- Specialty & Fine Chemicals

- Chemical Separation Membranes Market

Chemical Separation Membranes Market Size, Share, and Growth Forecast 2026 - 2033

Chemical Separation Membranes Market by Membrane Type (PTFE Membranes, EPTFE Membranes, PEEK Membranes, and Others), Application (Membrane Distillation, Membrane Liquid Extraction, Gas/Liquid Separation, Gas/Liquid Contacting, Gas Separation, and Others), Industry (Municipal Water Treatment Plants, Food and Beverages, Oil and Gas, and Others), and Regional Analysis, 2026 - 2033

Chemical Separation Membranes Market Size and Share Analysis

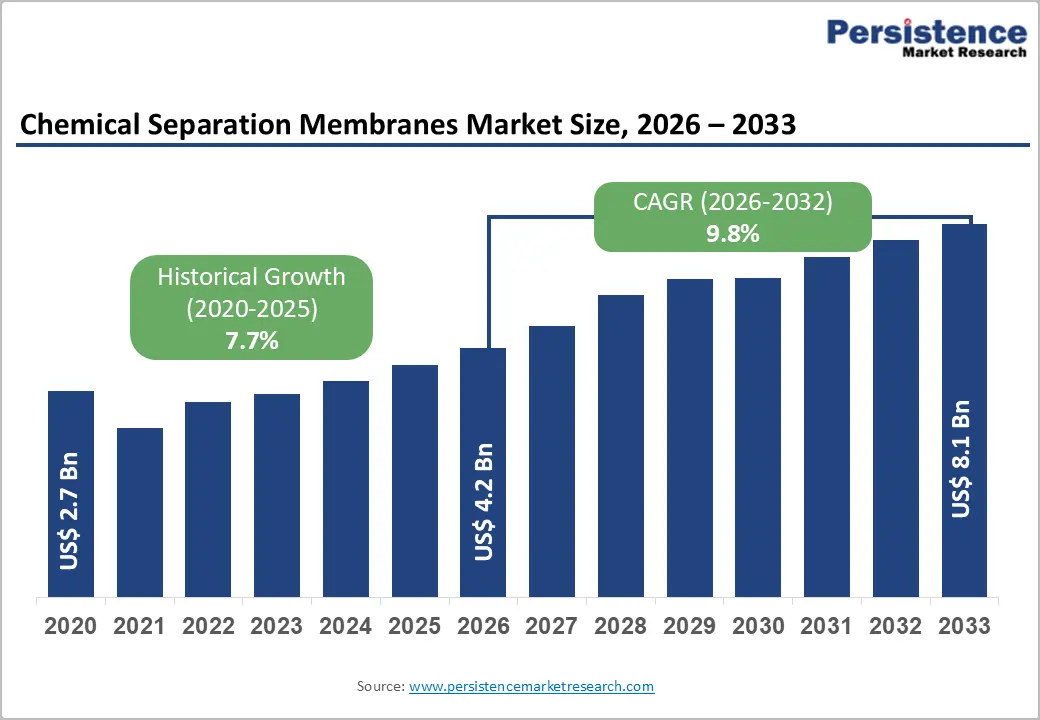

The global chemical separation membranes market size is likely to be valued at US$ 4.2 billion in 2026 and is projected to reach US$ 8.1 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033.

The chemical separation membranes market is experiencing accelerated expansion driven by the rise in demand for advanced water treatment and purification solutions across municipal and industrial sectors, stringent global environmental regulations mandating wastewater treatment and zero liquid discharge (ZLD) implementations, and significant investments in pharmaceutical, food and beverage, and oil and gas processing applications.

Key Industry Highlights:

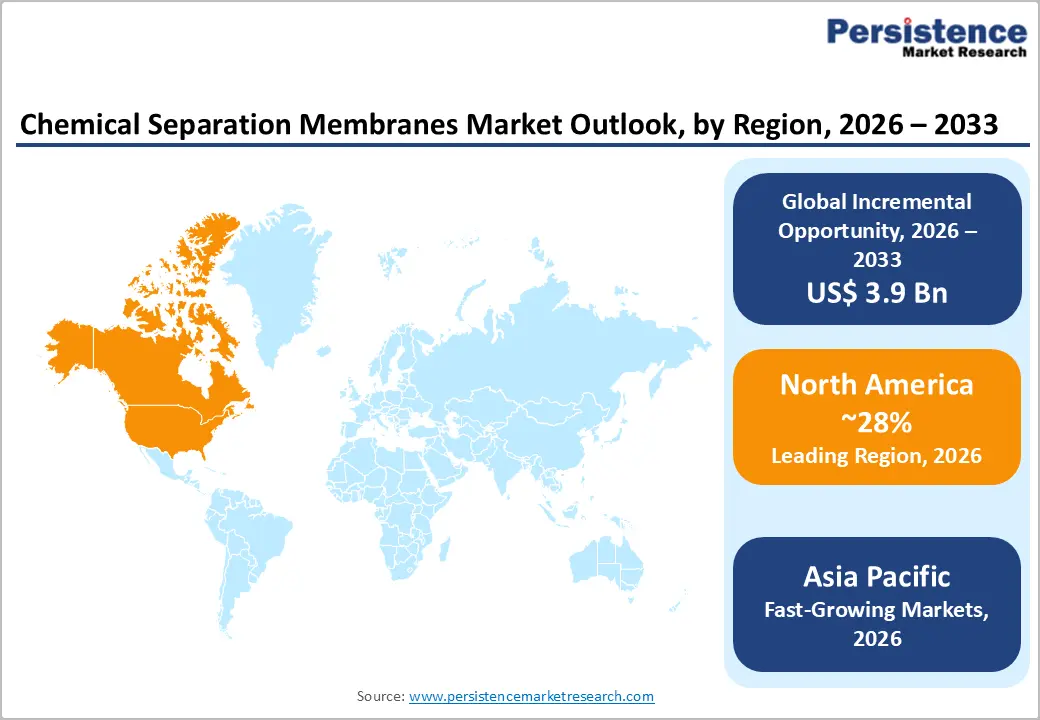

- Leading Region: North America maintains the strongest regional position with approximately 28% global market share, supported by established regulatory frameworks, mature treatment infrastructure, and substantial pharmaceutical manufacturing and industrial separation technology investments.

- Fastest Growing Region: Asia Pacific represents the fastest-growing region, expanding at approximately 10.5% CAGR through 2033, driven by rapid industrialization, pharmaceutical sector expansion, government water infrastructure investment, and emerging manufacturing capacity providing cost-competitive membrane solutions.

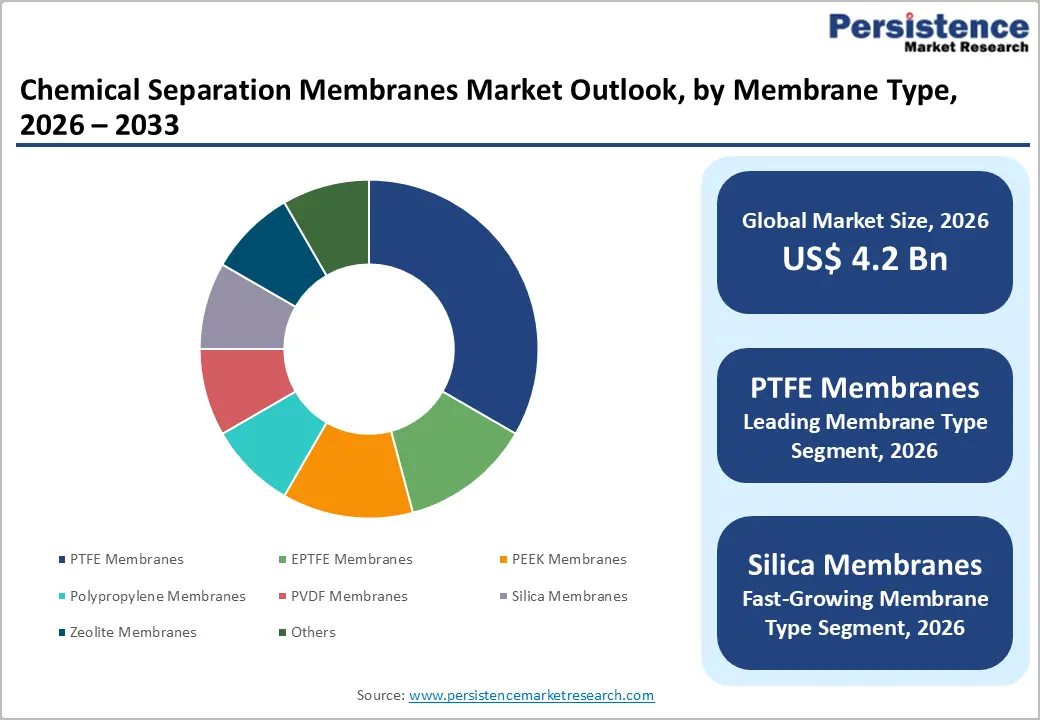

- Leading Membrane Type: PTFE (polytetrafluoroethylene) dominates the market, accounting for approximately 40% share, driven by exceptional chemical resistance enables reliable performance in highly aggressive chemical environments.

- Growing Application: Zero Liquid Discharge (ZLD) emerges as the fastest-growing application in the global Chemical Separation Membranes Market, supported by stringent environmental regulations and tightening industrial wastewater discharge norms accelerating ZLD adoption.

- Key Market Opportunity: Zero liquid discharge and sustainable water recovery applications represent significant long-term market opportunities, with industrial adoption accelerating through 2033 driven by regulatory mandates, sustainability goals, and demonstrated economic benefits from water resource recovery and reuse.

| Key Insights | Details |

|---|---|

| Chemical Separation Membranes Market Size (2026E) | US$ 4.2 Bn |

| Market Value Forecast (2033F) | US$ 8.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 9.8% |

| Historical Market Growth (2020 - 2025) | 7.7% |

Market Dynamics

Drivers - Rising Global Water Scarcity and Municipal Water Treatment Infrastructure Investment

Water scarcity is a critical global challenge, with UN-Water estimates indicating that approximately 2 billion people live in water-stressed regions and 4 billion experience severe water scarcity at least one month annually. This escalating crisis is driving substantial government and private-sector investments in advanced water treatment infrastructure, particularly in emerging markets across the Asia-Pacific region. Municipal water treatment facilities increasingly require sophisticated membrane separation technologies to achieve compliance with drinking water quality standards and environmental regulations.

Advanced membrane processes, including reverse osmosis, ultrafiltration, nanofiltration, and membrane distillation, enable municipalities to treat contaminated water sources and implement water reuse programs meeting sustainability objectives. India's municipal water treatment sector is expanding at approximately 15.9% CAGR, driven by rapid urbanization and government water infrastructure initiatives. The UK water sector is growing at a 12.1% CAGR, supporting continued investment in treatment facility modernization and the deployment of advanced separation membranes across municipal water utilities. This sustained infrastructure investment creates substantial incremental demand for high-performance membrane materials across diverse geographic markets.

Expanding Industrial Wastewater Treatment and Zero Liquid Discharge Regulatory Mandates

Industrial sectors, including oil and gas, pharmaceuticals, chemicals, and food and beverage processing, are subject to increasingly stringent environmental regulations mandating zero liquid discharge (ZLD) or minimal liquid discharge (MLD) practices. ZLD systems eliminate liquid effluent discharge by maximizing water recovery and leaving only solid waste, with membrane technologies including reverse osmosis, membrane distillation, and forward osmosis serving as critical process components. Environmental regulations across the European Union, the United States, and emerging economies in the Asia Pacific establish stringent discharge standards, creating regulatory drivers for ZLD technology adoption across manufacturing facilities.

Advanced membrane configurations that combine multiple separation technologies achieve progressively higher water recovery rates while reducing operational costs by enhancing energy efficiency relative to traditional thermal evaporation. Industrial facilities implementing ZLD systems benefit from recovered water resources suitable for process reuse, reduced environmental liability, and compliance with evolving sustainability mandates. The escalating adoption of membrane-based ZLD systems across diverse industrial sectors represents a significant growth driver for specialized chemical separation membranes engineered for extreme operating conditions and high-salinity feed streams.

Market Restraints

High Capital Investment and Operational Costs Limit Market Adoption

Chemical separation membrane systems require substantial capital investment for equipment procurement, installation, and process integration into existing industrial facilities. Advanced membrane technologies, including specialized PTFE, EPTFE, PEEK, and silica/zeolite membranes, command premium pricing compared to conventional separation approaches. Operational costs, including membrane replacement, energy consumption for pressure- or vacuum-driven separation processes, and system maintenance, represent ongoing financial obligations that limit adoption among cost-sensitive industrial segments and small- to medium-sized enterprises.

The average lifespan of high-performance membranes ranges from 3 to 7 years, depending on operating conditions and feedwater quality, necessitating planned capital expenditures for membrane replacement. Geographic variations in energy costs directly affect total cost of ownership calculations, with regions with high electricity costs experiencing higher operational expenses. These economic barriers constrain market expansion, particularly in price-sensitive emerging markets, where alternative separation technologies offer cost advantages despite lower performance.

Membrane Fouling and Scaling Challenges Impacting System Efficiency and Durability

Membrane fouling and scaling are persistent technical challenges that limit operational efficiency and reduce membrane lifespan across diverse chemical separation applications. Fouling occurs when suspended solids, organic matter, and colloidal substances accumulate on membrane surfaces, progressively reducing permeate flux and system throughput. Scaling occurs when dissolved salts precipitate on membrane surfaces, particularly in reverse osmosis and membrane distillation applications that process high-salinity or mineral-rich feed streams.

These phenomena necessitate frequent membrane cleaning and accelerated replacement cycles, increasing operational downtime and costs. Traditional cleaning methods using chemical solvents and mechanical methods risk permanent membrane damage and environmental contamination. Despite advancements in membrane material science and surface modification techniques, fouling and scaling remain challenging technical issues limiting widespread adoption of membrane-based ZLD systems and advanced separation applications in demanding industrial environments.

Opportunities - Expansion of Pharmaceutical and Biotechnology Industries Driving High-Purity Separation Demand

The pharmaceutical and biotechnology sectors are experiencing robust expansion, with the global biopharmaceutical market projected to reach approximately US$ 600+ billion by 2030. These industries require ultra-high-purity separation membranes for drug compound isolation, protein purification, vaccine manufacturing, and bioprocess applications. Membrane separation technologies, including ultrafiltration, nanofiltration, and specialized pervaporation systems, enable manufacturers to achieve pharmaceutical-grade product purity while meeting stringent regulatory requirements set by agencies such as the U.S. FDA, the European Medicines Agency, and the International Council for Harmonisation (ICH).

The emerging development of biosimilars, monoclonal antibodies, and advanced biologics represents a significant growth opportunity for membrane manufacturers serving the pharmaceutical sector with application-specific separation solutions. Regulatory agencies increasingly require comprehensive analytical characterization of pharmaceutical products, creating sustained demand for membrane-based purification systems in drug development and manufacturing processes. The convergence of pharmaceutical industry growth, regulatory emphasis on product quality, and technological advances in membrane materials positions this segment as a significant future growth opportunity for specialized chemical-separation membranes.

Bio-Based and Sustainable Membrane Technology Development Aligned with Corporate Sustainability Goals

Global corporations are establishing increasingly ambitious sustainability targets, including carbon neutrality commitments and circular economy principles, creating substantial demand for sustainable membrane technologies and processes. Bio-based and recycled-content membrane materials derived from renewable feedstocks offer sustainability credentials supporting corporate environmental goals and regulatory compliance with extended producer responsibility requirements. Advanced membrane configurations incorporating graphene oxide, chitosan, and other novel materials enhance separation performance while reducing environmental impact compared to conventional membrane formulations.

Silica-based zeolite membranes offer emerging opportunities for sustainable gas separation, replacing energy-intensive distillation in petrochemical refining and clean energy production. These materials enable hydrogen purification, carbon dioxide capture, and industrial gas separation with superior energy efficiency and reduced operational costs. The integration of sustainable membrane technologies into industrial processes supports decarbonization initiatives and positions early adopters as sustainability leaders, creating competitive advantages in environmentally conscious markets and supporting long-term growth in specialized membrane segments.

Category-wise Analysis

Membrane Type Insights

PTFE (polytetrafluoroethylene) membranes represent the leading membrane type, commanding approximately 40% market share driven by exceptional chemical resistance, outstanding thermal stability, superior durability in extreme operating conditions, and proven performance across diverse industrial applications. PTFE membranes exhibit exceptional properties, including remarkable resistance to environmental degradation, chemical inertness, and high porosity, enabling superior permeability compared to alternative membrane materials. These characteristics derive from PTFE's unique molecular structure featuring strong carbon-fluorine bonds and uniform helical sheath created by electron cloud of fluorine atoms, delivering unmatched chemical compatibility across aggressive industrial separation environments.

PTFE membranes demonstrate removal efficiencies exceeding 99% for multiple contaminant types, including sulfate, conductivity, iron, and aluminum, with studies reporting exceptional separation performance in membrane distillation, oil-water separation, and advanced filtration applications. The dominant market position reflects established manufacturing processes, comprehensive performance validation for demanding applications, and widespread adoption across pharmaceutical, oil and gas, chemical processing, and municipal water treatment sectors.

Emerging EPTFE (expanded PTFE) membranes exhibit rapid growth driven by enhanced flexibility, thermal stability, and permeability characteristics, enabling applications requiring a combination of robustness and high performance in gas separation and advanced filtration systems.

Application Insights

Gas Separation application represents the leading segment, commanding approximately 35% market share, driven by the widespread integration of gas separation membranes across industries such as petrochemicals, oil & gas processing, hydrogen recovery, and carbon capture, where membrane technologies offer lower energy consumption, reduced operational costs, and enhanced separation performance compared to conventional methods.

Zero Liquid Discharge (ZLD) is among the fastest-growing applications, driven by stricter environmental regulations, rising industrial wastewater volumes, and a growing focus on water recycling and sustainability. Membrane technologies underpinning ZLD systems - including membrane distillation and advanced liquid extraction- enable industries to eliminate effluent discharge and recover valuable water, particularly in water-stressed regions.

Industry Insights

Municipal water treatment plants constitute the largest end-use segment, accounting for approximately 38% of chemical separation membrane demand, driven by the critical importance of advanced water treatment infrastructure in ensuring a safe drinking water supply and environmental protection. Municipal utilities worldwide are investing substantially in the modernization and expansion of treatment facilities to meet escalating regulatory requirements and population growth.

Advanced membrane technologies, including ultrafiltration, nanofiltration, and reverse osmosis, enable municipalities to achieve comprehensive contaminant removal, achieving drinking water quality standards established by regulatory bodies, including the U.S. Environmental Protection Agency (EPA) and equivalent international regulatory organizations.

Municipal sector expansion is supported by government water infrastructure development programs that emphasize establishing modern treatment facilities that meet environmental standards and water quality requirements for sustainable urban development. The growing complexity of municipal wastewater streams and increasing regulatory requirements drive demand for advanced membrane separation technologies from certified providers with appropriate technical expertise and quality assurance systems. This sector's sustained expansion, driven by population growth, urbanization, and regulatory mandates, positions municipal water treatment as the dominant and most stable end-use segment with projected continued market leadership through 2033.

Regional Insights

North America Chemical Separation Membranes Market Trends

North America maintains a strong market position, supported by established regulatory frameworks, mature water-treatment infrastructure, and substantial investments in industrial separation technologies and pharmaceutical manufacturing. The region accounts for approximately 28% of global demand for chemical separation membranes, with the United States as the primary market, driven by stringent environmental regulations and advanced manufacturing capabilities. The U.S. Department of Energy reports that the market for chemical separation membranes in North America is projected to grow at an annual rate of 8.5% over the next five years, reflecting sustained demand in water purification, industrial separation, and energy-sector applications.

The rapid expansion in North America is further fueled by advances in desalination and industrial filtration, with the EPA noting that demand for advanced membrane technologies for desalination and wastewater treatment is increasing at 10% per year. Regulatory support for sustainable industrial practices and environmental protection, combined with mature supply chains and established relationships between membrane manufacturers and end users, positions North America as a significant market for specialized chemical-separation membranes that support industrial sustainability objectives.

Europe Chemical Separation Membranes Market Trends

Europe represents the second-largest regional market for chemical separation membranes, accounting for approximately 26% of global demand, with particularly strong activity in Germany, the United Kingdom, France, and Spain. The region's stringent environmental regulations and sustainability mandates have positioned advanced membrane technologies as critical components of industrial wastewater treatment infrastructure and environmental protection systems. European regulatory harmonization through the European Commission and national environmental agencies establishes demanding quality standards requiring sophisticated membrane separation systems meeting rigorous performance and sustainability specifications.

German specialty chemical manufacturers, including Evonik Industries AG maintain significant production capacity for advanced membrane technologies and separation systems serving pharmaceutical, chemical processing, and environmental protection sectors. European manufacturers have pioneered the development of sustainable membrane formulations using renewable feedstocks and circular-economy principles, thereby establishing competitive advantages in environmentally conscious markets.

Asia Pacific Chemical Separation Membranes Trends

Asia-Pacific is the fastest-growing regional market, with a projected CAGR of approximately 10.5% through 2033, driven by rapid industrialization, accelerating pharmaceutical-sector growth, expanding manufacturing capacity, and substantial government investment in water-treatment infrastructure. China dominates regional production and consumption, with membrane production capacity reaching 380 million square meters in 2023, representing a 42% increase from the previous year. The Chinese National Bureau of Statistics reports that membrane-based separation technologies contributed to 28% reduction in industrial water consumption across major chemical plants in 2023, demonstrating significant environmental benefits and regulatory compliance advantages.

India's pharmaceutical and water treatment sectors are experiencing particularly robust growth, with the polymeric membrane separation market projected to grow at an approximately 15.9% CAGR, driven by rapid urbanization and infrastructure development. Japan maintains advanced biotechnology and research capabilities that support the development of specialized membrane applications for the pharmaceutical and biotechnology sectors. The region's manufacturing cost advantages, expanding production capacity, and rising environmental regulatory standards position Asia-Pacific as the fastest-growing market for chemical separation membranes, with significant opportunities for regional manufacturers and international companies to establish a regional presence.

Competitive Landscape for the Chemical Separation Membranes Market

The chemical separation membranes market exhibits moderate consolidation, with the top five manufacturers accounting for approximately 50-60% of global production capacity and revenue. The market combines established multinational specialty chemical companies, including Evonik Industries AG, 3M Company, Pentair PLC, and DeltaMem AG, with regional manufacturers and specialized producers focusing on niche applications and geographic markets. Leading companies leverage vertically integrated production capabilities, extensive research and development infrastructure, and global distribution networks, enabling customization of membrane formulations for diverse separation applications.

Emerging competitive strategies emphasize partnerships with industrial end users, technology providers, and research institutions to develop application-specific membrane solutions and secure long-term supply agreements. The market remains sufficiently fragmented to enable specialty producers and regional competitors to maintain meaningful positions through technical differentiation, localized manufacturing capacity, and deep customer relationships.

Key Developments:

- In December 2024, Evonik Industries AG announced advancements in HISELECT membrane technology coupled with HIPURE pressure swing adsorption systems, delivering enhanced selectivity and efficiency for carbon dioxide removal, hydrogen purification, and specialized gas separation applications across industrial and energy sectors.

- In September 2024, 3M Company announced expansion of membrane manufacturing capacity for advanced water treatment and industrial separation applications, responding to accelerating global demand for sophisticated filtration solutions supporting pharmaceutical manufacturing and municipal water treatment infrastructure.

- In June 2024, Toray Industries announced a US$ 300 million investment in advanced membrane manufacturing facilities in Singapore, establishing regional production capacity for high-performance separation membranes supporting pharmaceutical, chemical processing, and water treatment applications across the Asia Pacific markets.

Companies Covered in Chemical Separation Membranes Market

- DeltaMem AG

- PBI Performance Products, Inc.

- Evonik Industries AG

- Markel Corporation

- 3M Company

- Overview

- Pentair PLC

- L'Air Liquide S.A.

- MedArray Inc.

- Compact Membrane Systems, Inc.

- Novamem Ltd.

- Pervatech BV

- DIC Corporation

- Toray Industries

- Mitsubishi Chemical Corporation

- Asahi Kasei Corporation

- Koch Membrane Systems

- Pall Corporation

Frequently Asked Questions

The global chemical separation membranes market is projected to reach US$ 8.1 billion by 2033 from US$ 4.2 billion in 2026, representing a compound annual growth rate (CAGR) of 9.8% during the forecast period.

Primary demand drivers include escalating global water scarcity requiring advanced treatment infrastructure, stringent environmental regulations mandating zero liquid discharge implementations, and substantial pharmaceutical and biotechnology sector expansion.

While municipal water treatment and purification applications currently command the largest share at approximately 43%, zero liquid discharge and specialized industrial separation applications represent the fastest-growing segments, with projected expansion rates of 10.2% annually through 2033.

North America maintains the largest regional market with approximately 28% global share, supported by established regulatory frameworks and mature water treatment infrastructure.

Primary opportunities include pharmaceutical and biotechnology industry expansion requiring specialized high-purity separation membranes, sustainable and bio-based membrane technology development aligned with corporate carbon neutrality goals, emerging applications in hydrogen purification and carbon dioxide capture supporting clean energy transitions, expanding municipal water treatment infrastructure.

Key market players include Evonik Industries AG, 3M Company, Pentair PLC, DeltaMem AG, L'Air Liquide S.A., Toray Industries, Mitsubishi Chemical, Asahi Kasei, and Koch Membrane Systems.