- Food Ingredients & Additives

- Food Grade Gases Market

Food Grade Gases Market Size, Share, and Growth Forecast 2026 - 2033

Food Grade Gases Market by Gas Type (Carbon Dioxide (CO₂), Nitrogen (N₂), Oxygen (O₂), Others), Application (Packaging & Preservation, Carbonation, Freezing & Chilling, Modified Atmosphere Packaging, Others), Mode of Supply (On-site Gas Generation, Cylinder Supply, Cryogenic Tanks & Liquid Dewars), End-Use Industry (Beverages, Meat, Poultry & Seafood, Dairy, Bakery & Confectionery, Fruits & Vegetables, Others), by Regional Analysis, 2026 - 2033

Food Grade Gases Market Size and Trend Analysis

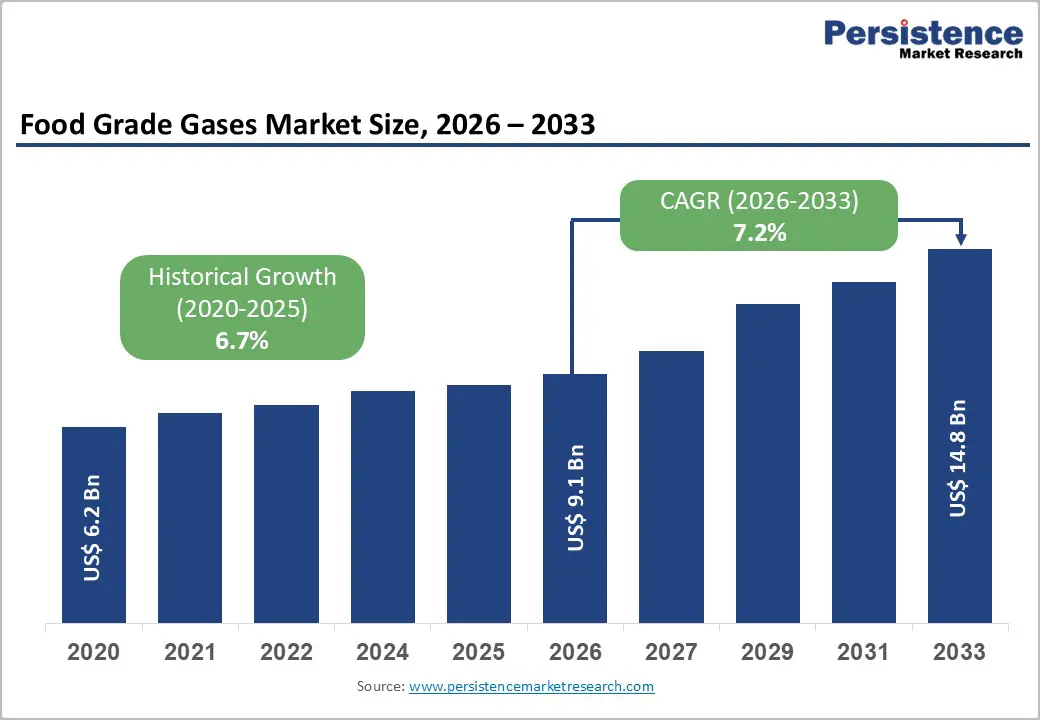

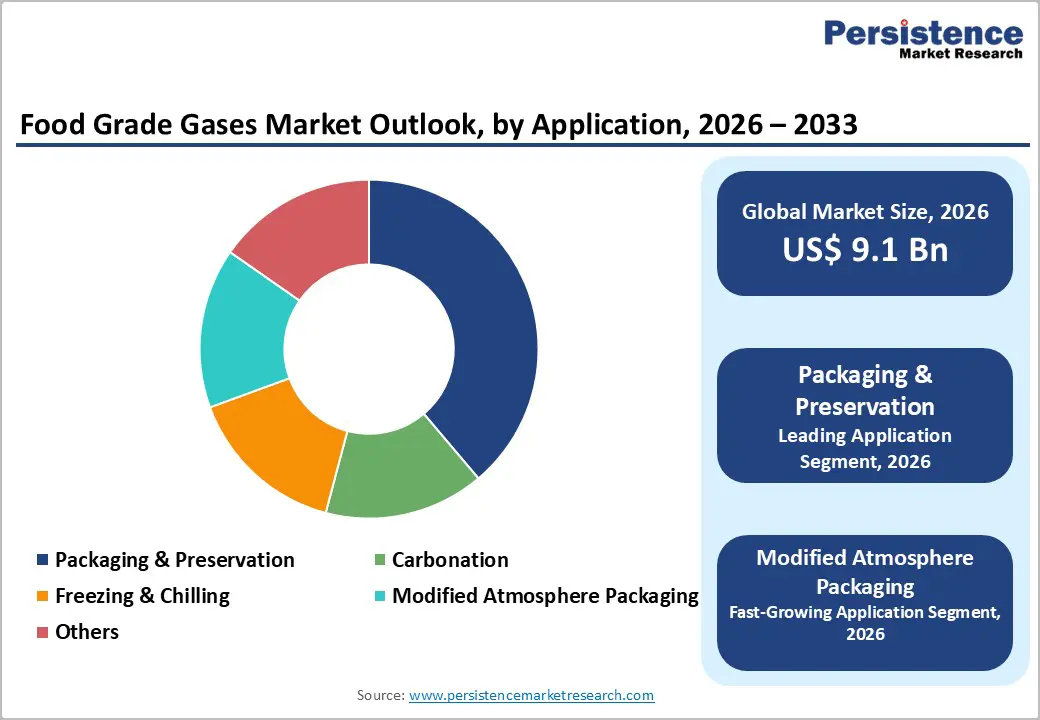

The global food grade gases market size is expected to be valued at US$ 9.1 billion in 2026 and projected to reach US$ 14.8 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

The market's sustained expansion is underpinned by accelerating global demand for packaged and convenience foods, rising consumption of carbonated beverages, and the widening adoption of Modified Atmosphere Packaging (MAP) technologies across the food processing value chain. Heightened consumer awareness around food safety, combined with stringent regulatory mandates from bodies such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), is compelling manufacturers to embrace high-purity food grade gases, including carbon dioxide (CO?), nitrogen (N?), and oxygen (O?), as indispensable tools for extending shelf life, preserving sensory quality, and ensuring microbiological safety across dairy, meat, beverage, and bakery segments.

Growing consumption of packaging foods across the world is fueling the global food grade gases market

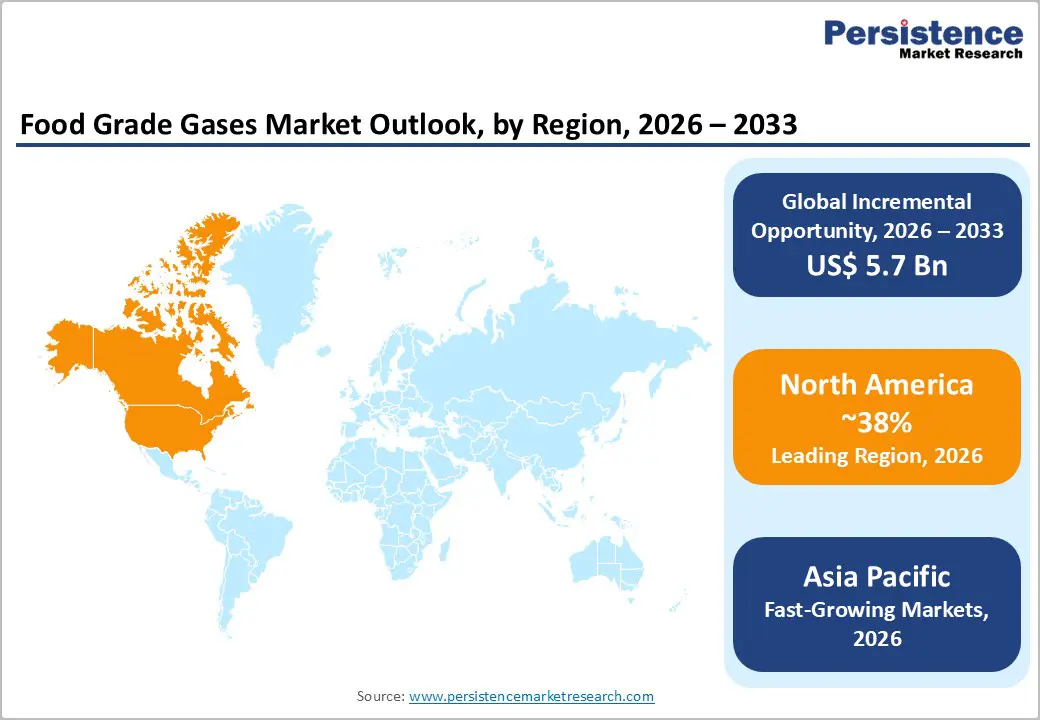

- Leading Region: North America leads the global food grade gases market with approximately 38% share in 2025, anchored by the U.S. food processing sector's large-scale use of CO? and nitrogen for MAP, cryogenic freezing, and beverage carbonation applications.

- Fastest Growing Region: Asia Pacific is the fastest growing region at approximately 8.5% CAGR through 2033, driven by rapid urbanization, expanding packaged food industries, and increasing adoption of MAP technologies across China, India, Japan, and ASEAN nations.

- Dominant Segment: Carbon dioxide (CO?) is the dominant gas type segment, holding approximately 45% market share in 2025, owing to its critical and irreplaceable role in carbonated beverage production and modified atmosphere packaging across multiple food categories.

- Fastest Growing Segment: Modified Atmosphere Packaging (MAP) is the fastest growing application segment through 2033, fueled by surging demand from meat, dairy, and bakery processors seeking chemical-free, regulatory-compliant shelf life extension solutions globally.

- Key Opportunity: Bio-derived CO? and on-site gas generation represent the most significant market opportunity, enabling food processors to achieve supply security, cost efficiency, and sustainability targets amid growing regulatory pressure and consumer demand for green food supply chains.

| Key Insights | Details |

|---|---|

|

Food Grade Gases Market Size (2026E) |

US$ 9.1 Billion |

|

Market Value Forecast (2033F) |

US$ 14.8 Billion |

|

Projected Growth CAGR (2026–2033) |

7.2% |

|

Historical Market Growth (2020–2025) |

6.7% CAGR |

Market Dynamics

Market Growth Drivers

Rising Demand for Packaged and Convenience Foods

The global surge in consumer preference for packaged, ready-to-eat, and convenience foods is one of the most powerful structural drivers of the food grade gases market. According to the Food and Agriculture Organization (FAO), urban populations across Asia, Latin America, and the Middle East are increasingly adopting Western dietary habits characterized by a preference for processed and pre-packaged food products. Food grade gases, particularly nitrogen (N?) and carbon dioxide (CO?), are central to MAP technologies that displace oxygen inside packaging, thereby inhibiting microbial growth, delaying oxidative spoilage, and extending product shelf life without the use of chemical preservatives. U.S. packaged food manufacturers alone used nearly 950,000 tonnes of food grade nitrogen and CO? for freezing, chilling, and MAP in 2024, underscoring the critical role of these gases in modern food supply chains.

Growth of the Carbonated Beverage Industry

The global carbonated beverage industry, encompassing soft drinks, sparkling water, craft beer, and ready-to-drink cocktails, remains a prolific consumer of food grade carbon dioxide (CO?), directly propelling market expansion. CO? is irreplaceable in imparting carbonation, enhancing taste profiles, and inhibiting bacterial growth in bottled and canned beverages. The beverages segment accounts for approximately 40% of total food grade CO? consumption globally. The rapid proliferation of craft breweries and premium beverage brands across North America, Europe, and Asia Pacific, along with the exponential growth of online food delivery services, projected to reach US$ 200 billion in 2025 per the Power to Persuade Organization, is sustaining robust, long-term demand for high-purity CO? across this segment.

Market Restraints

Stringent Purity Standards and High Certification Costs

One of the most significant restraints facing the food grade gases industry is the rigorous purity certification regime mandated by global regulatory frameworks. Standards such as FDA CFR Title 21 in the United States and EU Regulation EC 1333/2008 in Europe impose strict limits on contaminants, requiring gas producers to invest heavily in advanced filtration, purification, and quality assurance systems. Compliance with these evolving standards increases both capital expenditure and operating costs for gas manufacturers, creating barriers particularly for small and mid-sized regional players. These certification requirements also extend lead times for product approvals, limiting market responsiveness and potentially constraining the entry of new suppliers into high-growth geographies.

Supply Chain Complexity and CO? Availability Disruptions

The food grade gases market, particularly the CO? segment, has faced acute supply chain vulnerabilities in recent years. The decline of the UK bioethanol market, a major by-product source of industrial CO?, has contributed to supply shortages, prompting industry participants to seek alternative production pathways. Additionally, the specialized infrastructure required for cryogenic gas storage and transport, including cryogenic tankers, liquid dewars, and on-site generation equipment, adds to logistical complexity and cost, especially in emerging markets with underdeveloped cold-chain infrastructure. Such supply-side constraints can trigger price volatility, disrupt production schedules for food manufacturers, and erode buyer confidence in the reliability of gas supply.

Market Opportunities

Bio-Derived and Sustainable CO? Production

The accelerating global transition toward sustainable industrial practices is opening transformative opportunities for food grade gas manufacturers willing to invest in bio-derived and circular economy CO? production models. In September 2025, Bio Capital, a UK-based renewable energy producer, announced the production of food grade CO? from its anaerobic digestion facilities at Granville Eco Park and Corbiere Renewables, with a combined capacity to supply approximately 15,000 tonnes of CO? per year. Similarly, in September 2024, a consortium including Bluebox Energy Ltd, Woodtek Engineering Ltd, and Ricardo Plc installed a carbon-negative technology demonstrator that converts sustainable wood waste into clean energy, food grade CO?, and biochar. The global Carbon Capture, Utilization, and Storage Market is forecast to expand from US$ 3.5 billion in 2025 to US$ 22.0 billion by 2033, presenting significant co-development opportunities for food grade gas companies.

Expansion of On-Site Gas Generation in Asia Pacific

The rapid industrialization of food processing sectors across China, India, and ASEAN nations is generating strong demand for on-site gas generation systems, which offer food manufacturers greater supply security, cost efficiency, and operational independence compared to traditional cylinder or bulk delivery methods. Currently, approximately 17% of food processors in Asia Pacific utilize on-site nitrogen generation systems, a figure expected to rise significantly as domestic cold-chain and packaged food infrastructure matures. Governments across the region are actively investing in food safety regulations and processing standards that align with global benchmarks, further validating the adoption of MAP and cryogenic technologies. For market participants, establishing regional on-site gas generation capabilities represents a compelling strategy to capture the high-growth Asia Pacific opportunity while building long-term client relationships.

Category-wise Insights

Gas Type Analysis

Carbon dioxide (CO?) is the dominant segment by gas type in the global food grade gases market, commanding approximately 45% market share in 2025. CO?'s supremacy is rooted in its dual utility as both a carbonation agent and a preservation gas, making it indispensable across the beverage, dairy, and meat processing industries. CO? accounted for 44.8% of total gas type share in 2024, a position it has maintained due to growing demand from packaged and convenience food manufacturers adopting MAP and cryogenic freezing. The beverage segment alone, including soft drinks, sparkling water, and beer, drives nearly 40% of global food grade CO? consumption. Meanwhile, oxygen (O?) is emerging as the fastest growing sub-segment, driven by high-oxygen MAP applications for red meat color preservation and fresh produce packaging, with food grade oxygen shipments growing approximately 15% year-on-year in 2024.

Application Analysis

The packaging and preservation segment holds the leading position in the food grade gases market by application, capturing approximately 38% market share in 2025. The widespread deployment of MAP and vacuum sealing technologies across meat, dairy, bakery, and fresh produce segments is the primary driver, as food manufacturers seek chemical-free, regulatory-compliant solutions to extend shelf life and reduce food waste. The adoption of nitrogen flushing in bakery and confectionery packaging lines increased in roughly 22% of new installations in 2023, while food grade nitrogen and CO? usage in MAP grew by approximately 24% between 2022 and 2024. Modified Atmosphere Packaging is projected to be the fastest growing application segment through 2033, as food processors and retailers worldwide increase investments in extended shelf life technologies aligned with both regulatory mandates and sustainability goals.

Mode of Supply Analysis

Cryogenic tanks and liquid dewars represent the leading mode of supply in the food grade gases market, consolidating a market share of approximately 55% in 2025. Bulk supply via cryogenic systems, comprising large-capacity storage tanks and through-pipeline delivery, is the preferred choice of large-scale food processors, as it ensures continuous gas availability, reduces per-unit costs through economies of scale, and minimizes supply disruption risks. Bulk supply accounted for close to 35% of food grade gas market volume in 2022–2024, reflecting entrenched reliance on this mode in high-volume processing environments such as meat processing, dairy, and beverage manufacturing. On-site gas generation is the fastest growing mode of supply, driven by food processors seeking to reduce dependence on external suppliers, lower logistics costs, and comply with stringent purity requirements by generating gases in situ.

End-Use Industry Analysis

The beverages end-use segment leads the food grade gases market, accounting for approximately 36% market share in 2025. Beverages represent the single largest consumer of food grade CO? globally, as carbonation is a non-substitutable requirement in the production of soft drinks, sparkling water, beer, and other fizzy beverages. The global demand for carbonated beverages has demonstrated consistent resilience, supported by growing craft beer culture in North America and Europe, rapid urbanization-driven demand in Asia Pacific, and the proliferation of premium functional drinks. Meat, poultry, and seafood is the fastest growing end-use segment through 2033, as processors worldwide intensify their use of nitrogen (N?), CO?, and O? in cryogenic freezing and MAP applications to meet tightening food safety standards and consumer demands for fresh, preservative-free protein products across both developed and emerging markets.

Regional Insights

North America Food Grade Gases Market Trends and Insights

North America is the leading region in the global food grade gases market, commanding approximately 38% market share in 2025, driven by the United States' expansive and highly industrialized food processing sector. The U.S. accounts for approximately 37.8% of global food grade gas volume, with beef, poultry, and seafood processors heavily reliant on cryogenic CO? and nitrogen systems for freezing, chilling, and MAP. U.S. processors consumed nearly 950,000 tonnes of food grade nitrogen and CO? for these applications in 2024 alone. The regulatory environment, anchored by the FDA's comprehensive food safety framework, continues to ensure high and consistent gas purity standards across the supply chain, reinforcing buyer confidence in established suppliers.

The region's innovation ecosystem is a further competitive advantage, with companies such as Linde plc and Air Products & Chemicals, Inc. actively investing in next-generation gas delivery solutions, including on-site generation and digital gas monitoring platforms. The growing demand for nitrogen in MAP, reported to have captured over 41% of food grade industrial gas revenue by November 2025, and sustained beverage carbonation demand reinforce North America's role as both the largest and most technologically advanced market for food grade gases globally.

Europe Food Grade Gases Market Trends and Insights

Europe constitutes the second-largest regional market for food grade gases, with Germany, the United Kingdom, France, and Spain forming the demand core. The region's food processing sector is characterized by a strong emphasis on sustainability and circular economy principles, which is shaping gas procurement strategies toward bio-derived CO? and renewable energy-powered production. The European Food Safety Authority (EFSA) and EU Regulation EC 1333/2008 provide a harmonized regulatory framework that mandates strict gas purity standards, driving sustained investment in advanced filtration and quality assurance infrastructure across the continent.

In March 2025, Air Liquide S.A. launched a new range of food grade CO? cylinders across European markets, specifically designed for MAP, beverage carbonation, and food preservation applications, signaling continued market investment in European food safety infrastructure. The UK's CO? supply challenges, arising from the contraction of the domestic bioethanol sector, are simultaneously creating opportunities for renewable CO? producers and prompting food processors to diversify their gas sourcing strategies toward bio-based and waste-recovery sources.

Asia Pacific Food Grade Gases Market Trends and Insights

Asia Pacific is the fastest growing region, projected to expand at a CAGR of approximately 8.5% between 2026 and 2033, propelled by rapid urbanization, rising disposable incomes, and the expanding packaged food and beverage industries across China, India, Japan, and ASEAN nations. The region's growing middle class is driving unprecedented demand for packaged, processed, and convenience food products, directly stimulating the adoption of MAP, cryogenic freezing, and carbonation technologies. On-site nitrogen generation systems are currently utilized by approximately 17% of food processors in Asia Pacific as of 2024, a figure set to grow substantially as food safety regulations tighten and cold-chain infrastructure matures.

Japan, recognized as a mature and technologically sophisticated food market, is projected to be one of the fastest growing individual country markets, with its convenience food sector and advanced MAP adoption serving as primary demand catalysts. India's domestic packaged food growth and expanding on-site nitrogen generation installations position the country as a high-growth market through 2033. Regional manufacturers including Taiyo Nippon Sanso Corporation, Air Water Inc., and PT Aneka Gas Industri Tbk are capitalizing on these dynamics through localized production capacity expansion and strategic partnerships with regional food processors.

Competitive Landscape

The global food grade gases market exhibits a moderately consolidated structure, with a small group of multinational industrial gas companies accounting for a dominant share of revenues. High entry barriers, including capital-intensive production, stringent food safety compliance, and established distribution networks, limit the presence of new entrants and reinforce the position of leading players. The market is characterized by long-term supply agreements with food and beverage processors, ensuring stable demand and recurring revenue streams.

From a strategic standpoint, companies compete through investments in integrated supply chains, including bulk storage, cylinder distribution, and on-site gas generation capabilities. Increasing emphasis is placed on sustainable gas sourcing, particularly bio-derived and recovered CO?, to address supply volatility and decarbonization goals. Additionally, players are expanding geographically in high-growth regions such as Asia Pacific and the Middle East, while adopting digital monitoring and automation solutions to enhance supply efficiency, traceability, and customer value propositions.

Key Developments

- April 2025: Air Products inaugurated Uzbekistan’s first high-purity food-grade CO? production facility in Navoi, utilizing captured emissions from ammonia production, with a capacity of 120 tons per day and compliance with international purity standards.

- September 2025: Bio Capital announced food grade CO? production from its anaerobic digestion facilities in Northern Ireland and Norfolk, UK, with a combined capacity to supply approximately 15,000 tonnes of CO? per year, helping alleviate UK supply shortages.

- April 2024: Linde plc increased production capacity at its Mims, Florida facility by 50%, enhancing its food grade gas supply capabilities to meet growing demand from U.S. food and beverage processors in the Southeast region.

Companies Covered in Food Grade Gases Market

- Linde plc

- Air Liquide S.A.

- Air Products & Chemicals, Inc.

- Messer Group

- Taiyo Nippon Sanso Corporation

- Wesfarmers Limited

- Gulf Cryo

- SOL Group

- Massy Group

- Air Water Inc.

- PT Aneka Gas Industri Tbk

- National Gases Ltd.

- Coregas Pty Ltd.

- Emirates Industrial Gases Co., LLC

- Praxair Technology, Inc.

- Matheson Tri-Gas, Inc.

- SIAD Group

- Iwatani Corporation

Frequently Asked Questions

The global food grade gases market is valued at US$ 9.1 billion in 2026 and is projected to reach US$ 14.8 billion by 2033 at a CAGR of 7.2%.

Growth is driven by rising demand for packaged foods, increasing use of MAP and cryogenic preservation, expansion of carbonated beverages, and stringent food safety regulations.

North America leads the market, accounting for around 38% share, driven primarily by strong food processing and beverage industries in the United States.

The key opportunity lies in bio-derived and sustainable CO₂ production, including carbon capture and circular economy solutions.

Key players include Linde plc, Air Liquide S.A., Air Products & Chemicals, Inc., Messer Group, Taiyo Nippon Sanso Corporation, and others competing on purity, supply, and global reach.