- Bulk Chemicals

- Middle East Industrial Gases Market

Middle East Industrial Gases Market Size, Share, and Growth Forecast, 2025 - 2032

Middle East Industrial Gases Market By Gas Type (Oxygen, Nitrogen, Others), Application (Metal Manufacturing and Fabrication, Others), Supply Type (Pipeline, Others), and Regional Analysis for 2025 - 2032

Middle East Industrial Gases Market Size and Trends Analysis

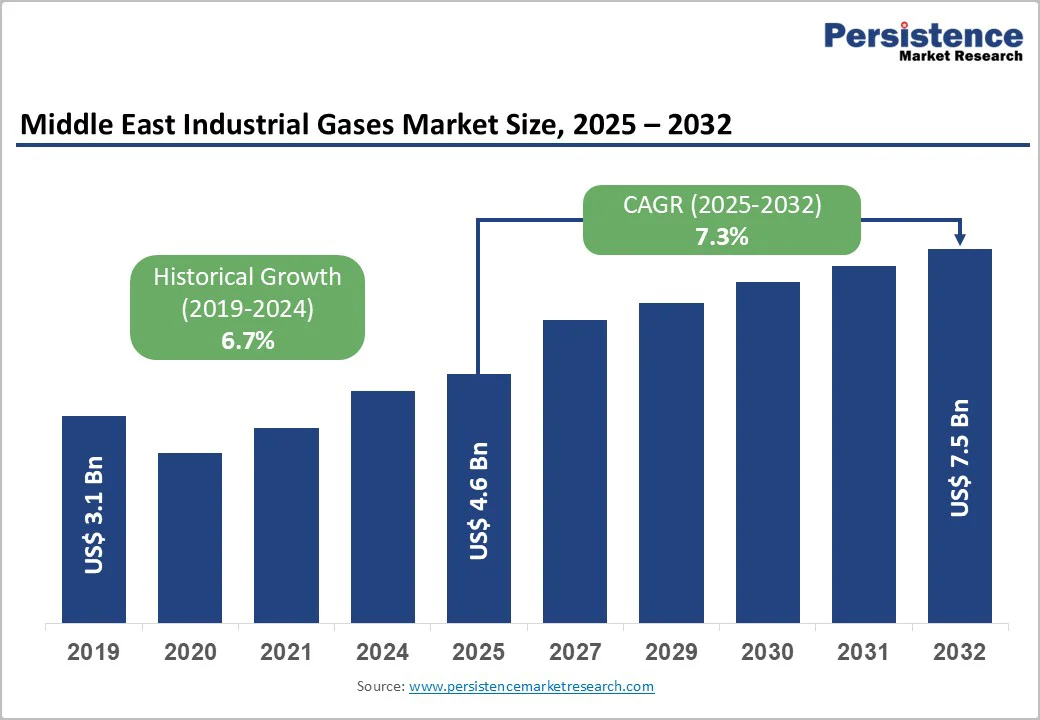

The global Middle East industrial gases market size is likely to be valued at US$4.6 Billion in 2025 and is expected to reach US$7.5 Billion by 2032, growing at a CAGR of 7.3% during the forecast period from 2025 to 2032, driven by petrochemical expansion, large-scale green hydrogen initiatives, and rising healthcare infrastructure needs across GCC countries.

Vision 2030, the UAE Energy Strategy 2050, and landmark projects such as NEOM’s US$8.4 Billion green hydrogen facility are transforming the region into a global clean-energy hub. Post-pandemic healthcare upgrades are also driving higher medical gas consumption, positioning the Middle East as the world’s fastest-growing industrial gases market.

Key Industry Highlights

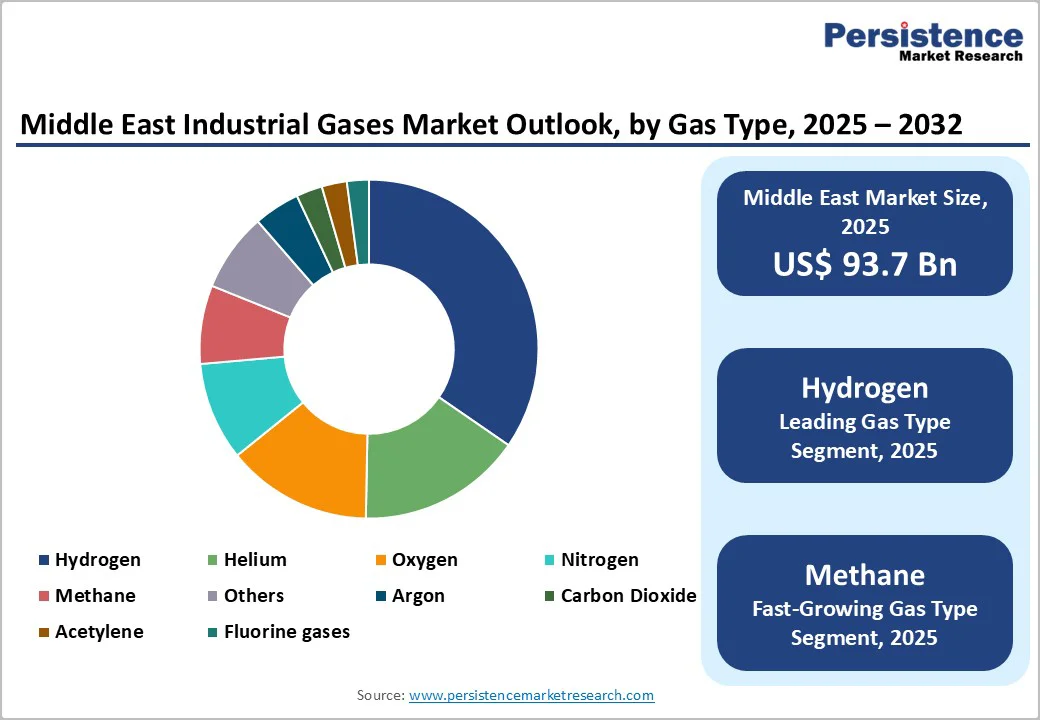

- Dominant and Fastest-growing Gas Type: Hydrogen dominates with 35% market share, supporting petrochemical refining and emerging clean energy applications, while methane demonstrates the highest CAGR growth driven by LNG expansion and power generation demand across Türkiye, the UAE, and Qatar markets.

- Fastest-growing Application Type: Healthcare applications grow at the highest CAGR through 2032, driven by medical oxygen, hospital infrastructure expansion, and aging population demographics across GCC countries.

- Dominant Application Type: Energy, oil, and gas applications maintain 30% market share as the leading segment, while pipeline on-site tonnage supply commands 55% share with cryogenic tanks growing at 7.9% CAGR supporting distributed customer segments.

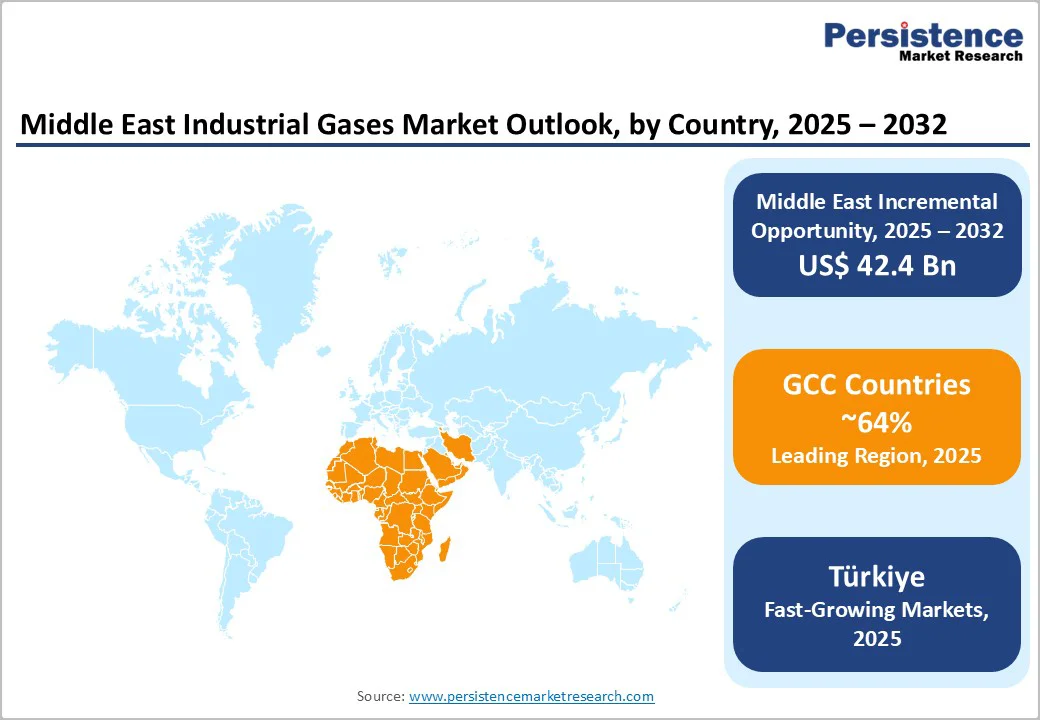

- Leading Country: GCC countries dominate with 64% market share, led by Saudi Arabia (39% share) through Vision 2030 initiatives, UAE (25% share) via technology diversification, and Qatar through massive LNG expansion targeting 142 million tonnes by 2030.

| Key Insights | Details |

|---|---|

| Middle East Industrial Gases Market Size (2025E) | US$4.6 Bn |

| Market Value Forecast (2032F) | US$7.5 Bn |

| Projected Growth CAGR (2025 - 2032) | 7.3% |

| Historical Market Growth (2019 - 2024) | 6.7% |

Market Dynamics Analysis

Growth Analysis - Hydrogen Megaprojects and Petrochemical Expansion

The Middle East industrial gases market is driven by massive hydrogen investments and growing petrochemical and refining capacities, especially in GCC countries. Saudi Arabia’s US$8.4 Billion NEOM Green Hydrogen Project, 80% complete by Q1 2025, will produce 600 t/day of hydrogen and 1.2 Mt/year of green ammonia.

Blue hydrogen projects, including Aramco’s BHIG stake and ADNOC-ExxonMobil collaboration, create integrated hydrogen export corridors. Petrochemical expansions in Saudi Arabia, Qatar, and the UAE, plus projects such as Jafurah gas, North Field LNG, and the US$11 Billion Amiral complex, boost demand for hydrogen, nitrogen, and specialty gases.

Carbon capture plants, such as Kuwait’s EQUATE CO2 facility, further expand industrial gas consumption, establishing the region as a global growth hub.

Accelerating Healthcare Infrastructure Development and Medical Gas Demand

The Middle East healthcare sector is expanding due to an aging population, rising chronic respiratory diseases, and enhanced post-pandemic hospital capacities, boosting demand for medical gases. Saudi Arabia’s US$8 Billion healthcare budget aims to improve care access and quality, particularly in underserved regions.

Medical oxygen demand grows for COPD, asthma, and respiratory treatments, with healthcare as the fastest-growing segment through 2032. Kuwait leads medical gas equipment growth. Post-COVID-19, hospitals maintain oxygen reserves, while advanced concentrators, home healthcare, and portable solutions gain traction. Programs such as Saudi Arabia’s National Health Transformation further drive consumption alongside industrial use.

Barrier Analysis - High Capital Expenditure Requirements and Energy-Intensive Production Processes

Industrial gas production in the Middle East requires massive capital investments, creating entry barriers and limiting geographic expansion. Infrastructure such as air separation units, cryogenic storage, and specialized transport demands multi-million-dollar commitments with long payback periods.

Large projects, such as Air Products’ Quadra hub, involve hundreds of millions in investment. High energy use and operational costs, plus depreciation, maintenance, and workforce expenses, challenge smaller suppliers. Multinationals such as Linde, Air Liquide, and Air Products dominate 70-75% of the market, reinforcing structural barriers and constraining competition and innovation.

Regulatory Compliance Complexity and Environmental Standards Harmonization

Middle East industrial gas manufacturers face complex regulations affecting production, storage, transport, and environmental compliance. Adhering to EH&S standards is estimated to reduce CAGR by 0.7%, requiring investments in monitoring systems, safety equipment, and training. Strict medical gas purity standards and hazardous materials rules increase costs and limit supply chain flexibility.

Regulatory differences across GCC countries, Egypt, and Türkiye demand tailored strategies, while carbon emission rules require short-term investments. Crude oil price volatility further restrains CAGR by 0.5%. These layered compliance burdens hinder market expansion and innovation, especially for smaller firms lacking regulatory expertise.

Opportunity Analysis - Carbon Capture, Utilization, and Storage (CCUS) Technology Deployment

The Middle East’s carbon neutrality goals are driving major opportunities for industrial gas suppliers through large-scale CCUS projects. ADNOC’s Hail and Ghasha uses Linde’s HISORP® technology to capture 1.5 million tonnes of CO2 annually, while Saudi Aramco’s Jubail CCS hub centralizes carbon management across multiple facilities, boosting demand for CO@ compression, transport, and injection.

Gulf Cryo aims to quadruple CO2 capture in Kuwait by 2030. Integration with blue hydrogen production enhances value chains, requiring oxygen, nitrogen, and specialty gases. Government incentives, emissions regulations, and corporate sustainability targets accelerate CCUS adoption, enabling suppliers to secure long-term partnerships and premium applications in decarbonization markets.

Semiconductor Manufacturing and Advanced Electronics Expansion

The Middle East’s push into semiconductors and advanced electronics drives high-purity specialty gas demand. Saudi Arabia’s Vision 2030 expands semiconductor fabs needing ultra-pure nitrogen, hydrogen, and specialty gases for etching, deposition, and doping. The UAE tech parks and US$100 Billion AI initiatives support electronics manufacturing and data centers requiring reliable gas supplies for cooling and environmental control.

Nikkiso’s 2025 Qatar service center highlights regional investment. Emerging LED, solar, and display facilities diversify demand beyond petrochemicals. Suppliers that deliver high purity and reliable supply benefit from stronger pricing power, while government incentives, infrastructure development, and collaborations with global technology firms further expand long-term opportunities across specialty gas value chains.

Category-wise Analysis

Gas Type Insights

Hydrogen holds a dominant 35% share in the Middle East industrial gases market, driven by petrochemical refining, enhanced oil recovery, and emerging clean energy projects. Concentrated refining capacities in Saudi Arabia, the UAE, and Kuwait sustain hydrogen demand for hydro-treating, sulfur removal, and fuel production aligned with international environmental standards.

Major projects such as Saudi Arabia’s Jafurah gas field and Qatar’s North Field LNG expansion require substantial hydrogen for gas processing and purification. The region leverages abundant natural gas for blue hydrogen and renewable energy for green hydrogen, providing structural advantages.

NEOM’s 600 tonnes/day hydrogen production and Aramco’s BHIG facility illustrate large-scale commercial deployment, supporting both domestic consumption and export ambitions.

Methane represents a key growth segment, driven by power generation, petrochemical feedstock, and LNG production. The UAE aims for gas self-sufficiency by 2030, while Türkiye’s daily gas consumption reached 333.7 million cubic meters in February 2025, supported by grid expansion to 913 districts and plans for 134 more by 2026.

Qatar’s LNG leadership, with output projected at 142 million tonnes by 2030, further fuels methane processing and distribution infrastructure development. Combined, hydrogen and methane dominate market dynamics, reflecting the region’s strategic role in energy, industrial applications, and global gas supply chains.

Application Insights

Energy, oil, and gas applications dominate the Middle East industrial gases market, accounting for 30% of total demand, reflecting the region’s abundant hydrocarbon resources and concentrated petrochemical industry. Major players such as Saudi Aramco, ADNOC, and Qatar Petroleum consume large volumes of hydrogen, nitrogen, and oxygen for catalytic processes, inerting, and enhanced oil recovery.

Upstream operations employ nitrogen for pressure maintenance, hydrogen for hydrocracking, and CO2 for EOR, while the continuous expansion of separation plants by Saudi Aramco and ADNOC ensures a sustained supply.

Midstream LNG facilities rely on specialty gases for purification, compression, and transportation, with ongoing projects such as Jafurah and North Field LNG trains reinforcing baseline industrial gas demand alongside emerging energy transition applications.

Healthcare applications show robust growth, driven by healthcare infrastructure modernization, aging populations, and rising chronic respiratory diseases. Medical oxygen dominates with a 53.2% share, critical for surgeries, respiratory care, and emergencies. Saudi Arabia’s healthcare budget has increased by 21% year-over-year, while the UAE expands advanced hospital networks.

Kuwait leads regional growth for medical gas equipment, supported by accessibility initiatives and tertiary care center development. Post-pandemic oxygen demand remains elevated as health systems maintain enhanced emergency preparedness and respiratory therapy infrastructure, sustaining long-term medical gas consumption growth.

Supply Mode Analysis

Pipeline supply and on-site tonnage generation account for 55% of the Middle East industrial gases market, offering cost-effective, reliable delivery to large industrial customers requiring high-volume, consistent supplies. This mode dominates major petrochemical facilities, refineries, and steel manufacturers in industrial hubs such as Jubail, Yanbu, Ruwais, and Ras Laffan.

Saudi Arabia’s integrated petrochemical clusters and extensive pipeline networks reduce distribution costs and support investment in cryogenic air separation units. On-site generation enhances supply security, lowers logistics costs, and reduces emissions, driving adoption among large-scale manufacturing operations.

ADNOC Industrial Gas operates advanced facilities at Al Ruwais Industrial City and Mirfa, producing gaseous and liquid nitrogen, liquid oxygen, and specialty products delivered via dedicated pipeline networks.

Cryogenic tank and liquid dewar distribution is projected to grow at the highest CAGR through 2032, serving smaller industrial clients, healthcare facilities, distributed manufacturing, and remote sites lacking on-site generation. This flexible delivery mode enables market access across hospitals, clinics, food processing, and small-scale manufacturing.

Expansion of healthcare infrastructure in secondary cities and remote regions fuels cryogenic demand, particularly for specialty gases. Gulf Cryo’s regional network, spanning 10 countries with 20+ sites, exemplifies extensive coverage, supporting cryogenic operations across diverse customer segments and geographies, reinforcing market penetration where pipeline infrastructure is economically unfeasible.

Regional Market Insights

GCC Countries (Saudi Arabia, UAE, and Qatar)

GCC countries dominate the Middle East industrial gases market with a 64% share and a projected 7.8% CAGR through 2032, driven by petrochemical industry concentration, clean energy investments, and healthcare infrastructure development. Saudi Arabia maintains a leading position in the Middle East industrial gases market, supported by its concentrated petrochemical and refining clusters in Jubail and Yanbu industrial cities.

Large pipeline networks across Saudi industrial cities reduce distribution costs and support ongoing cryogenic air separation unit investments. The UAE holds ~16% Middle East market share through 2032, driven by ADNOC's gas processing expansion, technology park development, and advanced healthcare infrastructure.

Qatar focuses on LNG and petrochemicals, with North Field output targeting 142 million tonnes by 2030, creating substantial nitrogen, hydrogen, and specialty gas requirements for supporting infrastructure.

GCC regulatory frameworks foster economic diversification beyond oil, improving the investment climate for industrial gas suppliers. Initiatives such as Saudi Arabia's NIDLP and IKTVA encourage local gas production, enhancing supply chain resilience. Strategic free zones and advanced port infrastructure attract international investments in the UAE and Qatar.

A regional focus on sustainability promotes projects in carbon capture, green hydrogen, and clean energy, creating opportunities for specialty gas suppliers. Investment trends highlight long-term supply agreements and partnerships that integrate gas supply with carbon management, supporting regional decarbonization and net-zero goals.

Egypt

Egypt holds 13% Middle East industrial gases market share, supported by chemical sector growth, healthcare infrastructure expansion, and food processing industry development. The industrial gases market in Egypt demonstrates significant growth potential driven by economic diversification initiatives and manufacturing sector expansion.

The chemicals/refining sector grows at a 6.8% CAGR, creating sustained hydrogen, nitrogen, and carbon dioxide demand for gasification, refining, and synthesis processes. The government establishment of the National Chemicals and Petrochemicals Company oversees sector development with tax incentives and subsidies supporting new project investments.

Food processing industry growth targeting US$25.6 Billion by 2026 drives industrial gas demand for carbonation, modified atmosphere packaging, and food preservation applications, supporting food security objectives.

Egyptian Organization for Standardization and Quality (EOS) establishes production and distribution standards ensuring medical gases meet quality and safety requirements. Government policies promoting local medical gas production reduce import dependence, with Egypt representing one of the world's largest medical gas importers, creating substantial localization opportunities.

M&A activity surged with 86 deals in H1 2025 compared to 48 in the same period in 2024, supported by IMF programs and Gulf investments alongside 3.8% GDP growth expectations, creating a favorable investment climate for industrial gas sector expansion and infrastructure development across Egyptian manufacturing and healthcare markets.

Türkiye

Türkiye demonstrates prominent growth momentum, positioning as the fastest-growing non-GCC Middle East market despite GCC countries maintaining overall regional leadership. Türkiye's industrial gas market is driven by healthcare expansion, manufacturing growth, and energy sector development. Industrial production index rose 2.9% year-over-year in September 2025, reflecting manufacturing sector strength supporting industrial gas demand.

Automotive manufacturing represents the largest export sector, with Türkiye's strategic position in European and Middle Eastern supply chains creating substantial nitrogen and hydrogen demand for metallurgy and welding applications.

The healthcare sector demonstrates robust oxygen and medical gas demand growth through hospital infrastructure investment and private healthcare facility expansion. Government infrastructure projects, transportation development, and construction initiatives increase demand for welding and cutting industrial gases across civil engineering applications.

Türkiye's energy hub ambitions drive industrial gas consumption across refining and petrochemical production, with natural gas demand reaching a record 333.7 million cubic meters daily in February 2025. Gas transmission system expansion, increasing import capacity to 75-80 billion cubic meters annually, exceeds domestic demand of 50 billion cubic meters, positioning Türkiye as a potential regional distribution hub.

Electronics manufacturing growth creates high-purity nitrogen and argon demand, supporting semiconductor and technology production. Renewable energy sector expansion, including solar and wind installations, drives specialty gas requirements for manufacturing and maintenance processes.

Competitive Landscape

The Middle East industrial gases market is moderately to highly consolidated, with Linde, Air Liquide, and Air Products jointly controlling 70-75% of the regional share through advanced technologies, extensive production networks, and decades of operational presence.

Regional players such as Gulf Cryo and ADNOC Industrial Gas enhance competitive depth with strong localized operations, sector-focused solutions, and established relationships across oil and gas, healthcare, and industrial customers. This structure supports premium pricing for commodity gases while enabling healthy competition in specialty gas segments.

Companies Covered in Middle East Industrial Gases Market

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- Gulf Cryo Holding CSC

- ADNOC Industrial Gas

- Praxair Technology Inc.

- Messer SE & Co. KGaA

- Air Water Inc.

- Taiyo Nippon Sanso Corporation

- Iwatani Corporation

- INOX-Air Products Inc.

- Nikkiso Clean Energy & Industrial Gases Group

- Abdullah Hashim Industrial Gases (AHG)

- Buzwair Industrial Gases

- National Industrial Gas Plants (NIGP)

Frequently Asked Questions

The Middle East industrial gases market was valued at US$4.6 Billion in 2025 and is projected to reach US$7.5 Billion by 2032.

The Middle East industrial gases market is driven by massive green and blue hydrogen infrastructure investments, petrochemical sector expansion, and accelerating healthcare infrastructure development.

The Middle East industrial gases market is projected to grow at a 7.3% CAGR during the forecast period.

Key market opportunities include carbon capture and storage technology deployment, semiconductor manufacturing and advanced electronics expansion, on-site generation systems and digitalization integration, and green hydrogen export infrastructure development.

The key market players include Linde plc, Air Liquide, Air Products and Chemicals, Gulf Cryo, ADNOC Industrial Gas, Praxair (merged with Linde), Messer SE, and Air Water Inc.