- Biotechnology

- Gastrointestinal Infection Testing Market

Gastrointestinal Infection Testing Market Size, Share, and Growth Forecast 2026 - 2033

Gastrointestinal Infection Testing Market by Product (Instruments, Reagents, and Consumables), Test Type (Molecular Tests, Immunoassays, Culture Tests, Others), Infection Type (Bacterial Infections, Viral Infections, Parasitic Infections), End-user (Hospitals, Diagnostic Laboratories, Ambulatory Surgery Centers, Research and Academic Institutes, Others), and Regional Analysis, 2026–2033

Gastrointestinal Infection Testing Market Share and Trends Analysis

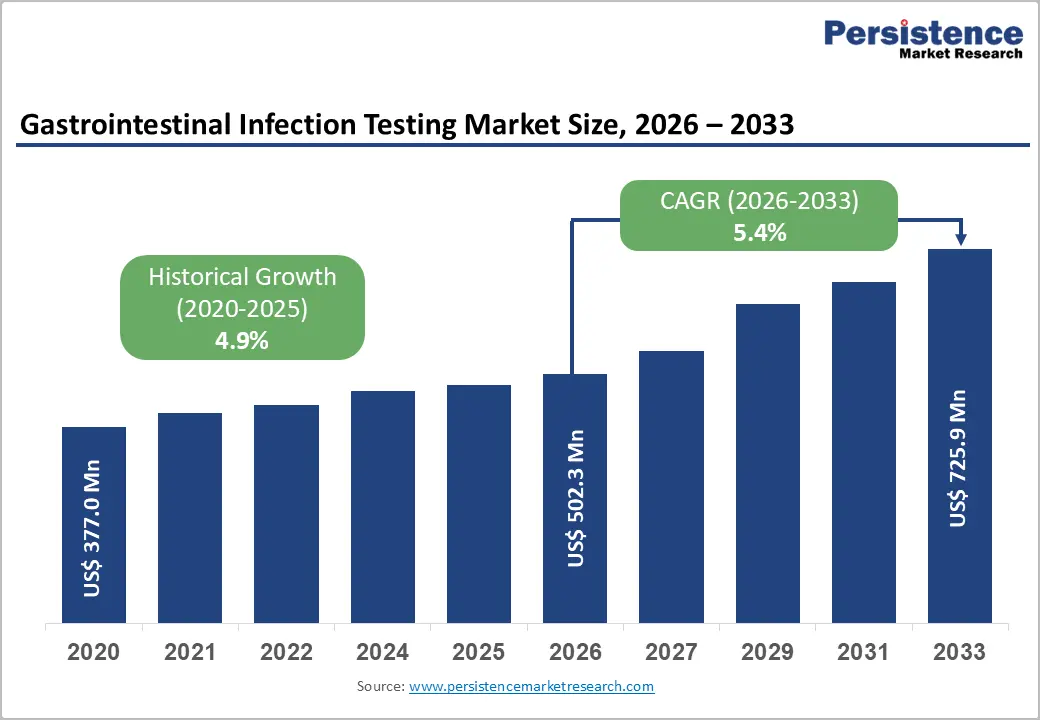

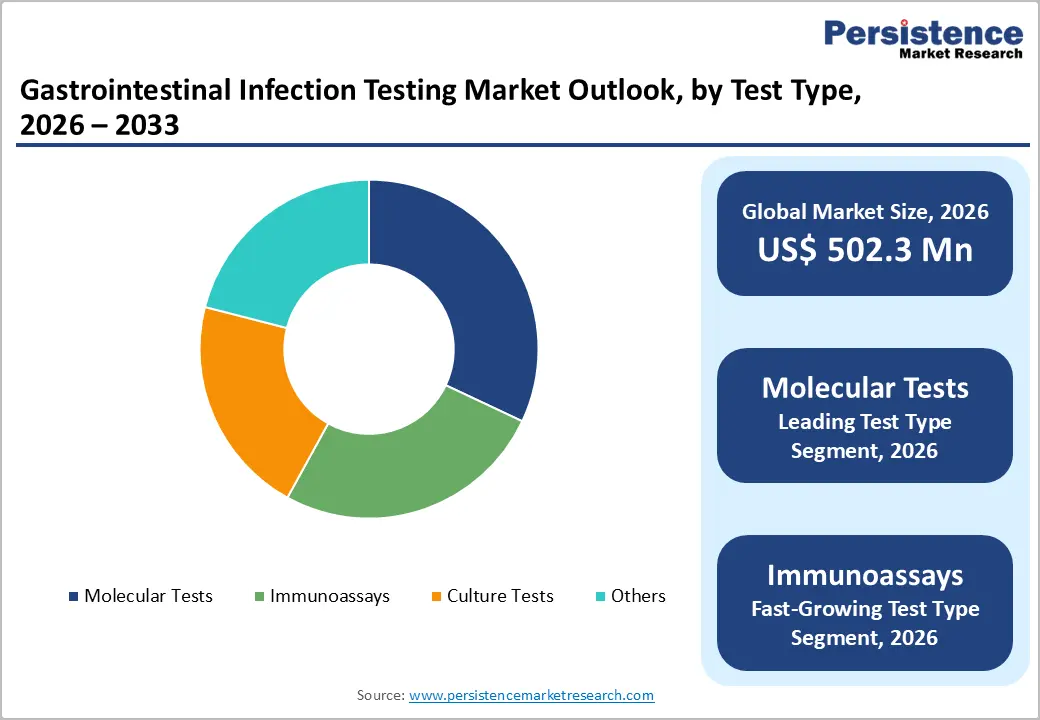

The global gastrointestinal infection testing market size is expected to be valued at US$ 502.3 million in 2026 and projected to reach US$ 725.9 million by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

The market's steady trajectory is driven by the rising global burden of gastrointestinal infections, rapid adoption of molecular diagnostic technologies, and expanding healthcare infrastructure in emerging economies. According to the World Health Organization (WHO), diarrheal diseases predominantly caused by GI pathogens claim approximately 1.6 million lives annually, underscoring the critical need for accurate, rapid diagnostic testing.

Technological advancement in multiplex PCR panels, point-of-care immunoassay platforms, and next-generation sequencing, combined with increasing laboratory automation and favorable reimbursement frameworks in North America and Europe, are collectively sustaining above-average market value growth throughout the forecast period.

Key Industry Highlights:

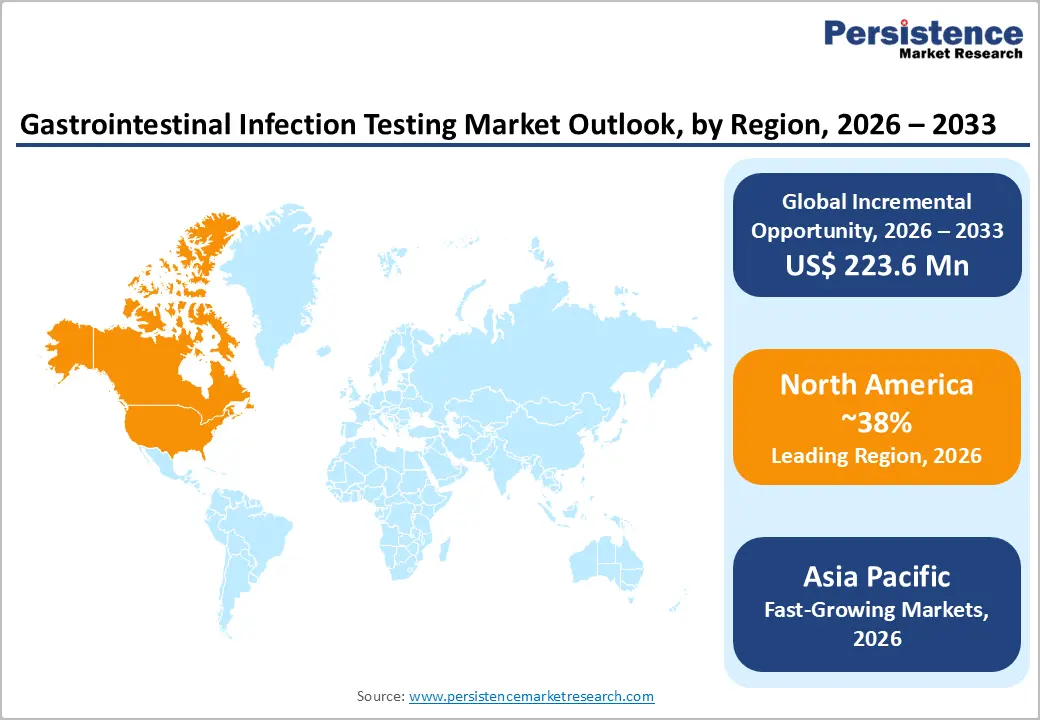

- Leading Region – North America commands 38% of the global GI infection testing market share in 2026, anchored by the U.S.'s high GI disease burden (48 million annual foodborne cases), FDA-cleared multiplex platforms, and antimicrobial stewardship mandates driving systematic molecular diagnostic adoption.

- Fast-Growing Region – Asia Pacific is the fastest-growing region, driven by China's vast hospital network expansion, India's Ayushman Bharat health coverage initiative, and Southeast Asia's laboratory modernization investments, all amplifying GI diagnostic testing volumes at above-market CAGR rates.

- Dominant Product Segment – Reagents and Consumables lead by product with ~62% share, generating recurring, high-margin revenue streams through cartridge and kit consumption across the growing global installed base of molecular and immunoassay GI testing instrument platforms.

- Fast-Growing Segment – Immunoassays are the fastest-growing test type, propelled by expanding CLIA-waived rapid POC platforms for Norovirus, Rotavirus, and C. difficile, enabling decentralized GI diagnostics in urgent care, physician offices, and underserved healthcare settings globally.

- Key Opportunity – NGS and POC Diagnostics Convergence: The convergence of declining NGS costs for metagenomic GI diagnostics and rapid immunoassay POC expansion in Asia Pacific and Latin America presents a US$ 223.6 million absolute incremental opportunity for innovative diagnostic companies.

Market Dynamics

Drivers - Rising Global Burden of Gastrointestinal Infections and Demand for Rapid Diagnostics

Gastrointestinal infections caused by pathogens such as Clostridioides difficile (C. diff), Salmonella, Norovirus, and Campylobacter impose an enormous clinical and economic burden globally. The U.S. Centers for Disease Control and Prevention (CDC) estimates that foodborne illnesses alone affect approximately 48 million Americans annually, resulting in 128,000 hospitalizations and 3,000 deaths.

In healthcare settings, C. difficile infection (CDI) is among the most common hospital-acquired infections, with the CDC reporting nearly 500,000 CDI cases per year in the U.S. alone. These statistics are directly fueling demand for rapid, accurate GI infection testing platforms capable of delivering same-day results to enable timely antimicrobial stewardship, reduce unnecessary antibiotic use, and improve patient outcomes across hospital and outpatient settings.

Proliferation of Multiplex Molecular Diagnostic Panels for GI Pathogens

The commercial introduction of FDA-cleared multiplex gastrointestinal pathogen panels capable of simultaneously detecting 20+ bacterial, viral, and parasitic targets from a single stool specimen in under one hour has fundamentally transformed clinical GI diagnostics. BioFire Diagnostics' FilmArray GI Panel, cleared by the U.S. FDA and endorsed by the Infectious Diseases Society of America (IDSA), has set a new standard of care for acute gastroenteritis workups.

A landmark study published in the Journal of Clinical Microbiology demonstrated that multiplex PCR panels increase GI pathogen detection rates by up to 40% compared to conventional culture methods. This diagnostic superiority, combined with workflow efficiencies and reduced time-to-result, is accelerating platform adoption across hospital and reference laboratory settings worldwide, directly expanding the Reagents and Consumables revenue base for manufacturers.

Restraints - High Cost of Molecular Diagnostic Platforms and Reimbursement Limitations

Despite their clinical advantages, molecular GI testing platforms carry substantial capital and per-test costs that create significant adoption barriers, particularly in resource-limited healthcare systems. A multiplex PCR GI panel test can cost US$ 300–500 per patient episode, approximately 5–10 times the cost of conventional culture-based testing. In many Asia Pacific, Latin American, and Middle Eastern markets, limited reimbursement coverage for advanced molecular diagnostics restricts utilization to tertiary referral centers, excluding large patient populations from timely, accurate diagnoses and suppressing market volume growth potential in these geographies.

Complexities of Stool Specimen Handling and Pre-Analytical Variability

Stool specimens present unique pre-analytical challenges that can compromise diagnostic accuracy and complicate laboratory workflows. Variability in specimen collection technique, transport media, storage temperature compliance, and time-to-processing can significantly affect pathogen viability and nucleic acid integrity. The Clinical and Laboratory Standards Institute (CLSI) guidelines acknowledge that pre-analytical errors account for the majority of false-negative results in GI pathogen testing. These complexities increase staff training requirements, add operational costs, and can lead to discordance in results across testing sites, limiting standardization and hindering the widespread deployment of advanced GI testing protocols in decentralized or point-of-care settings.

Opportunities - Expansion of Point-of-Care Immunoassay Testing in Outpatient and Primary Care Settings

The accelerating shift toward decentralized diagnostics presents a major growth opportunity for rapid immunoassay-based GI infection testing platforms designed for point-of-care (POC) deployment. The FIND (Foundation for Innovative New Diagnostics) has identified rapid POC GI diagnostics as a priority investment area for low- and middle-income country (LMIC) healthcare systems. Modern lateral flow immunoassay platforms now offer CLIA-waived status for key GI pathogens, including Norovirus, Rotavirus, and C. difficile, enabling deployment in physician offices, urgent care centers, and community clinics.

Abbott Laboratories' ID NOW platform and Quidel Corporation's Sofia 2 system exemplify this trend. As outpatient GI infection burden grows and healthcare systems prioritize antimicrobial stewardship, POC immunoassays represent a high-volume, scalable revenue expansion opportunity, particularly in Asia Pacific and Latin America, where laboratory infrastructure remains underdeveloped.

Next-Generation Sequencing (NGS) and Metagenomics for Complex GI Infection Diagnostics

Metagenomic next-generation sequencing (mNGS) is emerging as a transformative technology for diagnosing polymicrobial, treatment-refractory, and novel GI infections that evade conventional and multiplex PCR-based detection. Published research in the New England Journal of Medicine has demonstrated the mNGS capability to identify GI pathogens in cases where standard diagnostics were inconclusive.

Companies including Illumina, Inc. and Qiagen N.V. are actively developing clinical-grade mNGS workflows for infectious disease applications. The U.S. FDA's evolving regulatory framework for NGS-based diagnostics, including the 2020 NGS-Based Infectious Disease Diagnostic Tests Guidance, is reducing regulatory uncertainty. As costs decline toward US$ 100–200 per test, NGS-based GI diagnostics represent a significant long-term market opportunity, particularly for immunocompromised patient populations in transplant and oncology settings.

Category-wise Analysis

Product Insights

The reagents and consumables segment leads the gastrointestinal infection testing market by product, accounting for approximately 62% of the total share in 2026. This dominance reflects the recurring, high-volume expenditure nature of reagents and consumables, including PCR master mixes, extraction kits, assay cartridges, and specimen collection devices that are consumed with every diagnostic test performed.

Unlike instruments, which are capital purchases made infrequently, reagents and consumables generate predictable, recurring revenue streams that constitute the primary commercial model for leading diagnostic companies such as bioMérieux SA, Thermo Fisher Scientific, Inc., and Becton, Dickinson and Company (BD). The ongoing expansion of installed instrument bases across hospitals and diagnostic laboratories globally further amplifies consumable pull-through demand. High per-test reagent consumption in multiplex molecular panels, which require specialized cartridges, is a key structural driver sustaining segment leadership through the forecast horizon.

Test Type Insights

The molecular tests segment leads the gastrointestinal infection testing market by test type, holding approximately 32% share in 2026. Molecular diagnostics, primarily real-time PCR and multiplex PCR-based GI panels have achieved this leadership position through superior sensitivity and specificity compared to traditional culture and immunoassay methods. The FDA-cleared BioFire FilmArray GI Panel (bioMérieux SA) and Luminex xTAG Gastrointestinal Pathogen Panel (DiaSorin S.p.A.) represent the commercial vanguard of this segment.

A Lancet Infectious Diseases study confirmed PCR-based GI panel sensitivity exceeding 95% for the majority of target pathogens. Institutional adoption mandated by IDSA clinical guidelines, which recommend molecular testing as the preferred diagnostic approach for acute gastroenteritis, continues to drive the rapid expansion of molecular test volumes and associated reagent revenues.

Infection Type Insights

The bacterial infections segment leads the gastrointestinal infection testing market by infection type, accounting for approximately 48% share in 2026. Bacterial GI pathogens, including Salmonella, Campylobacter, Shigella, Escherichia coli O157:H7, Clostridioides difficile, and Helicobacter pylori represent the most clinically significant and diagnostically tested category due to their high global incidence, association with serious complications, and critical role in antimicrobial stewardship programs.

The CDC's FoodNet surveillance data consistently identifies bacterial pathogens as the leading cause of laboratory-confirmed GI infections in the United States. Hospital infection control programs mandate rapid GI bacterial testing for patients admitted with diarrheal illness, creating a high-volume, institutionally driven demand base. The breadth of bacterial targets in commercially available multiplex panels further solidifies bacterial infection diagnostics as the segment's revenue anchor.

End-user Insights

Hospitals represent the leading end-user segment in the gastrointestinal infection testing market, commanding approximately 44% share in 2026. Hospitals drive this leadership through high inpatient volumes of acute GI illness, institutional infection control mandates requiring rapid pathogen identification, and access to capital budgets enabling investment in advanced molecular diagnostic platforms. Academic medical centers and large health systems in the U.S., Germany, and Japan are early adopters of multiplex PCR GI panels, driving significant reagent and consumable revenues.

The Joint Commission and equivalent accreditation bodies in Europe mandate laboratory quality standards that incentivize the adoption of validated molecular testing platforms. Diagnostic Laboratories represent the fastest-growing end-user segment, driven by the outsourcing of complex GI testing from community hospitals to high-throughput reference laboratory networks such as Quest Diagnostics and Labcorp.

Regional Insights

North America Gastrointestinal Infection Testing Market Trends and Insights

North America leads the global Gastrointestinal Infection Testing market with 38% share in 2026, underpinned by a highly developed diagnostic infrastructure, robust reimbursement frameworks under Medicare and Medicaid, and early adoption of FDA-cleared multiplex molecular GI panels. Antimicrobial stewardship programs and CDC surveillance mandates continue to drive institutional GI testing volumes across hospital networks and reference laboratories.

U.S. Gastrointestinal Infection Testing Market Size

The United States accounts for approximately 85% of North America's GI infection testing revenue, reflecting its scale of healthcare expenditure and high per-test diagnostic rates. With 48 million annual foodborne illness cases and a significant C. difficile hospital burden, the U.S. generates the world's highest molecular GI test volumes, supported by broad FDA clearance of multiplex platforms.

Europe Gastrointestinal Infection Testing Market Trends and Insights

Europe represents the second-largest regional market, characterized by harmonized EU in vitro diagnostic regulations under IVDR (Regulation EU 2017/746), growing adoption of molecular GI diagnostics in tertiary hospitals, and national antimicrobial resistance action plans in Germany, the U.K., and France that drive structured GI pathogen surveillance and testing investment across public health laboratory networks.

Germany Gastrointestinal Infection Testing Market Size

Germany holds approximately 22% of European GI infection testing revenue, supported by its dense hospital network, Robert Koch Institute (RKI) surveillance mandates, and high per capita diagnostic expenditure. Germany's national antimicrobial resistance strategy DART 2030 drives systematic molecular GI testing integration across university hospitals and regional diagnostic centers.

U.K. Gastrointestinal Infection Testing Market Size

The United Kingdom accounts for approximately 17% of European market revenue, underpinned by NHS England's antimicrobial stewardship commitments and UKHSA (UK Health Security Agency) enteric disease surveillance programs. Post-Brexit regulatory alignment with UKCA marking has created a distinct but manageable pathway for GI diagnostic product approvals.

France Gastrointestinal Infection Testing Market Size

France contributes approximately 14% of European GI infection testing revenues. The Santé publique France national public health agency coordinates GI outbreak surveillance, generating structured diagnostic testing demand. France's centralized hospital procurement model and HAS (Haute Autorité de Santé) diagnostic reimbursement framework support consistent adoption of validated molecular GI testing platforms.

Asia Pacific Gastrointestinal Infection Testing Market Trends and Insights

Asia Pacific is the fastest-growing regional market for GI infection testing, driven by high GI infection prevalence, particularly in China, India, and Southeast Asia, expanding laboratory infrastructure investment, and government-led universal health coverage initiatives. China represents the largest Asia Pacific market, with its vast hospital network, National Medical Products Administration (NMPA)-approved molecular diagnostic platforms, and significant unmet diagnostic needs in tier-2 and tier-3 cities, driving accelerating testing volume growth.

India Gastrointestinal Infection Testing Market Size

India is one of the fastest-growing GI testing markets in the Asia Pacific, contributing approximately 12% of regional revenue. The country's high incidence of enteric diseases, including typhoid, cholera, and rotavirus gastroenteritis, combined with the Ayushman Bharat health scheme expanding diagnostics access, is driving laboratory network expansion and adoption of immunoassay-based GI testing platforms.

Competitive Landscape

The gastrointestinal infection testing market is moderately consolidated, with competition driven by advancements in molecular diagnostics, multiplex PCR panels, immunoassays, and rapid testing platforms. Market participants focus on improving diagnostic accuracy, reducing turnaround time, and expanding pathogen detection capabilities to strengthen their position. Strategic collaborations, product launches, acquisitions, and regional expansion remain key growth strategies. Demand from hospitals, diagnostic laboratories, and point-of-care settings continues to increase competitive intensity.

Key Developments:

- In January 2026, Cepheid received U.S. FDA clearance for its Xpert GI Panel, a multiplex PCR test designed to detect 11 clinically relevant gastrointestinal bacterial, viral, and parasitic pathogens from a single stool sample.

- In April 2026, QIAGEN launched the CE-IVDR-certified QIAstat-Dx BCID GPF Plus AMR Panel for bloodstream infection syndromic testing. The new panel was designed to identify 20 gram-positive bacterial and fungal pathogens along with 10 antimicrobial resistance markers from positive blood cultures and pure colonies in nearly one hour.

Companies Covered in Gastrointestinal Infection Testing Market

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific, Inc.

- Abbott Laboratories

- F. Hoffmann-La Roche AG

- Cepheid (a Danaher company)

- DiaSorin S.p.A.

- bioMérieux SA

- Quidel Corporation

- Hologic, Inc.

- Becton, Dickinson and Company (BD)

- Meridian Bioscience, Inc.

- Qiagen N.V.

- PerkinElmer, Inc.

- Illumina, Inc.

Frequently Asked Questions

The global gastrointestinal infection testing market size is estimated to reach US$ 502.3 million in 2026.

Key demand drivers include the high global burden of GI infections, with the CDC reporting 48 million annual U.S. foodborne cases, widespread clinical adoption of FDA-cleared multiplex PCR panels such as the BioFire FilmArray GI Panel, institutional antimicrobial stewardship program mandates requiring rapid pathogen identification, and the rapid expansion of point-of-care immunoassay platforms in decentralized diagnostic settings.

North America is likely to lead the global share with 38% share in 2026.

The key growth opportunity in the Gastrointestinal Infection Testing market lies in the rising adoption of multiplex molecular diagnostics and point-of-care testing solutions. Increasing demand for rapid, accurate, and simultaneous detection of multiple gastrointestinal pathogens is encouraging healthcare providers to shift from conventional culture methods to advanced PCR-based platforms.

Leading companies include bioMérieux SA, Thermo Fisher Scientific Inc., Abbott Laboratories, F. Hoffmann-La Roche AG, Cepheid (Danaher), Becton Dickinson and Company (BD), Qiagen N.V., DiaSorin S.p.A., Bio-Rad Laboratories Inc., Hologic Inc., Quidel Corporation, Meridian Bioscience Inc., PerkinElmer Inc., Illumina Inc., and Seegene Inc., among others.