- Hardware & Software IT Services

- Network Performance Monitoring Market

Network Performance Monitoring Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Network Performance Monitoring Market by Component (Hardware, Platforms/Software, Services), Enterprise Size (Small & Mid-sized Enterprises, Large Enterprises), End-user (Telecom Service Providers, Cloud Service Providers, Governments, Enterprises), and Regional Analysis for 2025 - 2032

Network Performance Monitoring Market Size and Trends Analysis

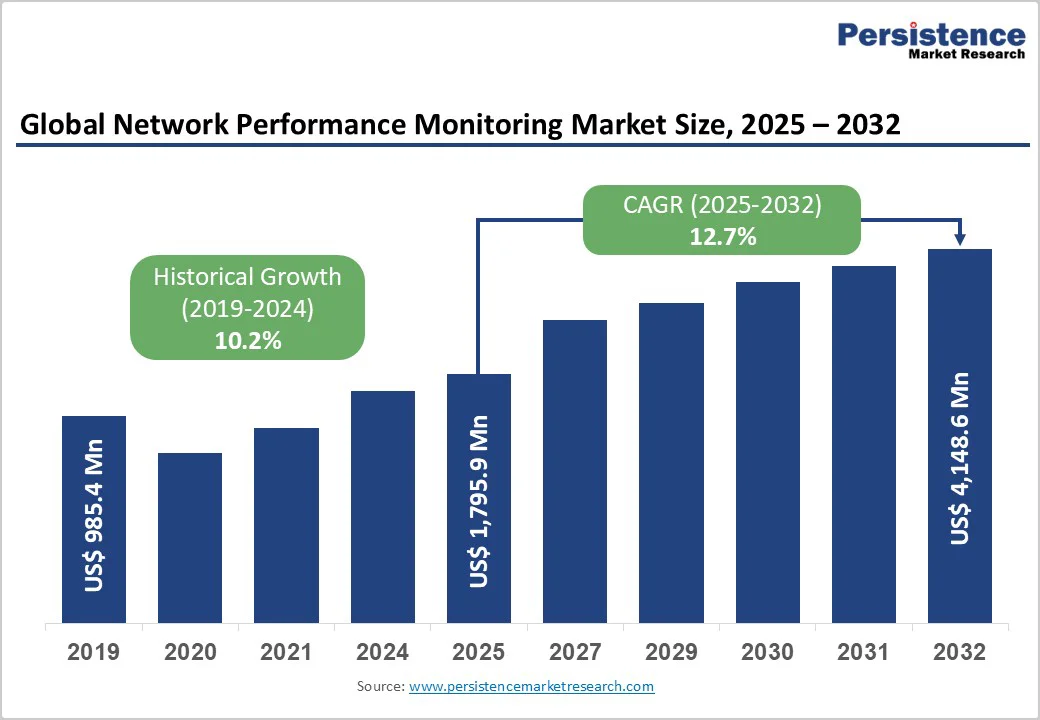

The global network performance monitoring (NPM) market size is projected to value at US$1,795.9 million in 2025 and projected to reach US$4,148.6 million, growing at a CAGR of 12.7% during the forecast period from 2025 to 2032.

Organizations increasingly depend on NPM solutions to ensure optimal uptime, latency control, and real-time visibility across hybrid and multi-cloud environments. The exponential surge in data traffic, growing edge computing deployments, AI-driven predictive analytics, and heightened focus on cybersecurity, compliance, and user experience optimization are further accelerating market demand across industries.

Key Industry Highlights:

- Leading Component: Hardware dominates with over 53% share in 2025, supported by the deployment of high-speed switches, routers, and monitoring probes that ensure real-time traffic visibility and reliability across core and edge networks. Software/platforms register the fastest growth, driven by demand for cloud-native, AI-integrated monitoring solutions offering automation and scalability across hybrid environments.

- Leading Enterprise Size: Large enterprises account for over 67% market share in 2025, owing to complex hybrid infrastructures, extensive IT budgets, and critical reliance on network uptime. SMEs represent the fastest-growing segment as they adopt affordable cloud-based and managed NPM services to enhance agility and visibility across distributed networks.

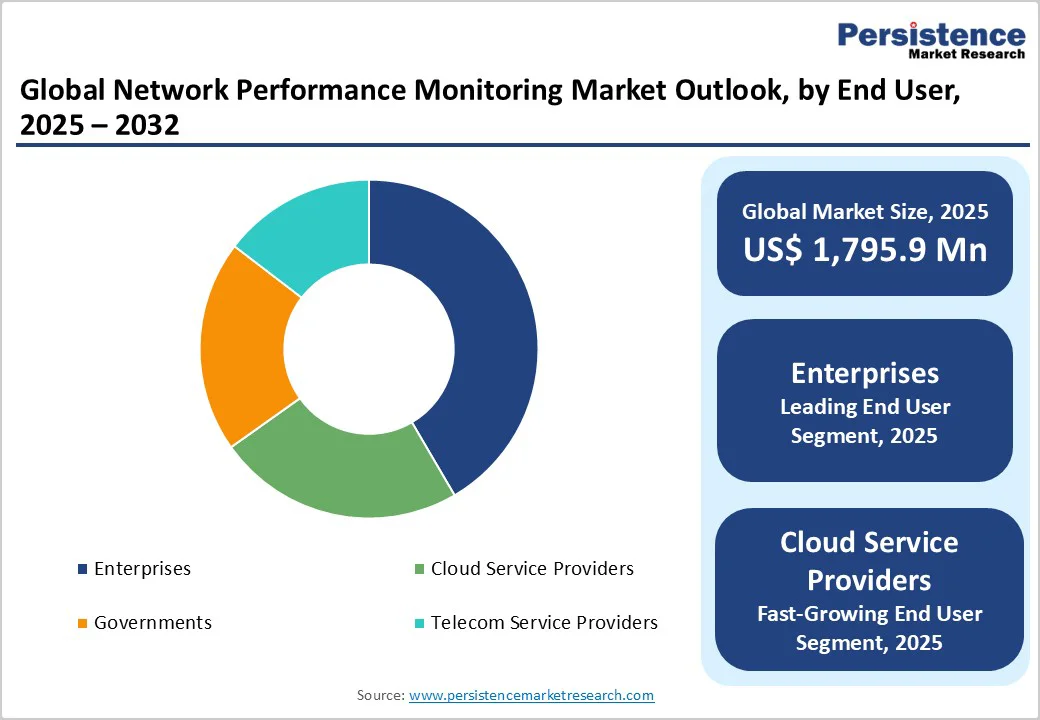

- Leading End-user: Enterprises lead with more than 38% share in 2025, driven by the need for scalable, proactive performance management. Cloud service providers grow fastest, propelled by hyperscale data center expansion and AI infrastructure requiring terabit-scale monitoring and SLA compliance.

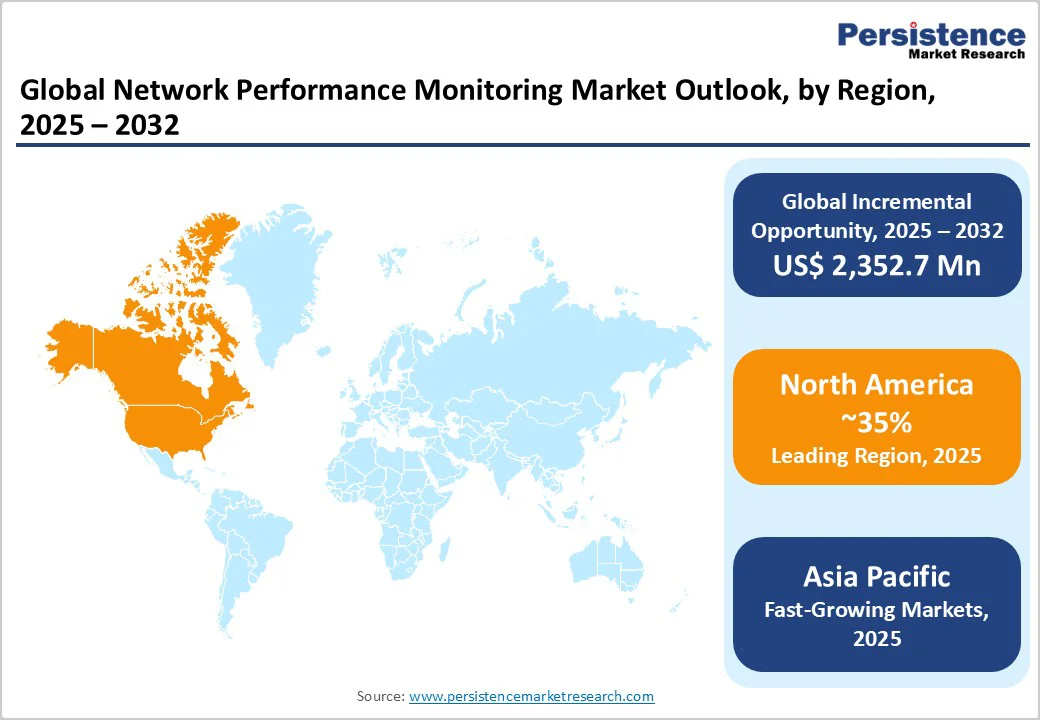

- Leading Region: North America captures over 35% share in 2025, driven by early 5G rollout, strong IT infrastructure, and stringent resilience mandates. Asia Pacific emerges as the fastest-growing region, led by China’s hyperscale expansion and India’s digital infrastructure boom, while Europe grows steadily under DORA and Industry 4.0-driven modernization.

- Growth Indicator: Exponential 5G and IoT proliferation, surpassing 2.25 billion global 5G connections and 25 billion IoT devices by 2025, fuels unprecedented demand for intelligent, scalable NPM tools capable of managing massive telemetry data and ensuring QoS across high-density networks.

| Key Insights | Details |

|---|---|

| Network Performance Monitoring Market Size (2025E) | US$1,795.9 Mn |

| Market Value Forecast (2032F) | US$4,148.6 Mn |

| Projected Growth (CAGR 2025 to 2032) | 12.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.2% |

Market Dynamics

Driver - Exponential Growth in 5G Network Deployment and IoT Device Proliferation

The exponential expansion of 5G networks, surpassing 2.25 billion global connections as of April 2025, is driving significant demand for advanced network performance monitoring solutions. With North America accounting for over 182 million 5G connections and sustaining nearly 20% annual growth, NPM tools are essential to manage high-density traffic, network slicing, and quality-of-service assurance.

The proliferation of IoT devices, rising from 10.3 billion in 2018 to 25 billion by 2025, as noted by Forbes, is generating massive telemetry data that traditional monitoring systems cannot efficiently process. This convergence underscores the critical role of intelligent, scalable NPM platforms in maintaining network visibility and reliability in data-intensive 5G and IoT environments.

Critical Imperative to Minimize Network Downtime and Ensure Business Continuity

The growing financial and operational impact of network downtime has made uptime assurance a critical business priority. ITIC’s 2024 survey indicates that over 90% of mid-sized and large enterprises incur losses exceeding US $300,000 per hour of downtime, with 41% facing costs between US $1 million and US $5 million.

EMA’s 2024 data further shows a 60% rise in per-minute downtime costs for firms with under 10,000 employees, underscoring rising digital dependency. This escalating risk is driving enterprises to adopt proactive network performance monitoring solutions powered by predictive analytics and automated anomaly detection to prevent outages and ensure business continuity.

Restraint - High Deployment Costs and Resource Demands in Enterprise NPM Implementations

The deployment of enterprise-grade network performance monitoring solutions demands significant financial and technical resources, creating a major adoption barrier. Organizations must invest heavily in software licensing, hardware infrastructure, and integration services, with implementation often extending over several months.

For small and medium-sized enterprises, deploying NPM across hybrid or distributed environments costs several hundred thousand dollars annually, including maintenance and staff training. The complexity of integrating these tools with legacy systems and managing specialized operations further increases the total cost of ownership, limiting accessibility for smaller firms.

Shortage of Skilled Professionals in Network Management and IT Operations

A growing shortage of critical skills in network management and IT operations is increasingly constraining the market. According to a study, by 2026, over 80-90% of organizations are projected to experience productivity and operational losses exceeding $5 trillion due to the global IT talent gap.

Expertise in network operations, cloud architecture, and AI-driven analytics, essential for advanced NPM deployment, remains in short supply. With specialized skills becoming obsolete within roughly 2.5 years, enterprises are compelled to invest continuously in retraining to sustain network efficiency and innovation.

Opportunity - Leveraging AI and ML for Predictive Network Intelligence

The integration of AI and ML is transforming NPM from reactive management to predictive network intelligence by enabling real-time analysis of vast telemetry data, anomaly detection, and automated root cause analysis. Predictive analytics supports proactive capacity planning and hardware failure forecasting, minimizing downtime.

For instance, India’s NASSCOM AI Adoption Index 2024 shows 87% of enterprises deploying AI solutions, while the UK’s AI Sector Study 2024 highlights a 68% surge in AI-company revenues to £23.9 billion, underscoring strong global momentum toward AI-driven NPM solutions.

Edge Computing and SD-WAN Adoption Creating Opportunities for Decentralized Network Monitoring

The growing adoption of edge computing and SD-WAN architecture presents a significant opportunity for the network performance monitoring market. As edge deployments process data closer to the source to support low-latency applications like autonomous vehicles, industrial automation, and augmented reality, enterprises require distributed NPM solutions that ensure seamless visibility and performance across hybrid cloud-edge environments.

SD-WAN adoption is driving demand for advanced monitoring tools capable of validating QoS, tracking multi-path connectivity, and optimizing application-aware traffic.

According to a European Commission survey, among organizations deploying edge solutions, 35.7% cited customer experience as their main focus, followed by 32.2% for visual inspection and 30.2% for process automation, underscoring the growing need for advanced NPM tools that ensure performance across distributed infrastructures.

Category-wise Analysis

By Component, Hardware Leading with High-Performance Monitoring and Real-Time Network Visibility

Hardware is expected to account for more than 53% share in 2025 due to the rising deployment of high-speed networking infrastructure, including switches, routers, and monitoring probes that enable real-time traffic visibility and fault detection.

Enterprises are investing heavily in specialized appliances to manage growing data volumes, complex multi-cloud networks, and low-latency edge environments. The need for high-performance monitoring at both core and edge networks drives demand for advanced hardware-based solutions that ensure scalability, reliability, and minimal packet loss.

Platforms/software are growing at the highest rate due to the increasing need for real-time visibility, automation, and analytics. Cloud-native monitoring platforms offer superior scalability, enabling organizations to expand monitoring coverage across hybrid multi-cloud environments without hardware procurement delays.

Software-defined monitoring approaches leverage virtual appliances and containerized collectors that can be rapidly deployed across distributed infrastructures. The integration of AI and ML capabilities within software platforms is delivering advanced analytics, automated anomaly detection, and predictive insights that hardware-centric solutions cannot match.

By Enterprise Size, Large Enterprises Leading Growth Owing to Complex Hybrid Infrastructures and High Network Reliability Demands

Large enterprises are expected to account for over 67% share in 2025, driven by their complex multi-site network infrastructures, substantial IT budgets, and critical dependence on network availability for business operations. Large organizations operate sophisticated hybrid environments spanning on-premises data centers, multiple public cloud platforms, and distributed branch networks requiring comprehensive end-to-end monitoring.

These enterprises invest in enterprise-grade NPM solutions with advanced features, including AI-driven analytics, integrated security capabilities, and extensive vendor support. The financial impact of network downtime for large enterprises averages $23,750 per minute.

Small and mid-sized enterprises are expected to witness rapid growth as they accelerate digital transformation to boost agility and competitiveness. With rising dependence on cloud applications, remote workforces, and digital customer engagement, SMEs require enterprise-grade network visibility.

Affordable, cloud-based NPM and managed monitoring services are bridging the IT skills gap, offering advanced performance analytics and proactive issue detection. As SMEs expand their cloud infrastructure, this segment is projected to sustain strong double-digit growth in the NPM market.

By End-user, Enterprises Leading with Rising Demand for Scalable and Proactive Network Performance Management

Enterprises are expected to account for more than 38% share in 2025 due to their growing dependence on complex, hybrid IT infrastructures that span on-premises, cloud, and edge environments. Rising adoption of bandwidth-intensive applications, remote workforce expansion, and multi-cloud strategies further amplify the need for advanced monitoring solutions.

Enterprises rely on NPM tools to ensure uninterrupted connectivity, optimize network resources, and proactively detect performance bottlenecks. These solutions also support compliance, enhance user experience, and enable seamless digital transformation initiatives.

Cloud service providers represent the fastest-growing segment, driven by exponential data center capacity expansion and investments in AI infrastructure. Major providers such as AWS, Azure, and Google Cloud are deploying massive hyperscale data centers to support growing demand and hold the largest share of the global cloud market.

These providers require ultra-high-performance monitoring solutions capable of analyzing terabit-scale traffic volumes, detecting anomalies across millions of virtual machines, and ensuring service-level agreement compliance for enterprise customers.

Regional Insights

North America Network Performance Monitoring Market Trends

North America is expected to account for over 35% of the network performance monitoring market by 2025, driven by early technology adoption, robust IT infrastructure, and a mature provider ecosystem. The region’s growth is fueled by rapid cloud and edge computing expansion, 5G rollout, and zero-trust mandates, enhancing demand for real-time visibility.

U.S. federal initiatives, including CISA’s 2024 focus on critical infrastructure monitoring (reducing average exploitable services from 12 to ~8), highlight security-driven NPM adoption. Enterprises increasingly rely on NPM to manage latency-sensitive workloads such as AI, telehealth, and video conferencing, integrating it with security analytics to ensure performance, resilience, and compliance across hybrid and distributed environments.

Asia Pacific Network Performance Monitoring Market Trends

Asia Pacific region represents the fastest-growing market, fueled by large-scale 5G rollouts, government smart city programs, and expanding fintech and manufacturing applications. China leads regional growth with a 16.1% CAGR (2025 - 2032), supported by hyperscale data centers, nationwide 5G core deployment, and over 1.1 billion internet users with 206.83 million ≥1,000 Mbps broadband connections driving high-capacity monitoring needs.

India’s growth is propelled by digital infrastructure initiatives like UPI and over 350 million 5G subscribers demanding reliable telecom networks. Japan shows mature adoption, focusing on AI-driven predictive analytics and automation to enhance reliability across finance, manufacturing, and healthcare sectors.

Europe Network Performance Monitoring Market Trends

European network performance monitoring market is expanding steadily, driven by large-scale IT modernization and stringent regulatory mandates such as the Digital Operational Resilience Act (DORA) that require continuous monitoring and operational resilience. Germany leads with heavy investments supporting Industry 4.0, as gigabit-capable broadband reached ~76.5% of households by mid-2024.

The UK follows with a projected 11.9% CAGR (2025 - 2032), fueled by rising cybersecurity needs, remote work infrastructure, and critical infrastructure monitoring, as 63% of SMEs gained access to full-fibre networks by July 2024. France’s growth is anchored in regulated sectors such as banking and healthcare, adopting cloud-first strategies.

Rising cloud and edge adoption under the EU’s digital and cloud policies further amplify demand for distributed telemetry and power-aware NPM solutions aligned with carbon reduction and data sovereignty goals.

Competitive Landscape

The network performance monitoring market is moderately fragmented, with competition driven by both established technology giants and emerging specialized vendors. Companies are adopting innovation-led strategies, integrating AI, ML, and automation to enhance real-time analytics and predictive performance insights.

They are also forming strategic partnerships with cloud providers and network equipment manufacturers to boost interoperability and expand their customer base. Continuous investment in R&D and cybersecurity integration helps differentiate their solutions and address the growing complexity of hybrid and multi-cloud network environments.

Key Industry Developments

- In February 2025, Juniper Networks and IBM expanded their collaboration to integrate Juniper’s Mist AI with IBM’s watsonx platform, aiming to simplify IT network management, enhance user experience, and reduce operational costs.

- In December 2024, Amazon introduced CloudWatch Network Monitoring with flow monitors, enabling near real-time visibility into network performance across AWS workloads like EC2, EKS, S3, RDS, and DynamoDB. The feature provides TCP-based metrics for packet loss, latency, and network health, helping users quickly identify whether issues stem from their application stack or AWS infrastructure and streamline troubleshooting with AWS Support.

- In January 2024, Juniper Networks launched the industry’s first AI-Native networking platform, designed to deliver reliable, secure, and measurable end-to-end connectivity across campus, branch, and data center networks. Powered by its unified AI engine and Marvis Virtual Network Assistant, the platform enables full AIOps capabilities, cutting operational costs by up to 85% and reducing network issues and onsite visits by up to 90%.

Companies Covered in Network Performance Monitoring Market

- Microsoft Corporation

- Juniper Networks

- SolarWinds Worldwide, LLC

- Cisco Systems, Inc.

- ManageEngine (Zoho Corp)

- Niagara Networks

- Ixia

- Profitap HQ B.V.

- Paessler AG

- Nagios Enterprises, LLC

- LogicMonitor, Inc.

- Cubro Network Visibility

- Xena Networks

- Gigamon

- IBM Corporation

- Others

Frequently Asked Questions

The global network performance monitoring market is projected to be valued at US$1,795.9 Mn in 2025.

The growing need for real-time visibility, reliability, and optimization of complex hybrid networks is a key driver of the market.

The market is poised to witness a CAGR of 12.7% from 2025 to 2032.

Adoption of AI-driven analytics, cloud-based monitoring solutions is creating strong growth opportunities.

Microsoft Corporation, Juniper Networks, SolarWinds Worldwide, LLC, Cisco Systems, Inc., ManageEngine, and IBM Corporation are among the leading key players.