- Healthcare Services

- Medical Gas Market

Medical Gas Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Gas Market by Gas Type (Pure Gases, Gas Mixtures), Application (Therapeutic Applications, Diagnostic Applications, Others), End-user (Hospitals, Ambulatory Surgical Centers (ASCs), Home Healthcare, Pharmaceutical & Biotechnology Companies, Others), and Regional Analysis for 2026 - 2033

Medical Gas Market Share and Trends Analysis

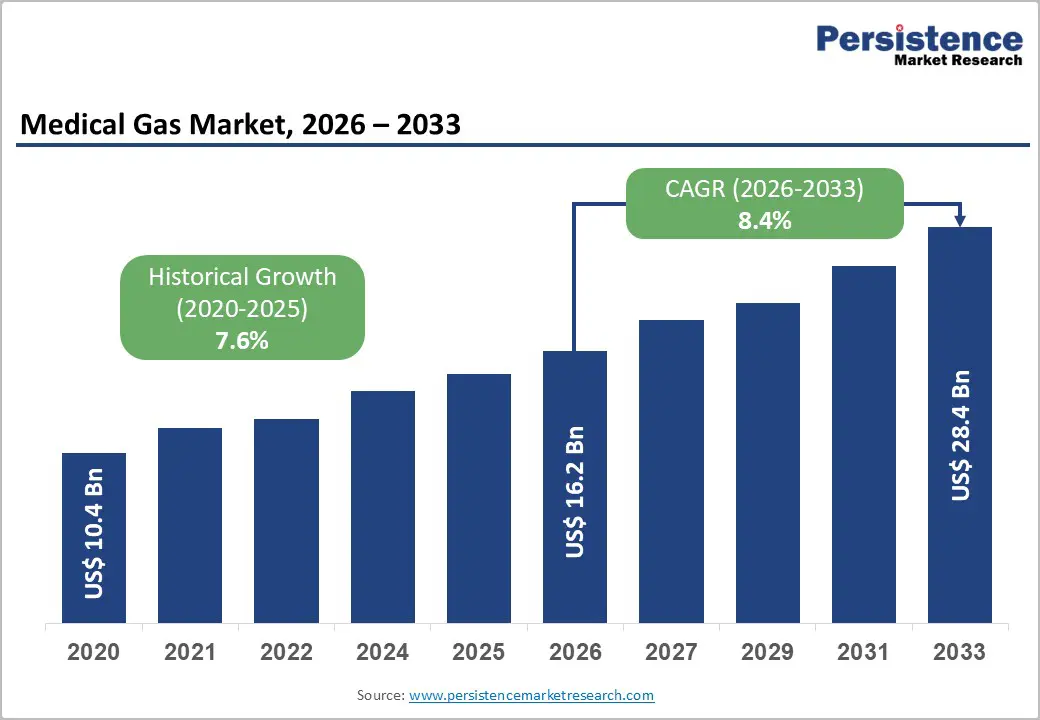

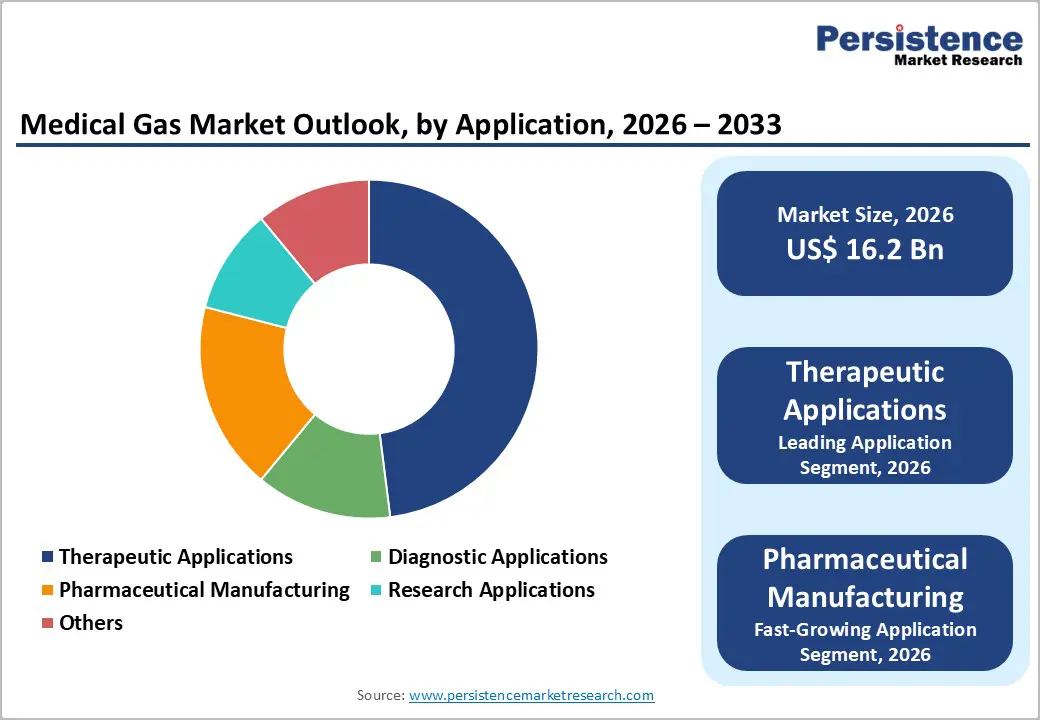

The global medical gas market size is likely to be valued at US$16.2 billion in 2026 and is expected to reach US$28.4 billion by 2033, growing at a CAGR of 8.4% during the forecast period from 2026 to 2033, driven by demographic shifts characterized by an aging population with elevated susceptibilities to chronic respiratory conditions.

Heightened regulatory standards mandate strict compliance with manufacturing protocols, reinforcing product safety and market standardization. Rapid technological integration within medical gas delivery equipment improves operational efficacy, accelerating clinical adoption across multiple healthcare segments. Accelerated healthcare infrastructure expansion in emerging economies further solidifies continuous market growth through increased medical facility development.

Key Industry Highlights:

- Leading Gas Type: Pure gases are set to hold around 62% revenue share in 2026, driven by indispensable oxygen demand across hospital respiratory therapy and surgical anesthesia applications.

- Fastest-growing Gas Type: Gas mixtures are projected as the fastest-growing segment, supported by rising clinical adoption of specialty blends in respiratory diagnostics and procedural sedation.

- Leading Application: Therapeutic applications are estimated to hold roughly 48% revenue share in 2026, due to the clinical criticality of oxygen and anesthetic gas use across emergency, intensive, and chronic care settings.

- Fastest-growing Application: Pharmaceutical manufacturing is forecast to record the fastest growth, driven by accelerating biologic and mRNA vaccine production requiring validated high-purity gas inputs.

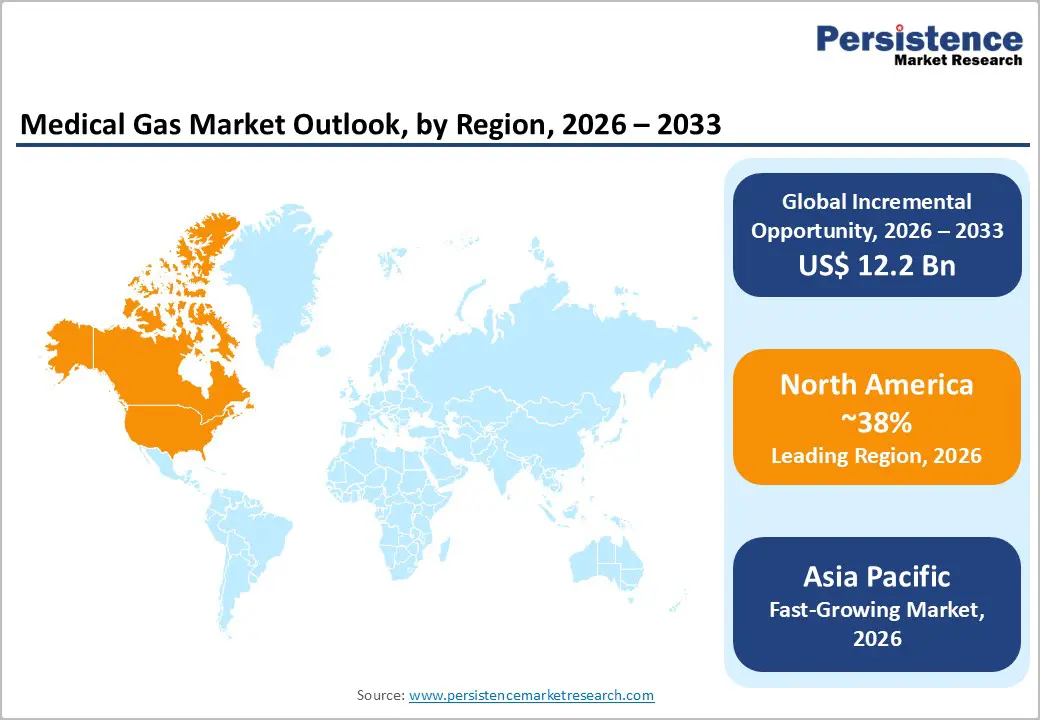

- Regional Leadership: North America is projected to capture roughly 38% of the market share in 2026, driven by advanced hospital infrastructure and established regulatory frameworks governing medical gas procurement.

- Competitive Environment: The market is moderately consolidated, with five multinational suppliers controlling approximately 60% of global revenue, while regional producers compete on local compliance capabilities and cost positioning.

DRO Analysis

Driver - Escalating Global Prevalence of Chronic Respiratory Diseases

The rising incidence of chronic respiratory conditions necessitates continuous administration of long-term oxygen therapies and respiratory interventions. Severe pulmonary illnesses significantly reduce natural lung function, requiring therapeutic gas supplementation to stabilize the patient’s arterial oxygen levels. This continuous clinical need drives demand for therapeutic pure gases across acute and long-term care environments.

According to data published by the Centers for Disease Control and Prevention (CDC) in 2024, approximately 16 million adults in the United States have chronic obstructive pulmonary disease (COPD). This clinical reality creates a substantial reliance on medical oxygen infrastructure. Increased diagnostic rates for respiratory disorders ensure an expanding patient base requiring permanent medical gas solutions.

Restraint - Complexity and Cost of Cryogenic Storage and Distribution Infrastructure

The transportation and storage of liquefied medical gases, particularly liquid oxygen and liquid nitrogen, requires specialized cryogenic equipment that carries high capital and maintenance costs. Facilities in remote or low-income geographies face acute infrastructure challenges, as the investment required to establish and maintain compliant cryogenic supply chains frequently exceeds available healthcare capital budgets.

Distribution network gaps directly limit market penetration in high-potential but underdeveloped regions. Even where clinical demand exists, the absence of reliable cold-chain infrastructure prevents consistent product availability, reducing effective market size below theoretical potential. The resulting supply inconsistency also creates patient safety risks that trigger regulatory scrutiny, further increasing the operational burden on distributors attempting to serve these markets.

Opportunity - Home Healthcare Oxygen Therapy as a High-Growth Addressable Segment

The global shift from inpatient to outpatient and home-based care models represents a structural opportunity for medical gas suppliers capable of adapting their delivery infrastructure to decentralized settings. Portable oxygen concentrators and lightweight cylinder systems are enabling patients with chronic respiratory conditions to receive continuous therapy at home, reducing hospital readmission rates and associated healthcare system costs. This transition is being accelerated by policy frameworks in the United States, European Union, and several Asia Pacific nations that explicitly prioritize home-based care as a cost-containment strategy.

Suppliers that invest in connected oxygen delivery devices equipped with remote monitoring capabilities are positioned to capture premium pricing and long-term service contract revenues. The integration of IoT-enabled flow monitoring with electronic health record systems allows care teams to optimize therapy dosing in real time, improving clinical outcomes and creating measurable value that supports reimbursement justification. As more national payers formalize reimbursement pathways for home oxygen therapy, the addressable market in this segment will expand materially.

Category-wise Analysis

Gas Type Insights

Pure gases are expected to lead the medical gas market, accounting for approximately 62% of revenue in 2026. Pure medical oxygen dominates procurement across hospital systems due to its indispensable role in respiratory therapy and surgical support. Linde plc, for example, supplies bulk liquid oxygen under long-term contracts to major hospital networks across North America and Europe. The direct link between patient census levels and oxygen consumption volumes makes this segment highly predictable in demand, supporting capacity planning and pricing stability for suppliers.

Gas mixtures are likely to represent the fastest-growing segment, propelled by rising demand for calibration gases, heliox therapy in airway management, and nitrous oxide-oxygen blends in procedural sedation. Specialty gas mixture applications in pulmonary function diagnostics are expanding as respiratory disease screening programs gain institutional support. Messer Group has introduced precision-blended respiratory diagnostic gas kits that reduce preparation time in clinical laboratories.

Application Insights

Therapeutic applications are projected to lead the market, capturing around 48% of the revenue share in 2026. The segment encompasses oxygen therapy, nitrous oxide analgesia, and helium-oxygen blends used across emergency, intensive care, and chronic disease management settings. Air Products and Chemicals has expanded its therapeutic gas portfolio to include integrated delivery systems for neonatal intensive care units.

Pharmaceutical manufacturing is likely to be the fastest-growing segment, fueled by accelerating biologic drug production and the proliferation of contract manufacturing organizations requiring validated high-purity gas inputs. Nippon Sanso Holdings has commissioned dedicated pharmaceutical gas production lines in response to rising orders from bio-manufacturing clients in Japan and Southeast Asia.

End-user Insights

Hospitals are likely to be the leading segment with a projected 45% of the medical gas market share in 2026 due to the concentration of high-acuity patients requiring continuous gas-supported interventions across surgical, critical care, and general ward settings. Large integrated health systems, such as Hospital Corporation of America (HCA) Healthcare in the U.S., operate centralized pipeline distribution systems that require continuous bulk gas supply agreements.

Home healthcare is anticipated to be the fastest-growing segment, fueled by national policies promoting outpatient care, the aging demographic requiring long-term oxygen therapy, and advances in portable oxygen delivery technology that make home treatment clinically equivalent to facility-based care. ResMed has deployed connected home oxygen concentrators that transmit usage and compliance data to clinical teams, enabling proactive intervention when therapy adherence declines.

Regional Insights

North America Medical Gas Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by advanced hospital infrastructure, high surgical procedure volumes, and a well-established regulatory framework administered by the U.S. Food and Drug Administration and Health Canada that enforces stringent pharmaceutical-grade gas standards.

U.S. Medical Gas Market Insights

The U.S. is projected to remain the largest market, supported by the highest per-capita surgical procedure rate among Organisation for Economic Co-operation and Development (OECD) nations and a robust home healthcare sector. Regulatory enforcement actions by the FDA in 2025 targeting non-compliant medical oxygen suppliers accelerated market consolidation, favoring large certified producers.

Canada Medical Gas Market Insights

Canada is expected to witness steady market progress due to public funding expansions directed at institutional infrastructure modernization. Regional healthcare centers are forecast to upgrade aging pipeline networks to improve gas delivery safety across perioperative departments. This transformation increases long-term contract values for regional gas production entities.

Europe Medical Gas Market Trends

Europe represents the second-largest regional market, characterized by universal healthcare systems that generate consistent institutional demand and rigorous European Medicines Agency pharmaceutical-grade standards that govern gas production and distribution. Germany, France, and the U.K collectively account for the majority of regional procurement.

Germany Medical Gas Market Insights

Germany is projected to lead European demand, reflecting a high density of acute care hospitals, a robust pharmaceutical manufacturing sector requiring industrial-grade specialty gases, and statutory health insurance coverage for home oxygen therapy. Linde plc, headquartered in Munich, maintains significant domestic production and distribution capacity that enables a rapid response to procurement requirements.

U.K. Medical Gas Market Insights

The U.K. is likely to experience demand growth supported by the National Health Service (NHS) Long Term Workforce Plan, which is expanding clinical capacity and, by extension, therapeutic gas consumption across NHS trust facilities. BOC, a Linde subsidiary, holds the dominant supply position within the NHS framework agreement.

Asia Pacific Medical Gas Market Trends

Asia Pacific is forecast to be the fastest-growing market for medical gas, stimulated by rapid hospital construction programs in China and India, and rising surgical procedure volumes driven by a growing middle-class patient population. China National Health Commission targets for hospital bed expansion and India National Health Mission investments in district hospital upgrades are creating large-scale institutional demand for centralized gas pipeline systems.

China Medical Gas Market Insights

China is projected to register the highest absolute volume growth in the regional market, underpinned by the national hospital accreditation system that now mandates centralized medical gas pipeline installation as a condition of tertiary hospital classification. Yingde Gases and Baosteel Gases have expanded their medical segment portfolios in response to domestic procurement mandates.

India Medical Gas Market Insights

India is expected to record strong growth, driven by Ayushman Bharat health scheme expansions that are increasing insured patient volumes in public hospitals and thereby intensifying oxygen and anesthetic gas consumption. INOX Air Products and Linde India have announced capacity expansions in 2025 to address supply shortfalls that became visible during peak demand periods.

Competitive Landscape

The global medical gas market is moderately consolidated, with a small number of multinational suppliers controlling the majority of production capacity and distribution infrastructure, while a larger base of regional and national producers competes across specific geographies and product categories. The leading participants, including Linde plc, Air Liquide, Air Products and Chemicals, Messer Group, and Nippon Sanso Holdings, collectively account for an estimated 60% of global revenue.

Competitive differentiation among market leaders increasingly rests on digital service capabilities, sustainability credentials, and the depth of regulatory expertise offered to customer procurement teams. Smaller regional players compete on local responsiveness and pricing flexibility but face structural disadvantages in meeting the quality documentation and continuous supply assurance requirements of large institutional buyers.

Key Industry Developments:

- In January 2026, Ghani Chemical Industries Limited partnered with Precision Parts UK Ltd under the CPX brand to expand medical gas pipeline systems and related healthcare infrastructure solutions across Pakistan hospitals.

- In August 2025, Coregas launched the IVRX-1 Touch medical oxygen solution featuring single-action operation, reinforcing safer cylinder handling and streamlined oxygen delivery across healthcare facilities.

- In July 2025, GCE Medical launched the DUPLEX PNP200 gas manifold with fully automatic three-source medical gas management, reinforcing uninterrupted hospital gas supply and advanced pipeline monitoring capabilities.

Companies Covered in Medical Gas Market

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals, Inc.

- Messer Group GmbH

- Nippon Sanso Holdings Corporation

- BOC (a Linde subsidiary)

- Taiyo Nippon Sanso Corporation

- INOX Air Products Pvt. Ltd.

- Yingde Gases Group Company Limited

- Ellenbarrie Industrial Gases Ltd.

- Gulf Cryo

- National Medical Care Company (NMC)

- SOL Group

- Luxfer Holdings PLC

- Matheson Tri-Gas, Inc.

Frequently Asked Questions

The global medical gas market is projected to reach US$16.2 billion in 2026.

Rising prevalence of respiratory diseases, expanding hospital infrastructure, and increasing demand for oxygen therapy and critical care support are driving the medical gas market.

The medical gas market is poised to witness a CAGR of 8.4% from 2026 to 2033.

Expansion of home healthcare oxygen therapy, growth in pharmaceutical manufacturing demand for high-purity gases, and increasing investment in hospital infrastructure modernization are creating key opportunities in the medical gas market.

Some of the key market players include Linde plc, Air Liquide, Air Products and Chemicals, Messer Group, and Nippon Sanso Holdings.