- Semiconductor Materials & Components

- U.S. Semiconductor Gases Market

U.S. Semiconductor Gases Market Size, Share, Growth, and Regional Forecast 2026 - 2033

U.S. Semiconductor Gases Market by Gas Type (Bulk Gases: Nitrogen, Oxygen, Argon, Helium, Hydrogen, Carbon Dioxide; Electronic Special Gases/ESGs: Chlorine, Ammonia, Silicone, Others), Process (Chamber Cleaning, Oxidation, Deposition, Etching, Doping, Others), and Regional Analysis for 2026 - 2033

U.S. Semiconductor Gases Market Size and Trend Analysis

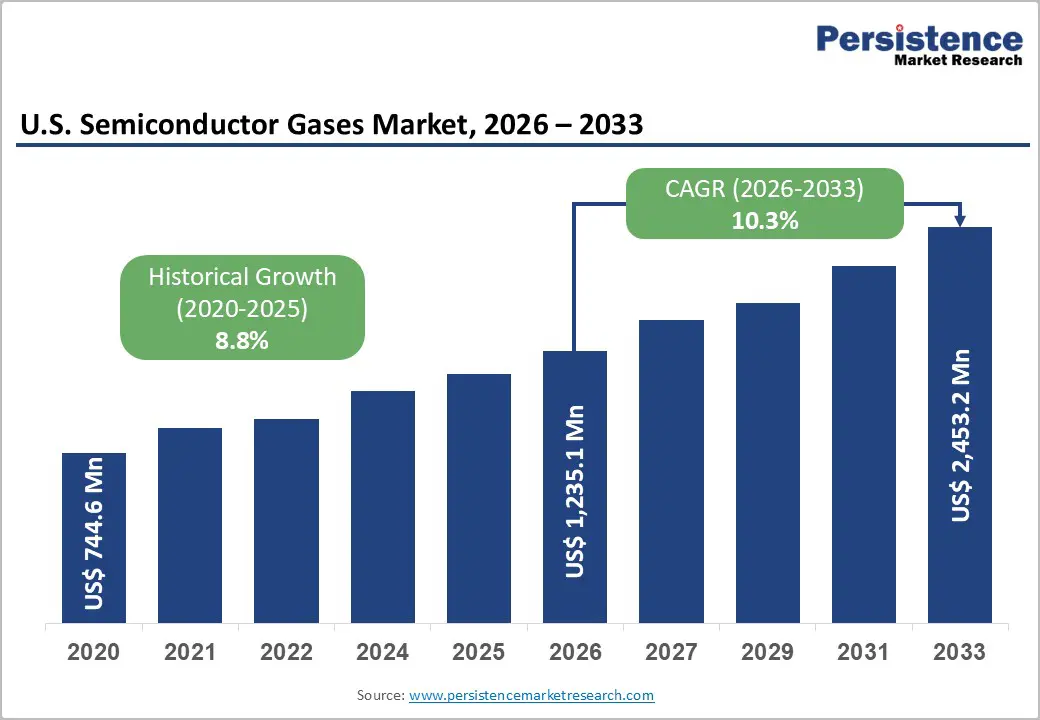

The U.S. semiconductor gases market size is supposed to be valued at US$ 1,235.1 Million in 2026 and is projected to reach US$ 2,453.2 Million by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

The U.S. semiconductor gases market is entering its most commercially dynamic growth decade, driven by the landmark CHIPS and Science Act of 2022 committing US$ 52.7 billion in federal investment to domestic semiconductor manufacturing, the structural demand acceleration from AI accelerator chip production, advanced logic and memory node transitions requiring increasingly gas-intensive fabrication processes, and the geopolitical imperative to onshore critical semiconductor supply chains away from Asia-concentrated production geographies.

Key Market Highlights

- Leading Region: West U.S. leads the U.S. semiconductor gases market, anchored by TSMC Arizona Fab 21's US$ 65 billion investments, Intel Oregon's Hillsboro fab complex, Air Products' on-site gas infrastructure at Phoenix and Hillsboro facilities, and Arizona Commerce Authority's CHIPS-aligned incentive programs.

- Fastest Growing Region: The Midwest U.S. is the fastest-growing region, propelled by Intel's US$ 100 billion New Ohio One fab campus commitment, the U.S. Department of Commerce's US$ 8.5 billion CHIPS Act preliminary agreement with Intel for Ohio/Arizona/New Mexico investments.

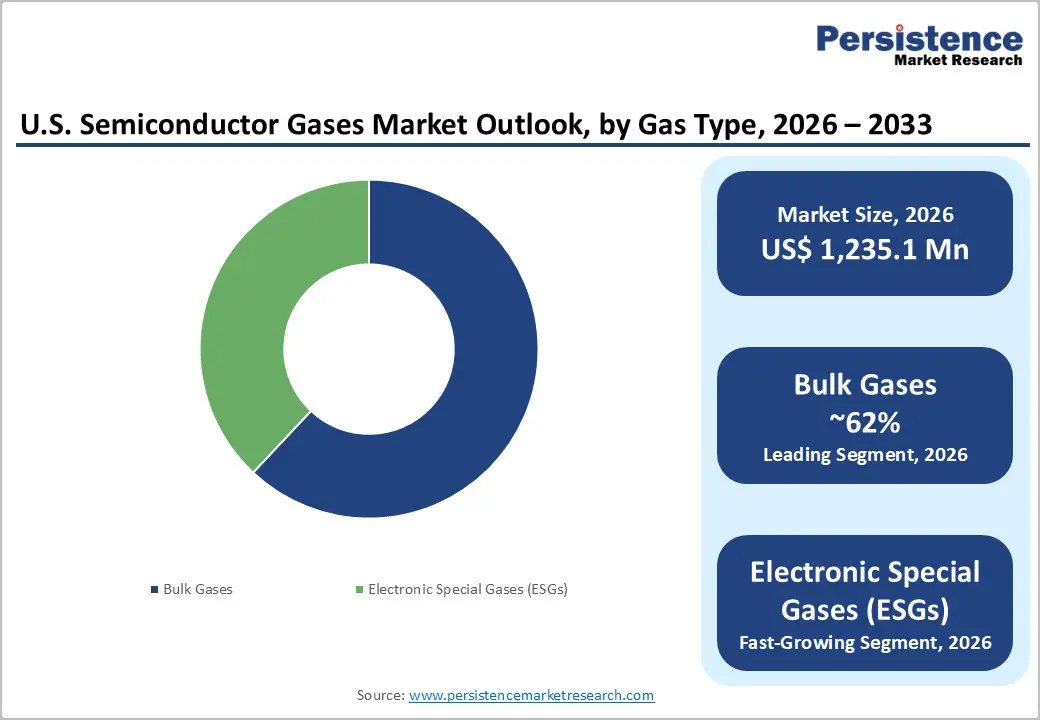

- Dominant Gas Type: Bulk Gases dominate the Gas Type segment with approximately 62% revenue share, anchored by nitrogen's documented consumption of 50-100 tons per day at advanced 300mm fabs, continuous 24/7 fab operation, gas purging requirements, and the irreplaceable role of argon, helium, and hydrogen across CVD, implant, and equipment cooling semiconductor process applications.

- Fastest Growing Gas Type: Electronic Special Gases (ESGs) represent the fastest-growing Gas Type sub-segment, driven by SEMI's documented 10-15x higher ESG consumption per wafer pass at advanced nodes, GAA transistor and 3D NAND process chemistry intensification.

- Key Market Opportunity: CHIPS Act on-site gas supply contracts and next-generation ESG formulation development represent the dual key market opportunities, with US$ 200 billion in U.S. fab co-investment generating decade-scale captive gas procurement.

| Key Insights | Details |

|---|---|

| U.S. Semiconductor Gases Market Size (2026E) | US$ 1,235.1 Million |

| Market Value Forecast (2033F) | US$ 2,453.2 Million |

| Projected Growth CAGR (2026 - 2033) | 10.3% |

| Historical Market Growth (2020 - 2025) | 8.8% |

DRO Analysis

CHIPS and Science Act Domestic Fab Expansion Creating Historic Semiconductor Gas Demand Wave Across U.S. Manufacturing Geography

The CHIPS and Science Act of 2022, signed into law by President Biden committing US$ 52.7 billion in direct federal semiconductor manufacturing and R&D investment, has catalyzed the most significant wave of domestic semiconductor fabrication capacity investment in U.S. history, with the U.S. Department of Commerce announcing preliminary agreements for CHIPS Act funding disbursements exceeding US$ 35 billion across major fab investment projects including TSMC's two Arizona fabs, Intel's Ohio fab cluster, Samsung's Taylor Texas expansion, and Micron Technology's New York and Idaho memory fab programs. Each advanced logic or memory fab at the 3nm, 2nm, and below technology nodes requires an exceptionally gas-intensive fabrication process, with industry data from the Semiconductor Equipment and Materials International (SEMI) organization documenting that advanced node fabs typically consume 10-15 times more specialty gases per wafer pass than mature node 200mm fabs, due to the dramatically increased number of process steps, multi-patterning lithography sequences, and atomic layer deposition (ALD) cycles required.

Air Products and Chemicals Inc., the U.S.'s most commercially dominant industrial and semiconductor gas supplier, has announced multiple long-term on-site gas supply agreements with U.S. CHIPS Act fab investment recipients, documenting the direct commercial linkage between federal semiconductor manufacturing policy and semiconductor gas supplier revenue growth. Messer SE and Co. KGaA's U.S. gas operations and Taiyo Nippon Sanso's U.S. semiconductor gas division are also actively investing in capacity expansions adjacent to new U.S. fab construction sites.

AI Chip Demand and Advanced Node Transition Accelerating ESG Consumption in U.S. Fab Operations

The global artificial intelligence infrastructure investment boom, anchored by hyperscaler procurement of NVIDIA's H100 and B200 series AI accelerator GPUs, AMD's Instinct MI300 series, and Google's Tensor Processing Units (TPUs), all manufactured at advanced TSMC and Samsung foundry nodes, is generating a structurally above-average demand acceleration for Electronic Special Gases (ESGs) consumed in the most gas-intensive fabrication process steps at sub-5nm technology nodes. Advanced AI chip manufacturing at 3nm, 2nm, and Gate-All-Around (GAA) transistor architecture nodes requires dramatically expanded deployment of high-purity deposition gases including silane (SiH), disilane (Si-H), ammonia (NH), and tungsten hexafluoride (WF), etching gases including nitrogen trifluoride (NF), octafluorocyclobutane (C-F), and sulfur hexafluoride (SF), and chamber cleaning gases including NF and C-F, all classified as ESGs requiring ultra-high-purity (UHP) 99.9999% (6N) purity specifications that command significant price premiums over standard industrial gas grades.

SEMI's Semiconductor Equipment Book documented a US$113 billion global semiconductor equipment market in 2023, with ALD and CVD deposition equipment representing the fastest-growing tool category, each requiring correspondingly higher ESG consumption volumes. Solvay (headquartered in Brussels, Belgium, with major U.S. operations) and Electronic Fluorocarbons LLC serve the U.S. ESG market with specialty fluorocarbon and nitrogen fluoride compound gases essential to advanced-node etching and chamber-cleaning processes.

Restraints - Helium Supply Scarcity and Geopolitical Concentration of Noble Gas Sources Creating Critical Supply Vulnerability

The U.S. semiconductor gas supply chain faces a structurally significant raw material vulnerability in helium, an irreplaceable noble gas used extensively in semiconductor manufacturing for equipment cooling, carrier gas applications in CVD processes, and fiber-optic equipment, whose global production is highly concentrated. The U.S. Bureau of Land Management (BLM) Federal Helium Reserve in Amarillo, Texas, which historically supplies approximately 30% of global helium, has been undergoing a federal divestiture transition, creating uncertainty about U.S. domestic supply.

Meanwhile, Qatar and Russia together account for over 60% of global helium production, with geopolitical supply disruption risks demonstrated by the impact of the Russia-Ukraine conflict on Russian helium export flows in 2022, generating temporary helium price spikes that directly impacted semiconductor fab operating costs across all major U.S. chip manufacturing facilities dependent on continuous helium supply.

Ultra-High-Purity Gas Specification Requirements: Creating Qualification Lead Times and Supply Flexibility Constraints

The semiconductor gas industry's requirement for UHP 99.9999% (6N) and above purity specifications, enforced through rigorous incoming quality control analytical testing protocols at semiconductor fab receiving inspection points per SEMI F5 and F20 standards, creates structural supply qualification lead times of 6-18 months that limit semiconductor gas supply agility and constrain the ability of fab operators to qualify alternative suppliers rapidly in response to primary supplier capacity shortfalls or quality incidents.

The International Technology Roadmap for Semiconductors (ITRS) documented progressively tightening metallic impurity and moisture specifications for semiconductor process gases at advanced nodes, with sub-ppt (parts per trillion) trace metallic contamination limits for some critical ESG applications, that require specialized manufacturing, purification, cylinder passivation, and analytical verification capabilities that restrict the qualified supplier base and create oligopolistic supply conditions limiting fab procurement flexibility.

Opportunities - CHIPS Act On-Site Gas Production Infrastructure Creating Long-Term Captive Supply Contract Opportunities

The CHIPS and Science Act fab investment wave, requiring each new advanced semiconductor fabrication plant to source continuous and uninterrupted ultra-high-purity gas supply volumes of nitrogen, argon, hydrogen, and oxygen on a 24/7/365 basis at volumes that cannot be economically transported from off-site sources, is creating a compelling commercial model of on-site gas generation plant co-investment where gas suppliers build and operate dedicated on-site nitrogen, oxygen, hydrogen, and argon generation plants adjacent to or inside the fab facility boundary under long-term exclusive supply contracts typically spanning 10-20 years that provide exceptional revenue visibility and return-on-investment security.

Air Products and Chemicals Inc.'s documented on-site gas supply model, which the company has deployed at semiconductor fabs globally and is now actively positioning for U.S. CHIPS Act fab projects, generates annuity-like recurring gas revenue streams indexed to fab production volume utilization that provide above-market revenue growth stability through technology node transitions and economic cycles. The U.S. Department of Energy (DOE)'s National Renewable Energy Laboratory (NREL) and the DOE Hydrogen Programs documentation of on-site green hydrogen production viability at industrial facilities creates an adjacent opportunity for semiconductor gas suppliers to co-locate green hydrogen generation with on-site nitrogen and oxygen plants at U.S. fab campuses, combining semiconductor gas supply with clean energy infrastructure investment. Messer SE and Co. KGaA's U.S. gas division and Iwatani Corporation's North American gas operations are both investing in on-site gas plant infrastructure development capabilities to compete for CHIPS Act fab supply contracts.

Advanced ESG Formulations for GAA Transistor and 3D NAND Memory Fabrication Creating Premium Product Segment Growth

The global semiconductor industry's transition to Gate-All-Around (GAA) nanosheet transistor architectures at sub-3nm logic nodes, implemented by Samsung Foundry from 3nm and by TSMC and Intel from 2nm onward, and the concurrent scaling of 3D NAND flash memory to 200+ layer stack heights introduces fundamentally new and extraordinarily gas-intensive process chemistry requirements that create substantial commercial opportunities for ESG suppliers able to develop, qualify, and supply next-generation specialty gas formulations at purity and analytical traceability specifications beyond existing commercial gas production capabilities. GAA transistor fabrication requires selective etching gases including Methyl fluoride (CH-F) and novel fluorocarbon compound blends with ultra-precise selectivity ratios between silicon, silicon nitride, and silicon oxide that are not achievable with conventional commodity fluorocarbon ESG grades, creating a premium specialty gas product development opportunity estimated by SEMI process technology working groups to require new gas chemistry solutions for each successive technology node transition.

Solvay's specialty fluorochemicals and electronic materials division and Sumitomo Seika Chemicals Company Ltd. (headquartered in Osaka, Japan, with U.S. distribution) are investing in next-generation ESG formulation development programs targeting GAA and 3D NAND process chemistry requirements. REC Silicon ASA, the U.S.'s only domestic manufacturer of polysilicon and UHP silane gas, is uniquely positioned to supply UHP silane (SiH) to U.S. CHIPS Act fabs with a domestically sourced supply chain that meets the CHIPS Act's supply chain resilience objectives.

Category-wise Insights

By Gas Type Analysis

Bulk Gases lead the U.S. Semiconductor Gases market by gas type, accounting for approximately 62% of total gas type segment revenue in 2026, a dominant position reflecting the exceptionally high volumetric consumption of nitrogen, argon, oxygen, hydrogen, and helium across virtually every semiconductor fabrication process step in continuous 24/7 fab operations, where bulk gas consumption volumes per fab can reach hundreds of tonnes per day of nitrogen alone for purging, inerting, and carrier gas applications.

Nitrogen is the single highest-volume semiconductor gas consumed in U.S. fabs, used for wafer environment purging in equipment loadlocks, process tool purging between process steps, and as a carrier gas in numerous CVD deposition processes, with an advanced 300mm logic fab consuming in excess of 50-100 tons per day of ultra-high-purity nitrogen at UHP 99.9999% specification. Electronic Special Gases (ESGs) hold approximately 38% of gas type revenue and are the fastest-growing sub-segment, driven by advanced node process intensification requirements.

By Process Insights

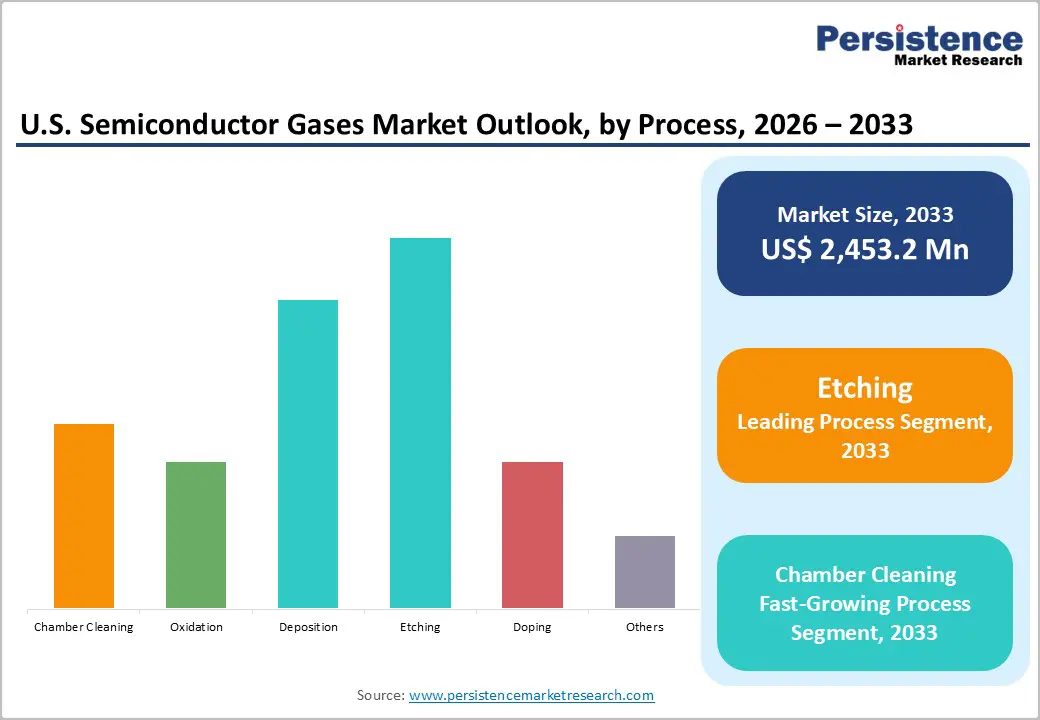

Etching leads the U.S. Semiconductor Gases market by process application, commanding approximately 30% of total process segment revenue in 2026, a dominant position reflecting etching's role as the most gas-consumptive and technically complex semiconductor fabrication process category, encompassing plasma dry etching (RIE, ICP, CCP) process steps that consume the largest variety and highest unit cost categories of Electronic Special Gases (ESGs) including nitrogen trifluoride (NF), octafluorocyclobutane (CF), hexafluorobutadiene (C-F), carbon tetrafluoride (CF), and chlorine (Cl).

Each advanced 3nm logic chip requires over 100 photolithography-etch-deposition cycle iterations in a multi-patterning or EUV exposure process sequence, with each etch step consuming specialized ESG mixtures whose complexity and purity requirements increase at each successive technology node. The Semiconductor Industry Association (SIA) documents that etching and deposition together represent the two largest process tool investment categories in advanced fab capital equipment, and that these categories directly correlate with their dominant gas consumption positions. Deposition holds the second largest process share at approximately 25%, driven by ALD and CVD deposition gas consumption.

Regional Insights

West U.S. Semiconductor Gases Market Trends

The West U.S. region, centered on California's Silicon Valley, the Portland/Hillsboro, Oregon semiconductor cluster and the rapidly emerging Arizona fab campus hub, leads the U.S. Semiconductor Gases market, anchored by the highest concentration of legacy and newly commissioned advanced semiconductor fabrication facilities in the country. Intel Corporation's semiconductor manufacturing operations in Hillsboro, Oregon (its largest and most advanced global R&D and logic fab complex) and Micron Technology's semiconductor manufacturing presence represent the West U.S.'s long-established industrial gas demand base.

TSMC Arizona's Fab 21 Phase 1 (4nm process, operational in 2024) and Phase 2 (2nm/3nm process, construction ongoing as of 2025) in Phoenix, Arizona, representing over US$ 65 billion in total planned investment, constitute the single most significant new semiconductor gas demand source in U.S. history.

The U.S. EPA's National Emission Standards for Hazardous Air Pollutants (NESHAP) semiconductor fabrication category regulations, which govern PFC (Perfluorocompound) greenhouse gas emissions from semiconductor etch and CVD chamber cleaning processes, apply stringently to all West U.S. fab operations and are driving fab operators to adopt NF remote plasma chamber cleaning systems as the lower-emission alternative to in-situ C-F and CF cleaning processes.

Midwest U.S. Semiconductor Gases Market Trends

The Midwest U.S. region is undergoing the most dramatic semiconductor manufacturing transformation in its industrial history, anchored by Intel's landmark New Ohio One semiconductor fab campus in New Albany, Ohio, representing a planned investment of up to US$ 100 billion over the next decade that will establish Ohio as one of the world's largest semiconductor manufacturing geography clusters outside Taiwan and South Korea.

The U.S. Department of Commerce announced a preliminary CHIPS Act funding agreement with Intel worth US$ 8.5 billion in direct funding for Ohio, Arizona, and New Mexico fab investments in March 2024, confirming the federal government's commitment to Midwest semiconductor manufacturing investment that will generate one of the largest new semiconductor gas demand concentrations in U.S. history as Ohio fab construction phases progress through 2026-2030.

The Ohio Department of Development's JobsOhio semiconductor manufacturing incentive program, which provided co-investment support to attract Intel's New Ohio One commitment, is stimulating a broader semiconductor supply chain ecosystem development in Ohio, Michigan, and Indiana that will generate ancillary semiconductor gas demand from equipment cleaning, materials testing, and semiconductor packaging operations co-locating in the Midwest semiconductor manufacturing hub over the forecast period.

Southwest U.S. Semiconductor Gases Trends

The Southwest U.S. region, encompassing Texas, New Mexico, and Nevada, is the third strategically significant semiconductor gas demand geography in the United States, anchored by Samsung Semiconductor's flagship Taylor, Texas advanced foundry fab investment, representing a planned US$ 17 billion+ investment in a 4nm and below logic foundry operation that received a preliminary US$ 6.4 billion CHIPS Act direct funding agreement from the U.S. Department of Commerce in April 2024, and Texas Instruments' continuous 300mm fab capacity expansion program across Richardson and Dallas, Texas serving analog and embedded semiconductor production.

Texas has become the second-largest state by semiconductor fab investment commitments, after Arizona, with the Texas Economic Development Corporation documenting over US$25 billion in semiconductor manufacturing investment commitments in the state between 2021 and 2025.

Taiyo Nippon Sanso JFP Corporation's U.S. semiconductor gas operations and Electronic Fluorocarbons LLC's specialty ESG supply network are both active in the Southwest U.S. semiconductor gas procurement market, serving Texas fab operations with specialty fluorocarbon etching and chamber cleaning gas supply. Intel's Rio Rancho, New Mexico fabrication facility, one of the company's established U.S. manufacturing sites receiving CHIPS Act investment for capacity modernization, sustains the Southwest U.S.'s established semiconductor gas demand base, with Air Products' on-site bulk gas supply infrastructure at the New Mexico facility serving as a reference deployment model for new Southwest U.S. fab gas supply agreements being developed in conjunction with the Samsung Taylor and expanded Texas Instruments fab programs.

Competitive Landscape

The U.S. Semiconductor Gases market is highly consolidated at the ultra-high-purity bulk gas tier, with Air Products and Chemicals Inc., Messer SE (U.S. operations), and Taiyo Nippon Sanso JFP commanding dominant positions through on-site gas generation infrastructure investments at major U.S. semiconductor fabs, long-term exclusive supply agreements, and SEMI F standard-certified UHP gas distribution systems.

Solvay and Electronic Fluorocarbons LLC lead in specialty fluorocarbon ESG segments. REC Silicon holds a unique domestic silane supply position. Key differentiators include on-site plant co-investment capability, analytical quality traceability infrastructure, CHIPS Act supply chain security credentials, and dedicated semiconductor application engineering teams. Emerging business model trends include green hydrogen co-production integration, digital gas supply monitoring platforms with real-time purity telemetry, and long-term 15-20 year supply agreements with CHIPS Act fab recipients.

Key Developments:

- In March 2025, Air Products and Chemicals Inc. announced a long-term on-site gas supply agreement with TSMC Arizona Fab 21 Phase 2, committing to construct and operate dedicated on-site nitrogen, oxygen, argon, and hydrogen ultra-high-purity generation plants serving the 2nm technology node advanced logic fab commissioned for production ramp beginning 2026.

- In November 2024, REC Silicon ASA announced the restart of its Butte, Montana polysilicon and UHP silane (SiH) gas production facility, directly enabled by U.S. CHIPS Act domestic semiconductor material supply chain investment incentives, positioning it as the only domestic U.S. source of semiconductor-grade silane for CHIPS Act funded fab operators seeking domestic supply chain security for this critical deposition process gas.

- In June 2024, Solvay announced a strategic capacity expansion of its North American specialty Electronic Special Gas (ESG) manufacturing operations, targeting the growing demand for ultra-high-purity NF chamber cleaning gas and advanced fluorocarbon etching gas formulations from newly commissioned and under-construction CHIPS Act-funded advanced semiconductor fab facilities across Arizona, Texas, and Ohio.

Companies Covered in U.S. Semiconductor Gases Market

- Air Products and Chemicals Inc.

- American Gas Products

- Electronic Fluorocarbons LLC

- Gruppo SIAD (Praxair Inc.)

- Iwatani Corporation

- Messer SE and Co. KGaA

- Mitsui Chemicals Inc.

- REC Silicon ASA

- Solvay

- Sumitomo Seika Chemicals Company Ltd.

- Taiyo Nippon Sanso JFP Corporation

Frequently Asked Questions

The U.S. Semiconductor Gases market is estimated to be valued at US$ 1,235.1 Million in 2026 and is projected to reach US$ 2,453.2 Million by 2033, registering a forecast CAGR of 10.3% from 2026 to 2033.

The primary drivers are the CHIPS and Science Act of 2022 committing US$ 52.7 billion in federal investment catalyzing US$ 200+ billion in private fab co-investment at TSMC Arizona, Intel Ohio, Samsung Texas, and Micron facilities.

Bulk Gases lead the Gas Type segment with approximately 62% revenue share in 2026, anchored by nitrogen's documented consumption of 50-100 tonnes per day at advanced 300mm fab operations, the continuous 24/7 purging and inerting requirements of semiconductor fab environments.

West U.S. leads the U.S. Semiconductor Gases market, anchored by TSMC Arizona Fab 21's US$ 65 billion total planned investment in Phoenix, Intel Corporation's Ronler Acres fab complex in Hillsboro, Oregon, Air Products' on-site gas generation infrastructure deployment at both locations.

The most significant opportunity is CHIPS Act on-site gas supply contract capture and next-generation ESG formulation development, with US$ 200 billion in U.S. fab co-investment requiring decade-scale captive gas procurement.

The leading companies include Air Products and Chemicals Inc. (Allentown PA), Messer SE and Co. KGaA (U.S. operations, Pittsburgh PA), Solvay (Electronic Materials, Brussels/U.S.), REC Silicon ASA (Butte MT), Taiyo Nippon Sanso JFP Corporation, Electronic Fluorocarbons LLC, Iwatani Corporation, Sumitomo Seika Chemicals Company Ltd., Mitsui Chemicals Inc., American Gas Products, Linde plc (U.S. operations), and Versum Materials (Merck KGaA).