- Healthcare Services

- Antibody Drug Conjugates Contract Manufacturing Market

Antibody Drug Conjugates Contract Manufacturing Market Size, Share, and Growth Forecast 2026 - 2033

Antibody Drug Conjugates (ADC) Contract Manufacturing Market by Service Type (Antibody Production, Cytotoxic Payload (HPAPI) Manufacturing, Conjugation & Purification, Fill-Finish Services, Others), Development Stage (Preclinical, Phase I, Phase II, Commercial Manufacturing, Others), Therapeutic Application (Solid Tumors, Hematological Malignancies, Breast Cancer, Lymphoma, Others), and Regional Analysis, 20262033

Antibody Drug Conjugates Contract Manufacturing Market Size and Trend Analysis

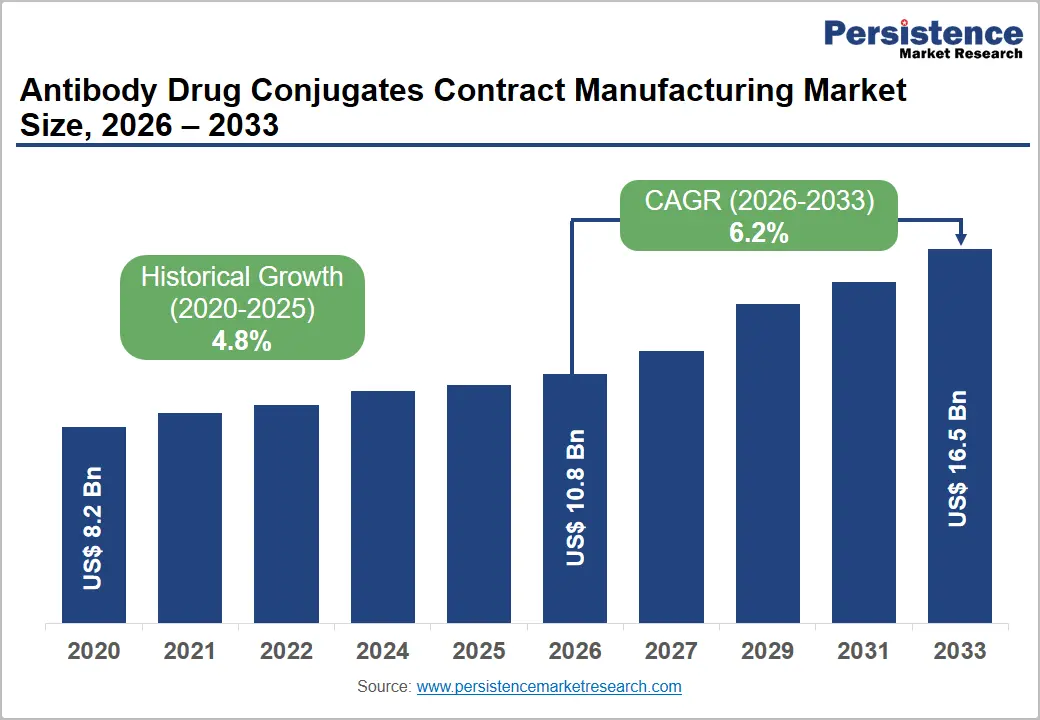

The global antibody drug conjugates contract manufacturing market size is expected to be valued at US$ 10.8 billion in 2026 and projected to reach US$ 16.5 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This robust growth is driven by the accelerating FDA and EMA approvals of ADC therapies, a deepening ADC clinical pipeline exceeding 100 molecules in active trials globally, and the inability of most pharmaceutical companies to manufacture the complex, highly toxic ADC molecules in-house, making contract manufacturing organizations (CMOs) and CDMOs the indispensable manufacturing backbone.

The FDA approved 14 ADCs for oncology indications as of 2024, with each commercial approval creating sustained long-term CDMO manufacturing contract demand. The specialized containment infrastructure required for cytotoxic HPAPI handling available at only a limited number of global CMO facilities, further reinforces the outsourcing imperative and supports premium pricing for ADC contract manufacturing services.

Key Industry Highlights

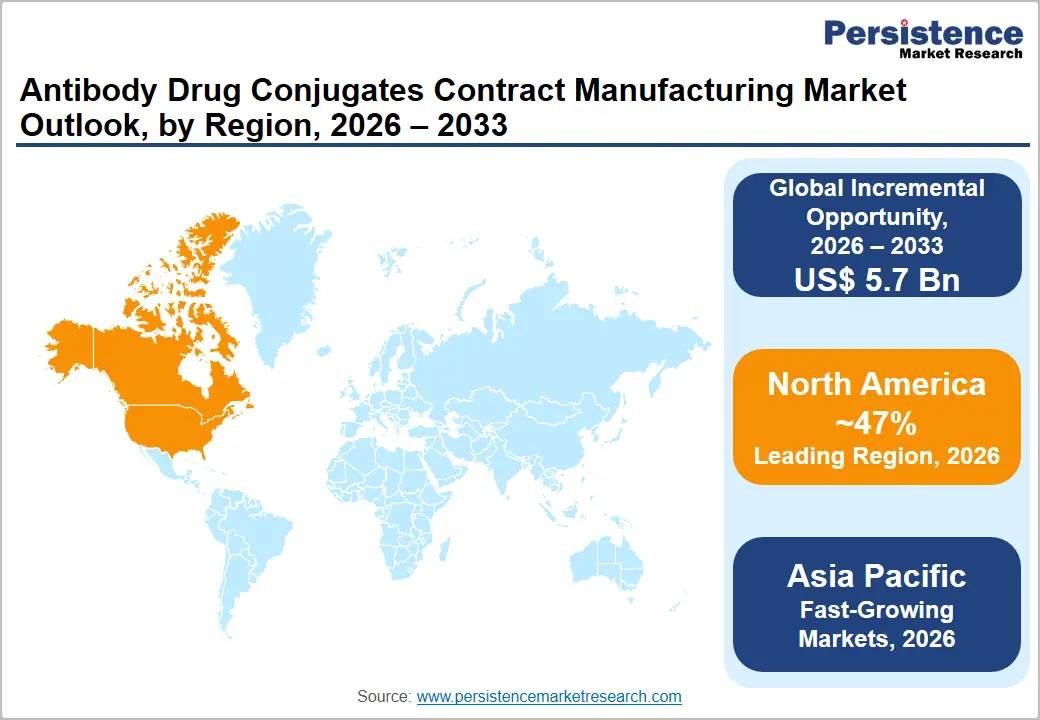

- Leading Region – North America: North America commands approximately 47% of the global Antibody drug conjugates contract manufacturing market in 2025, anchored by all 14 FDA-approved ADCs, the world's densest ADC development ecosystem, and CDMO leaders Lonza, Catalent, and Abzena operating major U.S. facilities.

- Fastest Growing Region – Asia Pacific: Asia Pacific is the fastest-growing ADC CDMO market in the forecast period, driven by WuXi Biologics' US$ 1B+ capacity investment, Samsung Biologics' Songdo ADC center, China's burgeoning domestic ADC pipeline, and India's Piramal Pharma Solutions expanding HPAPI and conjugation capabilities.

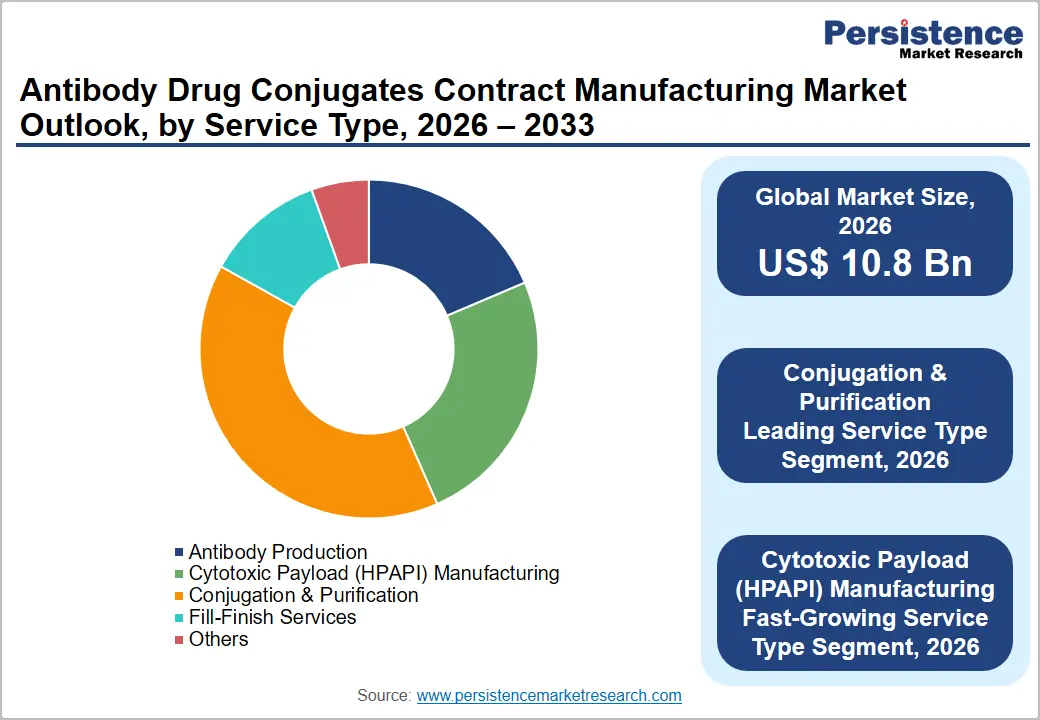

- Dominant Segment – Conjugation & Purification Services: Conjugation and purification services hold approximately 40% market share in 2026 the ADC process's highest-value step requiring specialized chemistry expertise, DAR characterization, and validated purification per FDA/EMA CMC regulatory requirements.

- Fast-Growing Segment – HPAPI Manufacturing: Cytotoxic HPAPI payload manufacturing is the fastest-growing service segment, driven by 150+ ADC clinical candidates requiring novel payload synthesis and the shift to next-generation topoisomerase I inhibitor payloads (DXd, SN-38) used in blockbusters Enhertu and Trodelvy.

- Key Opportunity – Asia Pacific Capacity Expansion and Supply Diversification: Supply chain diversification post-COVID and WuXi Biologics' >US$ 1 billion ADC capacity investment represents a structural opportunity for Asia Pacific CDMOs offering cost-competitive, FDA/EMA-qualified ADC manufacturing across antibody production, HPAPI synthesis, and fill-finish services.

Market Dynamics

Driver - Explosion in ADC Regulatory Approvals and Commercial Pipeline Driving CDMO Demand

The rapid pace of ADC regulatory approvals has transformed the landscape from a niche modality to a mainstream oncology treatment category, creating compounding demand for specialized contract manufacturing services. The FDA approved 14 ADC therapies as of 2024, including landmark approvals such as Enhertu (AstraZeneca/Daiichi Sankyo) for HER2-expressing cancers and Trodelvy (Gilead Sciences) for triple-negative breast cancer.

Each commercial ADC launch requires long-term, high-volume CDMO supply agreements spanning antibody production, HPAPI payload synthesis, conjugation, and fill-finish. Per ClinicalTrials.gov, over 150 ADC candidates are in active clinical trials globally, each representing a future CDMO contract pipeline. The Evaluate Pharma oncology drug pipeline database identifies ADCs as one of the fastest-growing drug classes by clinical stage volume, with Phase III completions expected to yield multiple additional approvals through 2033.

Structural Outsourcing Imperative Driven by HPAPI Containment Requirements

ADC manufacturing is among the most technically and regulatory complex processes in pharmaceutical manufacturing, requiring specialized high-potency API (HPAPI) handling infrastructure with occupational exposure limits (OELs) as low as nanograms per cubic meter. The majority of ADC payloads including auristatins (MMAE/MMAF), maytansinoids (DM1/DM4), and calicheamicins, are classified as Category 3 or 4 highly potent compounds under International Society for Pharmaceutical Engineering (ISPE) containment band guidelines. Building and validating dedicated HPAPI containment suites costs between US$ 50 million and US$ 200 million an investment that is economically justified only for CDMOs serving multiple clients. This capital barrier makes outsourcing the default manufacturing strategy for virtually all ADC developers, sustaining a structural, durable demand foundation for ADC CMOs through 2033.

Restraints - Limited Number of Qualified HPAPI-Capable CDMO Facilities Creating Supply Bottlenecks

Despite strong demand, the global supply of FDA- and EMA-qualified HPAPI-grade manufacturing facilities capable of full-service ADC production remains severely constrained. As of 2024, fewer than 30 CDMOs globally have the fully integrated capacity to handle all ADC manufacturing steps from cytotoxic payload synthesis through conjugation to sterile fill-finish. This supply constraint has created capacity queues of 12–24 months at leading CDMOs, delaying clinical timelines for ADC developers and creating execution risk for commercial supply chains, limiting the market's growth in proportion to pharmaceutical demand.

Complex Quality and Regulatory Compliance Burden Increasing CDMO Operating Costs

ADC manufacturing operates under the most stringent quality and regulatory frameworks in biopharmaceutical manufacturing, combining biologics cGMP requirements for the antibody component with chemical manufacturing controls for the cytotoxic payload and a highly controlled conjugation process. The FDA's guidance on combination products and the EMA's ADC-specific manufacturing guidelines impose extensive validation, analytical characterization, and stability testing requirements. Regulatory inspections at HPAPI-capable facilities have historically identified containment and process consistency gaps, resulting in warning letters and facility shutdowns that disrupt supply chains and impose significant remediation costs on CDMOs.

Opportunities - HPAPI Manufacturing Expansion: The Fastest-Growing Service Type Amid Surging Payload Demand

Cytotoxic HPAPI payload manufacturing is the fastest-growing ADC CDMO service segment, driven by the multiplying number of clinical-stage ADCs requiring novel or validated payload synthesis and the structural shortage of qualified HPAPI synthesis capacity globally. Each new ADC clinical program typically requires kilogram-scale payload synthesis at clinical stage and metric-ton scale upon commercialization creating compound capacity requirements per approval wave. CordenPharma International, Axplora (formerly Novasep), and Cerbios-Pharma have invested significantly in HPAPI synthesis capacity expansion. The shift toward next-generation ADC payloads including topoisomerase I inhibitors (DXd, SN-38) used in Enhertu and Trodelvy is creating demand for new custom payload synthesis capabilities beyond established auristatin/maytansinoid routes, representing a high-margin growth opportunity for specialized HPAPI CDMOs.

Asia Pacific CDMO Capacity Investment Creating Cost-Competitive Manufacturing Alternatives

Asia Pacific and particularly China, India, and South Korea is emerging as a strategically important ADC contract manufacturing geography, offering lower capital and labor costs relative to North America and Europe. WuXi Biologics has invested over US$ 1 billion in ADC-capable CDMO facilities in China and Ireland, positioning itself as the largest ADC CDMO globally by capacity. Samsung Biologics (South Korea) is rapidly adding ADC manufacturing capabilities to its expanding biopharmaceutical CDMO platform. For global pharma companies seeking supply chain diversification post-COVID-19, Asia Pacific CDMOs offer both cost efficiency and geographic manufacturing redundancy creating sustained demand for capacity expansion investment across the region through 2033.

Category-wise Analysis

Service Type Insights

Conjugation and purification services represent the leading service type segment in the Antibody drug conjugates contract manufacturing market, commanding approximately 40% of revenues in 2025. The conjugation step, where the cytotoxic payload is chemically linked to the antibody via a linker is the most technically differentiated, proprietary, and value-intensive step in the ADC manufacturing process. It requires specialized chemistry expertise, controlled conjugation environments (often inert atmosphere), advanced analytical tools for drug-antibody ratio (DAR) characterization, and validated purification workflows to achieve the narrow DAR distribution required for clinical and commercial ADCs. The FDA and EMA require extensive analytical package characterization of the conjugated product making this step the regulatory anchor of the ADC CMC package and sustaining its premium service pricing and revenue leadership.

Development Stage Insights

Commercial manufacturing represents the leading development stage segment in the Antibody drug conjugates contract manufacturing market, accounting for approximately 48% of revenues in 2025. Commercial ADC manufacturing contracts spanning multi-year supply agreements with defined volume commitments generate the highest revenue per engagement of any development stage category, due to the scale of antibody bioreactor batches, payload synthesis campaigns, and sterile fill-finish operations required. The 14 commercially approved ADCs as of 2024, each generating annual revenues ranging from US$ 200 million to US$ 3 billion+ (Enhertu surpassing US$ 2.6 billion in 2023 per AstraZeneca annual report) create long-term, recurring CDMO revenue streams that anchor the commercial manufacturing segment's revenue dominance.

Therapeutic Application Insights

Breast cancer is the leading therapeutic application segment in the Antibody drug conjugates contract manufacturing market, accounting for approximately 32% of revenues in 2026. This dominance is driven by the transformative commercial success of Enhertu (trastuzumab deruxtecan, AstraZeneca/Daiichi Sankyo) and Trodelvy (sacituzumab govitecan, Gilead Sciences) both blockbuster ADCs approved for HER2-positive and triple-negative breast cancer respectively. The American Cancer Society estimates approximately 310,000 new breast cancer diagnoses in the U.S. in 2024 making breast cancer the highest-incidence cancer in women globally. The large, well-characterized patient population, multiple validated ADC targets (HER2, TROP2), and robust clinical pipeline of breast cancer ADCs sustain the application's revenue leadership in the manufacturing market.

Regional Insights

North America Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

North America is likely to account for an estimated 47.2% share of the global antibody drug conjugates (ADC) contract manufacturing market in 2026, maintaining its position as the largest regional market. The region benefits from a highly mature biopharmaceutical ecosystem, extensive FDA experience in ADC approvals, and the presence of leading CDMOs with advanced high-potency manufacturing and bioconjugation capabilities.

Strong investment activity, expanding oncology pipelines, and increasing outsourcing by biotechnology companies continue to drive demand for specialized ADC manufacturing services. Growing adoption of next-generation ADC technologies, including site-specific conjugation and novel payload platforms, is further supporting capacity expansion across the region. Strategic collaborations between pharmaceutical companies and CDMOs are accelerating clinical development timelines while strengthening commercial manufacturing readiness.

U.S. Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

The U.S. accounted for approximately 89.1% of the North American ADC contract manufacturing market in 2026. Boston/Cambridge, the San Francisco Bay Area, and New Jersey remain major ADC development and outsourcing hubs, supported by leading CDMOs such as Lonza, Catalent, and Abzena. Strong FDA support for innovative oncology therapies and a robust ADC development pipeline continue to stimulate manufacturing demand. In June 2026, Biogen Inc. agreed to acquire RayThera Inc. in a transaction valued at up to US$1 billion, highlighting continued investment in advanced therapeutic development. The country's concentration of biotechnology innovators and commercial-stage ADC programs sustains demand for integrated development, conjugation, analytical testing, and fill-finish services.

Canada Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

Canada represented nearly 10.9% of the North American market in 2026. The country continues to strengthen its position through investments in biologics manufacturing infrastructure, oncology research, and GMP-compliant production facilities. Government-backed innovation initiatives and increasing partnerships between academic institutions and biotechnology companies are fostering ADC-related research activities.

Canadian organizations are also expanding capabilities in process development, analytical testing, and early-stage manufacturing support. As pharmaceutical companies seek diversified North American supply chains, Canada is increasingly viewed as a complementary destination for clinical-scale biologics and ADC manufacturing projects.

Europe Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

Europe accounted for approximately 29.1% of the global ADC contract manufacturing market in 2026, supported by advanced HPAPI manufacturing infrastructure, strong regulatory standards, and an established pharmaceutical industry. The region remains a major center for ADC process development, conjugation technologies, and commercial-scale production. Continued investments in pharmaceutical sovereignty, supply chain resilience, and advanced biologics manufacturing are encouraging capacity expansion across key European markets. The presence of globally recognized CDMOs and pharmaceutical companies further enhances Europe's competitiveness in ADC outsourcing. Growing oncology drug development activity and increasing demand for specialized manufacturing services continue to support regional market growth.

Germany Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

Germany is likely to account for an estimated 23.4% share of the European ADC contract manufacturing market in 2026. The country benefits from advanced engineering expertise, sophisticated containment technologies, and a strong chemical manufacturing base that supports linker and payload production. Leading companies such as CordenPharma continue to invest in specialized ADC manufacturing capabilities. Germany's well-developed pharmaceutical infrastructure and focus on process innovation make it an attractive location for both clinical and commercial ADC manufacturing projects. Increasing investments in high-potency production facilities are expected to further strengthen the country's role within the European ADC value chain.

Asia Pacific Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

Asia Pacific is poised to capture an estimated 20.3% share of the global market in 2026 and remains the fastest-expanding regional market. Growth is driven by increasing biologics manufacturing investments, competitive operating costs, and the rapid expansion of domestic ADC development pipelines across China, India, South Korea, and Japan. The region is witnessing substantial capacity additions in antibody production, HPAPI manufacturing, and conjugation services. Government support for biotechnology innovation, combined with increasing participation in global clinical development programs, is strengthening regional manufacturing capabilities. As pharmaceutical companies seek cost-efficient and diversified supply chains, Asia Pacific continues to attract both regional and international ADC outsourcing contracts.

China Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

China represented approximately 43.2% of the Asia Pacific ADC contract manufacturing market in 2026. Strong activity from domestic innovators such as RemeGen and Kelun Pharmaceutical is driving demand for integrated ADC development and manufacturing services. Companies including WuXi Biologics, continue expanding large-scale antibody and bioconjugation capabilities to support both domestic and international customers. Increasing licensing agreements between Chinese biotechnology firms and global pharmaceutical companies are accelerating manufacturing requirements. The country's expanding oncology pipeline and supportive biotechnology ecosystem position it as the largest ADC manufacturing hub within the Asia Pacific.

India Antibody Drug Conjugates Contract Manufacturing Market Trends and Insights

India accounted for nearly 19.3% of the Asia Pacific market in 2026. Competitive manufacturing costs, strong expertise in small-molecule synthesis, and growing investments in biologics infrastructure contribute to research and development initiatives in India. Companies such as Piramal Pharma Solutions are expanding HPAPI and ADC conjugation capabilities to address increasing global outsourcing demand. India's established pharmaceutical manufacturing ecosystem, combined with a skilled scientific workforce, supports efficient production of payloads, linkers, and antibody intermediates. Increasing participation in global biologics supply chains is strengthening India's role as a strategic destination for ADC contract manufacturing services.

Competitive Landscape

The global antibody drug conjugates contract manufacturing market is moderately consolidated, with Lonza Group, WuXi Biologics, Catalent, and Samsung Biologics collectively commanding over 45% of global revenues. Key differentiators include the breadth of integrated ADC services (antibody through fill-finish), HPAPI containment band capability, DAR analytical expertise, and FDA/EMA inspection track record. Emerging CDMOs Cerbios-Pharma, Axplora, Abzena compete on technical specialization and flexibility. Strategic M&A notably Danaher's acquisition of Cytiva and Revvity's ADC analytics investments, is reshaping capabilities. Platform technology licensing (linker-payload) and long-term commercial supply agreements are the dominant business models.

Key Developments:

- In October 2024, Simtra BioPharma Solutions, a leading CDMO focused on sterile injectable manufacturing, announced a US$14 million investment to expand its clinical-scale conjugation and purification capabilities for antibody-drug conjugates (ADCs). The investment strengthens the company’s ability to support early-stage ADC development and meet growing outsourcing demand from oncology-focused biopharmaceutical companies.

- In February 2024, Daiichi Sankyo announced an investment of nearly US$1 billion in its manufacturing facility in Germany to substantially increase antibody-drug conjugate production capacity. This expansion is intended to support rising global demand for its ADC portfolio and ensure long-term commercial supply for multiple oncology indications.

Global Antibody Drug Conjugates Contract Manufacturing Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 8.2 Bn |

|

Current Market Value (2026) |

US$ 10.8 Bn |

|

Projected Market Value (2033) |

US$ 16.5 Bn |

|

CAGR (2026-2033) |

6.2% |

|

Leading Region |

North America, 47% share |

|

Dominant Development Stage |

Commercial Manufacturing, 43.9% share |

|

Top-ranking Service Type |

Conjugation & Purification, 39.7% |

|

Incremental Opportunity |

US$ 5.7 Bn |

Companies Covered in Antibody Drug Conjugates Contract Manufacturing Market

- Sterling Pharma Solutions Limited

- Recipharm AB

- Lonza Group AG

- Catalent, Inc.

- WuXi Biologics (Cayman) Inc.

- Samsung Biologics Co., Ltd.

- Piramal Pharma Solutions

- AbbVie Contract Manufacturing (AbbVie Inc.)

- Merck KGaA

- Abzena

- AGC Biologics

- Cerbios-Pharma SA

- Axplora (Novasep CDMO)

- CordenPharma International GmbH

- Ajinomoto Bio-Pharma Services

- Others

Frequently Asked Questions

The global antibody drug conjugates contract manufacturing market is projected to be valued at US$ 10.8 billion in 2026, driven by 14 commercially approved ADC therapies as of 2024 (FDA), over 150 ADC candidates in active clinical trials (ClinicalTrials.gov), and the structural outsourcing imperative created by HPAPI containment requirements costing US$ 50–200 million per facility build making CDMOs the essential manufacturing partner for all ADC developers globally.

Growing ADC approvals, expanding oncology pipelines, increasing outsourcing of high-potency biologics manufacturing, and growing demand for specialized conjugation and containment capabilities are the primary demand drivers.

North America leads with approximately 47% market share in 2026, anchored by all 14 FDA-approved ADCs, the world's largest concentration of ADC clinical-stage developers in Boston/Cambridge and San Francisco Bay Area biopharma clusters, FDA Breakthrough Therapy Designations accelerating ADC development timelines, and major CDMO facilities operated by Lonza, Catalent, and Abzena.

Key opportunities lie in site-specific conjugation technologies, integrated end-to-end ADC manufacturing services, expansion of commercial-scale capacity in the Asia Pacific, and development of next-generation non-oncology ADCs.

The leading companies include Lonza Group AG (Visp ADC campus), WuXi Biologics (China/Ireland ADC facilities), Samsung Biologics (Songdo ADC center), Catalent, Inc., Abzena, Cerbios-Pharma SA, CordenPharma International, Axplora, Piramal Pharma Solutions, AGC Biologics, and Ajinomoto Bio-Pharma Services, collectively providing end-to-end ADC CDMO services from antibody production through sterile fill-finish.