- Renewable Energy

- Green Hydrogen Market

Green Hydrogen Market Size, Share, Trends, Growth, and Regional Forecasts 2025 - 2032

Green Hydrogen Market by Technology(Alkaline Electrolyzer, Polymer Electrolyte Membrane (PEM)Electrolyzer), Application (Power Generation, Transportation, Others), Distribution Channel (Pipeline, Cargo, ), and Regional Analysis 2025 - 2032

Green Hydrogen Market Share and Trends Analysis

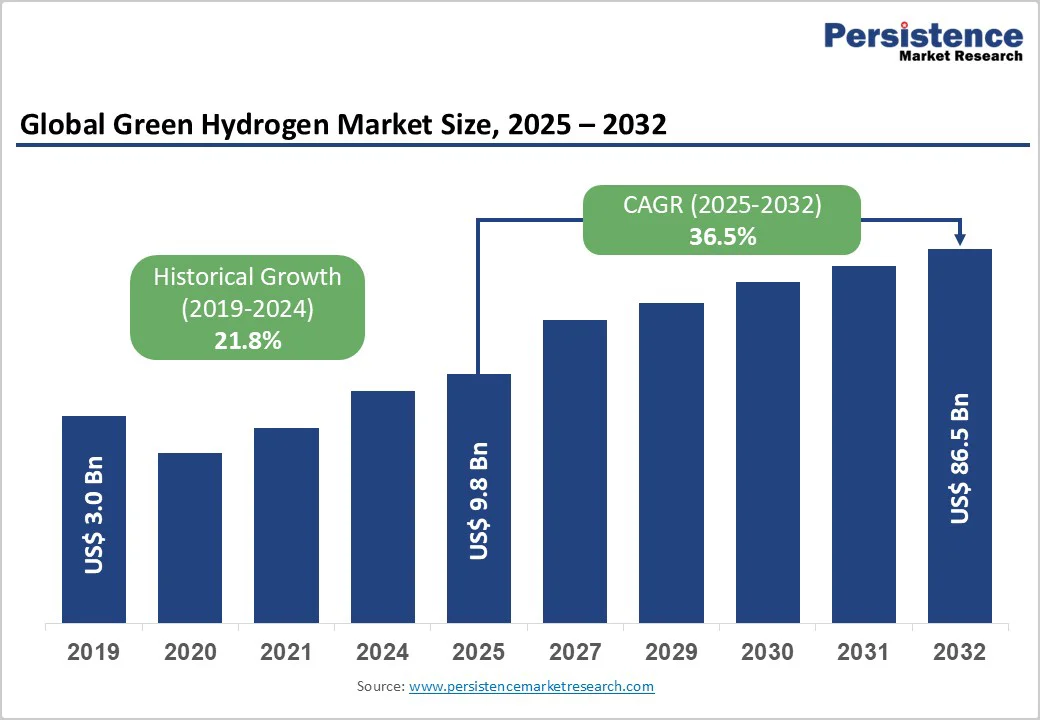

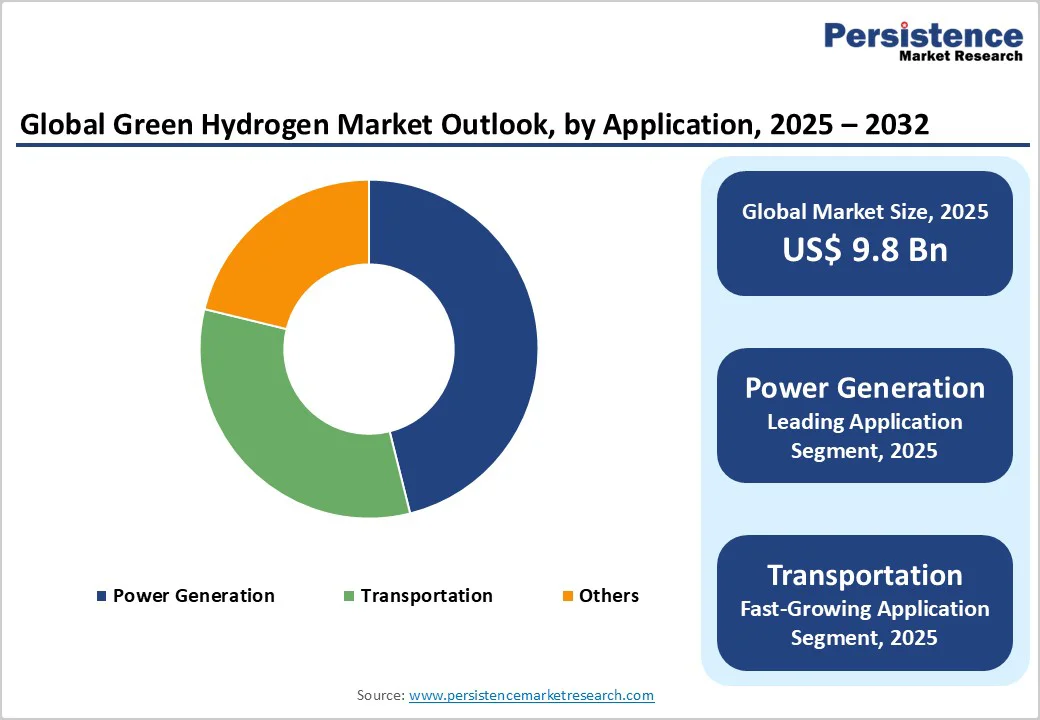

The global green hydrogen market size is likely to value at US$ 9.8 billion in 2025 and is projected to reach US$ 86.5 billion by 2032, growing at a CAGR of 36.5% between 2025 and 2032. This explosive growth trajectory is driven by accelerating decarbonization commitments across heavy industries, substantial government policy support including production tax credits, and rapidly declining renewable energy costs that enhance green hydrogen's economic competitiveness.

The market benefits from unprecedented government funding allocations, with the U.S. Infrastructure Investment and Jobs Act providing US$ 8 billion for Regional Clean Hydrogen Hubs, while global electrolyzer manufacturing capacity is projected to exceed 165 GW annually by 2030, creating the production infrastructure necessary for large-scale deployment across power generation, transportation, and industrial applications.

Key Highlights Summary

- Polymer Electrolyte Membrane (PEM) Electrolyzers represent the fastest-growing technology at 37.4% CAGR, outpacing the market-leading Alkaline segment's 57% share through superior renewable integration and operational flexibility.

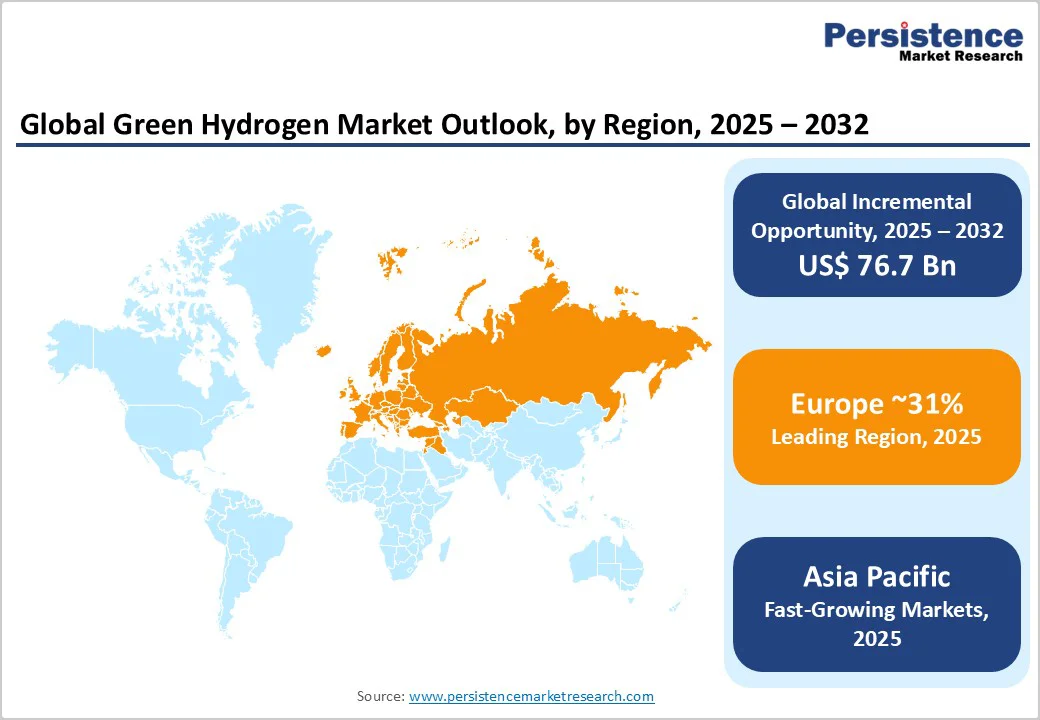

- Asia Pacific leads with the fastest regional growth at 38.9% CAGR and commands a dominating manufacturing capacity of global electrolyzer, with China controlling 60% of production, driving worldwide cost reduction.

- Transportation emerges as the fastest-growing application at 38.6% CAGR, propelled by fuel cell electric vehicle adoption, hydrogen-powered commercial fleets, and sustainable aviation fuel development beyond Power Generation's 46% market leadership.

- Government policy support provides unprecedented catalyst with U.S. offering up to US$ 3.00/kg production tax credits, EU mandating 42% industrial renewable hydrogen by 2030, and global hydrogen hub funding exceeding US$ 8 billion.

- North America demonstrates 35.2% CAGR growth with 76 green hydrogen projects totaling approximately US$ 36 billion investment, including Plug Power's capacity expansion to 500 tons daily by end-2025.

- Global electrolyzer manufacturing capacity reached 25 GW annually in 2023 with projections exceeding 165 GW by 2030, reflecting industry-scale infrastructure buildout supporting multi-gigawatt hydrogen production facilities worldwide.

| Key Insights | Details |

|---|---|

| Green Hydrogen Market Size (2025E) | US$ 9.8 billion |

| Market Value Forecast (2032F) | US$ 86.5 billion |

| Projected Growth CAGR (2025-2032) | 36.5% |

| Historical Market Growth (2019-2024) | 21.8% |

Market Dynamics Analysis

Market Drivers

Aggressive Government Policy Support and Production Incentives

Government policies and financial incentives constitute the most powerful catalyst driving green hydrogen market expansion, with regulatory frameworks establishing mandatory adoption targets and subsidies bridging the cost gap between green and conventional hydrogen. The European Union's Renewable Energy Directive III mandates that 42% of hydrogen used industrially must be produced from renewable sources by 2030, creating compulsory demand totaling approximately 29 PJ of green hydrogen annually for the Netherlands alone, with similar obligations across all member states. The U.S. Inflation Reduction Act's Section 45V Production Tax Credit offers unprecedented support of up to US$ 3.00 per kilogram for clean hydrogen production over ten years, making American green hydrogen projects economically competitive and attracting massive private capital deployment. Global policy momentum is accelerating, with India’s US$2.4 billion National Green Hydrogen Mission, Japan’s US$100 billion hydrogen strategy, and the U.S. investing US$7 billion in Regional Clean Hydrogen Hubs. These initiatives, alongside US$1 billion in demand-side support, establish strong production and offtake frameworks. Together, they create a resilient global policy architecture that drives large-scale deployment and investor confidence, shielding the market from short-term price volatility.

Decarbonization Imperatives Across Hard-to-Abate Sectors

The urgent requirement to decarbonize heavy industries, long-distance transportation, and energy-intensive manufacturing sectors where direct electrification proves technically or economically infeasible is creating structural demand for green hydrogen as the only viable zero-emission solution. Global hydrogen demand is projected to quadruple from 125 million tons in 2030 to over 500 million tons by 2050, driven primarily by steel production, chemical manufacturing, and heavy-duty transportation requiring high-energy-density fuels.

The steel industry alone presents massive decarbonization opportunities, with green hydrogen enabling direct reduction iron (DRI) processes, eliminating coal-based blast furnaces, while the refining sector currently consuming approximately 6 million metric tons of predominantly gray hydrogen annually represents immediate substitution potential reducing carbon intensity by 12%.

The green hydrogen revolution is transforming hard-to-decarbonize sectors, with maritime shipping adopting hydrogen fuel cells and ammonia-based propulsion to achieve zero-emission operations. Aviation gains momentum through hydrogen’s superior 120 MJ/kg energy density, enabling sustainable fuel production and regional fuel cell aircraft. On land, hydrogen powers buses, trucks, and trains, as seen in India’s SIGHT initiative, while its use in long-duration energy storage balances renewable intermittency, stabilizing grids as clean energy surpasses 50% generation share.

Restraint - High Production Costs and Green Premium Challenges

The substantial cost differential between green hydrogen and conventional gray hydrogen represents the industry's most significant commercial barrier, creating financing hurdles and limiting market penetration despite technological progress. Green hydrogen production costs currently range from US$ 4.00 to US$ 12.00 per kilogram globally, with European clean hydrogen levelized costs spanning US$ 5.00-8.00/kg, compared to gray hydrogen's US$ 1.00-3.00/kg production costs. This "green premium" of US$2.00-5.00/kg creates acute challenges for downstream markets, including fertilizer production, where companies struggle to pass increased costs to price-sensitive agricultural customers.

High capital intensity continues to challenge affordability, with large-scale green hydrogen plants demanding multibillion-dollar investments that delay final investment decisions. Despite a global pipeline exceeding US$570 billion, only a fraction has reached execution, underscoring investor caution. Stark regional cost disparities, Chinese electrolyzers costing one-fourth of Western systems, create both opportunity and imbalance. Meanwhile, enormous electricity demand exceeding EU’s annual generation highlights the competition between hydrogen production, EV charging, and broader industrial electrification priorities.

Infrastructure Deficits and Distribution Network Limitations

The absence of comprehensive hydrogen transportation, storage, and distribution infrastructure constitutes a critical bottleneck limiting market scalability and creating chicken-and-egg coordination problems between supply and demand development. Dedicated hydrogen pipeline networks remain nascent, with the European Union targeting 11,600 km of hydrogen pipelines by 2030 and 39,700 km by 2040, requiring massive capital deployment for new construction or natural gas pipeline conversions that face technical challenges, including hydrogen embrittlement of steel components and hydrogen permeation risks.

Pipeline conversion feasibility differs widely, with 15–20% hydrogen blending into gas grids needing minimal changes, while full conversion demands major material upgrades and FRP pipelines offering 20% cost savings pending approval. Infrastructure gaps, costly storage, limited refueling, and complex logistics, continue hindering large-scale green hydrogen and FCEV deployment.

Opportunity - Emerging Markets and Export-Oriented Production Hubs

Developing economies with abundant renewable energy resources and low-cost renewable electricity generation potential present transformative opportunities for establishing large-scale green hydrogen production hubs serving both domestic consumption and international export markets.

Asia Pacific demonstrates particularly strong growth potential, with a CAGR of 38.9%, driven by supportive government policies, renewable energy expansion, and industrial decarbonization requirements. India is emerging as a global green hydrogen powerhouse through its National Green Hydrogen Mission backed by US$ 2.4 billion funding and a 1.5 GW PEM electrolyzer tender, leveraging vast solar potential and projects such as Kakinada integrating existing ammonia infrastructure. China dominates electrolyzer manufacturing and leads capacity additions, positioning the nation as both major consumer and equipment exporter.

The Middle East leads mega-projects such as Saudi Arabia’s US$ 8.4 billion NEOM, exporting 200,000 tons annually. Africa targets 1.5–2.0 million tons of renewable hydrogen exports to the EU, Australia aims for 3 million tons/year by 2030, and Latin America benefits from production costs nearing US$ 0.50/kg, supported by US$ 11 trillion in global shipping infrastructure investments through 2050.

Technology Integration and Digital Optimization Systems

The convergence of artificial intelligence, Internet of Things connectivity, and advanced process control systems with electrolyzer operations creates opportunities for performance optimization, predictive maintenance, and renewable energy integration, maximizing hydrogen production economics.

AI integration is rapidly transforming the hydrogen electrolyzer market by improving efficiency, lowering costs, and enhancing green hydrogen adoption, with capabilities including real-time operating parameter adjustment based on renewable energy availability, electrolyzer voltage and current density optimization matching fluctuating inputs, and predictive algorithms identifying component degradation before failures occur.Digital innovation is transforming the green hydrogen landscape, with smart scheduling optimizing electrolyzer use through real-time weather and price signals, boosting utilization to as high as 60 to 70%. AI-driven catalyst research accelerates the discovery of low-cost alternatives to precious metals, while digital twin technologies reduce risk and speed up gigawatt-scale deployment. Blockchain-based certification enhances transparency and compliance, and remote monitoring platforms turn distributed electrolyzers into virtual power plants, unlocking new revenue through grid balancing and demand response.

Category-wise Analysis

Technology Analysis

The Alkaline Electrolyzer segment dominates technology segmentation with 57% market share in 2025, reflecting its status as the most mature and cost-effective electrolysis technology available commercially. Alkaline electrolyzers benefit from established manufacturing processes, longer operational track records exceeding 60,000 hours, and capital costs ranging €242-388/kW compared to €384-1,071/kW for PEM systems, making them preferred choices for large-scale industrial hydrogen production where continuous operation aligns with technology characteristics. Chinese manufacturers offer particularly competitive alkaline systems priced as low as US$ 303/kW for 10 MW installations, driving global cost benchmarks and enabling developing market deployment.

The technology's reliance on inexpensive materials avoiding precious metals further enhances economic attractiveness, though operational flexibility limitations requiring continuous protective current during standby restrict integration with highly intermittent renewable sources. However, Polymer Electrolyte Membrane (PEM) Electrolyzers represent the fastest-growing segment with an exceptional 37.4% CAGR through 2032, driven by superior performance characteristics including compact design, ability to operate at variable loads matching renewable energy intermittency, and higher current densities enabling smaller footprints. PEM technology's rapid response to power fluctuations and ability to handle renewable energy dynamics makes it ideally suited for wind and solar integration, addressing the fundamental challenge of utilizing intermittent generation for hydrogen production.

Application Analysis

Power Generation leads application segmentation with 46% market share in 2025, reflecting hydrogen's critical role as long-duration energy storage medium balancing renewable energy variability and providing grid stability services. Hydrogen-based energy storage enables excess renewable generation conversion during peak production periods for later reconversion to electricity via fuel cells or gas turbines during demand surges, addressing fundamental intermittency challenges as wind and solar penetration increase.

Stationary power applications including backup power systems for telecommunications and data centers leverage fuel cell reliability and quick-start capabilities, with Plug Power deploying 1 MW PEM electrolyzers at Amazon facilities powering fuel cell forklifts demonstrating integrated ecosystem development.

The transportation sector emerges as the fastest-growing application with an impressive 38.6% CAGR through 2032, propelled by fuel cell electric vehicle adoption, hydrogen-powered commercial vehicles, and emerging maritime and aviation applications. FCEVs deliver fast refueling, 300–400-mile range, and zero emissions, making them ideal for long-range and heavy-duty transport. Buses, trucks, and trains benefit from centralized refueling, as seen in Horizon Fuel Cell’s 42-ton truck projects and India’s hydrogen train program, while maritime and aviation sectors drive further adoption momentum.

Distribution Channel Analysis

Pipeline distribution commands dominant 67.4% market share in 2025, reflecting its status as the most cost-effective method for transporting large hydrogen volumes over medium distances where infrastructure exists or can be economically developed. Pipeline transport offers lower operational costs compared to trucked or shipped hydrogen, with existing natural gas pipeline repurposing providing accelerated deployment pathways albeit requiring materials compatibility assessments and regulatory approvals.

The European Hydrogen Backbone initiative proposes a pan-European pipeline network connecting over 20 countries enabling transnational hydrogen trade, while California's ARCHES Hub released requests for information on hydrogen-dedicated open-access pipelines designed similarly to current natural gas transmission systems, enabling cost-effective distribution and demand aggregation.

Cargo distribution, encompassing trucked compressed gas, liquid hydrogen tankers, and maritime ammonia shipping, represents the fastest-growing channel with 37.0% CAGR through 2032, driven by international hydrogen trade development and point-to-point delivery requirements where pipeline construction proves economically infeasible. Liquid hydrogen shipping enables global trade linking low-cost producers with major demand centers, supported by rising infrastructure investments. Truck transport serves smaller users, while ammonia conversion facilitates large-scale maritime shipping using existing infrastructure with reconversion needed at destination ports.

Regional Market Insights

North America Green Hydrogen Market Trends

North America demonstrates robust growth momentum with 35.2% CAGR through 2032, propelled by the U.S. Inflation Reduction Act's transformative policy support and strategic positioning as global green hydrogen production leader. The U.S. green hydrogen market is projected to grow at a 37.5% CAGR, driven by energy security priorities, clean energy transition acceleration, and declining production costs. The Infrastructure Investment and Jobs Act's US$ 8 billion allocation for Regional Clean Hydrogen Hubs, with seven hubs announced, including California's ARCHES. Major production facilities are rapidly coming online, including Plug Power's Georgia plant producing 15 tons per day representing North America's largest green hydrogen facility, with additional Tennessee and Louisiana sites combining for approximately 40 tons daily capacity and a Texas plant adding 45 tons per day by end-2025.

The regulatory framework's generosity, offering up to US$ 3.00/kg production tax credits over ten years, makes American green hydrogen projects economically competitive without requiring carbon pricing mechanisms, though final 45V guidance released December 2024 created initial uncertainty subsequently resolved providing investment confidence. Strategic partnerships are accelerating deployment, as seen with Plug Power's joint ventures with SK Group in Asia and Renault (Hyvia) in Europe, fostering technology transfer and market growth. Large-scale projects in key U.S. states utilize renewable resources, but competition from data centers and changing policies pose challenges despite robust legislative backing.

Europe Green Hydrogen Market Trends

Europe maintains its leadership in the global green hydrogen market with a 30.5% share in 2025, driven by the EU’s ambitious net-zero 2050 goal and intermediate targets of producing 10 million tons of domestic green hydrogen and importing an additional 10 million tons by 2030, supported by massive public–private investments and coordinated cross-border infrastructure initiatives. The Renewable Energy Directive III mandates that 42% of industrially-used hydrogen must be produced from renewable sources by 2030, creating compulsory demand across member states with particular concentration in Germany, Netherlands, France, and Belgium—countries with strong industrial bases requiring hydrogen for heavy industry and transportation decarbonization. Germany emerges as regional leader despite near-term construction sector challenges, with confirmed €500 billion off-budget infrastructure fund and regulatory framework providing unprecedented certainty compared to developing frameworks in Netherlands, France, and Italy.

Major infrastructure initiatives include the European Hydrogen Backbone proposing pan-European pipeline network connecting over 20 countries and the SoutH2 corridor from Tunisia and Algeria through Italy to Austria and Germany covering approximately 40% of REPowerEU import targets. Domestic production is expanding, with 207 clean hydrogen production and consumption projects including 141 already operational, while Sweden, France, and Germany lead capacity additions with combined 219,000 tons of additional renewable hydrogen capacity expected by 2026. Europe is diversifying its green hydrogen supply through import agreements with countries such as Saudi Arabia, Egypt, Morocco, Oman, and Norway, while leading manufacturers like Siemens Energy, Nel ASA, ITM Power, and McPhy Energy anchor production within the region.

Asia Pacific Green Hydrogen Market Trends

Asia Pacific demonstrates the fastest regional growth at 38.9% CAGR through 2032, commanding the largest absolute market size and driven by massive government commitments, unparalleled manufacturing scale, and urgent energy security requirements across the world's most populous nations. The region dominates the global electrolyzer market with around 85 to 90% share in 2024, reflecting concentration of equipment manufacturing particularly in China holding 60% of global electrolyzer production capacity and leading capacity additions with 780 MW cumulative in 2023 and over 9 GW at advanced stages.

Asia-Pacific dominates the global green hydrogen transition, led by China’s massive renewable infrastructure investment, directing half of its US$1.6 trillion energy spending toward renewables and achieving electrolyzer costs four times lower than Western levels. Japan advances its hydrogen society vision with 3 million tons annual output targeted by 2030, supported by US$100 billion funding and Australian import ties. India’s National Green Hydrogen Mission and expanding PEM manufacturing base position it as a key growth hub, while Australia, South Korea, and ASEAN initiatives strengthen regional supply chains, establishing Asia-Pacific as the world’s green hydrogen manufacturing and export powerhouse.

Competitive Landscape

Market Structure

The global green hydrogen market is moderately fragmented, led by Siemens Energy, Nel ASA, Plug Power, ITM Power, Air Liquide, and Linde, collectively holding around 30–35% of global capacity. Increasing vertical integration by players like Plug Power contrasts with specialized firms such as Nel ASA. Europe anchors regulatory-driven innovation, North America benefits from policy incentives, and Asia-Pacific, dominated by China, controls nearly 60% of global electrolyzer manufacturing capacity.

Strategic Developments

Capacity Expansion: In January 2023, Linde announced a new 5-megawatt PEM electrolyzer project in Ontario, California, aimed at meeting the growing hydrogen demand from the mobility sector. The facility, owned and operated by Linde, marks the first step in a broader hydrogen capacity expansion strategy.

Strategic Investment: In January 2021, Linde revealed plans to build and operate the world’s largest 24-megawatt PEM electrolyzer at its Leuna site in Germany. This landmark investment strengthens Linde’s leadership in green hydrogen, supplying clean fuel to industrial clients through its established pipeline network.

Business Strategies

The green hydrogen market is being reshaped by bold innovation, deep integration, and powerful collaborations. Industry leaders are racing to develop next-generation electrolyzers with advanced materials, modular containerized systems, and AI-driven optimization that boost efficiency and cut costs. China leads on manufacturing scale, while gigawatt-scale plants by Siemens Energy, Nel Hydrogen, and Toshiba accelerate cost parity. Emerging models like hydrogen-as-a-service, strategic equity alliances, and public-private hubs fuel rapid adoption, as blockchain-based certification and renewable provenance tracking redefine transparency, trust, and value across the global hydrogen ecosystem.

Companies Covered in Green Hydrogen Market

- Siemens Energy

- Nel ASA

- Plug Power Inc.

- Air Liquide S.A.

- ITM Power plc

- Linde plc

- Air Products and Chemicals Inc.

- Ballard Power Systems

- Cummins Inc.

- McPhy Energy S.A.

- Enapter

- Green Hydrogen Systems

- Toshiba Corporation

- Bloom Energy Corp.

- FuelCell Energy Inc.

Frequently Asked Questions

The global Green Hydrogen Market was valued at US$ 9.8 Billion in 2025 and is projected to reach US$ 86.5 Billion by 2032.

The market is primarily driven by aggressive government policy support, combined with rapidly declining renewable energy and electrolyzer costs and urgent decarbonization imperatives across steel production, refining, transportation, and chemical manufacturing sectors, where direct electrification proves technically or economically infeasible.

The Green Hydrogen Market is projected to grow at an exceptional CAGR of 36.49% from 2025 to 2032.

Major opportunities include emerging markets and export-oriented production hubs, and technology integration through AI-powered optimization systems, improving electrolyzer efficiency 20-30% while enabling renewable energy integration and predictive maintenance reducing operational costs and maximizing capacity utilization.

Leading manufacturers include Siemens Energy (Germany), Nel ASA (Norway), Plug Power (USA), Air Liquide (France), ITM Power (UK), Linde (Ireland/UK), Air Products and Chemicals (USA), Ballard Power Systems (Canada), Cummins (USA), McPhy Energy (France), Toshiba (Japan), and Green Hydrogen Systems (Denmark).