ID: PMRREP13075| 279 Pages | 21 Dec 2025 | Format: PDF, Excel, PPT* | Chemicals and Materials

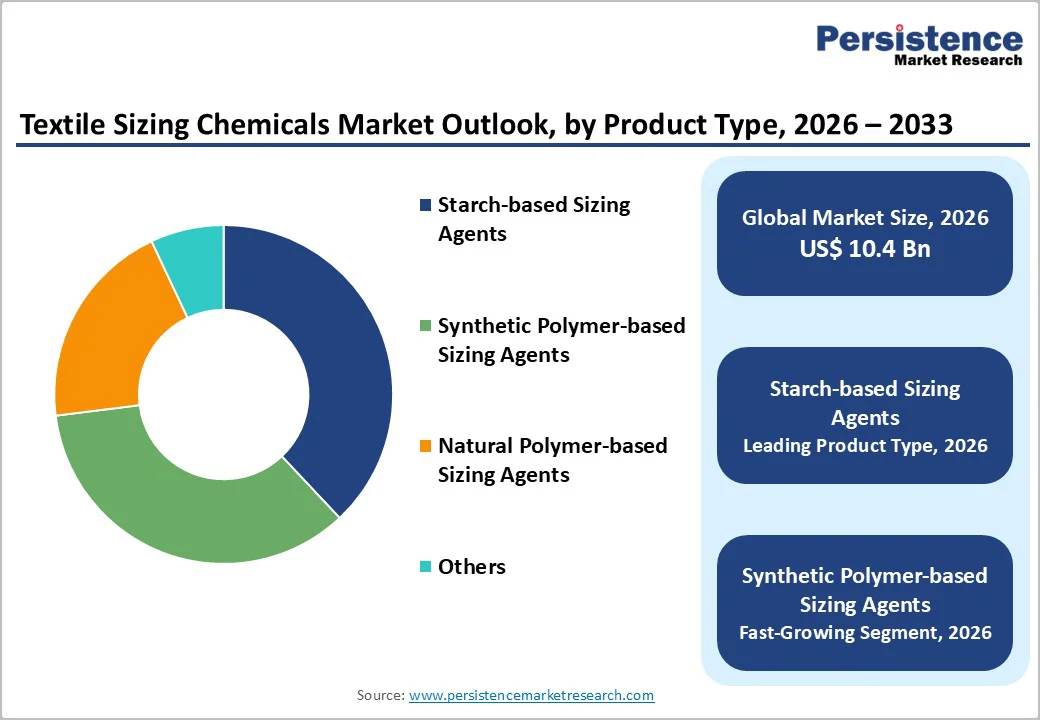

The global textile sizing chemical market size is likely to be valued at US$ 7.6 billion in 2026, and is projected to reach US$ 10.4 billion by 2033, growing at a CAGR of 4.6% during the forecast period 2026-2033. This steady expansion reflects sustained demand across key end-use sectors, including apparel manufacturing, home textiles, and the rapidly evolving technical textiles industry. Rising textile production volumes in emerging economies are creating sustained requirements for sizing solutions that enhance yarn strength, reduce breakage during weaving, and improve overall fabric quality. The growing preference for high-performance yarns in demanding applications further drives adoption of advanced sizing formulations that deliver superior adhesion, lubrication, and abrasion resistance throughout the manufacturing process. Modernization of cotton and blended-yarn production facilities globally is broadening the addressable market for both starch-based and synthetic sizing chemicals, each offering distinct performance and cost profiles suited to different manufacturing environments. Increasing fabric processing volumes reflect broader industrialization trends and rising consumer demand for diverse textile products across residential, commercial, and industrial applications

| Key Insights | Details |

|---|---|

| Textile Sizing Chemicals Market Size (2026E) | US$ 7.6 Bn |

| Market Value Forecast (2033F) | US$ 10.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Rising Demand from Apparel, Home, and Technical Textile Industries

Growing consumption of apparel and home textiles continues to elevate the need for efficient warp preparation and high-quality weaving, driving strong demand for textile sizing chemicals. Mills increasingly rely on starch-based and synthetic polymer agents to improve yarn strength, reduce breakage, and ensure consistent fabric output. To enhance operational efficiency, manufacturers are adopting advanced solutions such as Zydex Group’s nano-sized water-soluble polyester resins, which offer superior film formation and abrasion resistance. Sustainability expectations are also shaping demand, with bio-based, biodegradable options. These innovations support both traditional fabric production and the shift toward cleaner, more resource-efficient manufacturing.

Simultaneously, the rapid expansion of technical textiles in automotive, medical, construction, and protective applications is strengthening the market need for high-performance sizing technologies. These segments require specialized yarns with exceptional durability, driving adoption of nanomaterial-enhanced coatings that improve abrasion resistance and stability. Eco-friendly advancements such as Zydex’s bio-eliminable PVA alternatives (siZaltex LVn) further support high-speed weaving and low-energy desizing while reducing wastewater impact. Industry-wide transitions to safer chemical systems, including PFAS-free ranges promoted by leading chemical suppliers, reinforce long-term demand. Together, these developments ensure sustained growth across diversified textile manufacturing environments.

Raw Material Volatility and Regulatory Challenges

Fluctuating prices of key raw materials, particularly petroleum-based feedstock for synthetic sizing agents, pose significant challenges to manufacturers. Volatile input costs and supply chain disruptions create uncertainty in procurement and production planning, which can lead to margin pressures and affect the competitiveness of synthetic polymer sizing chemicals. Smaller manufacturers are especially vulnerable, as limited financial flexibility makes it harder to absorb cost swings, maintain stable pricing, or secure consistent raw material supply. These factors collectively constrain production scalability and operational efficiency across the sector.

Stringent environmental regulations and chemical safety standards are added limitations on the textile sizing chemicals market growth, since they require manufacturers to invest in compliance measures, including wastewater treatment and product reformulation. The associated costs and technical complexity can limit adoption of advanced sizing chemicals, particularly among smaller or regional producers. Balancing regulatory compliance with cost-effectiveness remains a critical challenge, potentially slowing market expansion. Combined, these pressures create structural obstacles that manufacturers must navigate to sustain growth and remain competitive.

Advent of Eco-Friendly and Innovative Sizing Solutions

The accelerating sustainability shift in textiles is creating a high-value investment opportunity for eco-friendly and biodegradable sizing chemicals. Natural polymer-based and water-soluble agents help mills reduce environmental impact, meet rising regulatory expectations, and appeal to eco-driven global brands, making them increasingly preferred in sourcing strategies. Even a 10–20% transition to green sizing solutions represents significant volume expansion for manufacturers. This momentum is strengthened by industry leaders such as Archroma, Clariant, and Huntsman, who have already introduced PFAS-free chemical ranges, signaling a broader move toward safer and compliant chemistry. Together, these developments position sustainable sizing technologies as strategic, future-ready growth assets for investors targeting long-term market value.

Rapid expansion of textile manufacturing in Asia Pacific, including India, China, Bangladesh, and Vietnam, further enhances the investment potential of advanced sizing solutions. These regions benefit from rising production volumes, cost-competitive operations, and supportive policy frameworks that elevate demand for both traditional and next-generation sizing chemicals. Strong opportunities lie in multifunctional and smart formulations offering lubricity, antistatic performance, easy wash-off, and compatibility with technical and digital textiles. As demand grows for medical, protective, and high-performance fabrics, investors stand to gain from technologies that combine productivity, sustainability, and superior weaving efficiency.

Starch-based sizing agents are likely to lead the market with around 38.6% share, supported by their low cost, easy processing, and strong penetration in traditional textile mills that rely on economical warp preparation. Their compatibility with cotton yarns and widespread machinery setups reinforces dominance, especially in regions where cost-efficiency shapes procurement preferences. The segment also benefits from long-standing operational familiarity, making it the default choice for mills seeking proven and stable sizing performance. Recent innovations such as Alpenol’s GOTS-certified biodegradable starch sizing further strengthen this segment by combining cost-efficiency with environmental compliance.

Synthetic polymer-based agents represent the fastest-growing segment, likely to expand at an estimated 6.2% CAGR from 2026 to 2033, driven by high-speed weaving, superior film strength, and consistent performance. Their ease of desizing, reduced wastewater load, and compatibility with synthetic and blended yarns further accelerate adoption. Demand is reinforced by modern weaving setups requiring uniform coating and minimal breakage. Natural polymer-based agents show niche growth tied to sustainability adoption.

Cotton fibers are expected to hold the leading position with an estimated 45% of the textile sizing chemicals market revenue share in 2026, owing to their dominant use across global apparel and home textiles. Cotton yarn requires sizing for warp strengthening, making it a significant consumer of starch-based and PVA-based agents. The established global cotton value chain, large spinning capacities, and compatibility with conventional sizing formulations reinforce its leading status. Cotton’s broad application in shirts, denim, bedding, and woven garments ensures ongoing demand for sizing chemicals. Eco-friendly and certified products, such as Amchem’s Supersize, ensure that even conventional cotton yarn processing meets stricter environmental and regulatory requirements while maintaining weaving efficiency. Despite diversification in fiber use, cotton remains foundational in numerous textile clusters worldwide.

Synthetic fibers, including polyester and nylon, represent the fastest-growing segment, estimated to showcase a 6.5% CAGR between 2026 and 2033, supported by their rising adoption in sportswear, athleisure, and technical textiles. The increasing use of blended yarns further boosts demand for sizing solutions optimized for synthetic performance. High-speed weaving, superior durability needs, and lower processing costs reinforce growth. Blended fibers also gain traction as manufacturers pursue material optimization and performance improvements.

The apparel/garments segment is poised to lead the market with approximately 52% revenue share, fueled by the consistently high and varied demand for fashionable garments, everyday wear, and mass-market clothing across the globe. Strong production volumes in woven apparel categories drive consistent consumption of sizing chemicals for warp preparation. Growth in e-commerce, fast fashion cycles, and rising disposable incomes across emerging economies further support steady demand. Apparel manufacturing hubs in Asia continue to underpin market dominance due to large-scale output and cost-efficient processes. Home textiles contribute additional stable consumption, complementing apparel-driven volume.

Industrial and technical textiles form the fastest-growing segment, anticipated to exhibit an approximate 7.1% CAGR from 2026 to 2033, driven by their wide applicability in automotive, medical, filtration, geotextiles, and protective fabrics. These sectors require precise yarn performance, high tensile strength, and specialized coatings, boosting demand for advanced synthetic and functional sizing agents. Increasing investments in high-performance materials and technical textile parks reinforce growth. The segment also benefits from global shifts toward durable, engineered, and application-specific fabrics.

North America is set to hold a 22% share, led by the U.S., and represents a stable and mature market supported by advanced textile manufacturing and strong adoption of technical textiles. Strict environmental and chemical safety standards drive steady use of low-impact and high-performance sizing chemicals, creating demand for eco-efficient formulations. The regional market benefits from a strong innovation ecosystem where chemical companies invest in modernizing sizing solutions and improving environmental compliance. High labor and operational costs moderate growth but emphasize quality-driven production. Manufacturers increasingly prioritize productivity enhancements and sustainable chemistry aligned with regulatory expectations.

The textile sizing chemicals market growth in North America is predicted to remain moderate at an estimated 3.2% CAGR, supported by technical textiles used in automotive, filtration, and protective applications. While the region does not compete with Asia Pacific on volume, it leads in premium, high-specification textile segments requiring precision sizing solutions. The market structure is moderately consolidated, with producers serving specialized apparel and industrial textile manufacturers.

Europe is expected to account for approximately 24% of the textile sizing chemicals market share in 2026, shaped by rigorous chemical regulations and a high preference for quality-focused textile production. The region’s strong sustainability framework pushes mills toward bio-based, natural polymer, and low-impact synthetic sizing agents despite higher costs. Textile clusters in Germany, Italy, France, and the U.K. maintain consistent demand for sizing chemicals used in apparel, technical fabrics, and industrial textiles. Harmonized environmental standards across the European Union (EU) have accelerated the shift toward eco-friendly solutions and wastewater-efficient processes. Rising adoption of advanced weaving technologies further supports the use of reliable, high-performance sizing agents.

The Europe market is foreseen to grow steadily during the 2026-2033 forecast period, on account of the wide deployment of technical textiles for medical, automotive, and protective applications. Although fiber and yarn production expands slowly, as compared to Asia Pacific. Europe also leads in innovation, precision performance, and premium-grade chemical formulations. Competitive dynamics include large industrial chemical producers and specialty suppliers actively investing in R&D to meet stringent compliance norms.

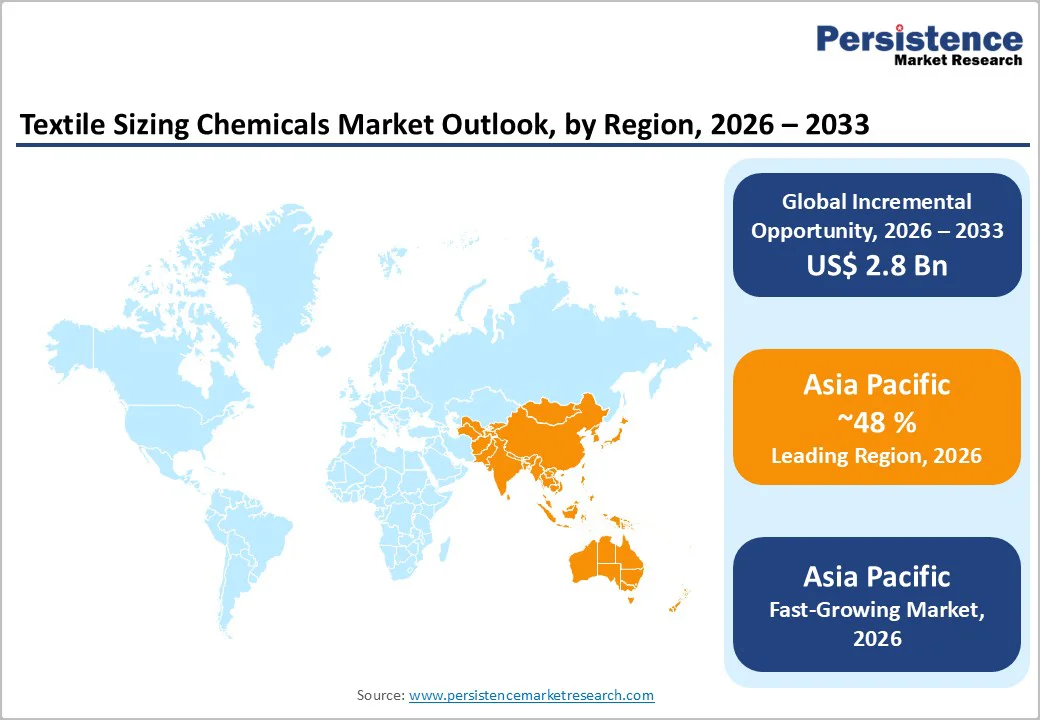

Asia Pacific is projected to be both the largest and fastest-growing regional market, accounting for about 48% share in 2026, driven by the deeply-entrenched presence of massive textile manufacturing hubs in China, India, and Bangladesh. Cost-efficient labor, abundant raw materials such as cotton and starch, and pro-manufacturing policies underpin large-scale textile output and high consumption of sizing chemicals. Rapid expansion of apparel exports, home textiles, and synthetic fiber production strengthens demand for starch-based and synthetic polymer-based agents. The region’s manufacturing scale, integrated supply chains, and growing investment in modern weaving technologies reinforce its market leadership.

The Asia Pacific market is anticipated to grow at an estimated 6.8% CAGR through 2033, supported by rising domestic consumption, export competitiveness, and gradual adoption of sustainable sizing solutions. While traditional chemicals remain dominant due to cost sensitivity, environmental reforms are accelerating the shift toward eco-friendly, low-impact formulations. The landscape is fragmented with numerous local and international suppliers, creating opportunities for capacity expansion, backward integration, and commercialization of greener sizing technologies.

The global textile sizing chemicals market landscape is moderately competitive, characterized by a mix of global chemical manufacturers and strong regional players supporting large-scale textile hubs. Leading companies such as BASF, Dow, Archroma, Bozzetto Group, Pulcra Chemicals, Avebe, and Solvay maintain significant influence through advanced formulation capabilities, broad product portfolios, and deep technical expertise. These players offer a wide range of starch-based, synthetic polymer-based, and natural polymer-based sizing solutions tailored for cotton, synthetic, and blended yarns. Their competitiveness is strengthened by investments in eco-friendly formulations, high-performance agents for high-speed weaving, and solutions aligned with global sustainability and wastewater compliance standards.

Complementing these leaders, regional manufacturers across Asia Pacific, including firms in China, India, and Southeast Asia, are expanding rapidly by leveraging cost-efficient production, proximity to large textile clusters, and the ability to customize formulations based on mill-specific requirements. These companies supply economical traditional starch-based agents as well as increasingly competitive synthetic polymer alternatives. Growing demand for apparel, home textiles, and industrial fabrics continues to intensify competition, pushing manufacturers to innovate in biodegradable sizing agents, low-BOD formulations, and smart multifunctional coatings. As textile mills modernize and sustainability pressures rise, competitive differentiation will center on performance efficiency, environmental compliance, and integrated technical service support.

The global textile sizing chemicals market is projected to reach US$ 7.6 billion in 2026.

Rising fabric production across Asia, increased demand for high-performance synthetic and blended yarns, technological improvements in sizing formulations, and industry-wide shifts toward eco-friendly and biodegradable sizing chemistries are driving the market.

The market is poised to witness a CAGR of 4.6% between 2026 and 2033.

Significant opportunities exist in bio-based and biodegradable sizing agents, synthetic sizing formulations compatible with high-speed looms, and demand growth across technical textiles, medical fabrics, and performance apparel.

Archroma, BASF SE, Huntsman Corporation, Evonik Industries AG, Solvay S.A., Lanxess AG, Omnova Solutions, and Govi N.V. are some of the key players in the market.

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2020 - 2025 |

| Forecast Period | 2026 - 2033 |

| Market Analysis | Value: US$ Bn |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Product Type

By Fiber/Yarn Type

By End-Use Industry

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author