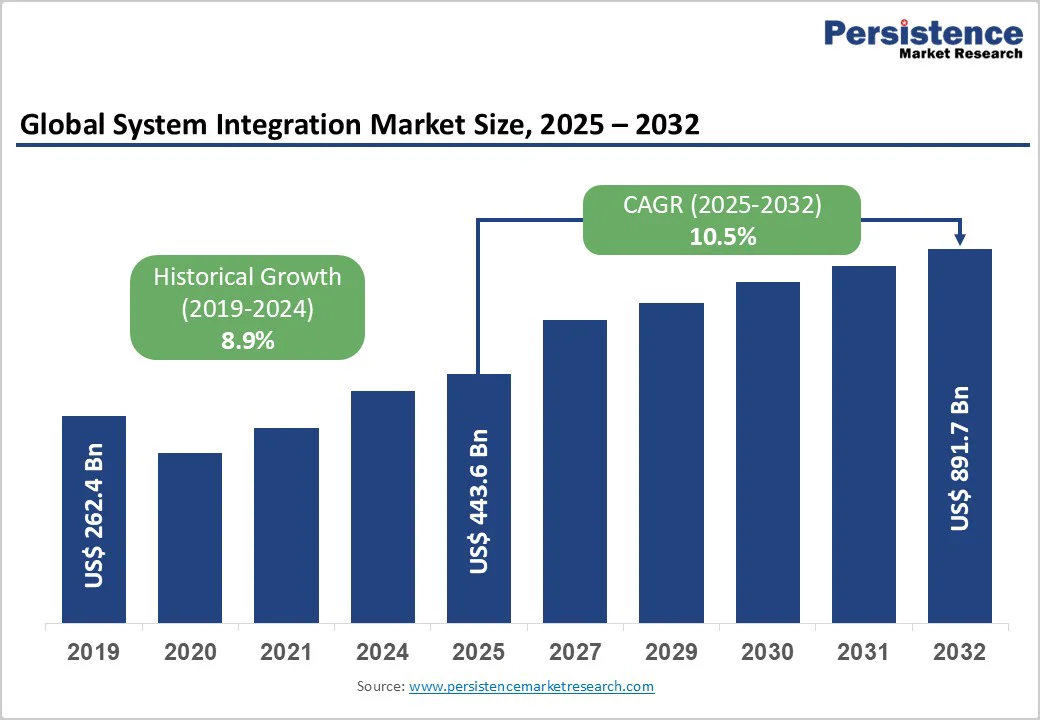

The global system integration market size is likely to value US$443.6 billion in 2025 and projected to reach US$891.7 billion at a CAGR of 10.5% during the forecast period from 2025 to 2032.

Organizations are seeking to unify complex and fragmented IT infrastructures to enhance operational efficiency and agility. Businesses are increasingly turning to integration services to modernize legacy systems, improve interoperability, and ensure real-time data flow across hybrid environments. The rise of API-led integration, microservices architecture, and automation tools is further enabling scalable and flexible system integration solutions.

Key Industry Highlights:

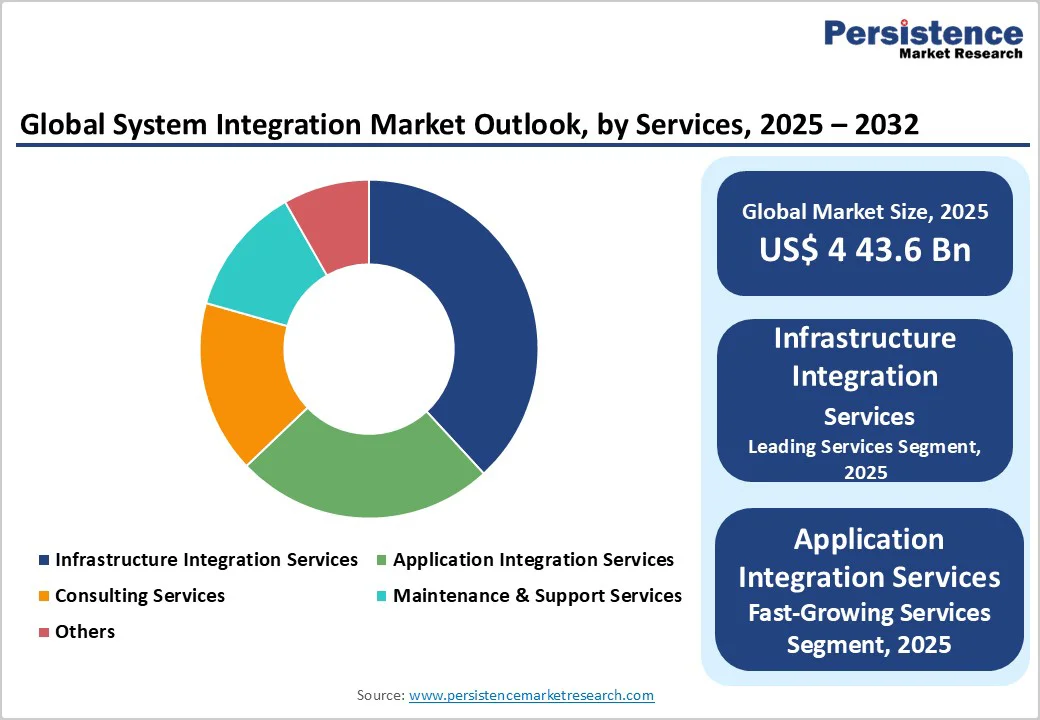

- Leading Service: Infrastructure integration service dominates with over 35% share in 2025, driven by hybrid IT modernization, network virtualization, and 5G deployment. Application integration emerges as the fastest-growing segment with holding over 27% share in 2025, fueled by rising SaaS adoption, workflow automation, and demand for real-time data synchronization across cloud environments.

- Leading Enterprise Size: Large enterprises account for over 64% of market share in 2025, supported by multi-vendor IT unification, AI and IoT deployment, and compliance automation. Small & medium enterprises register strong growth due to rising cloud adoption and reliance on outsourced integration for cost-effective modernization.

- Leading Industry: IT & Telecom leads with over 26% share in 2025, driven by 5G rollout, edge computing, and network virtualization projects. Healthcare grows fastest, propelled by electronic health record (EHR) interoperability, telehealth integration, and HIPAA-aligned compliance frameworks.

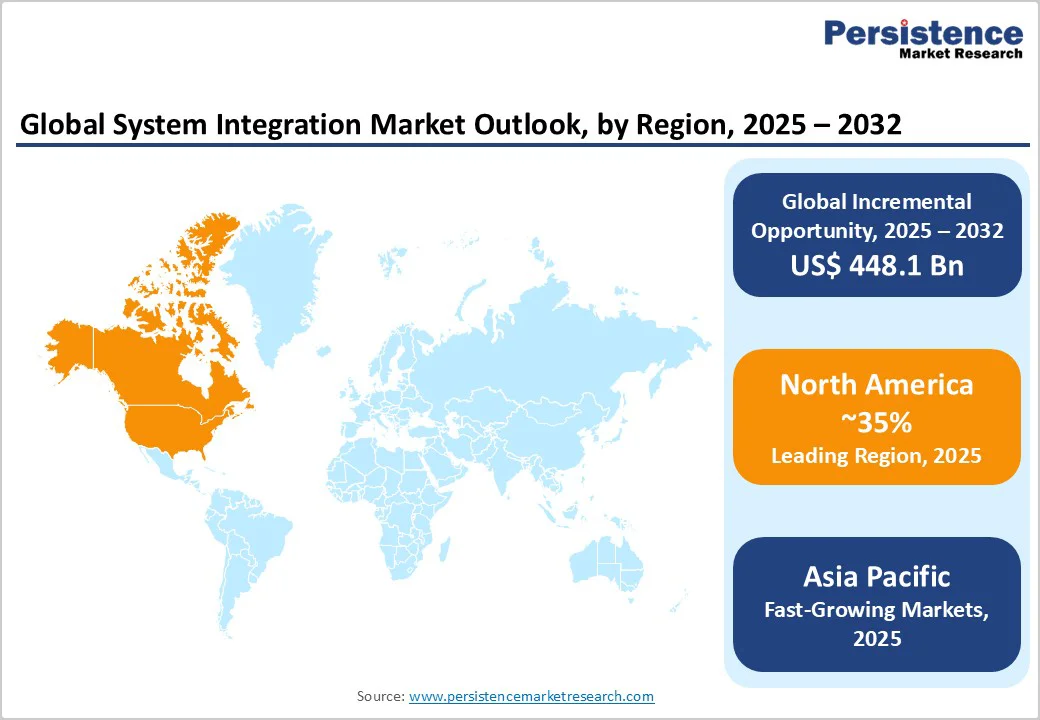

- Leading Region: North America captures over 35% share in 2025, supported by US$75.1 billion federal IT modernization initiatives, strong cybersecurity mandates, and extensive legacy upgrades. Asia Pacific grows fastest, led by China and India’s 5G expansion, automation programs, and large-scale digital transformation initiatives.

- Leading Driver: Cloud-Native and IT-OT Convergence strengthen industrial automation and predictive maintenance, with over 60-70% of OT systems expected to connect to IT networks by 2025. 5G-enabled IoT integration enhances real-time monitoring and operational efficiency across manufacturing sectors.

| Global Market Attribute | Key Insights |

|---|---|

| System Integration Market Size (2025E) | US$443.6 Bn |

| Market Value Forecast (2032F) | US$891.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.9% |

Market Dynamics

Driver - API-Led Connectivity and Microservices Architecture Driving Scalability

The rise of API-led connectivity and microservices architecture is transforming enterprise integration by replacing monolithic systems with modular, agile, and scalable solutions. System integrators play a crucial role in enabling seamless orchestration of distributed services through API management platforms that ensure security, versioning, and performance governance.

With the API management market projected to grow from US$ 7.9 billion in 2025 to US$ 31.2 billion by 2032 at a CAGR of 21.7%, integrators are facilitating ecosystem expansion via self-service developer portals, sandbox testing, and monetization models, accelerating digital innovation and ecosystem scalability.

Cloud-Native Adoption & IT and OT System Integration Strengthening Industrial Operations

The growing adoption of cloud-native architectures and the convergence of IT and OT systems are key drivers of the system integration market. As the global digital economy accounts for 15% of world GDP in 2025, enterprises increasingly invest 2-3% of annual revenue in integration and ERP systems to ensure interoperability and data continuity across hybrid IT environments.

With 60-70% of OT systems in manufacturing expected to connect to IT networks by 2025 in U.S., Latin America, and Europe, integration enables real-time monitoring, predictive maintenance, and automation, up from around 50% in 2024. 5G-enabled IoT integration enhances machine-to-machine communication, optimizing industrial operations and reducing downtime through real-time data exchange.

Restraint - Budget Overruns and Extended Deployment Timelines Impacting Return on Investment

System integration projects frequently encounter significant execution risks that hinder adoption among risk-averse organizations. Studies indicate that nearly 45% of large IT and integration projects exceed both budget and schedule targets, with average cost overruns reaching 30-40% of initial estimates and delivery timelines extending by 20-25% on average.

Complex legacy infrastructure upgrades, multi-application synchronization, and customized middleware development contribute to scope expansion that amplifies these overruns. Such delays compress the window for return-on-investment realization, discouraging modernization efforts, particularly among small enterprises and public agencies operating under strict fiscal constraints, thereby limiting broader market adoption in capital-sensitive segments.

Skill Shortage and Complexity of Integration Architecture

The system integration market faces significant challenges from acute skill shortages and complex integration architectures. Organizations struggle to find experts proficient in legacy systems, cloud-native technologies, APIs, security, and regulatory frameworks, driving up labor costs and project timelines.

Ongoing maintenance, performance optimization, and compliance updates further strain limited technical resources. Smaller firms lacking capital to recruit or contract premium integrators face barriers to effective system deployment and scalability.

Opportunity - Cybersecurity and Compliance-Driven Integration Demand Across Regulated Industries

Cybersecurity and compliance-driven integration demand is surging as over 60% of organizations globally implement zero-trust strategies. The post-M&A integration services market, growing at a CAGR of around 9.6%, reflects heightened focus on embedding security within integration frameworks rather than post-deployment.

Regulatory convergence of GDPR, HIPAA, and PSD2 is compelling enterprises in regulated sectors like BFSI and healthcare to adopt integration solutions with built-in compliance automation, audit trails, and role-based access controls, driving sustained demand for secure, standards-aligned system integration services.

5G System Integration and Edge Computing Infrastructure

5G network rollout globally is creating a substantial market opportunity for specialized system integration services addressing 5G infrastructure deployment complexity and edge computing platform integration. The 5G system integration market is valued at US$18.2 billion in 2025 and is projected to reach US$91.3 billion by 2032 with a projected compound annual growth rate of 25.9%.

This exceptional growth trajectory reflects the structural demand for integration capabilities supporting autonomous vehicles, industrial automation, and smart city infrastructure. Integrators play a critical role in network slicing, spectrum optimization, and URLLC deployment to enable real-time manufacturing and predictive maintenance.

According to the Ericsson Mobility Report, 5G subscriptions reached 2.3 billion in 2024 and are expected to approach 2.9 billion by end-2025, underscoring massive integration demand.

Category-wise Analysis

By Services, Infrastructure Integration, Leading Hybrid IT Modernization and Connectivity

Infrastructure integration services are expected to account for more than 35% share in 2025, driven by the need for seamless connectivity across hybrid IT environments combining legacy, cloud, and edge systems. Growing investments in data center modernization, network virtualization, and 5G deployment are fueling this demand.

Rising IoT and AI adoption requires secure, scalable infrastructure to ensure interoperability and support resilient hybrid work and disaster recovery environments.

Application integration services are projected to grow at the fastest rate, holding over 27% share in 2025, driven by the rising need for seamless interoperability across diverse enterprise applications and cloud platforms. As organizations modernize legacy systems and adopt SaaS solutions, demand for real-time data synchronization and workflow automation intensifies.

The expansion of API-driven architectures, microservices, and hybrid cloud models adds further integration complexity. With enterprises managing an average of 991 applications but integrating only 29%, a vast untapped opportunity exists to build unified ecosystems that enhance customer experience, agility, and data-driven decision-making.

By Enterprise Size, Large Enterprises Driving Demand for Complex, Scalable Integration Solutions

Large enterprises are expected to account for over 64% share in 2025 due to their need to unify complex, multi-vendor IT infrastructures across global operations. They rely on integrated platforms for data management, cybersecurity, and compliance automation.

Ongoing digital transformation initiatives such as AI-driven analytics, IoT deployment, and hybrid cloud migration further amplify demand for advanced integration services to ensure scalability and real-time performance. Large organizations typically allocate 2-3% of their annual revenue to integration and ERP systems, reflecting institutionalized budget commitments to these functions.

Small and medium enterprises will grow at a significant rate due to their urgent need to streamline fragmented IT infrastructure and enable seamless data exchange across cloud and on-premise systems. As SMEs increasingly adopt digital transformation, automation, and cloud-based business tools, they rely on integration services to enhance operational efficiency and scalability.

Limited in-house IT expertise also drives SMEs to outsource integration projects for cost-effective modernization.

By Industry, IT & Telecom Accelerating 5G, Cloud, and Edge Infrastructure Integration

IT & Telecom is expected to account for more than 26% share in 2025 due to the growing need for 5G network deployment, cloud-native infrastructure, and edge computing integration. Telecom operators are heavily investing in integrating legacy and next-generation networks to support data-intensive applications and IoT ecosystems.

Rising demand for automated service delivery, network virtualization, and cybersecurity integration drives continuous system integration requirements across the industry.

Healthcare will grow at the highest rate due to rising demand for interoperable health IT systems, electronic health records (EHR) integration, and telehealth platforms. Hospitals and clinics increasingly require seamless data exchange across diverse medical devices, diagnostic tools, and administrative systems to improve patient outcomes and operational efficiency.

Growing adoption of remote patient monitoring and compliance with regulatory frameworks like HIPAA further amplify integration needs.

Regional Insights

North America System Integration Market Trends

North America is projected to hold over 35% of the global system integration market by 2025, driven by advanced IT infrastructure, high enterprise spending, and modernization of extensive legacy systems. Strong government initiatives such as the U.S. federal civilian agencies’ FY 2025 IT budget of US$75.1 billion underscore ongoing investments in cloud migration, cybersecurity, and enterprise-scale integration.

The region’s regulatory mandates (HIPAA, SOX, GLBA) further fuel integration demand, particularly across healthcare and financial sectors. Rising IoT adoption, industrial automation, and the need for energy-efficient operations strengthen North America’s leadership in the system integration landscape.

Asia Pacific System Integration Market Trends

Asia Pacific represents the fastest-growing regional market, driven by rapid industrialization, government-led digital transformation programs, and accelerating enterprise adoption. China leads the region with massive digital investments. Its digital economy core industries accounted for about 10% of GDP in 2024, supported by over 4.25 million 5G base stations noted by National Data Administration.

India represents the strongest growth opportunity, with over 4.74 lakh 5G towers covering 99.6% of districts by mid-2024, fueling integration demand across telecom and manufacturing. Japan’s advanced manufacturing and telecom modernization further boost regional momentum. Expanding automation, IoT deployment, and smart city projects position the Asia Pacific as the key hub for large-scale system integration initiatives.

Europe System Integration Market Trends

The European system integration market is driven by harmonized regulatory frameworks like GDPR, fostering standardized integration across member states. Germany leads demand with Industry 4.0 and automation investments, while the UK focuses on open banking and data-sharing integration within financial services. France and Spain contribute through manufacturing and telecom growth.

Strategic partnerships, such as the Infosys-LKQ Europe collaboration in Dec 2023, highlight the region’s emphasis on integration-led operational efficiency. According to ITA, by 2026, 64% of German firms plan ERP investments, 75% in MES, 72% in cloud systems, and 70% in cybersecurity, aligning with the EU’s 2024 digitalization report showing 74% of businesses achieving basic digital intensity for SMEs, the share was 73%, for large firms 98%.

Competitive Landscape

The system integration market is highly fragmented, with numerous global and regional players competing across diverse service domains. Leading system integrators adopt strategic partnerships and acquisitions to enhance technical expertise and expand their global presence.

They emphasize industry-specific integration solutions across sectors such as healthcare, BFSI, and manufacturing. Companies invest in cloud innovation, AI-driven automation, and cybersecurity integration to differentiate their offerings and build long-term client relationships.

Key Industry Developments:

- In July 2025, Tech Mahindra joined J.P. Morgan Payments’ System Integrator Program to modernize global enterprises’ payment infrastructure. The collaboration leverages Tech Mahindra’s expertise in real-time payments, ERP, and SAP implementations with J.P. Morgan’s robust payments capabilities to enhance financial operations, real-time tracking, and AI-driven business insights.

- In May 2025, IBM introduced new hybrid technologies designed to overcome barriers in scaling enterprise AI, enabling organizations to build and deploy AI agents using their own data. IBM is integrating hybrid platforms, AI agent capabilities, and consulting expertise to help businesses operationalize AI across fragmented IT environments.

Companies Covered in System Integration Market

- IBM Corporation

- Accenture PLC

- Capgemini SA

- Wipro Limited

- Cognizant Technology Solutions Corporation

- Infosys Limited

- HCL Technologies Limited

- Atos SE

- SAP SE

- NTT DATA Corporation

- Siemens AG

- Tech Mahindra Limited

- NEC Corporation

- Others

Frequently Asked Questions

The global system integration market is projected to be valued at US$443.6 Bn in 2025.

The growing need for seamless connectivity between diverse IT systems to enhance operational efficiency, data visibility, and business agility is a key driver of the market.

The market is poised to witness a CAGR of 10.5% from 2025 to 2032.

Increasing adoption of 5G technologies, IoT, and AI-driven automation is creating strong growth opportunities.

IBM Corporation, Accenture PLC, Capgemini SA, Wipro Limited, Cognizant Technology Solutions Corporation, Infosys Limited are among the leading key players.