- Specialty & Fine Chemicals

- Gas Separation Membrane Market

Gas Separation Membrane Market Size, Share, and Growth Forecast, 2025 - 2032

Gas Separation Membrane Market by Material Type (Polyimide & Polyaramide, Polysulfone, Cellulose Acetate, Others), Application (Carbon Dioxide Removal, Nitrogen Generation & Oxygen Enrichment, Hydrogen Recovery, Vapor/Vapor Separation, Others), End-Use (Oil & Gas, Chemical, Electric Power, Food & Beverage, Others), and Regional Analysis for 2025 - 2032

Gas Separation Membrane Market Share and Trends Analysis

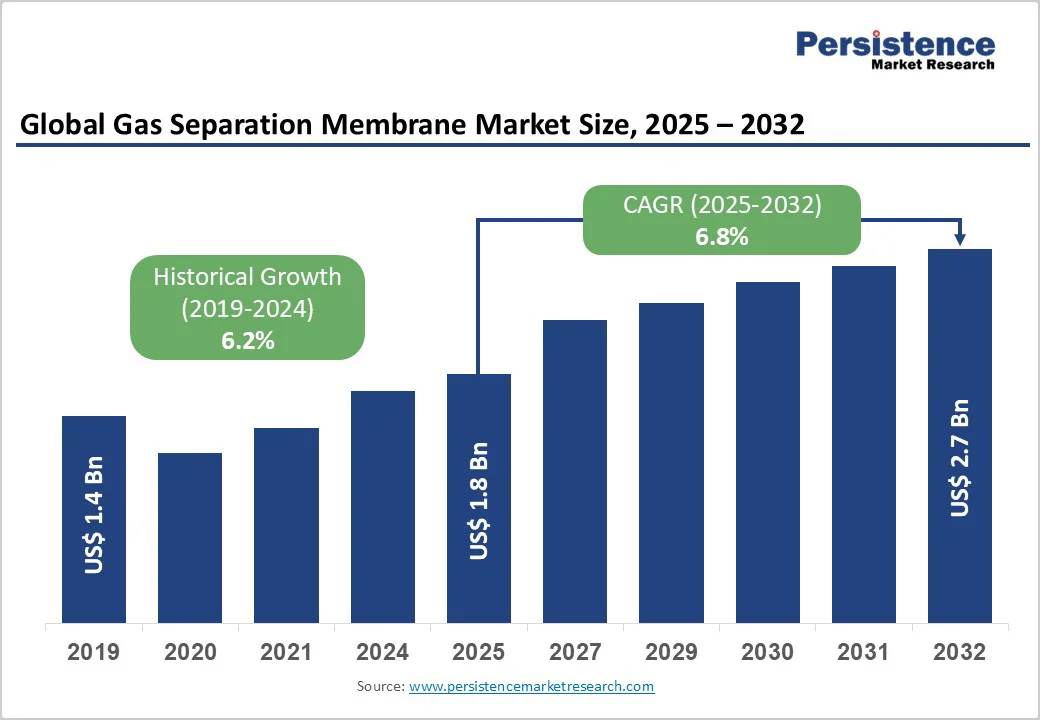

The global gas separation membrane market size is likely to be valued at US$ 1.8 billion in 2025, and is projected to reach US$ 2.7 billion by 2032, growing at a CAGR of 6.0% during the forecast period 2025-2032, driven by a rising demand for energy efficient gas processing solutions amid global sustainability goals. Key growth factors include stringent environmental regulations pushing industries toward low emission technologies and expanding applications in clean energy production, which enhance operational efficiency and reduce carbon footprints. Supporting this are advancements in membrane materials that improve selectivity and durability, coupled with increasing industrialization in emerging economies that boost demand for purified gases in sectors such as oil & gas and chemicals.

Key Industry Highlights

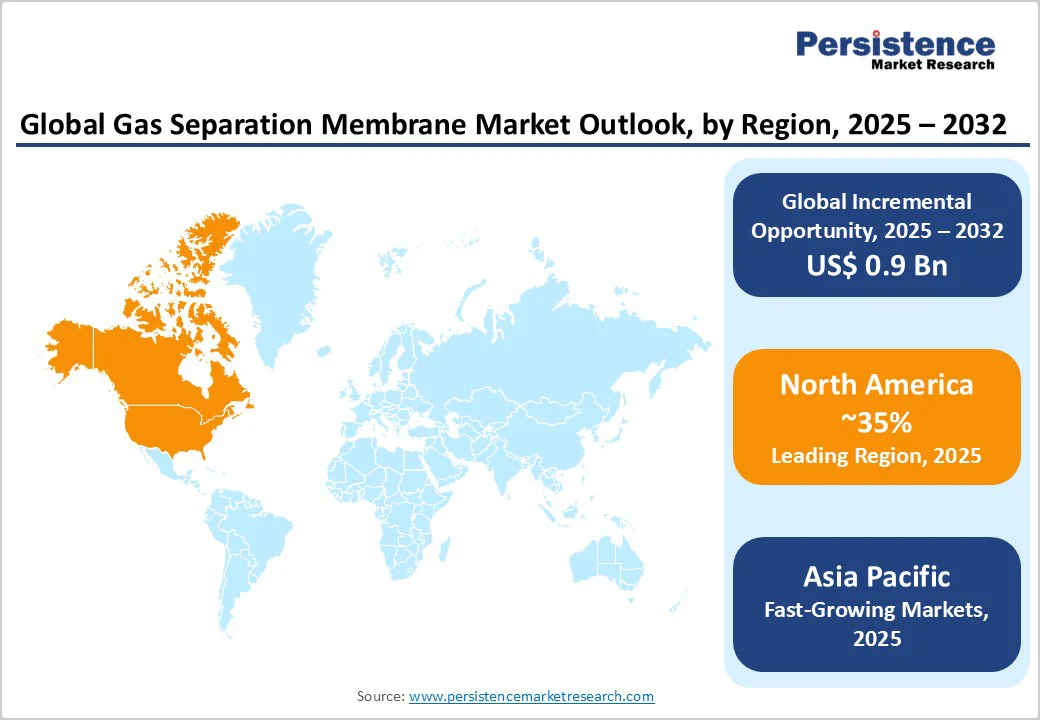

- Regional Leaders: North America dominates as the leading regional market, driven by U.S. regulatory leadership of the U.S. Environmental Protection Agency (EPA) and innovations in clean energy.

- Fastest-growing Regional Market: Asia Pacific is set to emerge as the fastest-growing regional market through 2032, fueled by China's manufacturing scale and India's green hydrogen investments.

- Leading End-User: Oil & Gas stands as the dominant end-user, capturing 45% share in 2025 due to critical applications in natural gas purification and CO2 removal for enhanced recovery processes.

- Fastest-growing Application: Hydrogen recovery is likely to be the fastest-growing application segment, expanding at over 8% CAGR during 2025-2032, propelled by global clean energy transitions and advancements in fuel cell technologies.

- Growth Opportunity: A key market opportunity lies in carbon capture technology expansions, with policies such as the Green Deal of the European Union (EU) that are generating a huge demand for scalable membranes in electric power.

| Key Insights | Details |

|---|---|

|

Gas Separation Membrane Size (2025E) |

US$ 1.8 Bn |

|

Market Value Forecast (2032F) |

US$ 2.7 Bn |

|

Projected Growth CAGR (2025-2032) |

6.0% |

|

Historical Market Growth (2019-2024) |

4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Soaring Demand for Clean Energy Solutions

The push for sustainable energy sources is a primary driver for the Gas Separation Membrane market, as membranes enable efficient separation of gases such as hydrogen and oxygen, crucial for fuel cells and renewable energy applications. According to the International Energy Agency (IEA), global hydrogen demand is expected to increase sixfold by 2050 to meet net-zero targets, directly boosting membrane adoption in hydrogen recovery processes. This is further supported by government incentives, such as the U.S. Department of Energy's funding for clean hydrogen projects, which reached over US$ 7 billion in recent allocations. In the hydrogen market, membranes facilitate cost-effective purification, reducing energy consumption by up to 30% compared to traditional methods, convincing industries of their long-term viability for emission reduction and operational savings.

Global regulations aimed at curbing greenhouse gas emissions are compelling industries to adopt advanced separation technologies, positively impacting the gas separation membrane market growth. The EU’s Emission Trading System has mandated a 55% reduction in emissions by 2030, driving the demand for membranes in carbon capture and storage (CCS) applications. This regulatory pressure, combined with rising natural gas processing needs in the U.S. Natural Gas Market, enhances market growth by offering scalable, low-maintenance solutions that align with international climate agreements such as the Paris Accord.

Prohibitive Initial Investment Costs

The substantial upfront costs associated with installing gas separation membrane systems pose a significant barrier, particularly for small and medium enterprises in developing regions. This is compounded by the need for specialized infrastructure, leading to extended payback periods of 5-7 years, as per IEA estimates. Such financial hurdles negatively affect market penetration, especially in price-sensitive sectors such as food & beverage, where alternatives in the form of cryogenic separation remain more accessible despite higher operational costs.

Membranes often face performance degradation in extreme conditions, such as high temperatures or corrosive gases, limiting their applicability and restraining market growth. The American Society of Mechanical Engineers (ASME) notes that polymeric membranes can lose up to 20% efficiency above 150°C, necessitating frequent replacements and increasing maintenance expenses. This issue is evident in oil & gas operations, where exposure to impurities reduces membrane lifespan, fueling hesitancy among stakeholders regarding reliability concerns and slowing the adoption of gas separation membranes in critical applications despite overall efficiency benefits.

Expansion in Hydrogen Recovery Technologies

The rapid growth of hydrogen as a clean fuel presents a lucrative opportunity for market participants, with membranes poised to dominate recovery processes in emerging green hydrogen projects. The IEA forecasts global hydrogen production to reach 80 million tons annually by 2030, driven by electrolysis and steam methane reforming, where membranes can achieve 95% purity levels. Recent developments, such as Japan's US$ 2 billion investment in hydrogen infrastructure announced in 2024, highlight potential demand surges. Companies can capitalize by innovating durable materials, tapping into policies such as the EU's Hydrogen Strategy, which aims for 40 GW of electrolyzers, generating significant revenue through scalable, eco-friendly solutions.

Increasing focus on CCS technologies offers opportunities in the fastest-growing carbon dioxide removal segment, supported by global net-zero commitments. The Intergovernmental Panel on Climate Change (IPCC) emphasizes CCS as essential for limiting warming to 1.5°C, with membranes enabling cost-effective capture at scales up to 1 million tons per year. This also aligns with policies incentives such as the U.S. 45Q tax credit, extended to US$ 85 per ton of CO2 stored, convincing companies of profitable expansions in electric power and chemical sectors.

Category-wise Analysis

Material Type Insights

Polyimide & polyaramide are likely to emerge as the leading material in 2025, commanding approximately 40% market share due to their superior thermal stability and selectivity in high-pressure environments. The dominant position of this segment is substantiated by industry data showing these materials withstand temperatures up to 200°C with 90% gas permeability, making them ideal for oil & gas applications. The American Chemical Society reports their use in 70% of hydrogen purification processes, supported by enhanced durability that reduces replacement frequency by 25% compared to alternatives such as cellulose acetate. This dominance is further reinforced by their growing demand in the Hydrogen Market, where the chemical resistance of these materials ensures efficient separation, driving adoption across industrial scales.

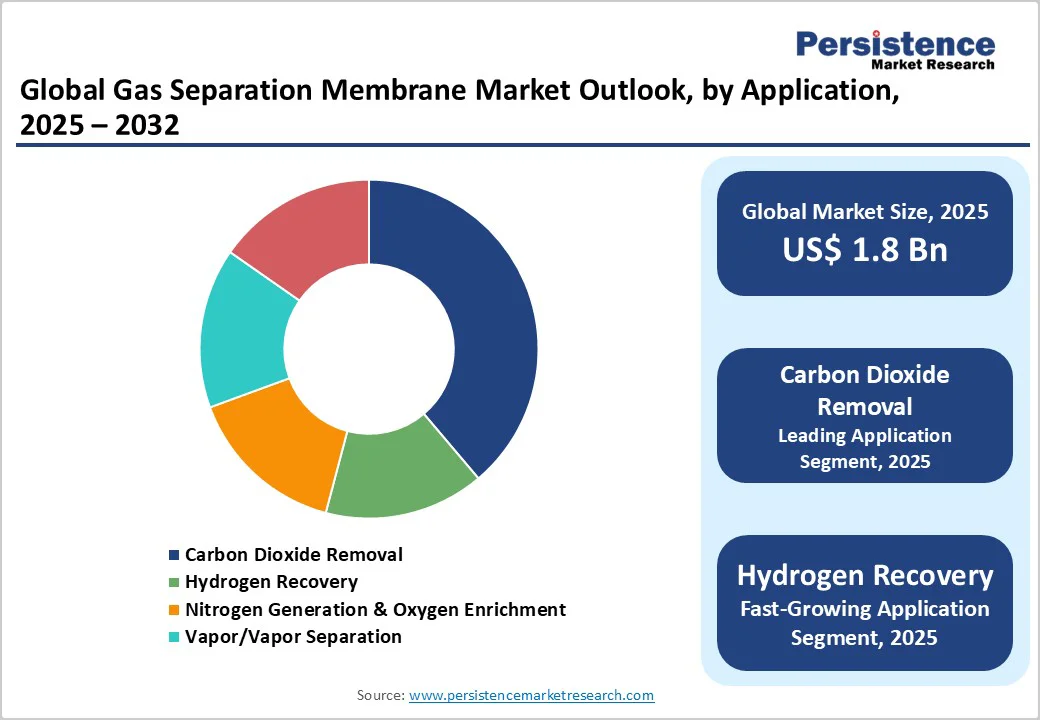

Application Insights

Carbon dioxide removal is projected to emerge as the dominant application, accounting for approximately 35% of the gas separation membrane market revenue share in 2025. This prominence is driven by its essential role in global emission reduction efforts, including widespread adoption in over 50% of CCS projects, as highlighted by the U.S. Department of Energy (DOE). Gas separation membranes are leveraged for their scalability and efficiency in power plants and integrate effectively with processes such as natural gas sweetening in the U.S. market, leading to operational benefits such as reducing downtime by 15%. These attributes enhance process reliability and efficiency, positioning carbon dioxide removal as central amid escalating global decarbonization initiatives. This growth outlook underscores the increasing shift towards advanced membrane technologies in mitigating greenhouse gas emissions and meeting industrial separation requirements.

End-Use Insights

The oil & gas sector dominates the end-use segment of the gas separation membrane market, capturing roughly 45% of the market share in 2025 due to its extensive use in natural gas processing and enhanced oil recovery applications. The World Oil journal highlights membranes’ critical role in processing billions of cubic feet of gas daily, aided by their robust resistance to sour gases. In the U.S., regulatory pressures to reduce methane emissions further drive demand for these membranes, ensuring steady market growth through reliable, low-energy separation solutions. This combination of regulatory support, operational efficiency, and technological advantages positions the oil & gas segment for sustained expansion within the broader gas separation membrane market.

Regional Insights

North America Gas Separation Membrane Market Trends

North America is expected to lead the gas separation membrane market share, fueled by the predominance of the U.S. on the back of its robust regulatory frameworks such as the Clean Air Act, which mandates emission controls in industries. Innovations from firms such as Air Products and Chemicals have advanced membrane durability, with DOE-funded projects achieving significantly higher efficiency in carbon capture since 2023. Moreover, the focus on innovation by regional stakeholders is evident in partnerships, such as Honeywell UOP's 2024 tech upgrades for hydrogen recovery, aligning with the U.S. Natural Gas Market's expansion. Strict EPA guidelines drive demand, positioning North America as a hub for sustainable gas separation advancements.

Europe Gas Separation Membrane Market Trends

The Europe gas separation membrane market thrives on regulatory harmonization under the EU Green Deal, emphasizing emission reductions in the key countries of Germany, the U.K., France, and Spain. Germany's performance excels with over 40% adoption in chemical sectors, per Fraunhofer Institute reports, while the U.K.'s Net Zero Strategy has spurred considerable annual growth in membrane tech since 2023. France and Spain have been contributing through aggressive renewable integrations, with Eurostat noting 25% efficiency improvements in power plants. Harmonized standards, pioneered by the REACH regulations, have facilitated cross-border innovations, supporting applications in hydrogen enrichment. Recent developments include Linde PLC's 2025 expansions in Spain for vapor separation, enhancing regional performance amid unified policies for sustainable industrial practices.

Asia Pacific Gas Separation Membrane Trends

In Asia Pacific, the gas separation membrane market is likely to register the highest growth rate through 2032, propelled by the well-established and highly functional manufacturing ecosystem in China, Japan, India, and ASEAN nations, where low-cost production scales meet rising industrial demands. China's dominance is clear with over 50% regional share, driven by National Development and Reform Commission policies boosting clean energy, as over 60% of biogas projects use membranes, as per IEA data. Japan's tech leadership in polyimide materials supports markedly higher efficiency rates in hydrogen recovery. In India and ASEAN, the market is slated to exhibit dynamic growth through investments like India's US$ 10 billion green hydrogen mission in 2024, leveraging cost-effective manufacturing. This is envisaged to foster rapid adoption in chemicals, with ASEAN's 20% annual increase in oil & gas applications, per regional association reports.

Competitive Landscape

The global gas separation membrane market exhibits a moderately consolidated structure, with top players holding about 60% share through strong portfolios and global presence. Companies pursue expansion via strategic acquisitions and R&D investments, such as developing hybrid membranes for enhanced selectivity. Key differentiators include Air Liquide's focus on sustainable innovations and UBE Corporation's material advancements. Emerging trends involve subscription-based models for membrane services, reducing upfront costs and promoting circular economy practices in industrial applications.

Key Industry Developments

- In July 2025, Air Liquide expanded its operations in Gujarat by establishing a new air separation unit and a cylinder filling station. The new facilities are designed to enhance the supply of industrial gases, supporting local manufacturing, healthcare, and other industrial sectors. This expansion aims to improve supply reliability, reduce logistics costs, and meet the growing demand for industrial gases in the region. The move underscores Air Liquide’s commitment to strengthening its presence in India’s rapidly developing industrial landscape.

- In May 2025, Canadian clean-tech firm Borna Membrane Solutions invested US $40 million to establish a facility in Egypt for manufacturing natural gas separation, flare gas recovery, and carbon capture technologies. The project, backed by the Canadian government and financial institutions, aims to lower emissions, reduce energy imports, and create jobs. Egypt’s private free zones offer Borna tax and customs benefits and proximity to production areas. The initiative also helps Egyptian exporters comply with the EU’s Carbon Border Adjustment Mechanism for lower-carbon product competitiveness.

- In January 2025, Arkema partnered with deep tech startup OOYOO to develop advanced CO2 separation membranes aimed at reducing greenhouse gas emissions. Using Arkema’s expertise in high-performance polymers like Pebax® elastomers, and OOYOO’s proprietary membrane design, the collaboration focuses on creating compact, cost-effective, and highly efficient CO2 capture technology. OOYOO’s membranes significantly cut CO2 recovery costs to less than one-third of traditional methods while enabling smaller installations.

Companies Covered in Gas Separation Membrane Market

- Air Liquide

- Air Products and Chemicals, Inc.

- UBE Corporation

- Honeywell UOP

- Evonik

- Linde PLC

- Atlas Copco AB

- DIC Corporation

- Parker Hannifin Corporation

- FUJIFILM

- Toray Industries

Frequently Asked Questions

The global gas separation membrane market size is projected to reach US$ 1.8 billion in 2025.

Primary market drivers include rising demand for clean energy solutions, such as hydrogen recovery and stringent environmental regulations such as the EU's Emission Trading System mandating 55% emission reductions by 2030.

The market is poised to witness a CAGR of 6.0% from 2025 to 2032.

A key opportunity lies in advancements in carbon capture and storage technologies, along with strong policy support for next-generation sustainability solutions, such as the U.S. 45Q tax credit.

Some of the key market players include Air Liquide, Air Products and Chemicals, Inc., UBE Corporation, and Honeywell UOP.