- Bulk Chemicals

- Thermal Conductive Polymers Market

Thermal Conductive Polymers Market Size, Growth, Share, Trends and Forecast, 2025 - 2032

Thermal Conductive Polymers Market by Product (Polyamide, Polycarbonate, Others), by End-use (Electrical & Electronics, Automotive, Others), and Regional Analysis for 2025 - 2032

Thermal Conductive Polymers Market Share and Trends Analysis

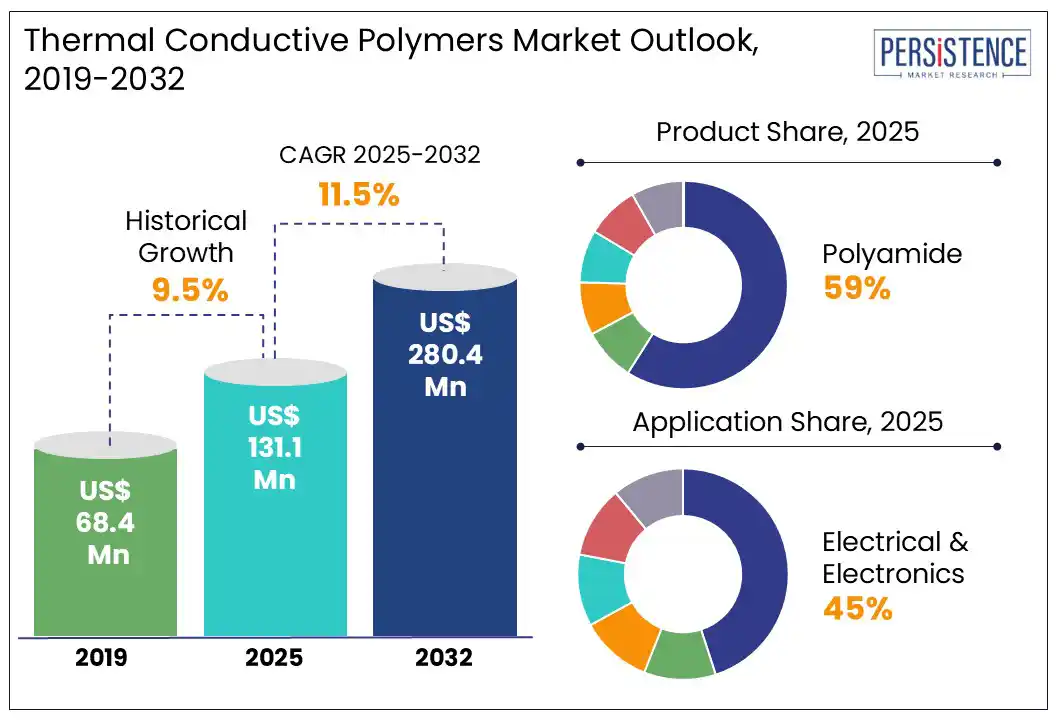

Global Thermal Conductive Polymers Market size is likely to be valued at US$ 131.1 mn in 2025 and is estimated to reach US$ 280.4 mn in 2032, at a CAGR of 11.5% during the forecast period 2025 – 2032.

According to the Persistence Market Research report, market growth is driven by the increasing demand for efficient heat dissipation in miniaturized electronics and EVs, substitution of metals with lightweight materials, and rising adoption in LEDs, 5G, and sustainable manufacturing.

Thermal conductive polymers are engineered plastic materials improved with conductive fillers such as metal particles, carbon-based materials (graphite, carbon black), or ceramic fillers (Aluminum Nitride (AlN), Aluminum Oxide (AlO), Boron Nitride (BN)), to significantly improve their ability to dissipate heat while retaining the processability and inherent lightness of common polymer materials. These materials are particularly useful in mechatronics and electronics, where compact design and dense component integration necessitate efficient thermal control. Depending on the fillers used, thermal conductivity can reach values up to 10–20 W/m·K, with ceramics providing electrical insulation and metals offering both thermal and electrical conductivity.

Key Industry Highlights

- Key drivers include the increasing demand for efficient heat dissipation in miniaturized electronics and EVs, substitution of metals with lightweight materials, and rising adoption in LEDs, 5G, and sustainable manufacturing.

- The polycarbonate segment is likely to experience the fastest growth due to its excellent combination of mechanical strength, dimensional stability, optical clarity, and inherent flame retardancy.

- The polyamide segment is expected to dominate the market due to its strong intermolecular hydrogen bonding that imparts excellent thermal & mechanical properties.

- North America is estimated to dominate the market in 2025, accounting for a market share of approximately 58% over the forecast period.

- Thermal conductive polymers combine heat dissipation, electrical insulation, and lightweight properties, making them increasingly important across electronics, automotive, and aerospace sectors.

|

Global Market Attribute |

Key Insights |

|

Thermal Conductive Polymers Market Size (2025E) |

US$ 131.1 Mn |

|

Market Value Forecast (2032F) |

US$ 280.4 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

11.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.5% |

Market Dynamics

Driver - Increasing demand in the EV sector

The transition of the automotive industry toward electric vehicles (EVs) is transforming the role of polymers in automotive engineering. Thermal conductive polymers are becoming vital in EV design as there is a high demand for lightweight materials that offer effective heat dissipation. Traditional polymers, with thermal conductivities around 0.2W/m·K, are inefficient compared to aluminum alloys (~150W/m·K), restricting their applications in thermal management, but can be rectified by incorporating filler-loaded composites.

Over 70% of plastics used in EVs are composed of just four polymers, Polyamide (PA), Polypropylene (PP), Polyurethane (PU), and PVC, which are not inherently thermally conductive polymers but can be made so for applications in EVs and electronics by incorporating special fillers or additives. PA, with a base conductivity of ~0.2 W/m·K, can be enhanced using ceramic or carbon fillers for battery cooling and electronic housings. Thermal conductive polymers play a major role in crucial components such as battery packs, enclosures, thermal interface materials (TIMs), phase change materials, motor potting compounds, and cooling channels, often incorporating fillers such as boron nitride to improve conductivity. Poor thermal management can compromise the performance, lifespan, and safety of EVs.

Restraints - Processing difficulties to hamper demand

Thermal conductive polymers present several processing challenges despite their importance in EVs and electronics. Achieving high thermal conductivity typically requires a high loading of conductive fillers such as boron nitride or graphite, which significantly increases melt viscosity and complicates extrusion, injection molding, and compounding processes. Uniform spreading of these fillers is essential to prevent thermal hotspots and maintain mechanical integrity but there is often poor compatibility between the polymer matrix and fillers. This often leads to high interfacial thermal resistance unless surface modification or coupling agents are employed.

Filler alignment during processing can also create anisotropic heat transfer properties, making it challenging to ensure steady thermal performance. High filler content can also reduce mechanical flexibility, leading to brittle composites that are difficult to shape into different forms. Additionally, abrasive fillers hasten tool wear, raising maintenance costs, while some fillers are sensitive to processing temperatures, limiting thermal processing options.

Opportunities - Innovations in thermal conductive polymer materials employed in electronics and EVs

Thermal conductive polymers combine heat dissipation, electrical insulation, and lightweight properties, making them vital across electronics, automotive, and aerospace sectors. In electronics, they replace bulky heat sinks in compact devices, serving as housings, connectors, and insulative layers, thereby improving both performance and reliability. In the automotive and aerospace industries, thermal conductive polymers enable efficient thermal management in battery housings, LED systems, and avionics, thereby reducing weight and enabling fuel efficiency. Advances in manufacturing, such as 3D printing and nanomaterial integration (graphene, carbon nanotubes), have further improved their capabilities. At the same time, sustainability is becoming vital, with research emphasizing recyclable, biodegradable, and natural-fiber-based composites.

Hybrid carbon Thermal Interface Materials (TIMs) embed carbon nanomaterials in a polymer matrix, lowering thermal resistance at the interface. This improves heat transfer from electronic components to heat sinks, thereby upgrading both device performance and reliability. These materials are essential in addressing the increasing thermal demands in high-performance computing, telecommunications, and automotive electronics. Nanomaterials such as boron nitride nanosheets (BNNS) have high thermal conductivity, electrical insulation, and thermal stability and when incorporated into TIMs, they enhance heat dissipation. These characteristics make BNNS-based TIMs suitable for futuristic applications such as smartphones, 5G systems, and EV power modules.

Category Wise Analysis

Product Type Insights

By product type, the polyamide segment is expected to dominate the market, holding approximately 59% of the market share during the forecast period. Their strong intermolecular hydrogen bonding imparts excellent thermal & mechanical properties. The two most common types used in packaging are PA-6 and PA-6,6. Both offer high melting points, heat resistance, flexibility, puncture resistance, thermal aging resistance, transparency, UV stability, and are excellent barriers to oxygen and many solvents. They are widely used in EVs and automotive components such as battery housings, heat sinks, and LED cooling systems; in electronics for connectors and enclosures; and in industrial applications such as motor potting and power electronics casings. Major manufacturers include Lanxess (Durethan TC), Celanese (Zytel), NUREL (Promyde®), Witcom, SABIC, BASF, and Covestro. Bio-based polyamide foams are gaining traction as eco-friendly solutions for building insulation and electrical insulation.

The polycarbonate (PC) segment is expected to experience the fastest growth over the forecast period, due to its excellent combination of mechanical strength, dimensional stability, optical clarity, and inherent flame retardancy. While unfilled polycarbonate has low thermal conductivity (~0.2 W/m·K), advanced composite formulations with thermal conductive fillers including boron nitride, graphite, or aluminum oxide can raise its conductivity to 1-10W/m·K, making thermal conductive PC ideal for LED lighting housings, battery casings, automotive sensors and electronic device enclosures, where flame retardancy and electrical insulation are critical. Innovations include multi-functional fillers to balance heat dissipation and 3D-printed conductive parts for customized thermal management solutions. Covestro has pioneered the use of thermal conductive (TC) polycarbonate, specifically Makrolon® TC8030, in automotive applications, integrating it into an LED fog lamp housing for a major light truck OEM.

End-use Insights

By end-use, the electrical & electronics segment is expected to dominate the market in 2025, accounting for around 45% over the forecast period, driven by the increasing demand for efficient heat management in compact devices. Thermal conductive polymers are used extensively in components such as connectors, circuit board housings, LED lighting fixtures, power modules, and TIMs. Their electrical insulation properties and enhanced thermal conductivity make them ideal for applications where both heat dissipation and electrical isolation are critical. Innovations such as filler hybridization (boron nitride with graphene) and filler alignment techniques further improve thermal performance while maintaining electrical insulation. Key manufacturers offering thermal conductive polymer compounds for electronics include Celanese (Zytel), Lanxess (Durethan TC grades), and NUREL (Promyde).

The automotive segment is anticipated to be the fastest-growing segment within this market, especially with the rise of EVs and advanced driver-assistance systems (ADAS) that require efficient thermal management. These polymers are increasingly used in battery housings, motor housings, heat sinks, LED headlamp cooling fins, and thermal interface materials to effectively dissipate heat, while reducing the overall vehicle weight. Compared to traditional metal components, thermal conductive polymers offer significant advantages such as weight savings (over 40%), corrosion resistance, electrical insulation, and design flexibility for integrated parts, which help improve vehicle efficiency and performance. Fortron® PPS is ideal for bearing blocks and mirror brackets due to its low thermal expansion and creep resistance across a wide temperature range. Hostaform® POM delivers excellent sliding performance for mirror adjustments.

Regional Insights

North America Thermal Conductive Polymers Market Trends

North America is estimated to dominate the market in 2025, accounting for a market share of approximately 58% over the forecast period, fueled by the rise of EVs, miniaturized electronics, and sustainability mandates. Key drivers include the integration of lightweight, thermally efficient materials in EV battery packs and powertrains and regulatory incentives that encourage the use of energy-efficient and recyclable materials. The Canadian Council of Ministers of the Environment (CCME) has developed rules for packaging, emphasizing waste reduction and resource conservation. Provinces, such as Ontario and British Columbia, have employed EPR programs for packaging materials, wanting businesses to take responsibility for recycling their packaging waste. Prominent market players include Celanese (CoolPoly® TCP series used in EV thermal management, LED housing, and HUD components) and DuPont (high-performance silicones for electronics thermal interfaces.

The U.S. thermal conductive polymers market is projected to grow substantially due to its dominant EV production, advanced electronics sector, and strong government incentives promoting clean energy solutions. The growth is fueled by the rising demand for lightweight, heat-dissipating materials in EV battery packs, power electronics, LED lighting, and smart devices. The U.S. Environmental Protection Agency (EPA) has been actively working towards reducing packaging waste and encouraging recycling through initiatives like the Sustainable Materials Management Program (SMM). which incentivizes sustainable material adoption in transportation and renewable energy sectors.

Europe Thermal Conductive Polymers Market Trends

Europe is expanding swiftly over the forecast period, driven by rising demand in automotive, electronics, aerospace, and industrial infrastructure applications. Key trends include the increased use of high-performance thermoplastics such as PPS, PA, and PC in EV battery modules, under-the-hood automobile parts, high-frequency electronics, and aerospace avionics systems. Europe is also at the forefront of sustainability and regulation, with growing emphasis on eco-friendly recyclable materials and energy efficiency. The EU’s Circular Economy Action Plan sets recycling and waste reduction targets. France has implemented regulations for eco-design and labeling for certain products, including packaging.

Germany is experiencing robust growth, propelled by its world-class automotive, electronics, and industrial manufacturing sectors. The major factors that drive the demand are automotive industry’s shift to lightweight thermal management materials for EVs, enhanced by strict emissions and sustainability regulations Germany introduced the Packaging Act, which focuses on waste prevention. Major applications include Lanxess’s thermal conductive polymers, such as Durethan BTC965FM30, in EV charge controllers and in Ensinger’s precision-engineered parts for automotive thermal systems.

Asia Pacific Thermal Conductive Polymers Market Trends

Asia Pacific is rapidly expanding, fueled by its massive electronics and EV manufacturing industries, along with strong infrastructure investments and supportive government policies Key market trends include the dominance of the polyamide segment, booming demand for thermal management in 5G telecommunications, aerospace, and medical imaging equipment. Covestro and Kaneka’s partnership on thermally conductive polycarbonate for electronics and SABIC’s LEXAN™ TC600 launch in 2022 are the major initiatives that will drive market growth in the region.

China is experiencing rapid growth, fueled by its dominance in electronics, EV production, and government-backed industrial innovation. Key trends include the shift toward sustainable and eco-friendly materials (biodegradable conductive polymers), extensive R&D in high-performance nanofillers, scaling up production capacity, and strong government incentives encouraging advanced material development. The Chinese government has set recycling targets, restricted the use of non-degradable packaging, and implemented a waste sorting system in major cities.

Competitive Landscape

The global thermal conductive polymers market is highly competitive with global and domestic players offering a wide range of products and competing for a higher market share. Companies are investing in R&D and adopting growth strategies such as product innovations, strategic partnerships, and acquisitions.

Key Industry Developments

- In March 2025, T-Global Technology introduced the new high-rebound and flexible thermal conductive gel TG-ASD35AB, which featured excellent thermal conductivity and long-term stability.

- In January 2025, during CES 2025, Covestro unveiled a cutting-edge digital design and simulation suite for its Makrolon® TC thermally conductive polycarbonates, marking a significant advancement in polymer-based heat management solutions.

Companies Covered in Thermal Conductive Polymers Market

- SABIC

- RTP Company

- Avient Corporation

- Celanese Corporation

- Covestro AG

- DSM

- MITSUBISHI ENGINEERING-PLASTICS CORPORATION

- HELLA GmbH & Co. KGaA

- TORAY INDUSTRIES, INC.

- DuPont

Frequently Asked Questions

The global market is projected to be valued at US$ 131.1 mn in 2025.

Key drivers include the increasing demand for efficient heat dissipation in miniaturized electronics and EVs, substitution of metals with lightweight materials, and rising adoption in LEDs, 5G, and sustainable manufacturing.

The market is poised to witness a CAGR of 11.5% from 2025 to 2032.

Thermal conductive polymers combine heat dissipation, electrical insulation, and lightweight properties, making them increasingly important across electronics, automotive, and aerospace sectors.

Major players in the global Thermal Conductive Polymers Market include SABIC, RTP Company, Avient Corporation, Celanese Corporation, and Covestro AG.