- Specialty & Fine Chemicals

- Membrane Separation Market

Membrane Separation Market Size, Share, and Growth Forecast 2025 - 2032

Membrane Separation Market by Material (Polymeric, Inorganic), Process (Reverse Osmosis, Ultrafiltration, Nano-filtration, Micro-filtration), Application (Gas Separation, Liquid Separation, Solid Separation), End-user, and Regional Analysis for 2025 - 2032

Membrane Separation Market Size and Trend Analysis

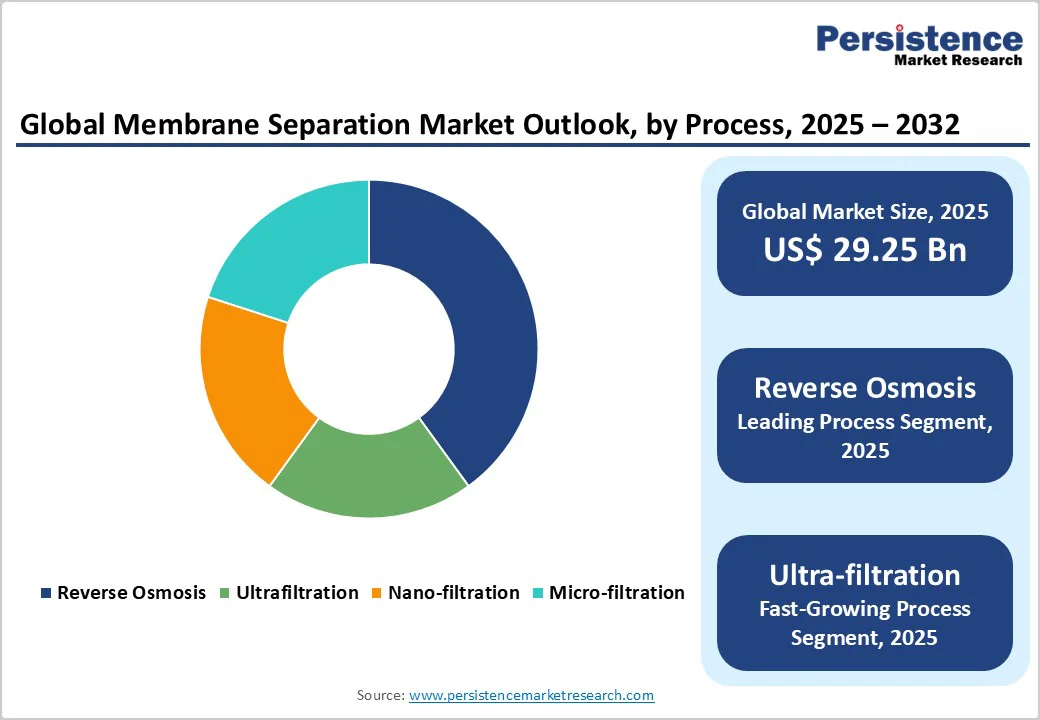

The global membrane separation market size is likely to value at US$ 29.3 billion in 2025 and is projected to reach US$ 53.1 billion by 2032, growing at a CAGR of 8.9% between 2025 and 2032.

This robust expansion is primarily driven by escalating global water scarcity challenges and stringent environmental regulations mandating advanced treatment solutions across industrial and municipal sectors. According to the United Nations, approximately 2 billion people lack access to safely managed drinking water services, creating unprecedented demand for efficient separation technologies.

Key Market Highlights:

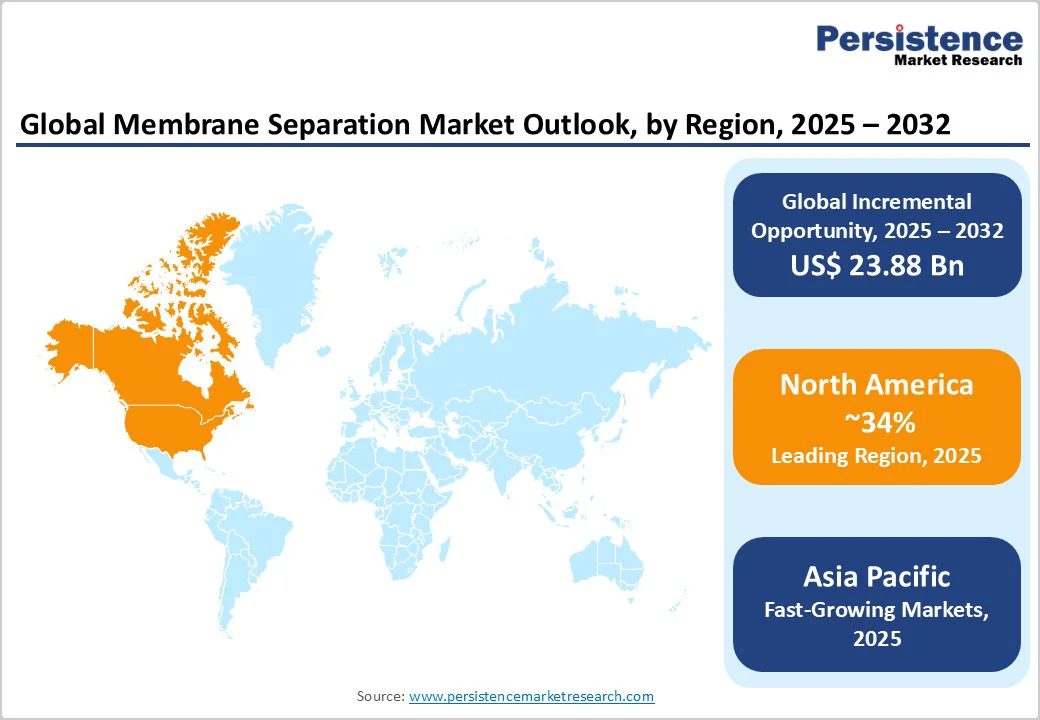

- Regional Leader: North America leads the Membrane Separation Market, with 34% of the market share, due to stringent EPA regulations and innovation hubs, ensuring high adoption in desalination and wastewater treatment for sustainable water security.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, propelled by urbanization in China and India, with manufacturing advantages accelerating membrane deployment in industrial processing.

- Leading Segment: Polymeric materials dominate as the leading segment with 60% of the market, offering cost-effective versatility for liquid separation in water treatment, supported by global scalability trends.

- Fastest Growing Segment: Reverse Osmosis stands out as the fastest-growing process segment, driven by desalination demands and efficiency improvements, capturing rising shares in emerging economies.

- Growth Opportunities: Advancements in nanomaterial membranes present a key opportunity, enabling antifouling solutions for wastewater recycling and aligning with sustainability policies worldwide.

| Key Insights | Details |

|---|---|

| Membrane Separation Market Size (2025E) | US$ 29.3 Bn |

| Market Value Forecast (2032F) | US$ 53.1 Bn |

| Projected Growth CAGR (2025 - 2032) | 8.9% |

| Historical Market Growth (2019 - 2024) | 7.3% |

Market Dynamics

Driver - Rising Demand for Clean Water Solutions

The increasing global population and urbanization have intensified water scarcity, driving the adoption of membrane separation technologies for efficient purification and reuse. By 2050, approximately 2 billion people across 44 countries will likely experience water scarcity conditions, with per capita availability dropping below 1,000 m³/year. This critical shortage is compelling governments and industries to invest heavily in desalination and water recycling infrastructure.

The Shuaibah 3 Independent Water Project in Saudi Arabia, operational in 2025, demonstrates this trend with a daily production capacity of 600,000 cubic meters of potable water using advanced reverse osmosis membranes supplied by Toray Industries. The facility integrates a 65-megawatt solar power system, reducing CO2 emissions by approximately 45 million tons annually.

In China, water consumption reached 592,020 million cubic meters in 2021, with government regulations under the Water Pollution Prevention and Control Law (Amended 2017) prioritizing drinking water source protection. Industrial water recycling projects across the Asia Pacific initiated in 2024 are anticipated to yield a collective capacity exceeding 1 million cubic meters per day, directly benefiting the membrane separation market.

Stringent Environmental Regulations

Governments worldwide are enforcing stricter wastewater discharge standards to protect ecosystems, boosting the integration of membrane separation in compliance efforts. The European Union Water Framework Directive establishes comprehensive standards for water quality and wastewater discharge, compelling industries across Germany, France, the U.K., and the Netherlands to implement sophisticated membrane filtration systems.

In Germany, which accounts for 28% of the European membrane bioreactor market, cities including Berlin and Munich have adopted MBR systems to address urban water scarcity while complying with EU directives.

The U.S. EPA's 2024 regulations for PFAS in drinking water represent a watershed moment, requiring water utilities to implement advanced treatment capable of removing contaminants to parts-per-trillion levels. Industrial sectors face parallel pressures, with the pharmaceutical industry requiring PES and PVDF membranes that achieve protein adsorption below 1% and flow rates of 211 mL/min for monoclonal antibody purification.

Market Restraints

High Initial and Maintenance Costs

Membrane separation systems require substantial upfront investment for installation and periodic replacements, posing barriers for small-scale operations in developing regions. Authentic data from industry journals indicate that membrane fouling leads to maintenance expenses accounting for 20-30% of total operational costs, necessitating frequent cleaning and downtime that hampers efficiency.

Energy consumption, particularly for seawater reverse osmosis systems, remains considerable despite technological improvements. Maintenance requirements, including chemical cleaning, fouling mitigation, and system monitoring, necessitate skilled personnel and specialized expertise, adding to the total cost of ownership.

This financial strain is exacerbated in harsh environments, where chemical degradation shortens membrane life to under 5 years, discouraging adoption despite performance benefits and limiting market expansion in cost-sensitive sectors.

Technical Challenges with Fouling and Scalability

Fouling from contaminants such as organics and inorganics reduces flux rates by up to 50%, complicating scalability for large-volume applications such as municipal treatment. Research from ScienceDirect highlights that biofouling in reverse osmosis systems demands energy-intensive pretreatment, increasing overall costs and environmental footprint.

Organic fouling, inorganic scaling, biofouling, and colloidal fouling can significantly reduce membrane permeability and separation efficiency over time. Despite advances in antifouling membrane materials and surface modifications, fouling remains inevitable in real-world applications, particularly when treating complex industrial effluents or contaminated water sources.

Market Opportunities

Advancements in Nanomaterial-Enhanced Membranes

Innovations in nanomaterials, such as graphene oxide and metal-organic frameworks, offer opportunities for developing high-flux, antifouling membranes that enhance selectivity and durability. Journals report that these materials improve rejection rates by 95% for contaminants, enabling applications in emerging sectors like biogas separation and advanced wastewater recycling.

With global investments in R&D reaching USD 1 Bn annually from organizations such as the International Energy Agency, companies can target fast-growing segments in pharmaceuticals and energy, where energy-efficient processes could generate significant demand through 2032. This potential is evident in pilot projects that have achieved 40% cost reductions, positioning participants for substantial revenue growth.

Expansion in Emerging Wastewater Treatment Markets

Rapid urbanization in the Asia Pacific presents opportunities for membrane technologies in decentralized treatment systems, driven by policies such as India's Namami Gange program, aiming to treat 100% of urban wastewater by 2030.

The Water Filter Market is expanding rapidly across urban and rural areas as awareness of waterborne diseases increases. Government investments in municipal water infrastructure, combined with private sector participation in industrial wastewater treatment, are creating robust demand for reverse osmosis, ultrafiltration, nanofiltration, and microfiltration systems across diverse applications.

China, with over 300 contract research organizations and numerous pharmaceutical manufacturers, represents a substantial market for membrane separation systems. According to the Water Pollution Prevention and Control Law principles, Chinese authorities prioritize prevention, control, and protection of drinking water sources, stimulating demand across pharmaceutical, food and beverage, and commercial applications.

Category-wise Insights

Material Analysis

The polymeric segment leads the material category with an approximate 60% market share, attributed to its cost-effectiveness and versatility in applications like water purification. Natural and synthetic polymers, such as polyethersulfone, offer superior chemical resistance and tunable pore sizes, enabling efficient separation in diverse environments, as per journal studies on membrane performance.

The Polytetrafluoroethylene (PTFE) Filter Membranes Market represents a specialized segment offering exceptional chemical resistance and high-temperature capabilities for demanding industrial applications. Natural polymers, including cellulose derivatives, serve niche laboratory and cost-sensitive applications.

Inorganic membranes, particularly ceramic materials comprising alumina (Al2O3), titania (TiO2), and zirconia, are gaining traction for their superior chemical and thermal stability, mechanical robustness, and extended service life exceeding 10 years in harsh industrial environments, including oil and gas, mining effluent treatment, and high-solids applications.

Process Analysis

Reverse Osmosis dominates the process category with around 40% share, driven by its proven efficacy in desalination and contaminant removal. Supported by EPA guidance manuals, this process excels in rejecting 99% of dissolved salts, making it indispensable for potable water production amid global scarcity. Toray Industries launched the TLF-400ULD reverse osmosis membrane in October 2025, featuring industry-leading specifications that double chemical resistance while using 10% less energy.

The reverse osmosis pump market supports this segment by providing essential pressure management for optimal membrane performance. Ultrafiltration represents the fastest-growing process segment, expanding rapidly due to its effectiveness in removing suspended solids, bacteria, viruses, and macromolecules while allowing dissolved salts to pass through. UF systems are increasingly deployed as pretreatment for RO systems and in membrane bioreactor (MBR) configurations for wastewater treatment.

Application Analysis

Liquid Separation holds the leading position in applications with roughly 50% market share, fueled by its critical role in fluid purification and recycling. Research journals emphasize its efficiency in removing organics and inorganics from wastewater, aligning with industrial needs for sustainable processing.

Water treatment facilities utilize membrane systems to remove contaminants ranging from suspended solids and microorganisms to dissolved salts and emerging pollutants. The pharmaceutical and biotechnology sectors employ membrane filtration for sterile filtration, virus removal, protein concentration, and buffer exchange operations.

Gas separation represents a growing application segment driven by industrial needs for hydrogen recovery, nitrogen generation, CO2 capture, and natural gas processing. The gas separation membranes market is experiencing robust expansion as industries pursue carbon capture and clean energy initiatives.

End-user Analysis

The Water and Wastewater Treatment end-user segment commands about 45% share, propelled by escalating demand for clean water resources. Authentic statistics from global organizations highlight its use in municipal systems to treat billions of liters daily, reducing pollution effectively.

Municipal water utilities deploy membrane systems to ensure compliance with stringent drinking water standards, including the EPA's 2024 PFAS regulations establishing maximum contaminant levels for six compounds. Industrial wastewater treatment facilities utilize membrane technologies to achieve zero liquid discharge (ZLD) targets and meet discharge permit requirements. SUEZ commissioned China's largest industrial membrane-based seawater desalination plant in July 2025, supporting long-term water security for industrial zones.

Regional Insights

North America Membrane Separation Trends

North America leads in membrane separation adoption, with the U.S. dominating due to robust regulatory frameworks from the EPA enforcing clean water standards. Innovations in antifouling technologies, supported by R&D investments exceeding USD 500 Mn annually, drive efficiency in desalination plants along coastal regions. This ecosystem fosters collaborations between academia and industry, accelerating deployment in oil and gas wastewater treatment.

The region's focus on sustainability is evident in federal initiatives like the Infrastructure Investment and Jobs Act, which allocates funds for advanced filtration, enhancing market dynamics through policy-backed expansions.

Europe Membrane Separation Trends

Europe exhibits strong performance, with Germany and the U.K. leading through harmonized regulations under the EU Water Framework Directive, promoting membrane use in industrial effluent control. According to the Netherlands Organisation for Applied Scientific Research, Germany accounts for over 30% of industrial MBR installations across Europe, reflecting its strong industrial base in pharmaceuticals, chemicals, and food processing.

Developments in ceramic-enhanced polymers have improved durability, as seen in France's wastewater projects, which achieve 90% recovery rates. Spain's emphasis on reuse aligns with circular economy goals, bolstering regional trends.

The EU Water Framework Directive, effective since December 2000, establishes coordinated waterbody management transcending national boundaries, mandating achievement of good water quality status. This regulatory framework compels industries to adopt advanced membrane technologies for both water supply treatment and wastewater discharge compliance, benefiting from the region's technological sophistication and environmental consciousness.

Asia Pacific Membrane Separation Trends

Asia Pacific demonstrates robust growth, led by China and India's manufacturing advantages and infrastructure booms. China, holding substantial market share in 2022, possesses well-established healthcare systems and hosts numerous pharmaceutical, biotechnology, and contract research organizations, including Pharmaron, Shanghai Medicilon, and JOINN Laboratories.

With approximately 300 contract research organizations and extensive medical device manufacturing capacity, China represents a massive end-user base for membrane separation systems. Water consumption reached 592,020 million cubic meters in 2021, with government regulations under the Water Pollution Prevention and Control Law (Amended 2017) prioritizing drinking water source protection and wastewater treatment.

ASEAN countries benefit from cost-effective polymeric membranes in textile wastewater treatment, with investments rising 12% yearly according to government reports. Japan's precision engineering supports high-end applications such as the gas separation membranes market in electronics.

Competitive Landscape

The global membrane separation market remains fragmented, with numerous global and regional players competing through specialized offerings rather than consolidation.

Companies pursue expansion via R&D investments in antifouling technologies and partnerships for sustainable innovations, as seen in collaborations for hybrid systems. Key differentiators include material durability and energy efficiency, while emerging models focus on modular, scalable units for decentralized applications.

Key Market Developments:

- March 2024: Dow Chemical Corporation launched advanced reverse osmosis membranes with enhanced antifouling properties for industrial wastewater.

- July 2025: Toray Industries introduced polymeric nanofiltration modules integrated with AI optimization for energy savings in desalination plants.

- January 2025: Pall Corporation partnered with Veolia Environnement to deploy ultrafiltration systems in municipal projects, targeting 20% efficiency gains.

Top Companies in the Membrane Separation Market

- Dow Chemical Corporation (U.S.) leads with a strong portfolio in reverse osmosis and polymeric membranes, generating significant revenue from water treatment solutions and influencing market standards through R&D maturity. Its global reach and innovation in sustainable materials solidify its 15% share dominance.

- Toray Industries (Japan) excels in advanced filtration technologies, with expertise in nanofiltration for industrial processing, boasting a high portfolio strength and partnerships driving 10% market influence. Headquarters in Tokyo supports Asian expansion.

- Pall Corporation (U.S.), part of Danaher, dominates healthcare applications with microfiltration expertise, leveraging order backlog and technological maturity for reliable separations, holding key positions in biopharma.

Companies Covered in Membrane Separation Market

- Dow Chemical Corporation

- Toray Industries

- Pall Corporation

- Applied Membranes, Inc.

- Evoqua Water Technologies

- GEA Filtration

- Koch Membrane Systems

- 3M Company

- Veolia Environnement

- Pentair plc

- Parker-Hannifin Corporation

- Microdyn Nadir

- UBE Corporation

- DuPont de Nemours, Inc.

- Merck KGaA

Frequently Asked Questions

The Membrane Separation Market is valued at US$ 29.3 Bn in 2025 and expected to reach US$ 53.1 Bn by 2032, growing at 8.9% CAGR due to rising water treatment demands.

Key drivers include global water scarcity and stringent regulations, with UN data showing 2 billion people lacking access to safe water, spurring adoption of efficient separation technologies.

Reverse Osmosis leads with 40% share, justified by its 99% salt rejection efficiency in desalination, as per EPA guidelines.

North America leads, driven by U.S. regulatory frameworks and innovation, with EPA standards boosting wastewater treatment applications.

Nanomaterial enhancements offer antifouling membranes, potentially reducing costs by 40% in wastewater recycling, aligning with sustainability trends.

Leading players include Dow Chemical Corporation, Toray Industries, and Pall Corporation, dominating through R&D and global portfolios in filtration technologies.