- Bulk Chemicals

- India Lubricants Market

India Lubricants Market Size, Share, Trends, and Growth Forecast for 2025 - 2032

India Lubricants Market by Product Type (Industrial Lubricants, Automotive Lubricants, Marine Lubricants, Aerospace Lubricants), by End-use (Automotive, Heavy Equipment, Metallurgy and Metalworking, Power Generation), and Analysis for 2025 - 2032

India Lubricants Market Size and Trends Analysis

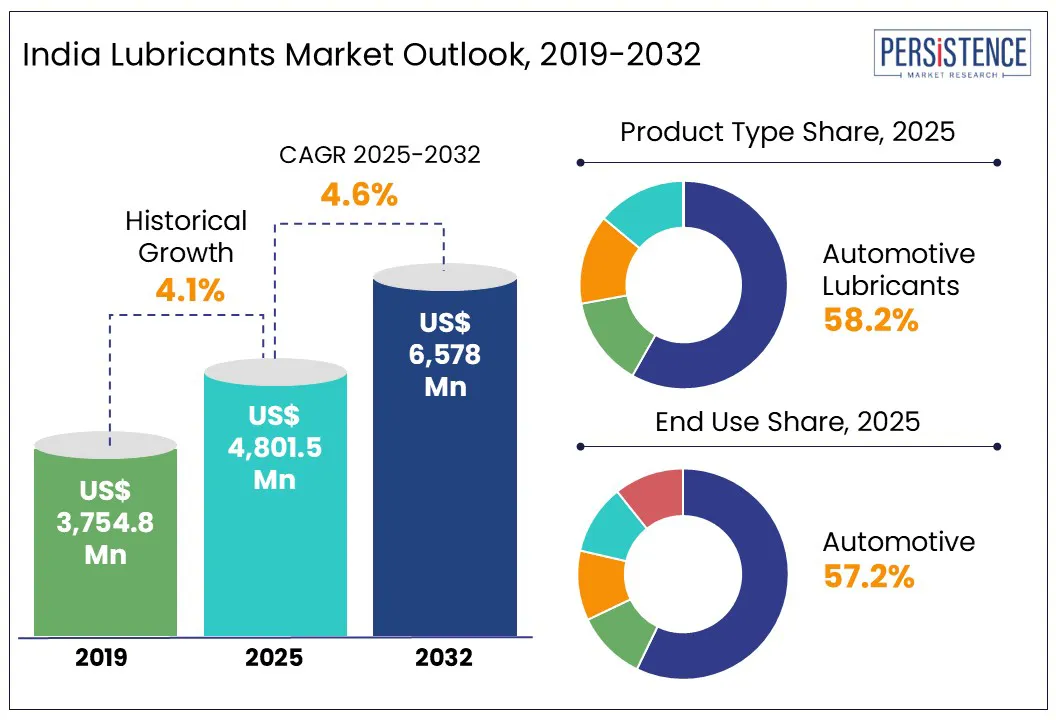

India lubricants market size is likely to be valued at US$ 4,801.5 Mn in 2025 and is estimated to reach US$ 6,578.0 Mn in 2032, growing at a CAGR of 4.6% during the forecast period 2025-2032.

India lubricants market is undergoing a dynamic transformation, pushed by evolving industrial demands, rapid automotive expansion, and a push toward sustainability. With the country poised to become the world’s third-largest energy consumer by 2030, the role of lubricants is becoming more important than ever. Yet, this evolving landscape is not just about volume, it is about innovation, regulation, and adaptability. As synthetic blends, bio-based alternatives, and application-specific formulations gain traction, the market is navigating a key inflection point, states a Persistence Market Research report.

Key Industry Highlights

- OEM-lubricant co-branding partnerships are anticipated to influence customer loyalty in the aftermarket.

- Inland waterways and coastal shipping projects are expected to unlock demand for marine-grade lubricants.

- Growth in mining activity across Jharkhand and Chhattisgarh is predicted to bolster demand for heavy-duty lubricants in East India.

- Rising consumer awareness about engine health and performance is speculated to augment demand for branded automotive coolants and lubricants.

- Automotive end-use segment will likely hold around 57.2% share in 2025 due to the unorganized service and repair ecosystem, which is pushing lubricant consumption in the aftermarket.

|

Market Attribute |

Key Insights |

|

India Lubricants Market Size (2025E) |

US$ 4,801.5 Mn |

|

Market Value Forecast (2032F) |

US$ 6,578.0 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

4.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.1% |

Market Dynamics

Driver - India’s cargo boom and maritime projects accelerate growth

The marine industry is significantly propelling India lubricants market growth amid increasing cargo traffic, port infrastructure expansion, and fleet modernization. According to India Brand Equity Foundation (IBEF), India’s 12 key ports handled 819.227 Mn tons of cargo in FY24, a 4.45% increase from 784.305 Mn tons in FY23. This surge has translated into high consumption of marine engine oils, cylinder oils, and trunk piston oils used in large diesel engines of bulk carriers, tankers, and container ships.

The Sagarmala Program and PM Gati Shakti have also accelerated the development of new ports and inland waterways. It is pushing demand for lubricants used in dredging vessels, tugboats, and barge fleets. The growth of India’s fishing industry is further contributing to marine lubricant consumption. Mechanized fishing trawlers and coastal surveillance vessels operated by agencies such as the Indian Coast Guard and state marine police are now key end-users of medium-speed diesel engine oils and gear oils.

Restraint - Poor storage practices and heat exposure hinder lubricant performance

The potential for lubricant degradation over time is a significant barrier to adoption in India. It is evident in price-sensitive and resource-constrained segments where end-users lack awareness or access to proper storage and maintenance protocols. In regions with high ambient temperatures and humidity, lubricants are often prone to oxidation, emulsification, and additive breakdown. Mineral-based lubricants, for example, stored improperly in open drums or exposed to direct sunlight degrade quickly. It leads to sludge formation and reduced viscosity, which compromises equipment performance and increases wear.

The issue is particularly evident among small-scale industries and transport fleet operators that often extend oil drain intervals beyond recommended cycles to cut costs. According to a 2023 online survey, approximately 37% of respondents in India’s SME segment admitted to reusing lubricants or delaying oil changes past OEM specifications. Such practices not only reduce engine efficiency but also increase long-term maintenance costs.

Opportunity - EV adoption and food safety norms create niche growth for bio-lubricants

The development of synthetic and bio-based lubricants in India is creating new opportunities for leading companies. Synthetic lubricants, primarily those made from polyalphaolefins and esters, are being adopted rapidly across both automotive and industrial sectors. This is because of their superior thermal stability, longer drain intervals, and fuel efficiency benefits. The shift toward synthetic lubricants is high in premium car segments, commercial vehicles running long hauls, and manufacturing units with high-load machinery.

Bio-based lubricants are emerging as an eco-conscious alternative, especially in applications where environmental contamination is a risk. India’s food-grade bio-lubricant segment, although niche, is showing strong traction. These lubricants are gaining relevance in food processing units, water-sensitive zones, and construction sites operating under green certification norms. The EV transition is another driver, as these vehicles require thermal management fluids and transmission oils that differ significantly from conventional ICE vehicles.

Category-wise Analysis

Product Type Insights

By product type, the market is segregated into industrial, automotive, marine, and aerospace lubricants. Among these, automotive lubricants are predicted to account for approximately 58.2% of share in 2025 due to the sharp rise in vehicle ownership across both urban and rural areas. The Ministry of Road Transport and Highways (MORTH) mentioned that India is home to 2.1 crore vehicles that are older than 20 years. This surge has broadened the addressable market for engine oils, transmission fluids, and coolants. It is evident in Tier 2 and Tier 3 cities where affordability and self-ownership of vehicles are increasing rapidly.

Aerospace lubricants, on the other hand, are expected to witness a steady growth rate through 2032 amid India’s expanding indigenous aerospace manufacturing and defense modernization programs. Hindustan Aeronautics Limited (HAL), the state-run aerospace behemoth, significantly increased its procurement of specialty lubricants between 2023 and 2024 for innovative fighter jet platforms. These platforms require high-performance synthetic oils and greases that can withstand extreme temperatures and pressures. It is further creating a high demand for products that meet MIL-SPEC and NATO standards.

End-use Insights

In terms of end-use, the market is divided into automotive, heavy equipment, metallurgy and metalworking, and power generation. Out of these, in 2025, the automotive segment is anticipated to hold nearly 57.2% of the India lubricants market share with the rapidly expanding vehicle base in India. It directly translates into recurring demand for engine oils, gear oils, brake fluids, and greases, specifically in the aftermarket segment. Two-wheelers require frequent oil changes, which has created a constant lubricant replacement cycle that dominates consumption patterns in both rural and urban India.

Heavy equipment is predicted to showcase a considerable CAGR from 2025 to 2032 due to the key role of lubricants in infrastructure, mining, and construction sectors, which operate in high-load, high-temperature environments. The mining industry significantly contributes to the demand for high-performance greases and synthetic oils that can withstand long operating hours and abrasive particulate exposure. Heavy construction equipment OEMs are increasingly offering branded lubricants as part of their annual maintenance contracts and extended warranty packages, further bolstering demand.

Regional Insights

East India Lubricants Market Trends

East India’s market is witnessing steady growth backed by infrastructure development, mining activities, and increased transportation across West Bengal, Jharkhand, and Odisha. The region’s industrial profile, rich in steel, coal, and aluminum production, makes it a significant zone for industrial lubricants, specifically for heavy machinery and hydraulic systems. Companies, including Indian Oil and Bharat Petroleum, maintain a strong presence due to their well-established dealer networks and ties with public sector enterprises operating in the mining and steel sectors.

Indian Oil, for example, has strategically improved its reach in Jharkhand and Odisha by collaborating with mining contractors and extending its Servo industrial product line. East India is also seeing rising demand for automotive lubricants due to increased two-wheeler and passenger car ownership. According to a 2024 report from Gulf Oil Lubricants, Tier 2 cities in West Bengal, such as Durgapur and Asansol, have shown a double-digit rise in automotive lubricant demand. Gulf Oil has been targeting mechanics and fleet owners in the region through loyalty programs and training workshops to enhance brand presence.

South India Lubricants Market Trends

South India’s market is characterized by a strong convergence of industrial and automotive demand, with Tamil Nadu and Karnataka leading the segment. This is because of their expansive manufacturing bases and dense vehicle population. Tamil Nadu, with its concentration of automobile and component manufacturing hubs, drives OEM-led and industrial lubricant consumption. Karnataka’s lubricant demand is bolstered by its booming logistics and IT corridor.

Bengaluru alone witnessed a 12% year-on-year growth in synthetic engine oil sales in FY 2023 to 2024, reveals a new study. It was pushed by the rising use of premium two-wheelers and a shift toward personal mobility. Telangana, despite its relatively smaller size, has become a lucrative labor pool due to its ongoing road-building projects and agriculture mechanization. Kerala presents a slightly different dynamic with its high urban density and service-oriented economy. The demand here skews toward personal mobility and marine lubricants due to its coastal geography.

West India Lubricants Market Trends

West India represents a mature yet evolving market for lubricants, with Maharashtra and Gujarat emerging as key consumption hubs. This is due to their industrial diversification and high vehicular density. Gujarat’s petrochemical and refining belt creates robust localized demand for industrial lubricants such as gear and compressor oils. Reliance’s Jamnagar refinery, one of the most prominent in the world, also acts as a production and export node for base oils, supporting the supply side of the market.

Maharashtra, especially the Mumbai-Pune-Nashik corridor, has become a significant automotive lubricants market in Western India. It is propelled by increasing personal vehicle ownership and the resurgence of on-road logistics post-COVID. As per a 2024 online survey, Maharashtra alone accounted for more than 13% of India’s total automotive lubricant consumption, led by SUV and two-wheeler segments. Castrol India, for instance, has intensified its presence in Pune’s aftermarket through partnerships with vehicle service chains such as GoMechanic and Pitstop to target tech-savvy urban users.

Competitive Landscape

The India lubricants market consists of several multinational giants and strong domestic players, each targeting different consumer bases. Indian Oil Corporation (IOC) dominates the space with its Servo brand, benefiting from its extensive retail and logistics infrastructure. Bharat Petroleum and Hindustan Petroleum follow closely with their respective brands Mak and Turbo. They are supported by state-owned loyalty in industrial and transportation segments. Private sector players such as Castrol India have strengthened their position in the automotive aftermarket through aggressive branding, premium product positioning, and deep penetration in mechanic workshops.

Key Industry Developments

- In June 2025, Chennai Corporation Limited announced the opening of its retail fuel outlets across India to mark its diamond jubilee year. It also launched new lubricants for specific industries.

- In May 2025, Daewoo introduced its high-performance lubricants in India, marking its entry into the country’s rapidly developing automotive lubricant sector. The company launched its premium range in collaboration with Mangali Industries Limited.

Companies Covered in India Lubricants Market

- Castrol Limited

- Bharat Petroleum Corporation Limited

- Indian Oil Corporation Ltd.

- Hindustan Petroleum Corporation Limited

- Savita Oil Technologies Ltd

- TIDE WATER OIL CO. (INDIA) LTD

- Valvoline Inc.

- Royal Dutch Shell Plc

- Exxon Mobil Corporation

- TotalEnergies SE

- Gulf Oil International

- Others

Frequently Asked Questions

The market is projected to reach US$ 4,801.5 Mn in 2025.

Rising vehicle ownership and port-led industrialization are the key market drivers.

The market is poised to witness a CAGR of 4.6% from 2025 to 2032.

Implementation of strict emission norms and the development of biodegradable lubricants are the key market opportunities.

Castrol Limited, Bharat Petroleum Corporation Limited, and Indian Oil Corporation Ltd. are a few key market players.