ID: PMRREP4327| 198 Pages | 8 Jan 2026 | Format: PDF, Excel, PPT* | Consumer Goods

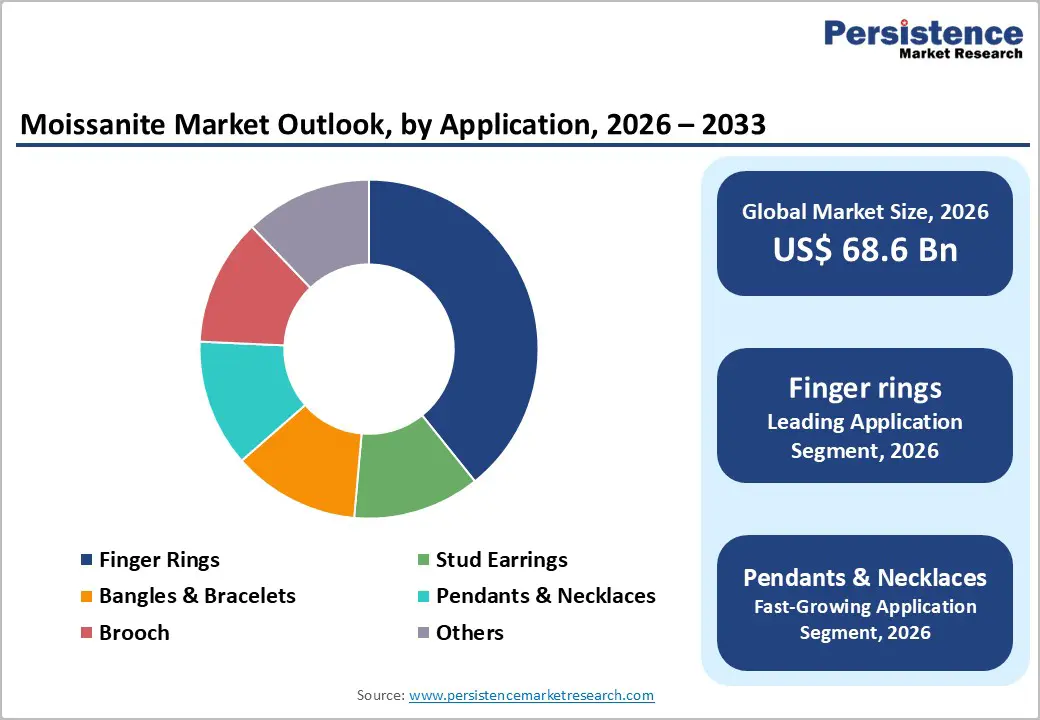

The global moissanite market is expected to be valued at US$ 68.6 billion in 2026 and projected to reach US$ 112.3 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033. Key drivers propelling this growth include the increasing demand for ethical and sustainable jewelry alternatives, rising consumer awareness about moissanite’s superior properties compared to diamonds, growing disposable incomes among millennial and Gen Z populations, and the expansion of e-commerce platforms facilitating direct-to-consumer sales.

The competitive pricing of moissanite compared to natural diamonds, coupled with technological advancements in production techniques enhancing gemstone quality, has positioned moissanite as a compelling choice for engagement rings, wedding bands, and fine jewelry.

| Global Market Attributes | Key Insights |

|---|---|

| Moissanite Market Size (2026E) | US$ 68.6 Billion |

| Market Value Forecast (2033F) | US$ 112.3 Billion |

| Projected Growth CAGR(2026-2033) | 7.3% |

| Historical Market Growth (2020-2025) | 7.9% |

Rising Ethical Consumerism and Sustainability Awareness

The global shift towards sustainable consumption patterns has become a primary catalyst for the moissanite market expansion. Modern consumers, particularly millennials and Gen Z, increasingly prioritize environmental impact and ethical sourcing in their purchasing decisions. Moissanite’s lab-created nature eliminates concerns associated with traditional diamond mining, including habitat destruction, water pollution, and carbon emissions. Unlike mined diamonds, moissanite production uses significantly less water and energy, resulting in a substantially smaller ecological footprint.

A substantial segment of consumers recognizes moissanite as a conflict-free gemstone, thereby avoiding the humanitarian concerns associated with diamond extraction. Studies indicate that approximately 65-70% of younger consumers actively seek sustainable luxury options, with moissanite directly addressing these evolving values. The environmental credentials of lab-grown moissanite have catalyzed partnerships between jewelry retailers and sustainability-focused brands, expanding market reach and reinforcing the gemstone’s position as the ethical alternative to mined diamonds. This consumer consciousness represents a fundamental market force that continues driving accelerated adoption across diverse geographic regions.

Technological Advancements and Production Quality Improvements

Significant innovations in synthetic moissanite production technologies have substantially enhanced product quality and market appeal. Advanced manufacturing techniques, including Chemical Vapor Deposition (CVD) and Physical Vapor Transport (PVT) methods, now enable the production of virtually flawless moissanite gemstones with exceptional clarity and brilliance. These technological breakthroughs have reduced production costs while improving visual properties that rival those of high-grade diamonds. Modern moissanite exhibits a higher refractive index, producing enhanced sparkle and fire compared to natural diamonds. The Lely process and improved flux-growth methods have enabled consistent, large-scale production of high-quality stones that meet stringent industry standards.

Manufacturers can now produce moissanite in diverse shapes and sizes, from intricate emerald cuts to cushion shapes, accommodating varied aesthetic preferences. Quality certifications from recognized gemological institutions enhance consumer confidence in product authenticity and value. These technological advances have democratized access to premium gemstones, making luxury jewelry affordable for broader market segments. Continued investments in production innovation position moissanite as an increasingly competitive alternative, combining beauty, durability, and ethical sourcing.

Intense Competition from Lab-Grown Diamonds and Price Pressures

Intensifying competition from lab-grown diamonds poses a major restraint on the moissanite market growth. Rapid capacity expansion and cost efficiencies have led to sustained price declines in lab-grown diamonds, narrowing the price gap with moissanite and weakening its affordability advantage. Many consumers perceive lab-grown diamonds as more authentic substitutes because of their chemical similarity to mined diamonds, thereby increasing substitution risk. This trend is particularly evident in fashion and bridal jewelry segments, where lab-grown diamonds are gaining share. Ongoing price erosion is also compressing margins across alternative gemstone categories. As a result, moissanite suppliers face growing pressure to defend positioning through differentiation rather than price. Continuous innovation in design, stronger branding, and greater emphasis on direct-to-consumer channels are increasingly necessary to sustain competitiveness.

Limited Consumer Awareness and Misconceptions Regarding Moissanite Properties

Limited consumer awareness remains a structural challenge for broader moissanite adoption. Many buyers lack understanding of moissanite’s optical performance, durability, and long-term wear characteristics, often defaulting to diamonds due to familiarity. Persistent misconceptions regarding authenticity and resilience reduce purchase confidence, particularly among older demographics and in less digitally connected markets. Awareness levels also vary significantly by region, creating uneven demand development. Established diamond marketing narratives continue to dominate consumer perception, overshadowing alternative gemstones. While education-focused selling approaches and digital comparison tools improve conversion rates, overall investment in consumer education remains inconsistent. Smaller market participants often lack resources to address these gaps effectively, constraining category-wide visibility and slowing adoption despite favorable product attributes.

Growth in Online Retail and Direct-to-Consumer Distribution Channels

The rapid expansion of e-commerce and direct-to-consumer models presents a major growth opportunity for the moissanite market. Online platforms offer broader product visibility, detailed pricing transparency, and wider customization options than traditional retail, enabling brands to reach global customers without geographic constraints. Digital-first sales models support competitive pricing by removing intermediary markups while preserving healthy margins. Advanced tools such as virtual try-ons, high-resolution imagery, and detailed certification information enhance buyer confidence and reduce purchase barriers. Social media–driven marketing, supported by influencers and user-generated content, significantly boosts engagement among younger consumers. Flexible payment options, easy returns, and the convenience of home-based purchasing further strengthen online channels as the primary growth engine for moissanite adoption through the forecast period.

Expanding Applications and Product Diversification Beyond Traditional Engagement Rings

Product diversification beyond engagement rings represents a key opportunity for sustained moissanite market expansion. Moissanite is increasingly used in earrings, bracelets, necklaces, pendants, and fashion jewelry, supported by its durability, brilliance, and affordability. Men’s jewelry and lifestyle-oriented segments are emerging growth areas, driven by demand for visually bold and customizable designs. Bridal offerings are also evolving to include coordinated sets, alternative metals, and personalized styling options. Suppliers are expanding moissanite availability across multiple product categories, enabling designers and retailers to innovate more freely. Customization enabled by advanced manufacturing techniques supports broader consumer appeal across age groups, reducing reliance on a single application segment.

Round-cut moissanite is the dominant shape category, commanding approximately 43% market share in 2025, driven by its timeless aesthetic appeal, exceptional brilliance, and universal consumer preference. The round brilliant cut, featuring optimal faceting geometry, maximizes moissanite’s inherent optical properties, producing unparalleled sparkle and fire that appeal to both traditional and contemporary consumers. This classic shape maintains consistent popularity across age groups, cultural regions, and income levels, positioning it as the foundational product offering for jewelry retailers worldwide. The psychological association of round cuts with engagement rings and formal occasions reinforces consumer preference, with market data consistently demonstrating round shapes as the fastest-moving inventory category.

Synthetic moissanite dominates market sourcing, capturing approximately 98% market share in 2025, establishing synthetic production as the industry standard. All commercially available moissanite is currently synthesized in laboratories, with natural moissanite remaining exceptionally rare and essentially unavailable in commercial markets. The synthetic production advantage stems from controlled manufacturing environments enabling consistent quality, absence of inclusions, and optimal clarity that exceed natural moissanite typically found in meteorite formations. Advanced CVD and PVT production methodologies have matured substantially, enabling scalable, cost-effective large-volume production while maintaining premium quality standards. Synthetic moissanite’s environmental credentials and ethical sourcing advantages align perfectly with contemporary consumer values, eliminating the need for mining-related infrastructure and associated ecological damage.

Finger rings, encompassing engagement rings and wedding bands, represent the leading application category, commanding approximately 37% market share in 2025, reflecting moissanite’s primary positioning as the diamond alternative for significant life milestones. Engagement ring demand continues accelerating, particularly among Gen Z and millennial consumers prioritizing affordability and ethical sourcing. Specialized ring designs incorporating moissanite include solitaire settings, halo configurations, three-stone designs, and elaborate vintage-inspired creations accommodating diverse aesthetic preferences. Wedding band markets show consistent growth as couples increasingly adopt coordinated moissanite jewelry sets.

The fastest-growing application segment comprises pendants and necklaces, projected to grow at an 8-9% CAGR through 2033, driven by adoption of fashion jewelry and increasing acceptance of moissanite beyond traditional engagement contexts. Pendant designs range from delicate solitaires to elaborate statement pieces, with customization enabling unique personal expression. Stud earrings and earring sets represent substantial growth opportunities, with transparent moissanite studs appealing to diverse consumer preferences for everyday, versatile jewelry. Bracelets, broaches, and specialty applications, including men’s jewelry, continue gaining traction, reflecting expanding moissanite positioning as a comprehensive fine jewelry solution.

Online retailers are the fastest-growing sales channel, projected to grow at a 9% CAGR through 2033, reflecting fundamental shifts in jewelry purchasing patterns and consumer preferences for digital shopping. E-commerce platforms provide unparalleled product selection, transparent price comparisons, detailed product specifications, and access to customer reviews that traditional retail cannot match. Online-exclusive brands including MoissaniteCo, Brilliant Earth, and specialized moissanite retailers have captured disproportionate market share through targeted digital marketing, social media engagement, and customer-centric service models.

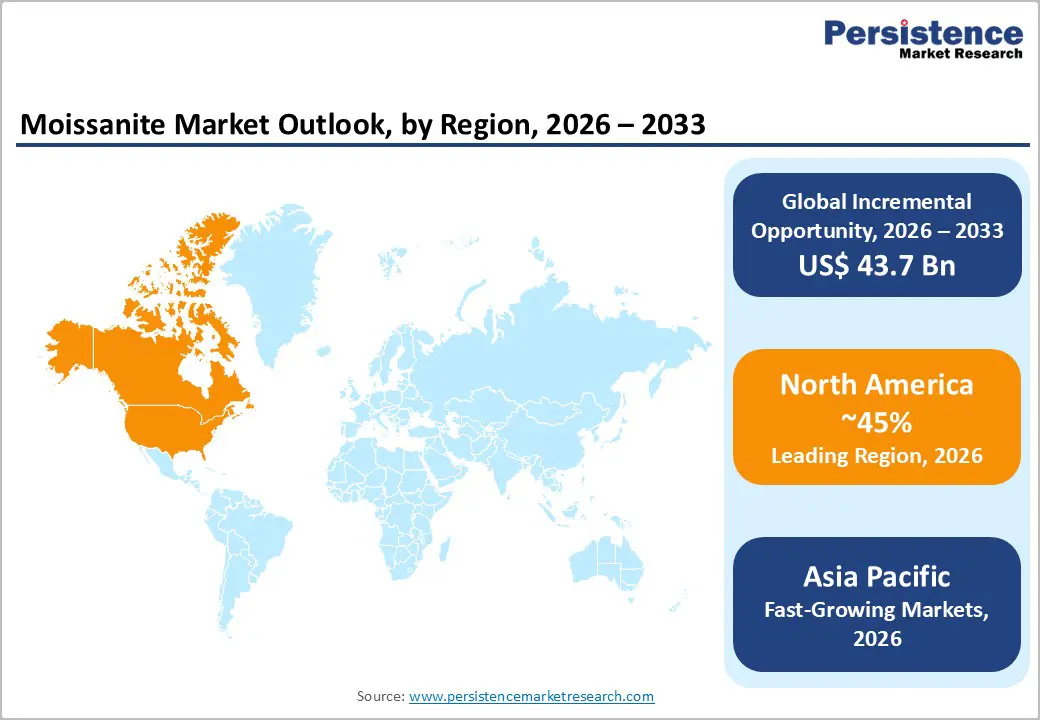

North America leads the global moissanite market, accounting for roughly 45% of total value in 2025, supported by high disposable incomes, advanced digital retail infrastructure, and strong consumer awareness of alternative gemstones. The United States represents the primary demand center, with urban regions driving adoption due to greater exposure to ethical jewelry trends and online purchasing channels. Younger consumers increasingly favor moissanite for engagement and fashion jewelry, valuing affordability, sustainability, and visual appeal.

A mature e-commerce ecosystem enables transparent pricing, product comparison, and nationwide accessibility, accelerating market penetration across income segments. Canada follows a similar trajectory, with rising environmental awareness and ethical consumption reinforcing demand. The region benefits from well-defined consumer protection regulations and gemstone certification practices, strengthening trust in moissanite products. Marketing strategies emphasizing environmental advantages and long-term value resonate strongly, while social media and influencer-driven promotion continue to expand visibility and acceptance among trend-oriented buyers.

Europe represents the second-largest regional market, driven by growing sustainability awareness and shifting attitudes toward traditional luxury jewelry. Demand is concentrated in the United Kingdom, Germany, France, and Spain, where ethical consumption increasingly influences purchasing decisions. Northern and Western European markets show strong acceptance of moissanite as a responsible gemstone alternative, supported by skepticism toward conventional diamond sourcing practices. Younger consumers, in particular, are redefining luxury by prioritizing transparency, environmental impact, and design originality.

The region benefits from harmonized regulations and standardized gemstone grading systems, which enhance cross-border consumer confidence. Online channels play a central role in market expansion, as European consumers are highly comfortable purchasing premium jewelry digitally. Fashion-oriented markets increasingly highlight moissanite’s brilliance and durability as aesthetic strengths rather than substitutes, while cross-border e-commerce within the European Union enables competitive pricing and wider product availability.

Asia Pacific is the fastest-growing moissanite market, projected to expand at a robust CAGR through 2033, supported by urbanization, rising middle-class incomes, and evolving jewelry preferences. The region serves as both a major production hub and an expanding consumer market, benefiting from cost-efficient manufacturing and advanced supply chains. Large metropolitan centers across East and South Asia are witnessing growing interest in moissanite jewelry among fashion-conscious and value-driven consumers.

Demand is supported by increasing bridal jewelry consumption, the westernization of engagement traditions, and heightened awareness of lab-created gemstones. E-commerce dominates jewelry retail across the region, particularly among younger buyers who favor digital discovery and price transparency. Social media platforms play a critical role in shaping preferences and accelerating adoption. Customization capabilities and region-specific design offerings further enhance market appeal, while competitive pricing strengthens Asia Pacific’s position in global trade.

The moissanite market is characterized by moderate consolidation, with a mix of established brands and emerging participants shaping a competitive yet accessible market structure. A limited number of large manufacturers and retailers control a significant share of global revenues, while numerous smaller players operate regionally or through online channels, supporting steady new entrant activity. Competition is increasingly driven by brand positioning, product quality, and design differentiation rather than price alone.

Market participants emphasize direct-to-consumer business models, leveraging digital platforms to improve margins, enhance customer engagement, and strengthen brand loyalty. Sustainability messaging and ethical sourcing credentials are widely used as strategic tools to align with evolving consumer preferences. Vertical integration across manufacturing, branding, and retail distribution provides cost efficiencies and supply control advantages. Additionally, customization capabilities, fast product innovation cycles, and investments in advanced production technologies are becoming critical strategies for maintaining competitiveness and avoiding commoditization within the market

The global moissanite market is projected to reach US$ 68.6 billion in 2026.

Key drivers include ethical sourcing preferences, improved product quality, affordability, and rising e-commerce adoption.

North America leads the market with about 45% share in 2025.

Online and direct-to-consumer retail expansion represents the main growth opportunity.

Major players include Charles & Colvard, Brilliant Earth, Stuller, MoissaniteCo, and Moissanite International.

| Report Attributes | Details |

|---|---|

| Historical Data/Actuals | 2020 – 2025 |

| Forecast Period | 2026 – 2033 |

| Market Analysis Units | Value: US$ Mn/Bn, Volume: As Applicable |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author