- Medical Devices

- Latin America Medical Gloves Market

Latin America Medical Gloves Market Size, Share, and Growth Forecast, 2026 - 2033

Latin America Medical Gloves Market by Product Types (Examination Gloves, Surgical Gloves), End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers), and Country Analysis for 2026 - 2033

Latin America Medical Gloves Market Size and Trends Analysis

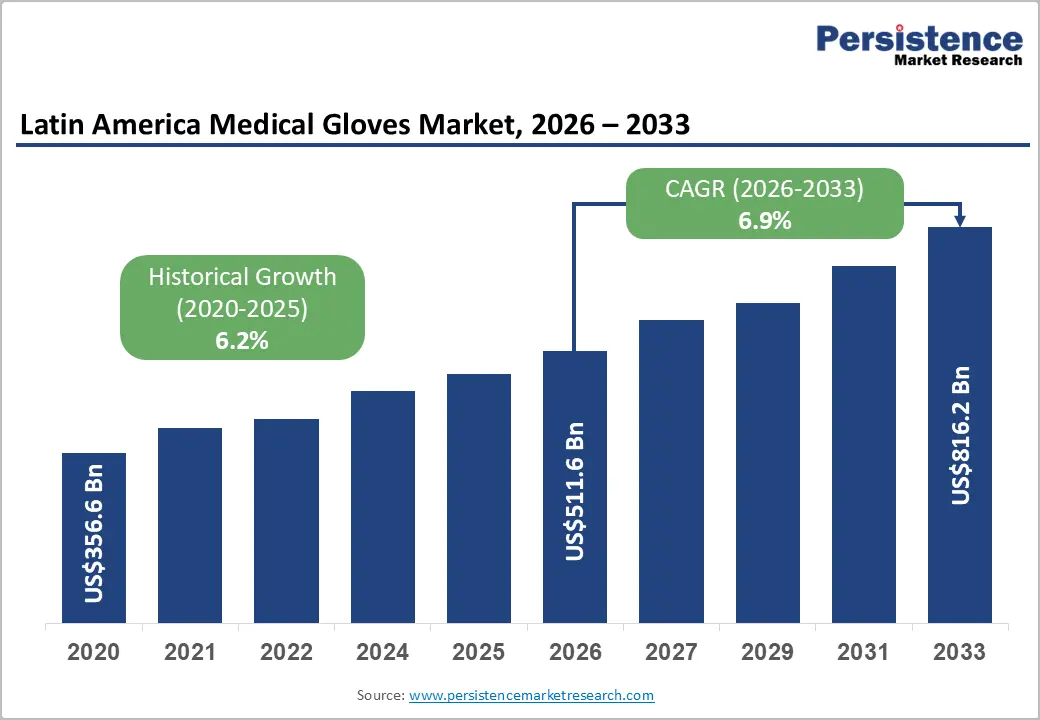

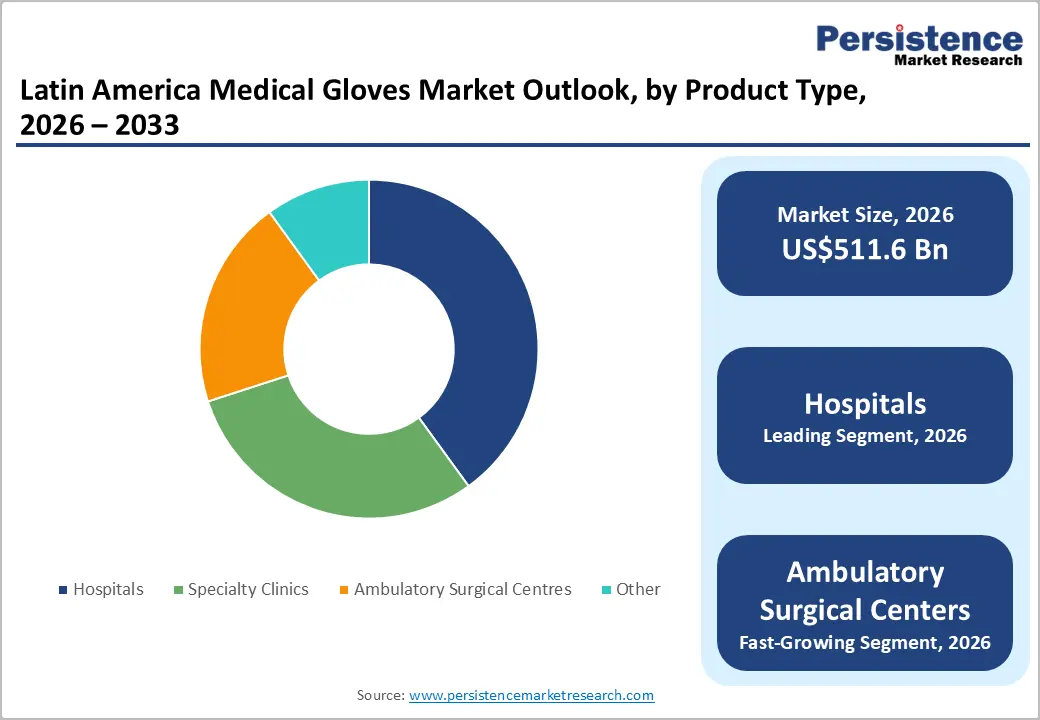

The Latin America medical gloves market size is likely to be valued at US$511.6 million in 2026 and is expected to reach US$816.2 million by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by increasing emphasis on infection prevention, rising surgical and diagnostic procedures, and expanding healthcare infrastructure across Brazil, Mexico, and Argentina.

According to the World Health Organization (WHO) 2025 infection prevention updates, healthcare-associated infections remain a major challenge globally, with up to 15% of hospitalized patients in low- and middle-income countries affected, accelerating demand for protective medical consumables such as gloves. The Pan American Health Organization (PAHO) highlighted in 2026 that the continuous availability of personal protective equipment (PPE) in healthcare facilities remains a critical regional healthcare priority.

Growing investments in public healthcare programs and the expansion of ambulatory surgical centers across Latin America are strengthening demand for disposable examination and surgical gloves.

Key Industry Highlights:

- Leading Region: Brazil is anticipated to lead the market, accounting for a market share of 38% in 2026, driven by its advanced healthcare infrastructure, rising surgical procedures, and strong infection prevention practices.

- Fastest-growing Region: Mexico is likely to be the fastest-growing, due to expanding healthcare access, growing medical manufacturing activities, and increasing demand for protective medical products.

- Leading Product Type: Examination gloves are anticipated to hold 72% market share in 2026, due to their extensive use in routine examinations and infection prevention practices.

- Leading End-user: Hospitals are estimated to hold 58% market share in 2026, owing to high patient volumes and stringent hygiene standards.

- Opportunity: The key market opportunity in the Latin America medical gloves market lies in expanding demand for sustainable nitrile and powder-free gloves driven by improving healthcare infrastructure, rising infection control standards, and increasing outpatient and surgical procedures across the region.

DRO Analysis

Driver - Rising Prevalence of Chronic Diseases and Surgical Procedures

Conditions such as diabetes, cardiovascular disorders, cancer, and respiratory diseases require continuous diagnostic testing, surgical interventions, and patient monitoring, increasing glove consumption in hospitals and clinics. Countries including Brazil and Mexico are witnessing rising hospital admissions and expanding healthcare access programs, supporting procedural volumes. Healthcare professionals rely heavily on examination and surgical gloves to maintain hygiene standards and prevent healthcare-associated infections.

Growing awareness regarding infection prevention, combined with post-pandemic emphasis on personal protective equipment, continues to strengthen long-term demand for disposable medical gloves across regional healthcare systems. The growing number of surgical procedures performed across Latin America is accelerating market expansion for medical gloves.

Increasing aging populations, trauma cases, orthopedic surgeries, cosmetic procedures, and minimally invasive treatments are generating higher consumption of sterile gloves in operating environments. Public and private healthcare investments are improving surgical infrastructure and expanding ambulatory surgical centers throughout the region. Hospitals continue adopting stricter infection control standards to reduce contamination risks during medical procedures.

Restraint- Raw Material Price Volatility and Supply Chain Dependencies

Manufacturers and distributors face difficulties maintaining stable pricing due to variations in petroleum costs, rubber production, transportation expenses, and currency fluctuations. Most Latin American countries depend heavily on imported goods and raw materials from Asian manufacturing hubs, increasing exposure to international trade disruptions and logistics challenges. Supply chain dependencies continue to create operational challenges for the regional medical gloves industry, particularly during periods of global healthcare emergencies and trade instability.

Delays in shipping, port congestion, limited manufacturing capacities, and geopolitical uncertainties can affect the availability of essential medical consumables throughout Latin America. Healthcare institutions increasingly require uninterrupted glove supplies to maintain infection prevention standards, yet import reliance exposes markets to shortages and delayed deliveries. Smaller healthcare facilities and rural clinics are especially vulnerable to fluctuating supply conditions and higher procurement costs.

Opportunity - Innovation in Sustainable and Specialized Gloves

Healthcare providers are increasingly focusing on environmentally responsible procurement practices, encouraging demand for biodegradable, recyclable, and eco-friendly glove materials. Manufacturers are investing in advanced production technologies that reduce chemical usage, improve waste management, and lower environmental impact during glove manufacturing processes. Rising sustainability awareness among healthcare institutions and regulatory authorities is supporting the adoption of greener protective equipment solutions.

Companies introducing sustainable nitrile and latex alternatives may strengthen competitive positioning while addressing environmental concerns associated with disposable medical products across hospitals, laboratories, and ambulatory healthcare facilities in the region. The development of specialized medical gloves designed for enhanced protection, comfort, and procedural efficiency is creating additional market growth opportunities across Latin America.

Advanced gloves offering improved chemical resistance, antimicrobial coatings, textured grip surfaces, and hypoallergenic properties are gaining increasing attention among healthcare professionals. Demand for premium nitrile gloves continues to rise due to their superior durability and reduced allergy risks compared to conventional latex products. Technological advancements supporting thinner yet stronger glove materials are improving user comfort during prolonged medical procedures.

Category-wise Analysis

Product Type Insights

Examination gloves are projected to hold approximately 72% of the market revenue share in 2026, driven by their widespread use across hospitals, diagnostic laboratories, specialty clinics, and ambulatory care centers. These gloves play a critical role in routine patient assessments, diagnostic testing, specimen collection, and infection control measures, making them indispensable in daily healthcare practices. For instance, large hospital networks in Brazil are increasingly adopting nitrile examination gloves to strengthen infection prevention protocols and minimize the risk of latex-related allergies among healthcare workers and patients, particularly in high-volume clinical environments.

Surgical gloves are likely to represent the fastest-growing segment in 2026, supported by rising surgical procedures, expanding operating room capacities, and increasing demand for sterile protective equipment. These gloves are specifically designed to provide enhanced precision, sensitivity, and barrier protection during complex medical procedures, making them critical in surgical environments. Growth in chronic diseases, trauma cases, orthopedic surgeries, cosmetic treatments, and minimally invasive procedures is accelerating demand for high-quality sterile surgical gloves throughout the region.

For example, the growing utilization of sterile surgical gloves across expanding ambulatory surgical centers in Mexico, where outpatient surgical procedures and medical tourism activities continue to increase rapidly across urban healthcare facilities.

End user Industry Insights

Hospitals are projected to lead the market, capturing around 58% of the revenue share in 2026, driven by high patient volumes, continuous medical procedures, and stringent infection prevention requirements. Hospitals remain the largest consumers of both examination and surgical gloves because healthcare professionals require reliable protective equipment during diagnostics, surgeries, emergency treatments, and routine patient care activities. Rising incidences of chronic diseases and infectious conditions are contributing to higher hospital admissions and procedural frequencies, increasing overall glove utilization.

For instance, major multispecialty hospitals in Brazil are increasing procurement of disposable nitrile gloves to support infection control protocols and enhance patient safety during high-volume inpatient and outpatient medical procedures.

Ambulatory surgical centers are likely to be the fastest-growing application, increasing preference for outpatient care, shorter recovery times, and cost-efficient surgical treatments. These facilities require continuous supplies of disposable examination and surgical gloves to maintain sterile environments and support various minimally invasive procedures. Rising healthcare infrastructure development and increasing medical tourism activities across Latin America are significantly increasing the number of outpatient surgeries performed in specialized healthcare centers.

For example, the rapid expansion of outpatient surgical centers in Mexico, where increasing cosmetic and orthopedic procedures are driving strong demand for sterile disposable medical gloves across modern ambulatory healthcare facilities.

Country Insights

Brazil Medical Gloves Market Trends

Brazil is projected to lead the market, accounting for approximately 38% of the market share in 2026, largely driven by its extensive healthcare infrastructure, rising surgical procedures, and growing focus on infection prevention standards. Increasing hospitalization rates, expansion of private healthcare networks, and rising awareness regarding healthcare-associated infections are significantly supporting demand for examination and surgical gloves across the country. The market is witnessing a strong preference for nitrile and powder-free gloves because healthcare institutions are prioritizing safer and hypoallergenic protective solutions.

Government healthcare investments and modernization of hospital facilities are strengthening glove procurement activities throughout Brazil. The expansion of ambulatory surgical centers and diagnostic laboratories is also contributing to increasing glove consumption in both urban and semi-urban healthcare facilities. Growing medical tourism and cosmetic surgery procedures continue to support higher usage of sterile surgical gloves. A notable example includes Cardinal Health, Inc., strengthening the distribution of disposable medical products, including nitrile examination gloves.

Mexico Medical Gloves Market Trends

Mexico is likely to be the fastest-growing market in 2026, propelled by expanding healthcare access, rising outpatient procedures, and increasing industrial and healthcare safety awareness. The country benefits from strong trade connectivity with North America, which supports medical product imports, distribution, and manufacturing activities. Growing investments in hospital infrastructure and ambulatory healthcare facilities are increasing demand for high-quality examination and surgical gloves across public and private healthcare sectors. Nitrile gloves are gaining rapid adoption because healthcare providers increasingly prefer products offering enhanced durability, chemical resistance, and lower allergy risks.

Rising chronic disease prevalence and increasing surgical volumes are also contributing to long-term market expansion. Regulatory alignment with international medical safety standards is encouraging greater use of certified disposable gloves throughout healthcare facilities. For instance, Medline Industries is expanding its medical consumables distribution capabilities in Mexico to support growing demand for infection prevention products across hospitals, specialty clinics, and ambulatory surgical centers. Mexico is experiencing growing demand for disposable medical gloves from both healthcare and industrial sectors due to increasing workplace safety awareness and hygiene compliance standards.

Competitive Landscape

The Latin America medical gloves market exhibits a moderately fragmented structure, driven by the presence of international manufacturers, regional distributors, and expanding healthcare procurement networks across Brazil, Mexico, and Argentina. Rising demand for disposable examination and surgical gloves has encouraged global companies to strengthen their regional distribution partnerships and improve product availability throughout hospitals, specialty clinics, and ambulatory surgical centers. The market is witnessing increasing preference for nitrile and powder-free gloves due to enhanced durability, chemical resistance, and reduced allergy risks.

With key leaders including Top Glove Corporation Berhad, Hartalega Holdings Berhad, Cardinal Health, Inc., Medline Industries, and B. Braun Melsungen AG, the competitive environment continues to evolve through product innovation and regional expansion strategies. These players compete through advanced nitrile glove technologies, enhanced distribution capabilities, long-term healthcare supply agreements, product quality certifications, and broader portfolios of infection prevention solutions.

Key Industry Developments:

- In May 2026, Top Glove Corporation Berhad reported improving demand recovery and stronger pricing momentum in the global medical gloves industry, supported by rising nitrile glove demand, higher utilization rates, and increasing supply shifts from China to Malaysian manufacturers amid ongoing global trade adjustments.

- In May 2026, Supermax Corporation Berhad announced plans to invest approximately RM200 million in a new medical glove manufacturing facility in Brazil to strengthen its presence in the Latin American healthcare market and reduce regional dependence on imported gloves.

Companies Covered in Latin America Medical Gloves Market

- Top Glove Corporation Bhd

- Medline Industries

- Thermo Fisher Scientific Inc.

- Cardinal Health, Inc.

- B. Braun Melsungen AG

- SHOWA GROUP

- Owens & Minor, O&M Halyard

- Hartalega Holdings Berhad

- Safe Glove Co. Ltd.

- Supermax Corporation Berhad

Frequently Asked Questions

The Latin America medical gloves market is projected to reach US$511.6 million in 2026.

The Latin America medical gloves market is driven by rising surgical procedures, growing infection prevention awareness, expanding healthcare infrastructure, and increasing demand for disposable protective equipment across hospitals and clinics.

The Latin America medical gloves market is expected to grow at a CAGR of 6.9% from 2026 to 2033.

Key opportunities include the development of sustainable gloves, expanding nitrile glove adoption, growth in outpatient healthcare facilities, and increasing regional healthcare investments across Latin America.

Top Glove Corporation Berhad, Medline Industries, Thermo Fisher Scientific Inc., and Cardinal Health, Inc are the leading players.